RESTRICTED WT/TPR/S/310 19 January 2015 (15-0296) Page

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

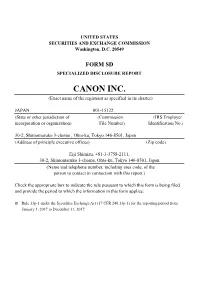

CANON INC. (Exact Name of the Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM SD SPECIALIZED DISCLOSURE REPORT CANON INC. (Exact name of the registrant as specified in its charter) JAPAN 001-15122 (State or other jurisdiction of (Commission (IRS Employer incorporation or organization) File Number) Identification No.) 30-2, Shimomaruko 3-chome , Ohta-ku, Tokyo 146-8501, Japan (Address of principle executive offices) (Zip code) Eiji Shimizu, +81-3-3758-2111, 30-2, Shimomaruko 3-chome, Ohta-ku, Tokyo 146-8501, Japan (Name and telephone number, including area code, of the person to contact in connection with this report.) Check the appropriate box to indicate the rule pursuant to which this form is being filed and provide the period to which the information in this form applies: Rule 13p-1 under the Securities Exchange Act (17 CFR 240.13p-1) for the reporting period from January 1, 2017 to December 31, 2017. Section 1 - Conflict Minerals Disclosure Established in 1937, Canon Inc. is a Japanese corporation with its headquarters in Tokyo, Japan. Canon Inc. is one of the world’s leading manufacturers of office multifunction devices (“MFDs”), plain paper copying machines, laser printers, inkjet printers, cameras, diagnostic equipment and lithography equipment. Canon Inc. earns revenues primarily from the manufacture and sale of these products domestically and internationally. Canon Inc. and its consolidated companies fully have been aware of conflict minerals issue and have been working together with business partners and industry entities to address the issue of conflict minerals. In response to Rule 13p-1, Canon Inc. conducted Reasonable Country of Origin Inquiry and due diligence based on the “OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas,” for its various products. -

Places of Employment of Graduates from Faculty/Graduate School (Master's Program) (FY2015)

Places of Employment of Graduates from Faculty/Graduate School (Master's Program) (FY2015) Faculty of Letters/Graduate School of Humanities ● Sumitomo Mitsui Banking Corp. ● Nippon Life Insurance Co. ● Osaka Customs ● Sumitomo Mitsui Trust Bank, Ltd. ● Teacher (JH&HS) ● Kobe Customs ● The Bank of Tokyo-Mitsubishi UFJ, Ltd. ● Hyogo Prefectural High School ● Kobe City Office ● Bank of Japan ● Osaka Regional Taxation Bureau ● Toyonaka City Office ● Japan Post Bank Co., Ltd. ● Japan MINT ● Hiroshima Home Television Co.,Ltd. ● Mizuho Securities Co., Ltd. ● Ministry of Education, Culture, Sports, Science and Technology ● Japan Broadcasting Corporation ● Daiwa Securities Co., Ltd. ● Osaka Public Prosecutors Office ● Kobe Steel,Ltd. ● Japan Post Insurance Co.,Ltd. ● Kobe District Court ● Mitsubishi Electric Corp. Faculty of Intercultural Studies/Graduate School of Intercultural Studies ● Ministry of Foreign Affairs of Japan ● Nippon Life Insurance Company ● Toyota Motor Corp. ● Osaka Immigration Bureau ● SUMITOMO LIFE INSURANCE COMPANY ● KANEKA CORPORATION ● Kansai Bureau of Economy ● Sumitomo Mitsui Banking Corp. ● Mitsubishi Electric Corp. ● Tokyo Metropolitan Government ● Resona Bank, Ltd. ● New Kansai International Airport Co., Ltd. ● Kobe City Office ● Mizuho Bank, Ltd. ● Daiwa Institute of Research Ltd. ● Hyogo Prefectural Museum of Art ● The Bank of Tokyo-Mitsubishi UFJ, Ltd. ● TAISEI CORPORATION ● Kansai Telecasting Corporation ● Tokyo Electric Power Company Holdings, Inc. ● Kobe Steel,Ltd. ● Japan Broadcasting Corp. ● THE KANSAI ELECTRIC POWER Co., INC. ● Hitachi, Ltd. Faculty of Human Development/Graduate School of Human Development and Environment ● Suntory Holdings Ltd. ● Mitsubishi Corp. ● Hyogo Prefectural High school ● ASICS Corp. ● Mizuho Bank, Ltd. ● Osaka Prefectural High school ● Kobe Steel,Ltd. ● The Bank of Tokyo-Mitsubishi UFJ, Ltd. ● Ministry of Health, Labour and Welfare ● Murata Manufacturing Co., Ltd. -

