A Case Study of the Cut-Flower Industry in Zimbabwe

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Appendix 25 Box 31/3 Airline Codes

March 2021 APPENDIX 25 BOX 31/3 AIRLINE CODES The information in this document is provided as a guide only and is not professional advice, including legal advice. It should not be assumed that the guidance is comprehensive or that it provides a definitive answer in every case. Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 000 ANTONOV DESIGN BUREAU 001 AMERICAN AIRLINES 005 CONTINENTAL AIRLINES 006 DELTA AIR LINES 012 NORTHWEST AIRLINES 014 AIR CANADA 015 TRANS WORLD AIRLINES 016 UNITED AIRLINES 018 CANADIAN AIRLINES INT 020 LUFTHANSA 023 FEDERAL EXPRESS CORP. (CARGO) 027 ALASKA AIRLINES 029 LINEAS AER DEL CARIBE (CARGO) 034 MILLON AIR (CARGO) 037 USAIR 042 VARIG BRAZILIAN AIRLINES 043 DRAGONAIR 044 AEROLINEAS ARGENTINAS 045 LAN-CHILE 046 LAV LINEA AERO VENEZOLANA 047 TAP AIR PORTUGAL 048 CYPRUS AIRWAYS 049 CRUZEIRO DO SUL 050 OLYMPIC AIRWAYS 051 LLOYD AEREO BOLIVIANO 053 AER LINGUS 055 ALITALIA 056 CYPRUS TURKISH AIRLINES 057 AIR FRANCE 058 INDIAN AIRLINES 060 FLIGHT WEST AIRLINES 061 AIR SEYCHELLES 062 DAN-AIR SERVICES 063 AIR CALEDONIE INTERNATIONAL 064 CSA CZECHOSLOVAK AIRLINES 065 SAUDI ARABIAN 066 NORONTAIR 067 AIR MOOREA 068 LAM-LINHAS AEREAS MOCAMBIQUE Page 2 of 19 Appendix 25 - SAD Box 31/3 Airline Codes March 2021 Airline code Code description 069 LAPA 070 SYRIAN ARAB AIRLINES 071 ETHIOPIAN AIRLINES 072 GULF AIR 073 IRAQI AIRWAYS 074 KLM ROYAL DUTCH AIRLINES 075 IBERIA 076 MIDDLE EAST AIRLINES 077 EGYPTAIR 078 AERO CALIFORNIA 079 PHILIPPINE AIRLINES 080 LOT POLISH AIRLINES 081 QANTAS AIRWAYS -

Fields Listed in Part I. Group (8)

Chile Group (1) All fields listed in part I. Group (2) 28. Recognized Medical Specializations (including, but not limited to: Anesthesiology, AUdiology, Cardiography, Cardiology, Dermatology, Embryology, Epidemiology, Forensic Medicine, Gastroenterology, Hematology, Immunology, Internal Medicine, Neurological Surgery, Obstetrics and Gynecology, Oncology, Ophthalmology, Orthopedic Surgery, Otolaryngology, Pathology, Pediatrics, Pharmacology and Pharmaceutics, Physical Medicine and Rehabilitation, Physiology, Plastic Surgery, Preventive Medicine, Proctology, Psychiatry and Neurology, Radiology, Speech Pathology, Sports Medicine, Surgery, Thoracic Surgery, Toxicology, Urology and Virology) 2C. Veterinary Medicine 2D. Emergency Medicine 2E. Nuclear Medicine 2F. Geriatrics 2G. Nursing (including, but not limited to registered nurses, practical nurses, physician's receptionists and medical records clerks) 21. Dentistry 2M. Medical Cybernetics 2N. All Therapies, Prosthetics and Healing (except Medicine, Osteopathy or Osteopathic Medicine, Nursing, Dentistry, Chiropractic and Optometry) 20. Medical Statistics and Documentation 2P. Cancer Research 20. Medical Photography 2R. Environmental Health Group (3) All fields listed in part I. Group (4) All fields listed in part I. Group (5) All fields listed in part I. Group (6) 6A. Sociology (except Economics and including Criminology) 68. Psychology (including, but not limited to Child Psychology, Psychometrics and Psychobiology) 6C. History (including Art History) 60. Philosophy (including Humanities) -

