Schroder Australian Equities Quarterly Investment Option Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2021 Half Year Results Presentation 2 1H21 RESULTS PRESENTATION 15 April 2021

1H21 INVESTOR MATERIALS 15 April 2021 Half Year ended 28 February 2021 BANK OF QUEENSLAND LIMITED ABN 32 009 656 740. AFSL NO 244616. CONTENTS 1H21 RESULTS PRESENTATION 3 ABOUT BOQ 30 1H21 RESULTS 34 PORTFOLIO QUALITY 38 CAPITAL, FUNDING & LIQUIDITY 45 DIVISIONAL RESULTS 52 ECONOMIC ASSUMPTIONS 56 Bank of Queensland Limited 2021 Half Year Results Presentation 2 1H21 RESULTS PRESENTATION 15 April 2021 Half Year ended 28 February 2021 BANK OF QUEENSLAND LIMITED ABN 32 009 656 740. AFSL NO 244616. AGENDA INTRODUCTION Cherie Bell, General Manager Investor Relations RESULTS OVERVIEW George Frazis, Managing Director and CEO FINANCIAL DETAIL AND PORTFOLIO QUALITY Ewen Stafford, Chief Financial Officer and Chief Operating Officer SUMMARY & OUTLOOK George Frazis, Managing Director and CEO Q&A George Frazis, Managing Director and CEO Ewen Stafford, Chief Financial Officer and Chief Operating Officer Bank of Queensland Limited 2021 Half Year Results Presentation 4 RESULTS OVERVIEW GEORGE FRAZIS MANAGING DIRECTOR AND CEO 1H21 OVERVIEW 1. Statutory profit growth of 66%, cash net profit up 9%, and EPS growth of 3%1, reflecting strong growth whilst managing margin, costs and lower impairments 2. Good business momentum, with strong housing loan growth of 1.6x system and improved NIM to 1.95% 3. Delivering on the strategic transformation, over the last three halves, with go live of the first phase of the retail digital banking platform, and acquisition of ME Bank announced 4. Asset quality remains sound, reflected by loan impairment expense to GLAs reducing to 10bps and arrears reducing over the half. Prudent provision levels maintained 5. Capital strength to support business growth and transformation investment with CET1 of 10.03% 6. -

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021

Westpac Online Investment Loan Acceptable Securities List - Effective 3 September2021 ASX listed securities ASX Code Security Name LVR ASX Code Security Name LVR A2M The a2 Milk Company Limited 50% CIN Carlton Investments Limited 60% ABC Adelaide Brighton Limited 60% CIP Centuria Industrial REIT 50% ABP Abacus Property Group 60% CKF Collins Foods Limited 50% ADI APN Industria REIT 40% CL1 Class Limited 45% AEF Australian Ethical Investment Limited 40% CLW Charter Hall Long Wale Reit 60% AFG Australian Finance Group Limited 40% CMW Cromwell Group 60% AFI Australian Foundation Investment Co. Ltd 75% CNI Centuria Capital Group 50% AGG AngloGold Ashanti Limited 50% CNU Chorus Limited 60% AGL AGL Energy Limited 75% COF Centuria Office REIT 50% AIA Auckland International Airport Limited 60% COH Cochlear Limited 65% ALD Ampol Limited 70% COL Coles Group Limited 75% ALI Argo Global Listed Infrastructure Limited 60% CPU Computershare Limited 70% ALL Aristocrat Leisure Limited 60% CQE Charter Hall Education Trust 50% ALQ Als Limited 65% CQR Charter Hall Retail Reit 60% ALU Altium Limited 50% CSL CSL Limited 75% ALX Atlas Arteria 60% CSR CSR Limited 60% AMC Amcor Limited 75% CTD Corporate Travel Management Limited ** 40% AMH Amcil Limited 50% CUV Clinuvel Pharmaceuticals Limited 40% AMI Aurelia Metals Limited 35% CWN Crown Limited 60% AMP AMP Limited 60% CWNHB Crown Resorts Ltd Subordinated Notes II 60% AMPPA AMP Limited Cap Note Deferred Settlement 60% CWP Cedar Woods Properties Limited 45% AMPPB AMP Limited Capital Notes 2 60% CWY Cleanaway Waste -

