Shifting Centers of Gravity the End of the Automotive Industry As We Know It? Contents Foreword

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2014 Kraftstoffförderung Fuel Supply and Control

Inklusive Dieselfahrzeuge Includes diesel-engine vehicles Véhicules diesel compris Veicoli diesel inclusi Включая дизельные автомобили de en fr it ru Sichere Diagnose. Reliable diagnosis. Diagnostic fiable. Diagnosi sicure. Ripara- Надежная диагностика. Zeitsparende Reparatur. Time-saving repairs. Réparation rapide. zioni rapide. Diagnostica, Экономящий время Bosch-Diagnostics und Bosch diagnostics and Diagnostics et pièces ricambi e formazione: tutto ремонт. Диагностическое Ersatzteile. service parts. de rechange Bosch. da un unico fornitore. оборудование и запчасти Bosch. Alles aus einer Hand. Everything from a single Un fournisseur unique. Bosch offre all’officina un Bosch bietet der Werkstatt source. Bosch offers a full Bosch propose aux pro- programma completo per Все из одних рук. ein Komplettprogramm range of products that boo- fessionnels une gamme una maggior efficienza e Bosch предлагает СТО zur Steigerung von Effizienz sts everyday efficiency and complète qui améliore qualità nel lavoro quotidia - полную программу, обе- und Qualität in der täglichen quality in the workshop. l’efficacité et la qualité du no d’autoriparazione. Con спечивающую повышение Arbeit. Service parts are available travail quotidien. il programma «Diagnostics», эффективности и качества Vom weltweit aktiven from the globally active En tant que concepteur Bosch mette a disposizione в повседневной ее работе. Entwickler und führenden developer and leading man- présent dans le monde en- dell’officina anche hard- Оригинальное качество Hersteller von Kfz-System- ufacturer of automotive sy- tier et leader dans la fabri- ware e software di diagnosi запчастей от мирового раз- technik kommen die Ersatz- stem technology in renow- cation de systèmes pour perfettamente in sintonia работчика и ведущего из- teile in bekannter Original- ned Bosch OE quality. -

Marketing Strategies for Chery Automobile Corporation

ISSN 1712-8056[Print] Canadian Social Science ISSN 1923-6697[Online] Vol. 9, No. 4, 2013, pp. 177-183 www.cscanada.net DOI:10.3968/j.css.1923669720130904.2560 www.cscanada.org Marketing Strategies for Chery Automobile Corporation ZHANG Junjie[a],*; DAI Xiajing[b] [a] Lecturer of Business and Management, Department of Business and Management, Business School, Jiaxing University. Jiaxing, Zhejiang, 1. RESEARCH BACKGROUND China. INTRODUCTION [b] Business School, Jiaxing University. Jiaxing, Zhejiang, China. *Corresponding author. In our modern consumer society, any organization which aims to survive and develop in the market should be marketing orientated. Satisfying customers’ needs and Abstract meeting their expectations are the most crucial ways to A marketing strategy is a road map for the marketing retain, expand a business. While marketing plan plays activities of an organization for future period of time. It a key role in the actualization of marketing activities. A always helps the organization to understand clearly about marketing plan is a road map for the marketing activities the questions like these: what are we now? Where do we of an organization for future period of time. In this want to go? How do we allocate our resources to get to business report, we mainly recommend a marketing plan where we want to go? How do we convert our plans into for Chery Automobile Corp through the studies about its actions? How do our results compare our plans, and do external business environment and internal environment deviations require new plans and actions? The paper tries by some useful business analytical tools like PEST to formulate a marketing strategy for Chery Automobile analysis and SWOT analysis. -

