PRIVATE EQUITY International

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

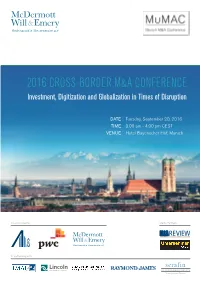

2016 Cross-Border M&A Conference

2016 CROSS-BORDER M&A CONFERENCE Investment, Digitization and Globalization in Times of Disruption DATE Tuesday, September 20, 2016 TIME 9.00 am - 4.00 pm CEST VENUE Hotel Bayerischer Hof, Munich Co-sponsored by Media Partners In partnership with 2016 CROSS-BORDER M&A CONFERENCE Investment, Digitization and Globalization in Times of Disruption US/Europe and Asia/Europe Cross-Border M&A and Activist Shareholders McDermott Will & Emery’s Munich M&A Conference In contrast with 2015, Q1of 2016 was considerably slow- (MuMAC) is celebrating its 6th year. We are looking forward er. M&A activity by deal volume globally was down by 24 to welcoming significant M&A market participants, strategic per cent this year, compared to Q1 of 2015. In the private and private equity investors, and individuals from the advi- equity market, buy-outs were down by 15.3 per cent and sory world to take part in discussions on topics relating to exits by 29.7 per cent over the same period. Was this as a cross-border M&A. result of the markets preparing for the uncertainty surround- ing the United Kingdom’s Brexit Referendum, or a sign of We would very much like to thank in advance our key note something wider? speaker Callum Mitchell-Thomson, Head of Investment Banking Germany for J.P. Morgan Chase & Co., and the MuMAC 2016 is the best place to get answers from experts. many speakers participating in the panel discussions. Come and join us. MuMAC 2016 will cover topics of major significance to the cross-border M&A markets, including regional investment trends in Europe, both from and into Asia and the United States. -

Private Equity in Sweden

PRIVATE EQUITY IN SWEDEN An analysis of the private equity industry in Sweden and two case studies on individual companies’ competitive strategy JOHAN MATTISSON MASTER THESIS LUND UNIVERSITY, 2017 Abstract Private equity is a growing global phenomena and private equity companies have become a major force in many of Sweden’s industries. These companies own portfolio companies which together employs around 190 000 people and have an annual revenue of over 318 billion SEK. The purpose of this thesis was to describe and analyze the Swedish private equity industry and individual companies’ competitive strategy to increase value of portfolio companies and to attract capital. The methodical approach of this thesis was qualitative and abductive. Only public data was used bar the two interviews that was conducted with the case companies. The theoretical framework for the industry analysis was Porters five forces. The case companies were analyzed on the corporate, business and operational levels of strategy. A resource based view was used to further analyze the case companies’ strategic capabilities. The main findings from the industry analysis was that the vast majority of investors in Swedish private equity funds are made by professional institutions and a large amount of the investments were of international origin. The large pool of investors makes it easier for Swedish private equity companies to attract capital. The number of new private equity funds have been declining since 2007 but at the same time the average fund size has grown. There are many differentiating factors between private equity companies. This differentiation is beneficial for the private equity companies as they become less commoditized from the viewpoint of an investor. -

