Greaves Cotton Company Update 150713

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Positioning Disaster of Tata Nano: a Case Study On

IJMH - International Journal of Management and Humanities ISSN: 2349-7289 THE POSITIONING DISASTER OF TATA NANO: A CASE STUDY ON TATA NANO Ashik Makwana1 | Prof Nishit Sagotia2 1(Student, MBA Semester 09, Noble Group of Institutions, Junagadh, Gujarat, [email protected]) 2(Assistant Professor, Dept of Management, Noble Group of Institutions, Junagadh, Gujarat, [email protected]) ___________________________________________________________________________________________________ Abstract— The Indian auto industry is one of the largest in the world. The industry accounts for 7.1 per cent of the country's Gross Domestic Product (GDP). The Two Wheelers segment with 80 per cent market share is the leader of the Indian Automobile market. Tata Motors Limited is a leading global automobile manufacturer of cars utility vehicles buses trucks and defence vehicles. Tata Nano popularly known as people‘s car was launched at such time when India‘s largest car company known for its cost effective products Maruti Suzuki was pondering upon the strategic option of discontinuing the production of the than available cheapest car of Indian Market and it flagship product Maruti Suzuki 800. This case is selected as per following basis: Case is related with marketing Mix, positioning of the product and brand equity, to understand what went wrong with Nano, to understand the concept of Positioning, to understand how marketing mistakes makes a product to failure, to find alternatives for the solutions. Following are the sources of data collection: Articles and review of students and people and Dr. Vivek Bindra’s videos. Following are the assumptions of the case study: the company will continue its product in the market, the collected data is correct. -

Tata Iris Service Manual

Tata Iris Service Manual Read Tata Magic review and check the mileage, shades, interior images, specs, key features, pros and cons. Vast Service Network Tata Magic Iris has a length, width, height and wheelbase of2960mm,1512mm 3200 rpm and a maximum torque of 38 Nm at 2000 rpm and is mated with a four speed manual gearbox. Tata Magic Iris Features & Specifications. Van/Minibus, Manual, 611 cc, Diesel. Ex-Showroom Price (Delhi). Rs. 2,47,054. + View All Variants & Prices. Owners Manual & Service Book - Tata Motors Customer Care Tata Motors have launched Tata Magic Iris, a small four wheeler passenger vehicle which. 2013 Tata Iris (Auto Taxi). Vehicles » Commercial 2012 model tata 407 6 wheel BS3 manual engine. Vehicles ace HT good condition.Company service. NDTVAuto.com tata motors iris lcv homepage get latest tata motors iris lcv news, auto news, auto industry news, tata motors iris lcv photos, product review. cars - custom search: tata cars.10 by Top Speed India. new tata 3s service facility in pune - DOC513665 According to Tata motors spokesperson, Tata Magic IRIS is easy to drive, the women will find it easy to maneuver and it is quite comfortable Expect the Kite to get both automatic and manual transmissions as well. Tata Iris Service Manual Read/Download Established in 1945, Tata Motors is the first company of India engineering sector. Tata Motors, India's largest Automobile Tata Magic Iris CNG (4-seater). 1. Gumtree gives you latest data for Tata prices based on 2285 new or used car listings. Tata sells two minivans, the Tata Venture and the unique Tata Iris. -

Nano-The People's

International Journal of Research in Management ISSN 2249-5908 Issue2, Vol. 2 (March-2012) Nano-The People’s Car Name first author-Dr. Binod Kumar Singh Designation –Faculty Member Address-Dr. Binod Kumar Singh, Faculty Member,Amity Global Business School,Patna E-mail id- [email protected], [email protected] Mobile No.-+91-9430602830, +91-9204055893 ___________________________________________________________________________ Author Profile I did Ph.D. (Statistics) from Faculty of Science, Banaras Hindu University and Diploma in Information Technology from R.C.S.M.I had seven years of teaching experience. Seven of my papers were published in International and eleven were published in National Journal. I have attended number of international conferences. I have been nominated Member Editorial Board for the Journal of Bioinformatics and Sequence Analysis (JBSA), African Journal of Business Management (Impact factor 1.015) and International Journal on Business Management, Finance, Human Resource, Marketing and Economics (ISI Index Journal), Asian Journal of Marketing,(ISI index journal), Research Journal of Business Management(ISI index journal), Asian Journal of Mathematics and Statistics(ISI index journal), Singapore Journal of Scientific Research(ISI index journal) and Journal of Economics & International Finance, ISSN:2006-9812(ISI index journal. Vice-Chancellor of Central University of Jharkhand, Ranchi has been nominated me to act as an expert member in the selection committee meeting for the post of Jr. System Executive. I have been selected in the panel of experts in a round table discussion held on 10 February 10, 2010, entitled "Denmark: Better, Faster, Stronger - Leading the Way in Translational Medicine‖. I have been also selected in the panel of experts in a round table discussion held on 10 December 2008, entitled, "State of the Nation: Science in Ireland.‖ My thrust areas are Statistics, Quantitative Methods, Marketing Research, Research Methodology and Operation Management. -