Specialist Australian Small Companies Quarterly Investment Option Update

Specialist Australian Small Companies Quarterly Investment Option Update 31 December 2020 Aim and Strategy Sector Allocation % To provide a total return (income and capital growth) Consumer Discretionary 21.97 after costs and before tax, above the performance Materials 17.24 benchmark, the S&P/ASX Small Ordinaries Industrials 14.87 Accumulation Index, on a rolling three-year basis. The Health Care 9.90 portfolio invests in small companies listed on the Information Technology 8.64 Australian Securities Exchange (ASX). For this Financials 6.06 portfolio small companies are considered to be those Communication Services 5.61 outside the top 100 listed companies (by market Consumer Staples 5.50 value). Up to 20% of the portfolio may be invested in Real Estate 5.37 unlisted companies that the investment manager Cash 2.80 believes are likely to be listed in the next 12 months, or Energy 2.05 in companies between the top 50 and 100 listed on the ASX. Top Holdings % City Chic Collective Ltd 2.49 Investment Option Performance Lynas Rare Earths Ltd 2.43 To view the latest investment performances for each Eagers Automotive Ltd 2.07 product, please visit www.amp.com.au/performance Integral Diagnostics Ltd 2.04 Marley Spoon AG 1.89 Investment Option Overview Technology One Ltd 1.85 Investment category Australian Shares Pilbara Minerals Ltd 1.84 Suggested minimum investment Seven Group Holdings Ltd 1.83 7 years timeframe Ingenia Communities Group 1.78 Relative risk rating Very High Auckland International Airport 1.75 Investment style Active Manager style Multi-manager Asset Allocation Benchmark (%) Australian Shares 100 Cash 0 Actual Allocation % International Shares 11.61 Australian Shares 82.23 Listed Property and Infrastructure 3.36 Cash 2.80 Fund Performance The Fund posted a very strong positive absolute return and outperformed its benchmark over the December quarter. -

Of the Corporations Act, AMP Limited Advises Its Current Interest in Shares of AMP Ltd

Company Secretary AMP Limited ABN: 49 079 354 519 33 Alfred Street Sydney NSW 2000 Australia GPO Box 4134 Sydney NSW 2001 Australia Email: [email protected] Web: amp.com.au Telephone: (02) 9257 5000 Facsimile: (02) 9257 7178 19-August-2021 Manager ASX Market Announcements Australian Securities Exchange Level 4, 20 Bridge Street Sydney NSW 2000 Notice Pursuant to Corporations Act Sub-section 259C(2) Exemption Dear Sir/Madam, Pursuant to an exemption under Sub-section 259C(2) of the Corporations Act, AMP Limited advises its current interest in shares of AMP Ltd. Marissa Bendyk Company Secretary, AMP Limited AMP Ltd ABN 49 079 354 519 Corporations Act 2001 Subsection 259C(2) Exemption To: AMP Ltd ACN/ARSN: 079 354 519 Shareholder: AMP Limited (ACN 079 354 519) and its related bodies corporate. Notice Date: 18-Aug-2021 1. Previous Notice Particulars of the shareholders' previous notice under sub-section 259C(2) exemption was given on: The previous notice was given to the company on: 05-Aug-2021 The previous notice was dated: 04-Aug-2021 2. Previous and present voting power The total number and percentage of shares in each class of voting shares in the company to which the shareholder has an interest in or derivative exposure to, when last required and when now required to give notice, are: Previous Notice Present Notice Class of securities Persons' votes Voting Power Persons' votes Voting Power Ordinary Share 53,430,902 1.64% 53,595,691 1.64% 3. Change in interest and derivative exposure Particulars of each change in, or change in the nature of, the interests of the substantial holder in, or derivative exposure to voting shares since the shareholder was last required to give a notice are: See Annexure 'A' 4. -