Alternative Investment News November 10, 2008

ain111008 6/11/08 19:18 Page 1 NOVEMBER 1O, 2008 LEHMAN/NOMURA PRIME BROKER VOL. IX, NO. 45 INTEGRATION HITS SYSTEMS SNAG Credit Suisse Cuts Combining the prime brokerage businesses of Nomura FoF Headcount Holdings and Lehman Brothers has reportedly hit a costly and The firm has trimmed 10 staffers from its fund of funds unit, with most of the unexpected snag that could delay full integration for an culled positions based in Europe. undetermined time, potentially stretching to several months or See story, page 9 over a year. An official involved with the merger integration plans told AIN that in Nomura’s acquisition of Lehman’s Asia, India and At Press Time European operations, it received the software for Lehman’s cash Zaragoza Likes Biotechs 2 prime brokerage system—which includes trading, analytics and (continued on page 19) The Americas Nonprofits To Add HFs 4 MELLON SUSPENDS SANCTUARY FUNDS Peloton Pro Sets Up Shop 4 Mellon Global Alternative Investments has suspended dealings on the $344 million Mellon RCG Bullish On Asia 6 Sanctuary Fund and the $426 million Mellon Sanctuary Fund II—its flagship event-driven Startup Readies Managed Account 7 and relative-value funds of hedge funds—as liquidity concerns have arisen from Europe unprecedented volatility in the markets. A number of the underlying funds “have invoked German Shop Revisits Launches 9 provisions that are intended for periods such as this where acute market illiquidity is coupled Pioneer Keen On Green 10 with extreme selling pressure,” stated an email sent to AIN by Spokesman Jamie Brookes. Mulvaney Sees Record Highs 11 (continued on page 20) Asia Pacific EX-FSA EXEC: SMALLER FUNDS NEED Infrastructure Firm Hires Trio 12 CLOSER SUPERVISION Japan Launch Pushed Back 13 The U.K.’s Financial Services Authority should monitor the behaviour of smaller hedge Middle East & Africa fund firms more closely because malpractice is more likely to go unnoticed in these firms. -

ANNUAL REVIEW 2017 Land of the Giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus

ANNUAL REVIEW 2017 Land of the giants Cycle-Tested Credit Expertise Extensive Market Coverage Comprehensive Solutions Relative Value Focus Ares Management is honored to be recognized as Lender of the Year in North America for the fourth consecutive year as well as Lender of the Year in Europe Lender of the year in Europe Ares Management, L.P. (NYSE: ARES) is a leading global alternative asset manager with approximately $106 billion of AUM1 and offices throughout the United States, Europe, Asia and Australia. With more than $70 billion in AUM1 and approximately 235 investment professionals, the Ares Credit Group is one of the largest global alternative credit managers across the non-investment grade credit universe. Ares is also one of the largest direct lenders to the U.S. and European middle markets, operating out of twelve office locations in both geographies. Note: As of December 31, 2017. The performance, awards/ratings noted herein may relate only to selected funds/strategies and may not be representative of any client’s given experience and should not be viewed as indicative of Ares’ past performance or its funds’ future performance. 1. AUM amounts include funds managed by Ivy Hill Asset Management, L.P., a wholly owned portfolio company of Ares Capital Corporation and a registered investment adviser. learn more at: www.aresmgmt.com | www.arescapitalcorp.com The battle of the brands the US market on page 80, advisor Hamilton TOBY MITCHENALL Lane said it had received a record number EDITOR'S of private placement memoranda in 2017 – ISSN 1474–8800 LETTER MARCH 2018 around 800 – and that this, combined with Senior Editor, Private Equity faster fundraising processes, has made it dif- Toby Mitchenall, Tel: +44 207 566 5447 [email protected] ficult to some investors to make considered Special Projects Editor decisions. -

Private Equity

Kuwait Financial Centre “Markaz” P R I V A T E E Q U I T Y U P D A T E Private Equity Month End February, 2008 Market Trends Private Equity update: Compiled from various public - The Private Equity market in 2008 has started off slow, with no sources expectation to pick up quickly. The sluggish start was expected for 2008, so this doesn’t come as a surprise to investors. Total leveraged buy-out volume so far in 2008 is down to $34 billion, two-thirds of the volume at this time the previous year. A single mega-deal from 2007 eclipses the total buy-out volume for 2008. While the level of activity has been slow-moving, the industry is still sitting on $820 billion of uncalled capital from investors. The average size of buy-outs this year, $120 million, is the lowest since 2001. - For the average private equity firm, about 38 individuals are employed for every $1 billion of assets under management, and this number decreases to 15 or less at many of the larger firms. With this type of a work force, it will prove influential since $10 billion buy-outs occur daily. However, if the investors deploy the funds across an array of smaller deals, it will result in longer waiting periods, as well as smaller returns. - Investors in the real estate market in 2008 are the most optimistic, due to predictions of higher or the same returns for this year. Investors intend on using the same type of strategy for deals in 2008. -

