Appendix D: Sh&E Forecast of Operations for 2007

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Airline Schedules

Airline Schedules This finding aid was produced using ArchivesSpace on January 08, 2019. English (eng) Describing Archives: A Content Standard Special Collections and Archives Division, History of Aviation Archives. 3020 Waterview Pkwy SP2 Suite 11.206 Richardson, Texas 75080 [email protected]. URL: https://www.utdallas.edu/library/special-collections-and-archives/ Airline Schedules Table of Contents Summary Information .................................................................................................................................... 3 Scope and Content ......................................................................................................................................... 3 Series Description .......................................................................................................................................... 4 Administrative Information ............................................................................................................................ 4 Related Materials ........................................................................................................................................... 5 Controlled Access Headings .......................................................................................................................... 5 Collection Inventory ....................................................................................................................................... 6 - Page 2 - Airline Schedules Summary Information Repository: -

APR 2009 Stats Rpts

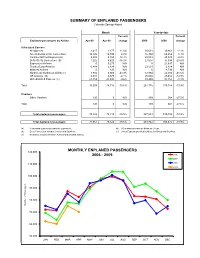

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Apr-09 Apr-08 change 2009 2008 change Scheduled Carriers Allegiant Air 2,417 2,177 11.0% 10,631 10,861 -2.1% American/American Connection 14,126 14,749 -4.2% 55,394 60,259 -8.1% Continental/Cont Express (a) 5,808 5,165 12.4% 22,544 23,049 -2.2% Delta /Delta Connection (b) 7,222 8,620 -16.2% 27,007 37,838 -28.6% ExpressJet Airlines 0 5,275 N/A 0 21,647 N/A Frontier/Lynx Aviation 6,888 2,874 N/A 23,531 2,874 N/A Midwest Airlines 0 120 N/A 0 4,793 N/A Northwest/ Northwest Airlink (c) 3,882 6,920 -43.9% 12,864 22,030 -41.6% US Airways (d) 6,301 6,570 -4.1% 25,665 29,462 -12.9% United/United Express (e) 23,359 25,845 -9.6% 89,499 97,355 -8.1% Total 70,003 78,315 -10.6% 267,135 310,168 -13.9% Charters Other Charters 120 0 N/A 409 564 -27.5% Total 120 0 N/A 409 564 -27.5% Total enplaned passengers 70,123 78,315 -10.5% 267,544 310,732 -13.9% Total deplaned passengers 71,061 79,522 -10.6% 263,922 306,475 -13.9% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

MAR 2009 Stats Rpts

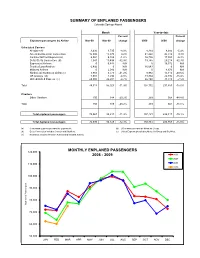

SUMMARY OF ENPLANED PASSENGERS Colorado Springs Airport Month Year-to-date Percent Percent Enplaned passengers by Airline Mar-09 Mar-08 change 2009 2008 change Scheduled Carriers Allegiant Air 3,436 3,735 -8.0% 8,214 8,684 -5.4% American/American Connection 15,900 15,873 0.2% 41,268 45,510 -9.3% Continental/Cont Express (a) 6,084 6,159 -1.2% 16,736 17,884 -6.4% Delta /Delta Connection (b) 7,041 10,498 -32.9% 19,785 29,218 -32.3% ExpressJet Airlines 0 6,444 N/A 0 16,372 N/A Frontier/Lynx Aviation 6,492 0 N/A 16,643 0 N/A Midwest Airlines 0 2,046 N/A 0 4,673 N/A Northwest/ Northwest Airlink (c) 3,983 6,773 -41.2% 8,982 15,110 -40.6% US Airways (d) 7,001 7,294 -4.0% 19,364 22,892 -15.4% United/United Express (e) 24,980 26,201 -4.7% 66,140 71,510 -7.5% Total 74,917 85,023 -11.9% 197,132 231,853 -15.0% Charters Other Charters 150 188 -20.2% 289 564 -48.8% Total 150 188 -20.2% 289 564 -48.8% Total enplaned passengers 75,067 85,211 -11.9% 197,421 232,417 -15.1% Total deplaned passengers 72,030 82,129 -12.3% 192,861 226,953 -15.0% (a) Continental Express provided by ExpressJet. (d) US Airways provided by Mesa Air Group. (b) Delta Connection includes Comair and SkyWest . (e) United Express provided by Mesa Air Group and SkyWest. -