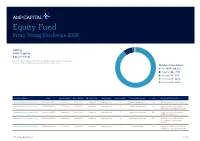

Equity Fund Proxy Voting Disclosure 2020

Equity Fund Proxy Voting Disclosure 2020 Voting AMP Capital Equity Fund Note: The below disclosures refer to Australian listed securities only and do not include foreign listed securities held in the portfolio. Number of resolutions: n For 1077 - 90.2% n Against 88 - 7.3% n Abstain 18 - 1.5% n Unvoted 8 – 0.7% n Unvoted 3 – 0.3% Company Name ISIN Meeting Date Record Date Meeting Type Proponent Proposal No. Type of Proposal Vote Proposal Description Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 1 Capital Management For Ratify Placement of Securities Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 2 Capital Management For Approve Issue of Securities (Executive chair Bill Beament) Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 3 Capital Management For Approve Issue of Securities (NED Mary Hackett) Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 4 Capital Management For Approve Issue of Securities (Former NED Christopher Rowe) Northern Star Resources Ltd AU000000NST8 1/22/2020 1/20/2020 Ordinary Management 5 Board Related For Approve Financial Assistance (Kalgoorlie Lake View Pty Ltd) AMP Capital Equity Fund 1 of 58 Company Name ISIN Meeting Date Record Date Meeting Type Proponent Proposal No. Type of Proposal Vote Proposal Description Virgin Money UK Plc. AU0000064966 1/29/2020 1/24/2020 Annual Management 1 Audit/Financials For Accounts and Reports Virgin Money UK Plc. AU0000064966 1/29/2020 1/24/2020 Annual Management 2 Compensation For Remuneration Policy (Binding) Virgin Money UK Plc. -

AMP17367 Reviewvis 27.Indd

2013 shareholder review Dividends Dividend cents per share The fi nal dividend of Final dividend 11.5 cents per share will Interim dividend be paid on 10 April 2014. The fi nal dividend will be 30 30 70% franked and brings 30 29 the total dividend for 2013 25 16 15 to 23 cents per share. 14 23 The payout ratio for the 20 12.5 full 2013 dividend is 80% 11.5 of the 2013 underlying profi t, which is at the 15 15 top of AMP’s target payout 10 14 range of 70–80% of 12.5 underlying profi t. 11.5 0 2009 2010 2011 2012 2013 Annual general meeting AMP’s 2014 annual general meeting (AGM) will be held at 10.00am (AEST) on Thursday 8 May 2014 at the Savoy Ballroom, Grand Hyatt Melbourne, 123 Collins Street, Melbourne, Australia. Full details of the 2014 AGM, including the notice of meeting and a link to the live webcast, are available at amp.com.au/agm. AMP 2013 annual report The full AMP 2013 annual report, including the complete fi nancial report, can be found at amp.com.au/2013annualreport. AMP Limited ABN 49 079 354 519. Unless otherwise specified, all amounts are in Australian dollars. Information in the review is current as at 3 March 2014. AMP was founded on a simple yet bold idea – that every individual should have the power and ability to control his or her life. For more than 160 years, we’ve dedicated ourselves to making this possible. And while we’ve grown and changed over the decades, one thing has remained the same – our unwavering sense of purpose to help people own tomorrow. -