2018.Pdf 1 11/4/18 9:17

AF_Cub-Anuario-ASCRI-2018.pdf 1 11/4/18 9:17 C M Y CM MY CY CMY K Anuario 2018 Directory Patrocinado por / Sponsored by: ANUARIO ASCRI 2018 Todos los derechos reservados ASCRI: Príncipe de Vergara, 55, 4ºD. 28006 Madrid DISEÑO EXTERIOR: Atela Comunicación Corporativa DISEÑO INTERIOR: Zingular FOTOMECÁNICA: Zingular IMPRENTA: Zingular 2 sumario / index CARTA DEL DIRECTOR GENERAL DE ASCRI 4 ASCRI Managing Director´s Letter QUÉ ES ASCRI 7 7 What is ASCRI PRIMEROS RESULTADOS DEL AÑO 2017 14 First results for the 2017 exercise LISTA DE ENTIDADES DE CAPITAL PRIVADO ORIENTADAS A INVERTIR EN VENTURE CAPITAL 26 Venture Capital entities LISTA DE ENTIDADES DE CAPITAL PRIVADO ORIENTADAS A CAPITAL EXPANSIÓN Y ÚLTIMAS ETAPAS DE INVERSIÓN 38 Private Equity entities DISTRIBUCIÓN GEOGRÁFICA DE LAS ENTIDADES DE VENTURE CAPITAL & PRIVATE EQUITY SOCIAS DE ASCRI 44 Geographical location of Venture Capital & Private Equity entities (ASCRI members) ÍNDICE DE TÉRMINOS QUE CONTIENEN LAS FICHAS 47 Index of terms included in this directory SOCIOS GESTORES 48 General Partners Members SOCIOS INVERSORES 150 Limited Partners Members SOCIOS ASESORES 160 Advisory Members LISTA DE PROFESIONALES DE LOS SOCIOS GESTORES E INVERSORES POR ENTIDAD 222 General Partners and Limited Partners Professionals listed by entity LISTA DE PROFESIONALES DE LOS SOCIOS GESTORES E INVERSORES POR APELLIDO 234 General Partners and Limited Partners Professionals listed by surname PROFESIONALES DE SOCIOS ASESORES POR EMPRESA 246 Advisory Members Professionals listed by entity PROFESIONALES DE SOCIOS ASESORES POR APELLIDO 256 Advisory Members Professionals listed by surname ASOCIACIONES EXTRANJERAS DE CAPITAL PRIVADO 266 Foreign Venture Capital & Private Equity Associations PUBLICACIONES DE INTERÉS 268 Publications related to the VC&PE Industry ANOTACIONES Y GLOSARIO DE TÉRMINOS 269 Notes and key words 3 I am honored to be leading the Spanish Venture Capital & Private Equity (ASCRI) (Asociación Española de Capital, Crecimiento e Inversión). -

Partners Group Global Value SICAV

Partners Group Global Value SICAV Société d’Investissement à Capital Variable ("SICAV") Unaudited Semi-Annual Report 2016 Unaudited financial statements for the period from 1 January 2016 to 30 June 2016 R.C.S. Luxembourg B 124.171 No subscription can be accepted on the basis of the financial reports. Subscriptions are only valid if they are made on the basis of the current prospectus accompanied by the latest annual report and the latest semi-annual report, if published thereafter. TABLE OF CONTENTS Mangement and Administration 3 Board of Director’s Report 4 Statement of net assets as at 30 June 2016 8 Statement of operations and changes in net assets for the period ended 30 June 2016 9 Statement of net asset value per share for the period ended 30 June 2016 20 Statement of changes in the number of shares outstanding for the period ended 30 June 2016 22 Notes to the financial statements as at 30 June 2016 23 - 2 - Management and Administration Registered office 2, Place François Joseph Dargent, L-1413 Luxembourg Board of Directors Chairman Sérgio Raposo Partners Group (Luxembourg) S.A. Directors Dr. Helene Müller Schwiering Advokatgruppen Luxembourg Roland Roffler Partners Group AG Daniel Van Hove Orionis Management S.A. AIFM Name Partners Group (UK) Ltd. 110 Bishopsgate, 14th Floor Registered office London EC2N4AY, United Kingdom Administration and Advisors Legal Advisor Loyens & Loeff Luxembourg S.à r.l. 18-20 rue Edward Steichen, L - 2510 Luxembourg Depositary and Paying Agent, Registrar and M.M.Warburg & CO Luxembourg S.A. Transfer Agent 2, Place François Joseph Dargent, L-1413 Luxembourg Administrator and Domicilary Agent WARBURG INVEST LUXEMBOURG S.A. -