Southern Africa, Vol. 6, No. 8

Southern Africa, Vol. 6, No. 8 http://www.aluka.org/action/showMetadata?doi=10.5555/AL.SFF.DOCUMENT.nusa197310 Use of the Aluka digital library is subject to Aluka’s Terms and Conditions, available at http://www.aluka.org/page/about/termsConditions.jsp. By using Aluka, you agree that you have read and will abide by the Terms and Conditions. Among other things, the Terms and Conditions provide that the content in the Aluka digital library is only for personal, non-commercial use by authorized users of Aluka in connection with research, scholarship, and education. The content in the Aluka digital library is subject to copyright, with the exception of certain governmental works and very old materials that may be in the public domain under applicable law. Permission must be sought from Aluka and/or the applicable copyright holder in connection with any duplication or distribution of these materials where required by applicable law. Aluka is a not-for-profit initiative dedicated to creating and preserving a digital archive of materials about and from the developing world. For more information about Aluka, please see http://www.aluka.org Southern Africa, Vol. 6, No. 8 Alternative title Southern AfricaSouthern Africa News BulletinRhodesia News Summary Author/Creator Southern Africa Committee Publisher Southern Africa Committee Date 1973-10-00 Resource type Magazines (Periodicals) Language English Subject Coverage (spatial) Southern Africa (region), South Africa, United States, Zimbabwe, Angola, Mozambique, Guinea-Bissau Coverage (temporal) 1973-00-00 Source Northwestern University Libraries Rights By kind permission of the Southern Africa Committee. Description Inside Mozambique. Black Sell-Outs Sell Apartheid. -

1.4. Coding and Decoding of Airlines 1.4.1. Coding Of

1.4. CODING AND DECODING OF AIRLINES 1.4.1. CODING OF AIRLINES In addition to the airlines' full names in alphabetical order the list below also contains: - Column 1: the airlines' prefix numbers (Cargo) - Column 2: the airlines' 2 character designators - Column 3: the airlines' 3 letter designators A Explanation of symbols: + IATA Member & IATA Associate Member * controlled duplication # Party to the IATA Standard Interline Traffic Agreement (see section 8.1.1.) © Cargo carrier only Full name of carrier 1 2 3 40-Mile Air, Ltd. Q5 MLA AAA - Air Alps Aviation A6 LPV AB Varmlandsflyg T9 ABX Air, Inc. © 832 GB Ada Air + 121 ZY ADE Adria Airways + # 165 JP ADR Aegean Airlines S.A. + # 390 A3 AEE Aer Arann Express (Comharbairt Gaillimh Teo) 809 RE REA Aeris SH AIS Aer Lingus Limited + # 053 EI EIN Aero Airlines A.S. 350 EE Aero Asia International Ltd. + # 532 E4 Aero Benin S.A. EM Aero California + 078 JR SER Aero-Charter 187 DW UCR Aero Continente 929 N6 ACQ Aero Continente Dominicana 9D Aero Express Del Ecuador - Trans AM © 144 7T Aero Honduras S.A. d/b/a/ Sol Air 4S Aero Lineas Sosa P4 Aero Lloyd Flugreisen GmbH & Co. YP AEF Aero Republica S.A. 845 P5 RPB Aero Zambia + # 509 Z9 Aero-Condor S.A. Q6 Aero Contractors Company of Nigeria Ltd. AJ NIG Aero-Service BF Aerocaribe 723 QA CBE Aerocaribbean S.A. 164 7L CRN Aerocontinente Chile S.A. C7 Aeroejecutivo S.A. de C.V. 456 SX AJO Aeroflot Russian Airlines + # 555 SU AFL Aeroflot-Don 733 D9 DNV Aerofreight Airlines JSC RS Aeroline GmbH 7E AWU Aerolineas Argentinas + # 044 AR ARG Aerolineas Centrales de Colombia (ACES) + 137 VX AES Aerolineas de Baleares AeBal 059 DF ABH Aerolineas Dominicanas S.A. -