Australian Listed Equities: Weekly Share Market Wrap

Australian Listed Equities: Weekly Share Market Wrap Total Shareholder Returns as at 04 December 2020 Price 1 week 1 month 6 months 1 year 2 years 3 years 5 years 10 years 10 years Ticker Stock Name $ % % % % % p.a. % p.a. % p.a. % p.a. ranking A2M The A2 Milk Company 13.48 -3.02 2.04 -24.57 -5.73 13.14 21.69 66.61 - - ABC Adelaide Brighton 3.23 2.22 3.19 -2.46 -0.08 -18.14 -17.52 -1.18 4.55 98 ABP Abacus Property Grp 3.15 -0.63 6.42 21.82 -10.83 4.23 -3.52 6.74 8.37 69 AFI Australian Foundat 7.22 -0.82 8.41 17.95 9.38 13.38 9.55 8.04 7.01 75 AGL AGL Energy Limited 13.52 -1.46 5.54 -20.24 -27.72 -9.15 -12.47 1.87 3.88 102 AIA Auckland Internation 7.32 -0.41 8.77 11.76 -12.65 5.08 9.74 10.98 18.12 22 ALD Ampol Limited 30.77 0.46 21.00 9.73 -8.08 8.66 -1.78 0.93 10.77 56 ALL Aristocrat Leisure 31.84 -3.74 3.67 17.51 -3.91 17.25 14.09 28.04 29.23 7 ALQ ALS Limited 9.52 -2.36 -0.98 31.69 7.40 14.26 14.25 21.73 5.54 90 ALU Altium Limited 35.72 2.09 -5.53 -1.48 2.44 24.33 41.36 50.26 71.58 1 ALX Atlas Arteria 6.48 -1.22 8.91 -2.66 -11.90 3.02 5.85 12.80 18.17 21 AMC Amcor PLC 15.34 -0.84 0.16 3.68 8.49 11.97 3.36 6.80 13.24 39 AMP AMP Limited 1.72 -1.15 3.30 2.84 0.04 -12.32 -25.31 -14.07 -2.03 121 ANN Ansell Limited 35.68 -5.06 -14.07 0.81 26.57 27.11 14.59 12.75 11.78 48 ANZ ANZ Banking Grp Ltd 23.30 0.91 22.54 24.41 -1.20 -1.64 -1.47 2.25 5.11 94 APA APA Group 10.18 -3.69 -6.86 -9.84 -0.47 13.21 7.59 8.16 14.00 36 APE AP Eagers Limited 13.25 -0.53 14.13 81.51 37.33 41.67 21.54 5.80 20.09 20 APT Afterpay Touch 94.50 -0.21 -6.20 81.03 224.97 -

Boral Reviews Its Cost Base and Completes an Organisational

ASX / MEDIA STATEMENT 20 May 2015 Boral Chairman Dr Bob Every AO to step down following Boral AGM and Dr Brian Clark to become Chairman Boral Limited (ASX: BLD) announced today that Dr Bob Every AO will step down from the Boral Limited Board, after eight years as a Director and five years as Chairman, at the conclusion of Boral’s Annual General Meeting to be held on Thursday 5 November 2015. Boral also announced that Dr Brian Clark will become the Chairman of Boral Limited at the conclusion of Boral’s 2015 AGM in November. Brian joined the Board of Boral in May 2007 and has been a member of the Remuneration & Nomination Committee since then and Chairman of that Committee since 2009. He is a Director of AMP Limited and Chairman of AMP Capital Limited, and he has experience as an executive and director in Australasia, Japan, China, Italy, the UK and South Africa. Bob said: “I am delighted that Brian has agreed to succeed me as Chairman of Boral following this year’s AGM. Brian has had an outstanding career as an executive with extensive international experience. He is also a very experienced director and is well positioned to chair the Company through the next phase of its Fix, Execute & Transform program. “Succession planning has been an important focus for the Board and I am confident that the Company and the Board will be in very capable hands under Brian’s Chairmanship.” Brian added: “I am looking forward to moving into the role of Boral’s Chairman following the Annual General Meeting, and I will be working closely with Bob over the coming months to ensure an orderly transition. -