Annual Report 2000

Northwest Northwest Annual Report Airlines Corporation Corporation Annual Report 2000 Northwest Airlines Corporation 5101 Northwest Drive St. Paul, MN 55000-3034 www.nwa.com ©2000 Northwest Airlines Corporation 2000 Northwest Airlines Annual Report 2000 CONDENSED FINANCIAL HIGHLIGHTS Northwest Airlines Corporation Year Ended December 31 Percent (Dollars in millions, except per share data) 2000 1999 Change FINANCIALS Operating Revenues $ 11,415 $ 10,276 11.1 Operating Expenses 10,846 9,562 13.4 Operating Income $ 569 $ 714 Operating Margin 5.0% 6.9% (1.9)pts. Net Income $ 256 $ 300 Our cover depicts the new Detroit terminal, Earnings Per Common Share: due to open in 2001. Basic $ 3.09 $ 3.69 Diluted $ 2.77 $ 3.26 Number of Common Shares Outstanding (millions) 85.1 84.6 NORTHWEST AIRLINES is the world’s fourth largest airline with domestic hubs in OPERATING STATISTICS Detroit, Minneapolis/St. Paul and Memphis, Asian hubs in Tokyo and Osaka, and a Scheduled Service: European hub in Amsterdam. Northwest Airlines and its alliance partners, including Available Seat Miles (ASM) (millions) 103,356 99,446 3.9 Continental Airlines and KLM Royal Dutch Airlines, offer customers a global airline Revenue Passenger Miles (RPM) (millions) 79,128 74,168 6.7 network serving more than 785 cities in 120 countries on six continents. Passenger Load Factor 76.6% 74.6% 2.0 pts. Revenue Passengers (millions) 58.7 56.1 4.6 Table of Contents Revenue Yield Per Passenger Mile 12.04¢ 11.58¢ 4.0 Passenger Revenue Per Scheduled ASM 9.21¢ 8.64¢ 6.6 To Our Shareholders . -

May 2011 to April 2012

Metropolitan Washington Airports Authority Washington Dulles International Airport Periodic Summary Report Total Passengers by Airline May 2011 - April 2012 Airline May - 11 Jun - 11 Jul - 11 Aug - 11 Sep - 11 Oct - 11 Nov - 11 Dec - 11 Jan - 12 Feb - 12 Mar - 12 Apr - 12 Total Air Carrier - Scheduled Aer Lingus 12,623 13,751 14,640 13,186 11,698 10,210 4,856 7,179 4,547 2,858 8,513 8,600 112,661 AeroSur 408 2,080 1,846 973 509 582 1,890 2,110 1,523 1,331 13,252 Aeroflot 1,417 1,904 1,628 1,610 1,761 1,238 1,089 1,683 1,421 986 1,667 1,315 17,719 Air France 27,793 36,649 41,790 40,354 33,502 32,417 25,303 27,774 22,764 13,445 24,577 27,332 353,700 AirTran 20,789 18,703 20,034 20,515 15,353 16,692 15,361 12,571 10,681 9,547 10,698 14,528 185,472 All Nippon 11,354 12,363 13,009 12,691 10,943 12,170 11,085 11,906 12,257 9,625 12,643 11,534 141,580 American 74,384 77,450 80,041 78,689 66,938 71,256 69,263 65,220 61,106 56,849 74,369 71,901 847,466 Austrian 11,662 11,848 12,089 11,135 12,345 11,443 8,990 9,675 7,652 7,169 10,907 11,914 126,829 Avianca 4,088 4,540 4,954 4,820 3,711 3,620 3,647 5,543 5,601 4,534 5,944 6,020 57,022 British Airways 37,374 37,522 38,244 37,826 35,128 34,813 29,423 31,867 28,467 19,917 32,881 37,066 400,528 COPA 7,026 6,340 6,904 6,093 5,224 5,131 6,165 6,946 6,972 5,865 6,926 6,133 75,725 Cayman 512 423 518 896 459 2,808 Continental 17,527 24,688 19,117 23,336 27,182 33,415 29,279 27,787 21,398 22,415 42,489 86,064 374,697 Delta 66,469 63,197 66,710 65,269 51,356 59,250 51,226 37,422 41,610 40,342 47,887 53,036 -