Analysis of the Dynamic Relationship Between the Emergence Of

Annals of Business Administrative Science 8 (2009) 21–42 Online ISSN 1347-4456 Print ISSN 1347-4464 Available at www.gbrc.jp ©2009 Global Business Research Center Analysis of the Dynamic Relationship between the Emergence of Independent Chinese Automobile Manufacturers and International Technology Transfer in China’s Auto Industry Zejian LI Manufacturing Management Research Center Faculty of Economics, the University of Tokyo E-mail: [email protected] Abstract: This paper examines the relationship between the emergence of independent Chinese automobile manufacturers (ICAMs) and International Technology Transfer. Many scholars indicate that the use of outside supplies is the sole reason for the high-speed growth of ICAMs. However, it is necessary to outline the reasons and factors that might contribute to the process at the company-level. This paper is based on the organizational view. It examines and clarifies the internal dynamics of the ICAMs from a historical perspective. The paper explores the role that international technology transfer has played in the emergence of ICAMs. In conclusion, it is clear that due to direct or indirect spillover from joint ventures, ICAMs were able to autonomously construct the necessary core competitive abilities. Keywords: marketing, international business, multinational corporations (MNCs), technology transfer, Chinese automobile industry but progressive emergence of independent Chinese 1. Introduction automobile manufacturers (ICAMs). It will also The purpose of this study is to investigate -

The Positioning Disaster of Tata Nano: a Case Study On

IJMH - International Journal of Management and Humanities ISSN: 2349-7289 THE POSITIONING DISASTER OF TATA NANO: A CASE STUDY ON TATA NANO Ashik Makwana1 | Prof Nishit Sagotia2 1(Student, MBA Semester 09, Noble Group of Institutions, Junagadh, Gujarat, [email protected]) 2(Assistant Professor, Dept of Management, Noble Group of Institutions, Junagadh, Gujarat, [email protected]) ___________________________________________________________________________________________________ Abstract— The Indian auto industry is one of the largest in the world. The industry accounts for 7.1 per cent of the country's Gross Domestic Product (GDP). The Two Wheelers segment with 80 per cent market share is the leader of the Indian Automobile market. Tata Motors Limited is a leading global automobile manufacturer of cars utility vehicles buses trucks and defence vehicles. Tata Nano popularly known as people‘s car was launched at such time when India‘s largest car company known for its cost effective products Maruti Suzuki was pondering upon the strategic option of discontinuing the production of the than available cheapest car of Indian Market and it flagship product Maruti Suzuki 800. This case is selected as per following basis: Case is related with marketing Mix, positioning of the product and brand equity, to understand what went wrong with Nano, to understand the concept of Positioning, to understand how marketing mistakes makes a product to failure, to find alternatives for the solutions. Following are the sources of data collection: Articles and review of students and people and Dr. Vivek Bindra’s videos. Following are the assumptions of the case study: the company will continue its product in the market, the collected data is correct. -

Chapter 2 China's Cars and Parts

Chapter 2 China’s cars and parts: development of an industry and strategic focus on Europe Peter Pawlicki and Siqi Luo 1. Introduction Initially, Chinese investments – across all industries in Europe – especially acquisitions of European companies were discussed in a relatively negative way. Politicians, trade unionists and workers, as well as industry representatives feared the sell-off and the subsequent rapid drainage of industrial capabilities – both manufacturing and R&D expertise – and with this a loss of jobs. However, with time, coverage of Chinese investments has changed due to good experiences with the new investors, as well as the sheer number of investments. Europe saw the first major wave of Chinese investments right after the financial crisis in 2008–2009 driven by the low share prices of European companies and general economic decline. However, Chinese investments worldwide as well as in Europe have not declined since, but have been growing and their strategic character strengthening. Chinese investors acquiring European companies are neither new nor exceptional anymore and acquired companies have already gained some experience with Chinese investors. The European automotive industry remains one of the most important investment targets for Chinese companies. As in Europe the automotive industry in China is one of the major pillars of its industry and its recent industrial upgrading dynamics. Many of China’s central industrial policy strategies – Sino-foreign joint ventures and trading market for technologies – have been established with the aim of developing an indigenous car industry with Chinese car OEMs. These instruments have also been transferred to other industries, such as telecommunications equipment. -