Private Equity Benchmark Report

Preqin Private Equity Benchmarks: All Private Equity Benchmark Report As of 31st March 2014 alternative assets. intelligent data. Preqin Private Equity Benchmarks: All Private Equity Benchmark Report As of 31st March 2014 Report Produced on 9th October 2014 This publication is not included in the CLA Licence so you must not copy any portion of it without the permission of the publisher. All rights reserved. The entire contents of the report are the Copyright of Preqin Ltd. No part of this publication or any information contained in it may be copied, transmitted by any electronic means, or stored in any electronic or other data storage medium, or printed or published in any document, report or publication, without the express prior written approval of Preqin Ltd. The information presented in the report is for information purposes only and does not constitute and should not be construed as a solicitation or other offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or as advice of any nature whatsoever. If the reader seeks advice rather than information then he should seek an independent fi nancial advisor and hereby agrees that he will not hold Preqin Ltd. responsible in law or equity for any decisions of whatever nature the reader makes or refrains from making following its use of the report. While reasonable efforts have been used to obtain information from sources that are believed to be accurate, and to confi rm the accuracy of such information wherever possible, Preqin Ltd. Does not make any representation or warranty that the information or opinions contained in the report are accurate, reliable, up-to-date or complete. -

EL CAPITAL PRIVADO, Impulso De La Economía Anuario 2019 Directory

EL CAPITAL PRIVADO, impulso de la economía Anuario 2019 Directory Patrocinado por / Sponsored by: ANUARIO ASCRI 2019 Todos los derechos reservados ASCRI: Príncipe de Vergara, 55, 4ºD. 28006 Madrid DISEÑO EXTERIOR: Atela Comunicación Corporativa DISEÑO INTERIOR: Zingular IMPRENTA: Zingular 2 sumario / index CARTA DEL PRESIDENTE Y DEL DIRECTOR GENERAL DE ASCRI 4 ASCRI Chairman and Managing Director´s Letter QUÉ ES ASCRI 7 What is ASCRI PRIMEROS RESULTADOS DEL AÑO 2018 16 First results for the 2018 exercise LISTA DE ENTIDADES DE VENTURE CAPITAL, CORPORATE VENTURE E IMPACTO SOCIAL 28 Venture Capital, Corporate Venture and Social Impact entities LISTA DE ENTIDADES DE PRIVATE EQUITY 44 Private Equity entities DISTRIBUCIÓN GEOGRÁFICA DE LAS ENTIDADES DE VENTURE CAPITAL & PRIVATE EQUITY SOCIAS DE ASCRI 50 Geographical location of Venture Capital & Private Equity entities (ASCRI members) LISTA DE COMPAÑÍAS PARTICIPADAS 2018 53 Portfolio directory 2018 ÍNDICE DE TÉRMINOS QUE CONTIENEN LAS FICHAS 85 Index of terms included in this directory SOCIOS GESTORES 86 General Partners Members SOCIOS INVERSORES 204 Limited Partners Members SOCIOS ASESORES 216 Advisory Members LISTA DE PROFESIONALES DE LOS SOCIOS GESTORES POR ENTIDAD 288 General Partners Professionals listed by entity LISTA DE PROFESIONALES DE LOS SOCIOS GESTORES POR APELLIDO 300 General Partners Professionals listed by surname LISTA DE PROFESIONALES DE LOS SOCIOS INVERSORES POR ENTIDAD 312 Limited Partners Professionals listed by entity LISTA DE PROFESIONALES DE LOS SOCIOS INVERSORES POR APELLIDO -