WASHINGTON AVIATION SUMMARY March 2009 EDITION

WASHINGTON AVIATION SUMMARY March 2009 EDITION CONTENTS I. REGULATORY NEWS................................................................................................ 1 II. AIRPORTS.................................................................................................................. 5 III. SECURITY AND DATA PRIVACY ……………………… ……………………….……...7 IV. E-COMMERCE AND TECHNOLOGY......................................................................... 9 V. ENERGY AND ENVIRONMENT............................................................................... 10 VI. U.S. CONGRESS...................................................................................................... 13 VII. BILATERAL AND STATE DEPARTMENT NEWS .................................................... 15 VIII. EUROPE/AFRICA..................................................................................................... 16 IX. ASIA/PACIFIC/MIDDLE EAST .................................................................................18 X. AMERICAS ............................................................................................................... 19 For further information, including documents referenced, contact: Joanne W. Young Kirstein & Young PLLC 1750 K Street NW Suite 200 Washington, D.C. 20006 Telephone: (202) 331-3348 Fax: (202) 331-3933 Email: [email protected] http://www.yklaw.com The Kirstein & Young law firm specializes in representing U.S. and foreign airlines, airports, leasing companies, financial institutions and aviation-related -

87110000 GREATER ORLANDO AVIATION AUTHORITY JP Morgan

NEW ISSUE – BOOK-ENTRY ONLY RATINGS: See “RATINGS” herein In the opinion of Co-Bond Counsel, under existing statutes, regulations, rulings and court decisions, assuming continuing compliance with certain tax covenants and the accuracy of certain representations of the Authority (as defined below), interest on the Series 2009C Bonds (as defined below) will be excludable from gross income for federal income tax purposes, except interest on a Series 2009C Bond for any period during which that Series 2009C Bond is held by a “substantial user” or a “related person” as those terms are used in Section 147(a) of the Internal Revenue Code of 1986, as amended. Interest on the Series 2009C Bonds will not be an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations and will not be taken into account in determining adjusted current earnings for purposes of the alternative minimum tax imposed on corporations. See “TAX MATTERS” herein for a description of certain other federal tax consequences of ownership of the Series 2009C Bonds. Co-Bond Counsel is further of the opinion that the Series 2009C Bonds and the interest thereon will not be subject to taxation under the laws of the State of Florida, except as to estate taxes and taxes imposed by Chapter 220, Florida Statutes, on interest, income or profits on debt obligations owned by corporations, as defined in Chapter 220. For a more complete discussion of certain tax aspects relating to the Series 2009C Bonds, see “TAX MATTERS” herein. $87,110,000 -

Trans States Holdings Signed Purchase Agreement with Mitsubishi Aircraft for 100 MRJ Aircraft on Dec 27, 2010 TSH President Richard A

MRJ Newsletter Trans States Holdings Signed Purchase Agreement with Mitsubishi Aircraft for 100 MRJ Aircraft on Dec 27, 2010 TSH President Richard A. Leach Attends Reception Ceremony held in Nagoya February 01,2011 Mitsubishi Aircraft Corporation finalized and executed a definitive Purchase Agreement with Trans States Holdings (TSH) for an order of 100 next- generation Mitsubishi Regional Jet (MRJ) aircraft (50 firm, 50 options) on December 27, 2010. TSH President Richard A. Leach visited Japan to attend the reception ceremony held on February 1st 2011 in Nagoya celebrating the definitive Purchase Agreement. Since the announcement of the LOI in October 2009, TSH and Mitsubishi Aircraft have been constantly exchanging views and strengthening the relationship. Both parties are pleased to conclude the definitive Purchase Agreement of the MRJ – the game-changing next- generation regional jet. Mr. Wigmore, CFO of TSH (left); Egawa, President of Mitsubishi Aircraft Corporation (center); Mr. Leach, President of TSH (right) TSH, based in St. Louis, Missouri, is an airline holding company that owns and operates three independent airlines, Trans States Airlines, GoJet Airlines, and Compass Airlines, all of which have significant regional operations in North America. TSH is entrusted with feeder services for United Airlines, Delta Air Lines, and US Airways. TSH President Richard A. Leach said, “We have been very excited about the MRJ program for a long time, and we are extremely pleased to conclude this major order on December 27 last year reaffirming the 100 aircraft commitment we made with our LOI. Since that launch order, we have learned a lot about the quality of the Mitsubishi Aircraft team and the quality of the MRJ aircraft. -