Japanese Business Concepts You Should Know

1 Japanese Business Concepts You Should Know Edited by Parissa Haghirian Sophia University Tokyo, Japan 2 Contents About this Book ......................................................................................... 4 The Editor ................................................................................................ 5 Japanese Business Concepts You Should Know ................................................. 6 Contributors of This Book ............................................................................ 94 Bibliography ............................................................................................ 96 Further Reading on Japanese Management .................................................... 102 3 About this Book This book is the result of one of my “Management in Japan” classes held at the Faculty of Liberal Arts at Sophia University in Tokyo. Students wrote this dictionary entries, I edited and updated them. The document is now available as a free e-book at my homepage www.haghirian.com. We hope that this book improves understanding of Japanese management and serves as inspiration for anyone interested in the subject. Questions and comments can be sent to [email protected]. Please inform the editor if you plan to quote parts of the book. Japanese Business Concepts You Should Know Edited by Parissa Haghirian First edition, Tokyo, October 2019 4 The Editor Parissa Haghirian is Professor of International Management at Sophia University in Tokyo. She lives and works in Japan since 2004 -

Rhetoric of Young Non-Regular Workers in Post-Bubble Japan: a Genealogical Analysis" (2015)

Wayne State University Wayne State University Dissertations 1-1-2015 Rhetoric Of Young Non-Regular Workers In Post- Bubble Japan: A Genealogical Analysis Noriaki Tajima Wayne State University, Follow this and additional works at: https://digitalcommons.wayne.edu/oa_dissertations Part of the Communication Commons, and the Rhetoric Commons Recommended Citation Tajima, Noriaki, "Rhetoric Of Young Non-Regular Workers In Post-Bubble Japan: A Genealogical Analysis" (2015). Wayne State University Dissertations. 1364. https://digitalcommons.wayne.edu/oa_dissertations/1364 This Open Access Dissertation is brought to you for free and open access by DigitalCommons@WayneState. It has been accepted for inclusion in Wayne State University Dissertations by an authorized administrator of DigitalCommons@WayneState. RHETORIC OF YOUNG NON-REGULAR WORKERS IN POST-BUBBLE JAPAN: A GENEALOGICAL ANALYSIS by NORIAKI TAJIMA DISSERTATION Submitted to the Graduate School of Wayne State University, Detroit, Michigan in partial fulfillment of the requirements for the degree of DOCTOR OF PHILOSOPHY 2015 MAJOR: COMMUNICATION Approved By: Advisor Date © COPYRIGHT BY NORIAKI TAJIMA 2015 All Rights Reserved ACKNOWLEDGMENTS This work, the work on pain, struggles and hope, has been soulful for me. So I am very thankful to a number of people who have been involved in the process of developing it. First and foremost, I appreciate Dr. Kelly Young. This work is successfully at this point thanks to his careful examination of a number of past drafts. Even though Kelly was not originally my adviser, he has always welcomed students like me and become an important source of insights, inspirations and encouragements. Like many other students of him, I also profoundly appreciate his smart intelligence and fun-loving, warm-hearted personality. -

Guide to Japan's Flow of Funds Accounts

Guide to Japan's Flow of Funds Accounts Research and Statistics Department Bank of Japan Introduction The Bank of Japan has been compiling the Flow of Funds Accounts Statistics (the FFA) since 1958, covering the data from 1954. The FFA is released quarterly; preliminary data is released about three months later, and revised data about six months later. In principle, the FFA is revised retroactively once a year. The FFA is a matrix showing financial transactions among various economic entities, and corresponding stock data on financial claims and liabilities of them. It records movements of financial assets and liabilities among institutional units called sectors, such as financial institutions, corporations and households, for each financial instrument called transaction items such as deposits and loans. Being extremely detailed and having wide coverage, the FFA is very useful, but on the other hand, it sometimes adopts unique principles and concepts, and has original definition of sectors and transactions items. Therefore, in using the FFA, it is necessary to accurately understand its features. To help users fulfill their needs better, the Research and Statistics Department publishes a booklet explaining the overall concept of the FFA; it also defines individual sectors and items. The booklet is comprised of the following chapters. The first chapter outlines the FFA, and chapter two explains considerations to be made from a statistical viewpoint. Then, chapter three and four describe definition and scope of each figure by sectors and by transaction items. Compilation method of the FFA is outlined in chapter five. Chapter six details the relationship between the FFA and other statistics in order to provide better understanding of the framework of the FFA. -