Fulbright-Hays Seminars Abroad Automobility in China Dr. Toni Marzotto

Fulbright-Hays Seminars Abroad Automobility in China Dr. Toni Marzotto “The mountains are high and the emperor is far away.” (Chinese Proverb)1 Title: The Rise of China's Auto Industry: Automobility with Chinese Characteristics Curriculum Project: The project is part of an interdisciplinary course taught in the Political Science Department entitled: The Machine that Changed the World: Automobility in an Age of Scarcity. This course looks at the effects of mass motorization in the United States and compares it with other countries. I am teaching the course this fall; my syllabus contains a section on Chinese Innovations and other global issues. This project will be used to expand this section. Grade Level: Undergraduate students in any major. This course is part of Towson University’s new Core Curriculum approved in 2011. My focus in this course is getting students to consider how automobiles foster the development of a built environment that comes to affect all aspects of life whether in the U.S., China or any country with a car culture. How much of our life is influenced by the automobile? We are what we drive! Objectives and Student Outcomes: My objective in teaching this interdisciplinary course is to provide students with an understanding of how the invention of the automobile in the 1890’s has come to dominate the world in which we live. Today an increasing number of individuals, across the globe, depend on the automobile for many activities. Although the United States was the first country to embrace mass motorization (there are more cars per 1000 inhabitants in the United States than in any other country in the world), other countries are catching up. -

Nano-The People's

International Journal of Research in Management ISSN 2249-5908 Issue2, Vol. 2 (March-2012) Nano-The People’s Car Name first author-Dr. Binod Kumar Singh Designation –Faculty Member Address-Dr. Binod Kumar Singh, Faculty Member,Amity Global Business School,Patna E-mail id- [email protected], [email protected] Mobile No.-+91-9430602830, +91-9204055893 ___________________________________________________________________________ Author Profile I did Ph.D. (Statistics) from Faculty of Science, Banaras Hindu University and Diploma in Information Technology from R.C.S.M.I had seven years of teaching experience. Seven of my papers were published in International and eleven were published in National Journal. I have attended number of international conferences. I have been nominated Member Editorial Board for the Journal of Bioinformatics and Sequence Analysis (JBSA), African Journal of Business Management (Impact factor 1.015) and International Journal on Business Management, Finance, Human Resource, Marketing and Economics (ISI Index Journal), Asian Journal of Marketing,(ISI index journal), Research Journal of Business Management(ISI index journal), Asian Journal of Mathematics and Statistics(ISI index journal), Singapore Journal of Scientific Research(ISI index journal) and Journal of Economics & International Finance, ISSN:2006-9812(ISI index journal. Vice-Chancellor of Central University of Jharkhand, Ranchi has been nominated me to act as an expert member in the selection committee meeting for the post of Jr. System Executive. I have been selected in the panel of experts in a round table discussion held on 10 February 10, 2010, entitled "Denmark: Better, Faster, Stronger - Leading the Way in Translational Medicine‖. I have been also selected in the panel of experts in a round table discussion held on 10 December 2008, entitled, "State of the Nation: Science in Ireland.‖ My thrust areas are Statistics, Quantitative Methods, Marketing Research, Research Methodology and Operation Management. -

CHINA CORP. 2015 AUTO INDUSTRY on the Wan Li Road

CHINA CORP. 2015 AUTO INDUSTRY On the Wan Li Road Cars – Commercial Vehicles – Electric Vehicles Market Evolution - Regional Overview - Main Chinese Firms DCA Chine-Analyse China’s half-way auto industry CHINA CORP. 2015 Wan Li (ten thousand Li) is the Chinese traditional phrase for is a publication by DCA Chine-Analyse evoking a long way. When considering China’s automotive Tél. : (33) 663 527 781 sector in 2015, one may think that the main part of its Wan Li Email : [email protected] road has been covered. Web : www.chine-analyse.com From a marginal and closed market in 2000, the country has Editor : Jean-François Dufour become the World’s first auto market since 2009, absorbing Contributors : Jeffrey De Lairg, over one quarter of today’s global vehicles output. It is not Du Shangfu only much bigger, but also much more complex and No part of this publication may be sophisticated, with its high-end segment rising fast. reproduced without prior written permission Nevertheless, a closer look reveals China’s auto industry to be of the publisher. © DCA Chine-Analyse only half-way of its long road. Its success today, is mainly that of foreign brands behind joint- ventures. And at the same time, it remains much too fragmented between too many builders. China’s ultimate goal, of having an independant auto industry able to compete on the global market, still has to be reached, through own brands development and restructuring. China’s auto industry is only half-way also because a main technological evolution that may play a decisive role in its future still has to take off. -