General Aviation Activity and Airport Facilities

New Hampshire State Airport System Plan Update CHAPTER 2 - AIRPORT SYSTEM INVENTORY 2.1 INTRODUCTION This chapter describes the existing airport system in New Hampshire as of the end of 2001 and early 2002 and served as the database for the overall System Plan. As such, it was updated throughout the course of the study. This Chapter focuses on the aviation infrastructure that makes up the system of airports in the State, as well as aviation activity, airport facilities, airport financing, airspace and air traffic services, as well as airport access. Chapter 3 discusses the general economic conditions within the regions and municipalities that are served by the airport system. The primary purpose of this data collection and analysis was to provide a comprehensive overview of the aviation system and its key elements. These elements also served as the basis for the subsequent recommendations presented for the airport system. The specific topics covered in this Chapter include: S Data Collection Process S Airport Descriptions S Airport Financing S Airport System Structure S Airspace and Navigational Aids S Capital Improvement Program S Definitions S Scheduled Air Service Summary S Environmental Factors 2.2 DATA COLLECTION PROCESS The data collection was accomplished through a multi-step process that included cataloging existing relevant literature and data, and conducting individual airport surveys and site visits. Division of Aeronautics provided information from their files that included existing airport master plans, FAA Form 5010 Airport Master Records, financial information, and other pertinent data. Two important element of the data collection process included visits to each of the system airports, as well as surveys of airport managers and users. -

Columbus Regional Airport Authority

COLUMBUS REGIONAL AIRPORT AUTHORITY - PORT COLUMBUS INTERNATIONAL AIRPORT TRAFFIC REPORT August, 2008 9/30/2008 Airline Enplaned Passengers Deplaned Passengers Enplaned Air Mail Deplaned Air Mail Enplaned Air Freight Deplaned Air Freight Landings Landing Weight Air Canada Jazz - Regional 1,943 2,186 0 0 0 0 101 3,437,000 Air Canada Jazz Totals 1,943 2,186 0 0 0 0 101 3,437,000 American 13,470 13,202 32,251 13,553 5 476 119 14,781,000 American Connection - Chautauqua 3,413 3,351 0 0 0 0 93 3,834,900 American Eagle 20,065 21,086 0 0 5,384 2,947 595 26,252,005 American Totals 36,948 37,639 32,251 13,553 5,389 3,423 807 44,867,905 Continental 8,425 8,813 22,955 21,807 8,205 39,697 104 11,770,000 Continental Express - Chautauqua 4,875 5,244 0 0 810 0 121 5,561,000 Continental Express - Colgan 828 711 0 0 0 0 24 1,488,000 Continental Express - CommutAir 2,128 1,735 0 0 0 0 83 2,863,500 Continental Express - ExpressJet 2,671 3,029 0 0 121 1,821 83 3,572,786 Continental Totals 18,927 19,532 22,955 21,807 9,136 41,518 415 25,255,286 Delta 11,808 11,455 0 0 8,944 29,855 91 10,345,000 Delta Connection - Atlantic SE 3,189 3,043 0 0 372 0 60 3,260,000 Delta Connection - Chautauqua 11,439 12,415 0 0 0 0 304 12,881,976 Delta Connection - Comair 9,195 9,999 0 0 436 556 225 11,635,000 Delta Connection - Mesa/Freedom 0 0 0 0 0 0 0 0 Delta Connection - Shuttle America 4,812 4,736 0 0 0 0 80 5,821,858 Delta Connection - Skywest 1,600 1,580 0 0 0 0 25 1,875,000 Delta Totals 42,043 43,228 0 0 9,752 30,411 785 45,818,834 JetBlue 0 0 0 0 0 0 0 0 JetBlue Totals -