AZSA Quality 2019 Initiatives for Enhancing Audit Quality

AZSA Quality 2019 Initiatives for Enhancing Audit Quality October 2019 home.kpmg/jp/azsa Contents Message from our CEO 2 TOPICS KPMG AZSA’s Digital Strategy 4 Initiatives for the Digitalization of Audit 10 Structure and Initiatives Supporting Audit Quality 14 Our Initiatives for Audit Quality viewed from AQI 16 I. Organizational Foundation 18 II. System of Quality Control 26 III. Human Resource Development 44 IV. KPMG Network 50 V. Corporate Overview 55 VI. Compliance with the Audit Firm Governance Code 60 © 2020 KPMG AZSA LLC, a limited liability audit corporation incorporated under the Japanese Certified Public Accountants Law and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. AZSA Quality 2019 Initiatives for Enhancing Audit Quality 1 Message Message from our CEO Marking our 50th anniversary Digital Innovation (DI) as a new division within KPMG AZSA, which will focus on solution development. We In July 2019 KPMG AZSA marked the 50th anniversary also incorporated KPMG Ignition Tokyo, Inc. (KIT) as our of its foundation. Over these past 50 years, we have subsidiary. KIT will lead the development of platforms adapted to an evolving economic environment and using cutting-edge technologies. We are confident striven to earn the trust of the capital markets. In that our DI Division and KIT will work together to take recent years, the state of the world has become the lead in continuously identifying and addressing the increasingly complex and transparency is diminishing changing expectations of society. against a backdrop of worldwide political and economic changes. -

Japan Mint World Money Fair 2020 Coin

EHRENGAST GUEST OF HONOR JAPAN MINT MESSEKATALOG FAIR CATALOG 1 ALLGEMEINE INFORMATIONEN FIRMENPRÄSENTATIONEN A–Z PROGRAMM | PROGRAM GENERAL INFORMATION COMPANIES A–Z Ausstellerliste | List of Exhibitors 132 Aichelin Group 85 DIENSTAG | TUESDAY (28.01.2020) 13.30 – 14.30 und Hallenplan | Exhibition Map 146 Allgemeine Gold- und 15.00 – 18.00 Vorbesichtigung | Viewing 15.30 – 16.30 Japanese Calligraphy Performance Impressum | Imprint 145 Silberscheideanstalt AG 74 15. Berlin Auktion Künker Japan Mint (Stand | booth D3 Media Forum 20 Austrian Mint (Münze Österreich AG) 30 (Saal | room Estrel B) 17.00 – 18.30 Empfang | Reception Partner 124 Bank of Greece 34 MITTWOCH | WEDNESDAY (29.01.2020) The Perth Mint ** Programm | Program 3 Berufsverband des Deutschen 10.00 – 18.00 Vorbesichtigung | Viewing 19.00 – 23.00 Gala Dinner ** Sitzungszimmer | Meeting Rooms 84 Münzenfachhandels e. V. 113 15. Berlin Auktion Künker World Money Fair und | and Japan Technical Forum 72 Blockchain Mint 98 (Saal | room Estrel B) Mint (Stand | booth D3) C.Hafner 106 ARTIKEL 18.30 – 21.00 Reception hosted by His Exellency SAMSTAG | SATURDAY (01.02.2020) CDN Publishing – Greysheet 96 Takeshi Yagi, Ambassador of ARTICLE China Gold Coin Incorporation 36 Japan** 10.00 – 12.00 MDC Internal Affairs CIT Coin Invest AG 100 (Raum | room Paris) * »Bronzen wie Tiere. Heide Dobberkau DONNERSTAG | THURSDAY (30.01.2020) und ihre Tierwelten« 108 Gibraltar National Mint 38 10.00 – 18.00 Messe | Trade Fair Heimerle + Meule Group 97 09.00 – 13.00 MDWG Plenary * “Bronzes like animals. Heide Dobberkau (room ECC 4, 2nd floor) 11.00 – 14.00 Weißwurstfrühstück – Bayern LB ** and her animal worlds” 110 Hungarian Mint 39 10.00 – 20.00 15. -