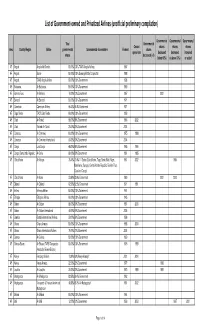

List of Government-Owned and Privatized Airlines (Unofficial Preliminary Compilation)

List of Government-owned and Privatized Airlines (unofficial preliminary compilation) Governmental Governmental Governmental Total Governmental Ceased shares shares shares Area Country/Region Airline governmental Governmental shareholders Formed shares operations decreased decreased increased shares decreased (=0) (below 50%) (=/above 50%) or added AF Angola Angola Air Charter 100.00% 100% TAAG Angola Airlines 1987 AF Angola Sonair 100.00% 100% Sonangol State Corporation 1998 AF Angola TAAG Angola Airlines 100.00% 100% Government 1938 AF Botswana Air Botswana 100.00% 100% Government 1969 AF Burkina Faso Air Burkina 10.00% 10% Government 1967 2001 AF Burundi Air Burundi 100.00% 100% Government 1971 AF Cameroon Cameroon Airlines 96.43% 96.4% Government 1971 AF Cape Verde TACV Cabo Verde 100.00% 100% Government 1958 AF Chad Air Tchad 98.00% 98% Government 1966 2002 AF Chad Toumai Air Tchad 25.00% 25% Government 2004 AF Comoros Air Comores 100.00% 100% Government 1975 1998 AF Comoros Air Comores International 60.00% 60% Government 2004 AF Congo Lina Congo 66.00% 66% Government 1965 1999 AF Congo, Democratic Republic Air Zaire 80.00% 80% Government 1961 1995 AF Cofôte d'Ivoire Air Afrique 70.40% 70.4% 11 States (Cote d'Ivoire, Togo, Benin, Mali, Niger, 1961 2002 1994 Mauritania, Senegal, Central African Republic, Burkino Faso, Chad and Congo) AF Côte d'Ivoire Air Ivoire 23.60% 23.6% Government 1960 2001 2000 AF Djibouti Air Djibouti 62.50% 62.5% Government 1971 1991 AF Eritrea Eritrean Airlines 100.00% 100% Government 1991 AF Ethiopia Ethiopian -

A Decade of Civil Aviation in Zimbabwe: Towards a History of Air Zimbabwe Corporation 1980 to 1990

The African e-Journals Project has digitized full text of articles of eleven social science and humanities journals. This item is from the digital archive maintained by Michigan State University Library. Find more at: http://digital.lib.msu.edu/projects/africanjournals/ Available through a partnership with Scroll down to read the article. Zambezia (1995), XXII (i). A DECADE OF CIVIL AVIATION IN ZIMBABWE: TOWARDS A HISTORY OF AIR ZIMBABWE CORPORATION 1980 TO 1990 A. S. MLAMBO Department of Economic History, University of Zimbabwe Abstract In 1980 when Air Zimbabwe was established, there was great hope that it would prosper, especially since it was going to operate in a global atmosphere without the restrictions of economic sanctions that had constrained its predecessor, Rhodesia Airways. In the first few years, Air Zimbabwe expanded its services, replaced old aircraft with newer and more hiel-efficient state-of- the-art aeroplanes. By the mid-1980s however, the airline had started to lose money and continued to do so for the rest of the decade, necessitating hefty subsidies from the government. This article traces the development of Air Zimbabwe from 1980 to 1990 and attempts to analyze the reasons behind the airline's disappointing performance. It suggests that the failure of the airline to operate as a viable commercial enterprise was a result of both internal weaknesses of the airline's administration and restrictive government policies, as well as a generally difficult global economic climate. INTRODUCTION Air Zimbabwe Corporation (hereafter called AirZim) was established under the Zimbabwe Corporation Act (Chapter 253) of 1980.1 The new airline took over from Rhodesia Airways which had been established in 1967 and which had operated profitably throughout its existence, with the exception of the 1979 financial year when it registered its first deficit. -