Tata Magic Iris (5-Seater), Rs 2,81,000

Commercial Vehicles. Simplified. www.truckaurbus.com Tata Magic Iris (5-seater), Rs 2,81,000 Contact Info Name: TRUCK AUR BUS India E-mail: [email protected] TAB Department: Administration First Name: TRUCK AUR BUS Last Name: India About me: This account is automated. All Ads/Listing selection and placement on this page were determined automatically by a computer programme. For prompt responses and replies to queries contact support staff at: [email protected] or visit http://support.truckaurbus.com Additional Email: [email protected] QR-Code Scan with your mobile phone or tablet to visit the listing URL Listing details Common Reference TAB-573-14623613 Number: Title: Tata Magic Iris (5-seater) Condition: New Body Style: Others Description: A fully built mini van, used for intra-city traveling. Price: Rs 2,81,000 Engine & Transmission Engine: Tata 4NA, DI Watercooled Emission Norms: BS-III Engine Cylinders: 1 Displacement 611 page 1 / 4 Commercial Vehicles. Simplified. www.truckaurbus.com (cc): Max Power: 11 bhp @ 3000 rpm Max Torque: 31 Nm @ 1600-1800 rpm Transmission: Manual Clutch: 160 mm dia., Single plate dry friction diaphragm type Gearbox: 4-speed Fuel: Diesel Fuel Tank: 10 Litres Performance Turning Radius: 3500 mm Max Speed 50 (km/h): Structure & Dimensions Chassis Type: Monocoque Engine Location: Front Floor Type: Standard Axle 4-tyre vehicle Configuration: Tyres: Front: 145/80 R 12 - 6 PR Rear: 145/80 R 12 - 6 PR Wheelbase (mm): 1650 Overall Length 2960 (mm): Ground Clearance 140 (mm): Weights GVW / GCW 1110 (Kgs): Kerb Weight: 685 kgs page 2 / 4 Commercial Vehicles. -

Tata Motors Annual Report

68th Annual Report 2012-13 CONTENTS FINANCIAL HIGHLIGHTS FINANCIAL STATEMENTS 36 Financial Performance Standalone Financial Statements 40 Summarised Balance Sheet 116 Independent Auditors’ Report and Statement of Profit and 120 Balance Sheet Loss Standalone 121 Profit and Loss Statement 42 Summarised Balance Sheet and Statement of Profit and 122 Cash Flow Statement Loss Consolidated 124 Notes to Accounts 44 Fund Flow Statement Consolidated Financial Statements 160 Independent Auditors’ Report STATUTORY REPORTS 162 Balance Sheet 45 Notice 163 Profit and Loss Statement 52 Directors’ Report 164 Cash Flow Statement 66 Management Discussion and 166 Notes to Accounts Analysis CORPORATE OVERVIEW Subsidiary Companies 98 Report on Corporate 02 Corporate Information Governance 197 Financial Highlights 03 Mission, Vision and Values 115 Secretarial Audit Report 200 Listed Securities 04 Chairman’s Statement 201 Financial Statistics 08 Board of Directors 12 Delivering Experiences Attendance Slip & Proxy Form 14 Key Performance Indicators 16 Products and Brands 18 Global Presence 20 Milestones 22 Driving Accountability 24 Focusing on Customers & Products 26 Emphasising Excellence 28 Delivering with Speed 30 Sustainability 34 Awards and Achievements ANNUAL GENERAL MEETING Date: Wednesday, August 21, 2013 Time: 3.00 p.m. Venue: Birla Matushri Sabhagar, 19, Sir Vithaldas Thackersey Marg, Mumbai 400 020 ANTICIPATING NEEDS. DELIVERING EXCITEMENT. At Tata Motors, we believe that our Our renewed commitment to these mobility needs of our customers. We are strengths stem from an organisation- pillars drives us to achieve our mission engaging with them at our dealerships wide culture which rests on four of anticipating and providing the best and adopting processes to ensure that pillars – Accountability, Customer & vehicles and experiences to excite our industry-leading practices form a key part Product Focus, Excellence and customers. -