State of Automotive Technology in PR China - 2014

Lanza, G. (Editor) Hauns, D.; Hochdörffer, J.; Peters, S.; Ruhrmann, S.: State of Automotive Technology in PR China - 2014 Shanghai Lanza, G. (Editor); Hauns, D.; Hochdörffer, J.; Peters, S.; Ruhrmann, S.: State of Automotive Technology in PR China - 2014 Institute of Production Science (wbk) Karlsruhe Institute of Technology (KIT) Global Advanced Manufacturing Institute (GAMI) Leading Edge Cluster Electric Mobility South-West Contents Foreword 4 Core Findings and Implications 5 1. Initial Situation and Ambition 6 Map of China 2. Current State of the Chinese Automotive Industry 8 2.1 Current State of the Chinese Automotive Market 8 2.2 Differences between Global and Local Players 14 2.3 An Overview of the Current Status of Joint Ventures 24 2.4 Production Methods 32 3. Research Capacities in China 40 4. Development Focus Areas of the Automotive Sector 50 4.1 Comfort and Safety 50 4.1.1 Advanced Driver Assistance Systems 53 4.1.2 Connectivity and Intermodality 57 4.2 Sustainability 60 4.2.1 Development of Alternative Drives 61 4.2.2 Development of New Lightweight Materials 64 5. Geographical Structure 68 5.1 Industrial Cluster 68 5.2 Geographical Development 73 6. Summary 76 List of References 78 List of Figures 93 List of Abbreviations 94 Edition Notice 96 2 3 Foreword Core Findings and Implications . China’s market plays a decisive role in the . A Chinese lean culture is still in the initial future of the automotive industry. China rose to stage; therefore further extensive training and become the largest automobile manufacturer education opportunities are indispensable. -

68 DIÁRIO OFICIAL Nº 33769 Sexta-Feira, 28 DE

68 DIÁRIO OFICIAL Nº 33769 Sexta-feira, 28 DE DEZEMBRO DE 2018 5932 106701 I/CADILLAC SEVILLE STS G 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 5933 216311 I/CADILLAC SRX G 0,00 0,00 0,00 0,00 0,00 0,00 3.286,00 2.929,00 2.856,00 2.832,00 2.431,00 0,00 2.347,00 2.111,00 1.959,00 5934 216326 I/CADILLAC SRX AWD G 0,00 0,00 0,00 0,00 0,00 0,00 4.576,00 3.896,00 3.620,00 0,00 0,00 0,00 0,00 0,00 0,00 5935 216330 I/CADILLAC SRX AWD T PRE G 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 3.827,00 0,00 0,00 0,00 0,00 0,00 0,00 5936 216335 I/CADILLAC SRX CROSSOVER G 0,00 0,00 0,00 0,00 0,00 0,00 0,00 3.349,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 5937 216322 I/CADILLAC SRX FWD G 0,00 0,00 0,00 0,00 4.568,00 0,00 0,00 2.808,00 0,00 2.598,00 0,00 0,00 0,00 0,00 0,00 5938 216324 I/CADILLAC SRX LUXURY G 0,00 0,00 0,00 0,00 0,00 0,00 3.967,00 3.529,00 3.379,00 0,00 0,00 0,00 0,00 0,00 0,00 5939 216328 I/CADILLAC SRX PREMI AWD G 0,00 0,00 0,00 0,00 0,00 0,00 0,00 2.965,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 5940 216327 I/CADILLAC SRX PREMIUM G 0,00 0,00 0,00 0,00 4.955,00 4.676,00 4.457,00 3.930,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 5941 216325 I/CADILLAC SRX4 G 0,00 0,00 0,00 0,00 0,00 0,00 4.475,00 4.072,00 3.884,00 0,00 0,00 0,00 0,00 0,00 0,00 5942 106712 I/CADILLAC STS G 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 971,00 0,00 5943 106716 I/CADILLAC XLR CONV G 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 0,00 4.468,00 0,00 0,00 0,00 5944 149589 I/CADILLAC XTS LUXURY G 0,00 0,00 0,00 0,00 0,00 0,00 7.042,00 -