3 Digit 2 Digit Ticketing Code Code Name Code ------6M 40-MILE AIR VY A.C.E

06/07/2021 www.kovrik.com/sib/travel/airline-codes.txt 3 Digit 2 Digit Ticketing Code Code Name Code ------- ------- ------------------------------ --------- 6M 40-MILE AIR VY A.C.E. A.S. NORVING AARON AIRLINES PTY SM ABERDEEN AIRWAYS 731 GB ABX AIR (CARGO) 832 VX ACES 137 XQ ACTION AIRLINES 410 ZY ADALBANAIR 121 IN ADIRONDACK AIRLINES JP ADRIA AIRWAYS 165 REA RE AER ARANN 684 EIN EI AER LINGUS 053 AEREOS SERVICIOS DE TRANSPORTE 278 DU AERIAL TRANSIT COMPANY(CARGO) 892 JR AERO CALIFORNIA 078 DF AERO COACH AVIATION INT 868 2G AERO DYNAMICS (CARGO) AERO EJECUTIVOS 681 YP AERO LLOYD 633 AERO SERVICIOS 243 AERO TRANSPORTES PANAMENOS 155 QA AEROCARIBE 723 AEROCHAGO AIRLINES 198 3Q AEROCHASQUI 298 AEROCOZUMEL 686 AFL SU AEROFLOT 555 FP AEROLEASING S.A. ARG AR AEROLINEAS ARGENTINAS 044 VG AEROLINEAS EL SALVADOR (CARGO) 680 AEROLINEAS URUGUAYAS 966 BQ AEROMAR (CARGO) 926 AM AEROMEXICO 139 AEROMONTERREY 722 XX AERONAVES DEL PERU (CARGO) 624 RL AERONICA 127 PO AEROPELICAN AIR SERVICES WL AEROPERLAS PL AEROPERU 210 6P AEROPUMA, S.A. (CARGO) AW AEROQUETZAL 291 XU AEROVIAS (CARGO) 316 AEROVIAS COLOMBIANAS (CARGO) 158 AFFRETAIR (PRIVATE) (CARGO) 292 AFRICAN INTERNATIONAL AIRWAYS 648 ZI AIGLE AZUR AMM DP AIR 2000 RK AIR AFRIQUE 092 DAH AH AIR ALGERIE 124 3J AIR ALLIANCE 188 4L AIR ALMA 248 AIR ALPHA AIR AQUITAINE FQ AIR ARUBA 276 9A AIR ATLANTIC LTD. AAG ES AIR ATLANTIQUE OU AIR ATONABEE/CITY EXPRESS 253 AX AIR AURORA (CARGO) 386 ZX AIR B.C. 742 KF AIR BOTNIA BP AIR BOTSWANA 636 AIR BRASIL 853 AIR BRIDGE CARRIERS (CARGO) 912 VH AIR BURKINA 226 PB AIR BURUNDI 919 TY AIR CALEDONIE 190 www.kovrik.com/sib/travel/airline-codes.txt 1/15 06/07/2021 www.kovrik.com/sib/travel/airline-codes.txt SB AIR CALEDONIE INTERNATIONAL 063 ACA AC AIR CANADA 014 XC AIR CARIBBEAN 918 SF AIR CHARTER AIR CHARTER (CHARTER) AIR CHARTER SYSTEMS 272 CCA CA AIR CHINA 999 CE AIR CITY S.A. -

“Honoured More in the Breach Than in the Observance”: Economic Sanctions on Rhodesia1 and International Response, 1965 to 1979