Morningstar Equity Research Coverage

December 2019 Equity Research Coverage Morningstar covers more than 200 companies in We use the following guidelines to Contact Details Australia and New Zealand as part of our global determine our Australian equity coverage: Australia stock coverage of about 1,500 companies. We are × Nearly all companies in the S&P/ASX 100 Index. Helpdesk: +61 2 9276 4446 Email: [email protected] one of the largest research teams globally with × Companies in the S&P/ASX 200 Index which more than 100 analysts, associates, and have an economic moat and/or have cash flow New Zealand strategists, including 17 in Australia. Local analysts which is at least mildly predictable. Helpdesk: +64 9 915 6770 regularly glean insights from our global sector teams × In total, Morningstar will cover about 80% of Email: [email protected] in China, Europe, and the United States, enriching S&P/ASX 200 companies (which typically the process and enhancing outcomes for investors. equates to about 95% of S&P/ASX 200 by Our research philosophy focuses on bottom-up market capitalisation). Companies we choose analysis, developing differentiated and deep not to cover in this index are usually unattractive opinions on competitive forces, growth prospects, for most portfolios, in our opinion. and valuations for every company we cover. We × About 30 ex-S&P/ASX 200 stocks are selected publish on each company under coverage at least on Morningstar’s judgement of each security's quarterly, and as events demand, to ensure investment merit − which includes a very investment ideas are always relevant. strong lean towards high-quality companies We are an independent research house, and with sustainable competitive advantages, or therefore determine our coverage universe based economic moats. -

ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 18Th December 2017

et6 ASX CLEAR – ACCEPTABLE COLLATERAL LIST Effective from 18th December 2017 APPROVED SECURITIES AND COVER Subject to approval and on such conditions as ASX Clear may determine from time to time, the following may be provided in respect of margin: Cover provided in Instrument Approved Cover Valuation Haircut respect of Initial Margin Cash Cover AUD Cash N/A Additional Initial Margin Specific Cover N/A Cash S&P/ASX 200 Securities Tiered Initial Margin Equities ETFs Tiered Notes to the table . All securities in the table are classified as Unrestricted (accepted as general Collateral and specific cover); . Specific cover only securities are not included in the table. Any securities is acceptable as specific cover, with the exception of ASX securities as well as Participant issued or Parent/associated entity issued securities lodged against a House Account; . Haircut refers to the percentage discount applied to the market value of securities during collateral valuation. ASX CODE SECURITY NAME HAIRCUT A2M The A2 Milk Company Limited 30% AAA Betashares Australian High Interest Cash ETF 15% AAC Australian Agricultural Company Limited 30% AAD Ardent Leisure Group 30% ABC Adelaide Brighton Limited 30% ABP Abacus Property Group 30% ACX Aconex Limited 30% AGL AGL Energy Limited 20% AHG Automotive Holdings Group Limited 30% AHY Asaleo Care Limited 30% ALL Aristocrat Leisure Limited 30% ALQ ALS Limited 30% ALU Altium Limited 30% AMC Amcor Limited 15% AMP AMP Limited 20% © 2018 ASX Limited ABN 98 008 624 691 1/7 ASX CODE SECURITY NAME HAIRCUT ANN Ansell -