Rice Asian Studies Review

Rice Asian Studies Review Volume 3 2018-19 Issue rasr.rice.edu ABOUT RICE ASIAN STUDIES REVIEW i Asia in the 21st century is undergoing rapid political, economic, and cultural change. As people, goods, ideas, and cultures reverse colonial fow and begin emanating from Asia across the globe, it is clear that the scholarly lens through which Asia has traditionally been approached by Western-trained academics is sorely in need of revision. Te Rice Asian Studies Review (RASR), as an undergraduate Asia- focused academic journal authored, edited, and published by students, situates itself on the front-line of this process by providing a venue for young scholars to exhibit their own ideas and learn from those of their peers. Our goal is produce a compilation of diverse, unconventional, and informed Asian studies perspectives. As authors, editors, and publishers come together in the production of RASR, this fresh cohort of 21st century scholars hopes to promote a dynamic, modern, and interdisciplinary approach to Asian Studies. From left to right: Coleman Lambo, Flora Naylor, Sophie Laferty, Gennifer Geer, and Erin Ye. VOLUME 3, 2018-19 ISSUE PUBLISHED ON APRIL 2019 Website: rasr.rice.edu Email: [email protected] About the cover: Fifty-one nations and territories defned geographically as “Asia” by the United Nations are represented in decreasing order of population. Designed by Justin Park (McMurtry College, 2017). ii ACKNOWLEDGEMENTS Te 2018-19 RASR staf would like to ofer our sincerest gratitude to everyone in the Chao Center for Asian Studies. Tis third edition would not be possible without the intellectual, emotional, and fnancial support of the Center, as well as the generous eforts of Director Dr. -

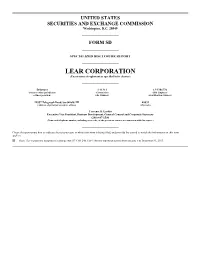

LEAR CORPORATION (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM SD SPECIALIZED DISCLOSURE REPORT LEAR CORPORATION (Exact name of registrant as specified in its charter) Delaware 1-11311 13-3386776 (State or other jurisdiction (Commission (IRS Employer of incorporation) File Number) Identification Number) 21557 Telegraph Road, Southfield, MI 48033 (Address of principal executive offices) (Zip code) Terrence B. Larkin Executive Vice President, Business Development, General Counsel and Corporate Secretary (248) 447-1500 (Name and telephone number, including area code, of the person to contact in connection with this report.) Check the appropriate box to indicate the rule pursuant to which this form is being filed, and provide the period to which the information in this form applies: x Rule 13p-1 under the Securities Exchange Act (17 CFR 240.13p-1) for the reporting period from January 1 to December 31, 2013. Introduction Lear Corporation (“Lear” or the “Company”) is a leading Tier 1 supplier to the global automotive industry. Our business spans all major automotive markets, and we supply seating and electrical distribution systems and related components to virtually every major automotive manufacturer in the world. As of December 31, 2013, we have manufacturing, engineering and administrative capabilities in 36 countries with 226 locations and are continuing to grow our business in all automotive producing regions of the world. Lear is a recognized global leader in complete automotive seat systems and certain key individual component parts. Our seating business consists of the design, engineering, just-in-time assembly and delivery of complete seat systems, as well as the manufacture of all major seat components, including seat structures and mechanisms, seat covers, seat foam and headrests. -

The Vitality and Resilience of Inherited Japanese Houses -100 Years of Shimizu-Gumi Houses-

The Vitality and Resilience of Inherited Japanese Houses -100 Years of Shimizu-gumi Houses- Preface Since its foundation in 1804, residential architecture had been one of the primary business focuses for Shimizu-gumi, the present Shimizu Corporation. Many books have been published to showcase its works, such as Sekkei zushū, jūtaku no maki, ji 1907 nen shi 1923 nen (Drawing collection: house, from 1907 to 1923) and Sekkei zushū, shitsunai narabini kagu dentō no maki, ji 1909 nen shi 1913 nen (Drawing collection: interior, furniture and lighting, from 1909 to 1913). These books feature painted drawings of large houses, which could be considered mansions in the Western sense, designed and built by Shimizu-gumi, and include plans, elevations, development plans, and illustrations of furniture. The books enable the reader to visualize many aspects of mansions in the Meiji era (1868-1912) and Taisho era (1912-1926,) and to understand how these mansions were significant as elements of urban culture. Additionally, an academic work based on these earlier texts was published to commemorate the 60th anniversary of the Housing Research Foundation JUSOKEN: Meiji/Taisho no teitaku, Shimizu-gumi sakusei saishiki-zu no sekai (Mansions in Meiji and Taisho, the world of colored drawings created by Shimizu-gumi, Kashiwashobo, 2009, currently unavailable). This book is the product of joint research by “Shimizu Kensetsu Teitaku Shiryō Kenkyūkai” (Shimizu Corporation Mansion Document Study Group, 2004 to 2009) in the “Jūtaku Shiryō Iinkai” (Committee for historical materials about houses) of Jusoken. For the next phase of study, surveys and research on Jūtaku kenchiku zushū (Residential architecture catalog, 1st volume: 1935, 2nd volume: 1939) should be conducted. -