“HONOURED MORE IN THE BREACH THAN IN THE OBSERVANCE”: ECONOMIC SANCTIONS ON RHODESIA1 AND INTERNATIONAL RESPONSE, 1965 TO 1979 A. S. Mlambo Department of Historical and Heritage Studies University of Pretoria Abstract The United Nations Security Council passed a series of resolutions condemning Rhodesia’s unilateral declaration of independence (UDI) in 1965, culminating in Resolution 253 of 1968 imposing comprehensive mandatory international sanctions on Rhodesia. With a few exceptions, notably South Africa and Portugal, most member states supported the resolution and pledged their commitment to uphold and enforce the measures. Yet, most countries, including those at the forefront of imposing sanctions against Rhodesia, broke sanctions or did little to enforce them. An examination of the records of the Security Council Committee Established in Pursuance of Resolution 253 (1968) Concerning the Question of Southern Rhodesia (the Sanctions Committee) shows that sanctions against Rhodesia were honoured more in the breach than in the observance. Keywords: Sanctions, UDI, United Nations, Security Council, Sanctions busting, Ian Smith, Harold Wilson Introduction On November 11, 1965, the Rhodesia Front Government of Prime Minister Ian Douglas Smith unilaterally declared independence (UDI) from Britain in response to the colonial authority’s reluctance to grant independence to the country under white minority rule. Facing mounting pressure to use force to topple the illegal regime in Rhodesia from the Afro-Asian lobby at the United Nations (UN), Britain opted, to impose economic sanctions on Rhodesia, instead. British Prime Minister Harold Wilson confidently predicted at the time 1 The names Rhodesia and Southern Rhodesia are used interchangeably in this paper. While the UDI leaders referred to the country only as ‘Rhodesia’, the United Nations continued to call it ‘Southern Rhodesia’ throughout the UDI period. -

ZWE C2055 1.Pdf

The Building of Zimbabwe. Climate Taxation Investment Production Amenities A foundation of the strongest economy in indépendant Africa. With a flooring of a polished and sophisticated investment infrastructure. Walled by solid small, medium and large indust¬ rial, agricultural and commercial development Easy access gained through import and export doors which swing easily both ways with equal facility. With windows opening out onto the panorama of the markets of Africa. A ceiling which offers the protection of one of the most stable taxation systems in the world. Amenities which include one of the most pro¬ gressive and sophisticated communications systems on the continent. And ... we haven't stopped building yet— we don't envisage doing so for a long, long time. Department of Information, '.O. Box 8150, Causeway. Harare. Zimbabwe. Tel. 703891 Telex 4142 ZW A FIELD FOR INVESTMENT 1985/86 Published annually in the interests of economic progress — selective world distribution Printed by: Editor Published by: Thomson Amalgamated Press, Advertising Sales Publications Zimbabwe, P.O. Box Box ST293, Southerton. Production, Layout & Design 1683, Harare. CONTENTS Facts about Zimbabwe 2 National Statistics 3 Agriculture 4 Mining 8 Manufacturing 11 Commerce 13 Energy 14 Exports 15 The Private Sector 16 The Banking Sector 17 Finance and the Institutions 23 Transport 28 Tourism 33 Industrial and Commercial Centres 39 Statistics are taken from official sources and the Economic Survey of Zimbabwe 1980, produced by the Ministry of Finance. PARTICIPANTS L__ Page Air Zimbabwe 30 Lonrho Zimabwe Ltd Aluminium Industries Ltd 13 National Railways of Zimbabwe Anglo American Corp. Services Ltd 9 Oyxo Barclays Bank of Zimbabwe 19 PG Industries CABS 44 POSB Cold Storage Commission 6 RAL Merchant Bank Ltd Department of Information .. -

Joanna Warson Phd FINAL 2013

France in Rhodesia: French policy and perceptions throughout the era of decolonisation Joanna Warson This thesis is submitted in partial fulfilment of the requirements for the award of the degree of Doctor of Philosophy of the University of Portsmouth 2013 i Abstract This thesis analyses French policies towards and perceptions of the British colony of Rhodesia, from the immediate aftermath of the Second World War up until the territory’s independence as Zimbabwe in 1980. Its main objective is to challenge notions of exceptionality associated with Franco- African relations, by investigating French engagement with a region outside of its traditional sphere of African influence. The first two chapters explore the development of Franco-Rhodesian relations in the eighteen years following the establishment of a French Consulate in Salisbury in 1947. Chapter One examines the foreign policy mind-set that underpinned French engagement with Rhodesia at this time, whilst Chapter Two addresses how this mind-set operated in practice. The remaining three chapters explore the evolution of France’s presence in this British colony in the fourteen and a half years following the white settlers’ Unilateral Declaration of Independence. Chapter Three sets out the particularities of the post-1965 context, in terms of France’s foreign policy agenda and the situation on the ground in Central Southern Anglophone Africa. Chapter Four analyses how the policies of state and non-state French actors were implemented in Rhodesia after 1965, and Chapter Five assesses the impact of these policies for France’s relations with Africa, Britain and the United States, as well as for the end of European rule in Rhodesia. -