Australian Listed Equities: Weekly Share Market Wrap

Australian Listed Equities: Weekly Share Market Wrap Total Shareholder Returns as at 19 May 2017 Price 1 week 1 month 6 months 1 year 2 years 3 years 5 years 10 years 10 years Ticker Stock Name $ % % % % % p.a. % p.a. % p.a. % p.a. ranking A2M The A2 Milk Company 3.27 0.31 9.36 62.69 125.52 158.33 - - - - ABC Adelaide Brighton 5.61 -2.94 0.54 10.95 8.19 16.12 18.37 17.52 7.59 37 ABP Abacus Property Group 3.42 0.89 0.29 27.08 11.22 14.30 17.39 17.37 -4.79 111 AFI Australian Foundation 5.80 -1.53 0.52 2.97 7.09 0.40 3.45 10.62 3.45 67 AGL AGL Energy Limited 26.57 -2.06 -3.14 34.43 48.18 37.31 23.60 16.71 8.17 34 AIA Auckland Internation 6.37 -0.62 0.00 8.07 9.13 24.60 22.20 28.64 11.99 20 AIZ Air New Zealand 2.66 2.70 13.68 46.06 51.17 11.77 23.93 40.03 5.16 53 ALL Aristocrat Leisure 20.20 2.28 6.32 38.91 64.79 63.22 61.32 48.77 3.74 63 ALQ ALS Limited 5.81 -8.36 -7.78 -6.46 40.74 4.10 -3.39 -7.38 6.12 49 AMC Amcor Limited 15.00 -1.77 -1.32 6.91 -4.77 7.76 16.88 20.78 11.42 23 AMP AMP Limited 5.08 -3.61 -2.31 10.36 -2.37 -5.31 4.30 10.46 -2.30 103 ANN Ansell Limited 24.18 -0.45 4.13 10.86 33.44 -0.94 12.31 12.86 8.78 33 ANZ ANZ Banking Grp Ltd 28.50 -2.46 -5.97 4.72 20.84 -0.23 1.01 12.12 3.80 62 AOG Aveo Group 3.30 0.00 5.43 6.11 2.11 12.92 19.57 8.48 -13.15 122 APA APA Group 9.35 -0.85 3.09 27.40 8.91 7.53 17.29 18.72 12.16 18 APE AP Eagers Limited 7.95 1.92 -8.20 -11.20 -19.96 -3.78 18.44 25.11 14.35 13 ARG Argo Investments 7.61 -1.42 0.13 6.16 9.93 1.56 5.27 12.21 2.40 76 AST AusNet Services Ltd 1.75 0.86 4.48 21.63 14.27 14.32 13.81 -

AMP Capital Corporate Bond Quarterly Investment Option Update

AMP Capital Corporate Bond Quarterly Investment Option Update 31 March 2021 Aim and Strategy Actual Allocation % To deliver to investors regular monthly income (which International Fixed Interest 3.35 exceeds the income from term deposits and Australian Fixed Interest 93.55 government bonds) whilst seeking to provide capital stability to investors over the medium term. The Cash 3.10 portfolio also seeks provide total returns (primarily Sector Allocation % income with some capital growth) above the Bloomberg AusBond Bank Bill Index over a rolling Investment Grade Corporate 81.50 three-year basis. The option invests in an actively Agency MBS 10.96 managed portfolio of corporate bonds , primarily on Cash 4.69 investment grade rated corporate bonds in the High-Yield Corporate 3.05 Australian market and also has exposure to global ABS (Non-Mortgage) 1.23 bond markets. Exposure to global credit securities will Government Agencies/Regionals 0.17 principally be hedged back to Australian dollars. Top Holdings % National Australia Bank Ltd 3.50 Investment Option Performance Australia & New Zealand Banking Group 3.30 To view the latest investment performances for each Ltd product, please visit www.amp.com.au/performance Westpac Banking Corp 2.99 COMMONWEALTH BANK AUST 2.65 Investment Option Overview Sumitomo Mitsui Financial Grou 2.33 Investment category Australian Fixed Banco Santander SA 2.29 Interest BPCE SA 2.27 Suggested minimum investment 3 years Qantas Airways Ltd 2.25 timeframe BANK OF MONTREAL 2.21 Relative risk rating Medium to High TORONTO-DOMINION BANK 1.85 Investment style Active Manager style Single Asset Allocation Benchmark (%) Australian Fixed Interest 100 Cash 0 Quality Allocation % BBB 44.08 A 32.80 AAA 12.27 Cash 4.69 AA 4.54 BB 2.10 CCC 0.95 Agency/Government 0.17 Fund Performance The Fund produced a positive absolute return in the March quarter.