Foiling the Forgers

Feature SAFETY FIRST Watermark Watermarking is a technique to prevent counterfeiting by producing variations in the thickness of the paper. The watermark has sharp and spatial gradation in its image. Foiling the Forgers Japan’s advanced anti-counterfeiting technologies are beginning to attract the attention of countries around the world. TOSHIO MATSUBARA target cash handling machines. These measures contribute to the extremely small number of counterfeit notes in Japan. Over the past apanese banknotes are loaded with various few years, only a couple of thousand counterfeit anti-counterfeiting measures that can be con- notes have been found annually. firmed in four different ways: by touch, by see- In Japan, banknotes are manufactured by the Jing against the light, by tilting and with tools. National Printing Bureau (NPB). Leveraging its By touch: Lines produced using intaglio print- expertise in banknote printing, NPB has been con- ing can be confirmed by touch. In intaglio printing, tributing to the implementation of a Japan Inter- the ink is raised on the paper surface. The textured national Cooperation Agency (JICA) project called feel and the ultra-fineness of the printed lines are “Strengthening Capacity of the State Bank of Viet- very difficult to reproduce using regular printing and nam in Printing Ink Production.” Based on the proj- color photocopying equipment. By seeing against the light: Watermarks can be confirmed when seen against the light. They include a portrait on the center and vertical black and white bars on the side that are not normally visible. By tilting: Holograms and latent images can be confirmed by tilting. -

Heft 2 3-09.Indd

Herausgegeben im Auftrag der Karl-Lamprecht-Gesellschaft e. V. (KLG) / European Network in Universal and Global History (ENIUGH) von Matthias Middell und Hannes Siegrist Redaktion Gerald Diesener (Leipzig), Andreas Eckert (Berlin), Hartmut Elsenhans (Leipzig), Ulf Engel (Leipzig), Wolfgang Fach (Leipzig), Eckhardt Fuchs (Braunschweig), Frank Hadler (Leipzig), Katharina Middell (Leipzig), Matthias Middell (Leipzig), Hannes Siegrist (Leipzig), Stefan Troebst (Leipzig), Michael Zeuske (Köln) Anschrift der Redaktion Global and European Studies Institute Universität Leipzig Emil-Fuchs-Str. 1 D – 04105 Leipzig Tel.: +49 / (0)341 / 97 30 230 Fax.: +49 / (0)341 / 960 52 61 E-Mail: [email protected] Internet: www.uni-leipzig.de/zhs/comp/ Redaktionssekretärin: Katja Naumann ([email protected]) Comparativ erscheint sechsmal jährlich mit einem Umfang von jeweils ca. 140 Seiten. Einzelheft: 12.00 €; Doppelheft 22.00€; Jahresabonnement 50.00 €; ermäßigtes Abonnement 25.00 €. Für Mitglieder der KLG / ENIUGH ist das Abonne- ment im Mitgliedsbeitrag enthalten. Zuschriften und Manuskripte senden Sie bitte an die Redaktion. Bestellungen richten Sie an den Buchhandel oder direkt an den Verlag. Ein Bestellformular fi nden Sie unter: http://www.uni-leipzig.de/zhs/comp/ Wissenschaftlicher Beirat Gareth Austin (London), Carlo Marco Belfanti (Brescia), Jerry Bentley (Honolulu), Ida Blom (Bergen), Christophe Charle (Paris), Catherine Coquery-Vidrovitch (Paris), Michel Espagne (Paris), Etienne François (Paris / Berlin), Michael Geyer (Chicago), Alberto