Zimbabwe News, Vol. 25, No. 4

Zimbabwe News, Vol. 25, No. 4 http://www.aluka.org/action/showMetadata?doi=10.5555/AL.SFF.DOCUMENT.nuzr19942504 Use of the Aluka digital library is subject to Aluka’s Terms and Conditions, available at http://www.aluka.org/page/about/termsConditions.jsp. By using Aluka, you agree that you have read and will abide by the Terms and Conditions. Among other things, the Terms and Conditions provide that the content in the Aluka digital library is only for personal, non-commercial use by authorized users of Aluka in connection with research, scholarship, and education. The content in the Aluka digital library is subject to copyright, with the exception of certain governmental works and very old materials that may be in the public domain under applicable law. Permission must be sought from Aluka and/or the applicable copyright holder in connection with any duplication or distribution of these materials where required by applicable law. Aluka is a not-for-profit initiative dedicated to creating and preserving a digital archive of materials about and from the developing world. For more information about Aluka, please see http://www.aluka.org Zimbabwe News, Vol. 25, No. 4 Alternative title Zimbabwe News Author/Creator Zimbabwe African National Union Publisher Zimbabwe African National Union (Harare, Zimbabwe) Date 1994-07-00 Resource type Magazines (Periodicals) Language English Subject Coverage (spatial) Zimbabwe, United Kingdom, China Coverage (temporal) 1994 Rights By kind permission of ZANU, the Zimbabwe African National Union Patriotic Front. Description EDITORIAL. LETTERS. NATIONAL NEWS: Government committed to black economic empowerment. Zimbabwe committed to achieving convertibility of Z$. -

Iata Three Digits Awb Airline Prefix and Two Letters Codes for All Major Airlines

SEPTEMBER 18, 2019 IATA THREE DIGITS AWB AIRLINE PREFIX AND TWO LETTERS CODES FOR ALL MAJOR AIRLINES The most comprehensive list of IATA Air Waybill Prefix and two letters code for virtually all operational airlines. Airline Name IATA AWB Prefix Country Etihad Airways Crystal Cargo EY 607 Abu Dhabi Ariana Afghan Airlines FG 255 Afghanistan Ada Air ZY 121 Albania Albanian Airlines LV 639 Albania Air Algerie AH 124 Algeria Tassili Airlines SF 515 Algeria TAAG Angola Airlines DT 118 Angola LIAT (1974) LI 140 Antigua & Barbuda Air Plus Argentina U3 017 Argentina Lineas Aereas Del Estado 5U 022 Argentina Aerolineas Argentinas AR 044 Argentina LAPA Lineas Aereas Privadas Argentinas MJ 069 Argentina Austral Lineas Aereas AU 143 Argentina Southern Winds A4 242 Argentina STAF Airlines FS 278 Argentina Dinar Lineas Aereas D7 429 Argentina LAN Argentina 4M 469 Argentina American Falcon WK 676 Argentina Armavia U8 669 Armenia Airline Name IATA AWB Prefix Country Armenian International Airways MV 904 Armenia Air Armenia QN 907 Armenia Armenian Airlines R3 956 Armenia Jetstar JQ 041 Australia Flight West Airlines YC 060 Australia Qantas Freight QF 081 Australia Impulse Airlines VQ 253 Australia Macair Airlines CC 374 Australia Australian Air Express XM 524 Australia Skywest Airlines XR 674 Australia Kendell Airlines KD 678 Australia East West Airlines EW 804 Australia Regional Express ZL 899 Australia Airnorth Regional TL 935 Australia Lauda Air NG 231 Austria Austrian Cargo OS 257 Austria Eurosky Airlines JO 473 Austria Air Alps A6 527 Austria Eagle