China Autos 2020 Outlook – Slow Lane to a Full Recovery

2 December 2019 China EQUITIES China autos Macquarie China auto coverage 2020 outlook – slow lane to a full recovery Name Ticker Price Rating TP +/- Brilliance 1114 HK 8.17 Outperform 10.10 23.6% Dongfeng 489 HK 7.64 Outperform 8.10 6.0% Key points GAC 2238 HK 8.52 Outperform 9.60 12.7% SAIC Motor 600104 CH 23.04 Outperform 31.50 36.7% Cautious outlook for 2020 PV demand, mainly considering weak demand Nexteer 1316 HK 6.66 Outperform 12.15 82.4% from lower-tier cities, increased household leverage and rising CPI. Minth 425 HK 27.30 Outperform 25.80 -5.5% Geely 175 HK 15.08 Neutral 11.20 -25.7% We expect to see further relaxation of the license plate quota in 2020. Yutong Bus 600066 CH 14.31 Neutral 12.70 -11.3% BAIC 1958 HK 4.51 Neutral 4.20 -6.9% Sector preference: higher-end > lower-end > NEVs. Near-term risks on the BYD 1211 HK 38.15 Underperform 20.70 -45.7% downside. OP: Brilliance, DFG, GAC; UP: GWM, BYD, CATL. CATL 300750 CH 87.41 Underperform 60.30 -31.0% Great Wall 2333 HK 6.04 Underperform 3.70 -38.7% Changan-B 200625 CH 3.54 Underperform 3.10 -12.4% Changan-A 000625 CH 8.31 Underperform 3.60 -56.7% Conclusions Note: updated as of 28 November closing prices; Prices are denominated in Rmb for A-share stocks, and HKD for A slow road back to recovery: We lower our 2020 China auto sales by 5% B/H-share stocks. -

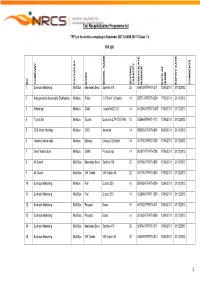

TRP Programme List July Revision 64

- 1 -Last saved by nthitemd - 1 -19 Taxi Recapitalization Programme list TRP List for vehicles complying to September 2007 & SANS 20107 Clause 7.6 TRP 2009 ISSUE DATE EXPIRY COMMENTS NO COMPANY CATEGORY NAME MODEL NAME SEATING CAPACITY CERTIFICATE NUMBER OF DATE 1 Bustruck Marketing Midi Bus Mercedes Benz Sprinter 518 22 556739-TRP07-0311 13/06/2011 31/12/2013 2 Amalgamated Automobile Distributors Minibus Foton 2.2 Petrol 13 Seater 14 550713-TRP07-0309 17/06/2011 31/12/2013 3 Whallinger Minibus CAM Inyathi XGD 2.2i 14 541394-TRPO7-0609 17/06/2011 31/12/2013 4 Toyota SA Minibus Toyota Quantum 2.7P 15S TAXI 15 555664-TRP07-1110 17/06/2011 31/12/2013 5 CCE Motor Holdings Minibus CMC Amandla 14 550826-TRP07-0609 20/06/2011 31/12/2013 6 Nanfeng Automobile Minibus Ekhaya Ekhaya 2.2i Hatch 14 551700-TRP07-0709 17/06/2011 31/12/2013 7 Great Wall motors Minibus GWM Proteus Mpi 14 551517-TRP07-0709 17/06/2011 31/12/2013 8 Mr Coach Midi Bus Mercedes Benz Sprinter 518 22 551798-TRP07-0809 17/06/2011 31/12/2013 9 Mr Coach Midi Bus VW Crafter VW Crafter 50 22 551799-TRP07-0809 17/06/2011 31/12/2013 10 Bustruck Marketing Minibus Fiat Ducato 250 16 551958-TRP07-0809 13/06/2011 31/12/2013 11 Bustruck Marketing Midi Bus Fiat Ducato 250 19 552898-TRP07-1209 13/06/2011 31/12/2013 12 Bustruck Marketing Midi Bus Peugeot Boxer 19 557082-TRP07-0411 13/06/2011 31/12/2013 13 Bustruck Marketing Midi Bus Peugeot Boxer 16 551959-TRP07-0809 13/06/2011 31/12/2013 14 Bustruck Marketing Midi Bus Mercedes Benz Sprinter 416 22 556740-TRP07-0311 13/06/2011 31/12/2013 15