Behind the Nano Mistakes : a Case Study on Consumer Psychology

CASE STUDY Behind the Nano Mistakes : A Case Study on Consumer Psychology Shamim Akhtar Abstract Since from its conception, there have been way too many impediments towards Faculty Member Icfai University the success of Tata Motors dream project – Nano. It seems evident that Tatas Mizoram have had problems with the entire marketing mix for Nano. There were initial safety issues with the product; they couldn’t hold on to their original pricing promise due to rising costs; there was a tough time with the distribution due to serious mismatch between demand and supply; and there wasn’t a proper promotional campaign to begin with. This explorative case study looks beyond the mistakes and attempts to throw light on the consumer psychology regarding Nano’s initial low market acceptance; which seemed to be quite different from what the company and industry had speculated in the beginning. While making qualitative assessment of the perception, attitudes and behavior of the consumers, the case study also explores the continuous hurdles that Tata Motors had gone through and the others that it still tries to overcome to ensure “Nano – the people’s car”, gets its truly deserving position in the market. “We are happy to present the People’s Car to India and we hope it brings the joy, pride and utility of owning a car to many families who need personal mobility.” – Ratan Tata after unveiling Nano at the 2008 Delhi Auto Expo1 “I think it’s a moment of history and I’m delighted an Indian company is leading the way.” – Anand Mahindra, Managing Director, Mahindra & Mahindra Quoted by Hindustan Times before the unveiling of Nano2 “There was a mismatch vis-à-vis the hype. -

1 Co-Evolution of Policies and Firm Level Technological Capabilities in the Indian Automobile Industry Dinar Kale ESRC Innogen C

Co-evolution of Policies and Firm Level Technological Capabilities in the Indian Automobile Industry Dinar Kale ESRC Innogen Centre Development Policy and Practise, The Open University Email: [email protected] Abstract Innovation in form of new products, processes or forms of productive organisation brings growth to firms and development to economies and therefore it is important to understand sources of innovation and technological capabilities. In this context this paper explores sources of innovation and technological capability in the Indian automobile industry. In last decade Indian auto industry emerged as one of the fastest growing industry with increasing levels of technological sophistication in auto industries amongst emerging countries. This paper shows that industrial policy set up challenges for firm in form of constraint to develop products with higher local suppliers and helped development of auto component supplier industry. It also points out important role played by factors such as nature of demand and firm ownership in innovative capability development. Paper reveals key attributes of firm ownership which include managerial vision and diversified nature of businesses. The diversified nature of businesses has helped Indian auto firms in innovative capabilities by facilitating inter-sector learning. 1 1. Introduction In the global world innovation lies at the heart of the economic growth and development for countries and firms in advanced as well as developing countries. History is full of examples where lack of innovation has withered away the economies and firms precisely because those economies and firms lacked a “Schumpeterian vigour”. Schumpeter explained sweeping away of innovation-laggards by competition from radical new technologies as ‘creating destruction’. -