INTERNATIONAL CONFERENCE on AIR LAW (Montréal, 20 April to 2

DCCD Doc No. 28 28/4/09 (English only) INTERNATIONAL CONFERENCE ON AIR LAW (Montréal, 20 April to 2 May 2009) CONVENTION ON COMPENSATION FOR DAMAGE CAUSED BY AIRCRAFT TO THIRD PARTIES AND CONVENTION ON COMPENSATION FOR DAMAGE TO THIRD PARTIES, RESULTING FROM ACTS OF UNLAWFUL INTERFERENCE INVOLVING AIRCRAFT (Presented by the Air Crash Victims Families Group) 1. INTRODUCTION – SUPPLEMENTAL AND OTHER COMPENSATIONS 1.1 The apocalyptic terrorist attack by the means of four hi-jacked planes committed against the World Trade Center in New York, NY , the Pentagon in Arlington, VA and the aborted flight ending in a crash in the rural area in Shankville, PA ON September 11th, 2001 is the only real time example that triggered this proposed Convention on Compensation for Damage to Third Parties from Acts of Unlawful Interference Involving Aircraft. 1.2 It is therefore important to look towards the post incident resolution of this tragedy in order to adequately and pro actively complete ONE new General Risk Convention (including compensation for ALL catastrophic damages) for the twenty first century. 2. DISCUSSION 2.1 Immediately after September 11th, 2001 – the Government and Congress met with all affected and interested parties resulting in the “Air Transportation Safety and System Stabilization Act” (Public Law 107-42-Sept. 22,2001). 2.2 This Law provided the basis for Rules and Regulations for: a) Airline Stabilization; b) Aviation Insurance; c) Tax Provisions; d) Victims Compensation; and e) Air Transportation Safety. DCCD Doc No. 28 - 2 - 2.3 The Airline Stabilization Act created the legislative vehicle needed to reimburse the air transport industry for their losses of income as a result of the flight interruption due to the 911 attack. -

Saab 340 the VERSATILE TURBOPROP Saab 340 > the Versatile TURBOPROP

SAAB 340 THE VERSATILE TURBOPROP SAAB 340 > THE VERSATILE TURBOPROP 2 SAAB 340 > THE VERSATILE TURBOPROP ”WE ARE A NICHE MARKET operator...THE SAAB 340 IS A WORKHORSE AIRCRAFT AND very RELIABLE.” GEORG POMMER ROBIN HOOD Aviation CEO THE FLEXIBLE PERFORMER To safeguard against today’s rapidly changing environment and improve profitability, successful airlines must choose an aircraft that minimizes risk and is adaptable to an ever-changing market environment. In addition, passengers demand comfort and service similar to that offered by major carriers. The Saab 340 is a favorite among airline passengers due to its flexibility, comfort and reliable performance. With about half the operating costs of a regional jet, the Saab 340 can offer service in a variety of markets, large or small. RELIABILITY IN A VARIETY OF OPERATIONS The cost-effective Saab 340 consistently generates profits for a wide range of regional air transport services. With the right blend of technologies, the Saab 340 combines high productivity with dependability. THE “FACTS” @ 4Q – 2009 • 25-year track record • best selling 30-seat turboprop • more than 410 operational aircraft found on six continents and in 30 countries • over 13 million hours flown and an estimated 250 million passengers • consistent 99% dispatch reliability • award winning customer support services 3 SAAB 340 > THE VERSATILE TURBOPROP THE BIG AIRLINE CHOICE 4 SAAB 340 > THE VERSATILE TURBOPROP WORLD’S LARGEST 340BPLUS OPERATOR ”...OUR OVERALL OBJECTIVE IS TO PROVIDE A SEAMLESS The red, white and blue Delta livery is replacing Northwest colors service PRODUCT TO OUR on all aircraft and airport signage as the newly merged airline is passengers.