2018 Comprehensive Annual Financial Report

2018 ANNUAL REPORT Comprehensive Annual Financial Report Fiscal Years Ended June 30, 2018 and 2017 NYSTRS.org Comprehensive Annual Financial Report Fiscal Years Ended June 30, 2018 and 2017 STNYRS Committed to Providing Educators With a Secure Retirement Since 1921 NEW YORK STATE TEACHERS’ RETIREMENT SYSTEM Comprehensive Annual Financial Report Fiscal Years Ended June 30, 2018 and 2017 Our Mission: To provide our members with a secure pension. Our Vision: To be the model for pension fund excellence and exceptional customer service. Our Values: Integrity Excellence Respect Resourcefulness Diversity Diligence Balance In addition to the above, NYSTRS has five Strategic Objectives. These objectives serve as a guiding light for staff and are a daily reminder of our core beliefs. Each tabbed section divider in this report will examine one of the Strategic Objectives. When taken in concert with our Mission,Vision and Values, these ideals form the fabric of our culture. New York State Teachers’ Retirement System 10 Corporate Woods Drive Albany, NY 12211-2395 (800) 348-7298 NYSTRS.org xxx Table of Contents INTRODUCTION INVESTMENTS (cont.) ACTUARIAL (cont.) 88 Breakdown of Real Estate 117 History of Member Payroll and the 7 Board of Trustees Equity Portfolio Employer Contribution Rate 8 Organizational Structure & Geographic Distribution of the Schedule of Retired Members and Executive Staff Real Estate Equity Portfolio Benefciaries Added to and 9 NYSTRS Staff 89 Private Equity Net Asset Value by Removed from the Beneft Payroll 10 Letter -

Institutional Non Bank Lending and the Role of Debt Funds

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Kraemer-Eis, Helmut; Battazzi, Francesco; Charrier, Remi; Natoli, Marco; Squilloni, Matteo Working Paper Institutional non bank lending and the role of debt funds EIF Working Paper, No. 2014/25 Provided in Cooperation with: European Investment Fund (EIF), Luxembourg Suggested Citation: Kraemer-Eis, Helmut; Battazzi, Francesco; Charrier, Remi; Natoli, Marco; Squilloni, Matteo (2014) : Institutional non bank lending and the role of debt funds, EIF Working Paper, No. 2014/25, European Investment Fund (EIF), Luxembourg, http://www.eif.org/news_centre/publications/EIF_Working_Paper_2014_25.htm This Version is available at: http://hdl.handle.net/10419/176655 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben -

SURVEY Venture Capital & Private Equity in Spain

SURVEY Venture Capital & Private Equity in Spain 2014 WITH THE SPONSORSHIP OF SURVEY Venture Capital & Private Equity in Spain 2014 Príncipe de Vergara, 55 4º D • 28006 Madrid tel. (34) 91 411 96 17 • www.ascri.org CUBIERTA Informe ASCRI 2014-ingles.indd 1 15/04/14 12:45 ascri asociación española de entidades de capital - riesgo SURVEY 2014 Accuracy Venture Capital & Private Equity in Spain THIS SURVEY WAS ELABORATED BY: Dominique Barthel (ASCRI Managing Director) and Ángela Alférez (ASCRI Head of Research), from the data obtained and collected by José Martí Pellón (Universidad Complutense of Madrid) and Marcos Salas de la Hera (Webcapitalriesgo.com) Copyright ASCRI 2014 ascri asociación española de entidades de capital - riesgo The Spanish Private Equity & Venture Capital Association (ASCRI) is a non-profitmaking association that was set up in 1986 to represent, manage and defend its member`s professional interests, and to foster and promote the creation of companies whose corporate purpose consists of acquiring temporary stakes in the capital of non-financial companies whose shares are not quoted on the primary market of the Stock Exchanges. REPORT 2014 INDEX INDEX 5 CHAIRMAN´S LETTER 7 SUMMARY OF THE YEAR 2013 9 1. FUNDRAISING 12 2. TOTAL FUNDS UNDER MANAGEMENT 14 3. INVESTMENT 16 4. DIVESTMENT 20 5. PORTFOLIO 21 6. VENTURE CAPITAL 22 STATISTICS 27 A NEW REGULATORY FRAMEWORK FOR THE VENTURE CAPITAL 49 & PRIVATE EQUITY SECTOR IN SPAIN FOND-ICO GLOBAL INITIATIVE 53 COMPANIES INCLUDED IN THIS SURVEY 54 Our goal is to support the expansion