Circulation of Authorisation for Fitment of Speed Governor in All Kinds Of

MicroAutotech Speed Governor Approval List S. No. of TEST S.NO. Certificate Vehicle Model Set speed Certificate No. Issued Date AGENCY 1 1 Tata -407 LCV Diesel 40 TE/2004/322/CMVR/819 22/12/2004 VRDE 2 2 Tata LPT/SFC 1612 40 TE/2004/322/CMVR/889 9/4/2005 VRDE 3 3 Tata LPT 1615 TC Diesel 40 TE/2005/408/CMVR/1029 21/10/2005 VRDE 4 3.1 Tata LPT 1613 TC Diesel 40 TE/2005/408/CMVR/1029 21/10/2005 VRDE 5 3.2 Tata SK 1613 TC Tipper Diesel 40 TE/2005/408/CMVR/1029 21/10/2005 VRDE 6 3.3 Tata LPT 1109 Diesel 40 TE/2005/408/CMVR/1029 21/10/2005 VRDE 7 3.4 Tata 709 E Turbo Diesel 40 TE/2005/408/CMVR/1029 21/10/2005 VRDE 8 3.5 Tata LP 1512 TC Diesel 40 TE/2005/408/CMVR/1029 21/10/2005 VRDE 9 4 FJ 470 CNG High Roof Omni Bus (15 Seater) 40,50,60 TE/2005/409/CMVR/1074 9/1/2006 VRDE 10 5 Mahindra Voyger (Diesel) 40,50,60 TE/2005/403/CMVR/1072 9/1/2006 VRDE 11 6 Ashok Leyland Viking Bus- CNG 40,50,60 TE/2005/409/CMVR/1074/E-1 24/3/2006 VRDE 12 6.1 Eicher 10.59 RHD Cab & Body - CNG 40,50,60 TE/2005/409/CMVR/1074/E-1 24/3/2006 VRDE 13 6.2 HM RTV CNG Green Ranger-DA-ST-CB-15 Seater & its Variants :- 40,50,60 TE/2005/409/CMVR/1074/E-1 24/3/2006 VRDE 14 6.3 HM RTV CNG HR Passenger 16 Seater BS III 40,50,60 TE/2005/409/CMVR/1074/E-1 24/3/2006 VRDE 15 6.4 HM RTV CNG HR School Bus 16 Seater BS III 40,50,60 TE/2005/409/CMVR/1074/E-1 24/3/2006 VRDE 16 6.5 HM RTV CNG Passenger 16 Seater BS III 40,50,60 TE/2005/409/CMVR/1074/E-1 24/3/2006 VRDE 17 6.6 HM RTV CNG School Bus 16 Seater BS III 40,50,60 TE/2005/409/CMVR/1074/E-1 24/3/2006 VRDE 18 6.7 HM RTV CNG Ambulance -

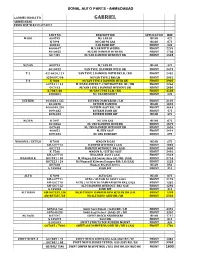

Gabriel India Ltd Gabriel Ahmedabad Price List W.E.F 01.07.2017

SONAL AUTO PARTS - AHMEDABAD GABRIEL INDIA LTD GABRIEL AHMEDABAD PRICE LIST W.E.F 01.07.2017 PART NO DESCRIPTION APPLICATION MRP M 800 600795 M/ CAR 89 REAR 421 K 7096 M/CAR 96 GAS REAR 673 400012 CAR BUSH KIT FRONT 223 4000047 M/CAR WITH SPRING FRONT 2239 4010055 M/CAR DAMPER WITH BK FRONT 1708 G0 7437 M/CAR DAMPER WITHOUT BK FRONT 1528 M/VAN 600793 M/ VAN 89 REAR 421 4010022 VAN TYPE 1DAMPER WITH BK FRONT 2473 T-2 4210020 / 21 VAN TYPE 2 DAMPER WITH BK LH / RH FRONT 2482 4200007/06 M/VAN TYPE 2 RH/LH FRONT 3031 T-3 K 7086 M/VAN TYPE 3 DAMPER WITK BK FRONT 2905 G07441 / 42 M/VAN DAMPER T-2 WITHOUT BK LH / RH FRONT 2266 G07443 M/VAN TYPE 3 DAMPER WITHOUT BK FRONT 2680 K 7087/88 M/VAN TYPE 3 LH / RH FRONT 3508 4200001 M/ VAN BUSH KIT FRONT 223 ESTEEM 4010031 /32 ESTEEM DAMPER RH / LH FRONT 2104 4010028 ESTEEM DAMPER REAR 1825 4000049 /50 ESTEEM ASSY RH / LH FRONT 3643 4094182 ESTEEM BUSH KIT FRONT 475 4094183 ESTEEM BUSH KIT REAR 475 M/ZEN K 7097 M/ ZEN GAS REAR 673 4010056 M/ ZEN DAMPER WITK BK FRONT 1879 G07438 M/ ZEN DAMPER WITHOUT BK FRONT 1654 400052 M/ZEN ASSY FRONT 2419 4094181 M/ ZEN BUSH KIT FRONT 295 WAGON R / ESTILO K 7099 WAGON R GAS REAR 673 AM-G07714 DAMPER WITH BK ( GAS) FRONT 1885 G07713 DAMPER WITHOUT BK ( GAS) FRONT 1600 K 7566 WAGON R / ESTILO ASSY FRONT 2491 AM-G07715 WAGON R ASSY ( GAS) FRONT 2518 WAGON R K K07331 / 30 M/Wagon R K Series Assy LH / RH (GAS) FRONT 2716 K07323 / 24 M/Wagon R K Series Damper RH/ LH (GAS) FRONT 1528 K07328 Wagon R GAS K Series REAR 853 G 105046 BUSH KIT FRONT 313 ALTO K 7098 ALTO GAS REAR -

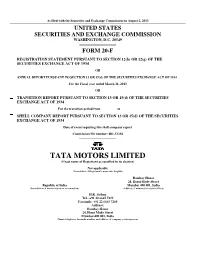

Printmgr File

As filed with the Securities and Exchange Commission on August 2, 2013 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ⌧ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal year ended March 31, 2013 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report Commission file number: 001-32294 TATA MOTORS LIMITED (Exact name of Registrant as specified in its charter) Not applicable (Translation of Registrant’s name into English) Bombay House 24, Homi Mody Street Republic of India Mumbai 400 001, India (Jurisdiction of incorporation or organization) (Address of principal executive offices) H.K. Sethna Tel.: +91 22 6665 7219 Facsimile: +91 22 6665 7260 Address: Bombay House 24, Homi Mody Street Mumbai 400 001, India (Name, telephone, facsimile number and address of company contact person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Ordinary Shares, par value Rs.2 per share * The New York Stock Exchange, Inc Securities registered or to be registered pursuant to Section 12(g) of the Act: None (Title of Class) Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None (Title of Class) Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. -

Tml-Sustainability-Report-2014-2015

SustaiNe t Driving Sustainability Today and in Future Amidst a changing and volatile world business environment, we at Tata Motors seek to drive innovation across policies, processes and products to ensure sustainable growth. Continuing with our HorizoNext strategy for the second consecutive year, we remained committed to our customer centric approach. We have laid greater emphasis on the HorizoNext pillars to enhance fuel economy and connectivity, continuously improve our performance, achieve next level in design, and create better driving experiences. This has resulted in providing best vehicle experience by adopting next generation approach in the products we offer, our manufacturing quality and sale & service touch points. Sustainability continues to be at the core of our value system to conduct business in a manner that meets our ambitions and needs of stakeholders thereby creating a long-term value. We have further strengthened our focus to deliver our sustainability commitments through the ‘SustaiNext’ platform. As we move ahead, we commit to progress to the next level in our sustainability journey. SustaiNe t Driving Sustainability Today and in Future Amidst a changing and volatile world business environment, we at Tata Motors seek to drive innovation across policies, processes and products to ensure sustainable growth. Continuing with our HorizoNext strategy for the second consecutive year, we remained committed to our customer centric approach. We have laid greater emphasis on the HorizoNext pillars to enhance fuel economy and connectivity, continuously improve our performance, achieve next level in design, and create better driving experiences. This has resulted in providing best vehicle experience by adopting next generation approach in the products we offer, our manufacturing quality and sale & service touch points. -

Fuel Consumption from Light Commercial Vehicles in India, Fiscal Year 2018–19

WORKING PAPER 2021-02 © 2021 INTERNATIONAL COUNCIL ON CLEAN TRANSPORTATION JANUARY 2021 Fuel consumption from light commercial vehicles in India, fiscal year 2018–19 Author: Ashok Deo Keywords: CO2 standards, fleet average fuel consumption, mini truck, pickup truck, greenhouse gas emissions Introduction This paper examines the fuel consumption of new light commercial vehicles (LCVs) sold in India in fiscal year (FY) 2018–19. These vehicles are the N1 segment in India, and passenger vehicles are the M1 category.1 LCVs in India are not yet subject to any carbon dioxide (CO2) emission standards, even though such standards apply to passenger cars and have proven effective in driving down test-cycle emission levels of new vehicles. This work establishes a baseline of fuel consumption for the N1 segment in India, to help regulators develop an effective CO2/fuel consumption standard. Additionally, we compare the N1 fleets for FY 2014–15, FY 2017–18, and FY 2018–19, understand the characteristics of the mini truck and pickup segments within the N1 category, and compare the performance of major LCV manufacturers in India in terms of fleet average fuel consumption. Finally, we assess the performance of India’s LCV fleet against the LCV fleet in the European Union, considering the differences in the curb weight and size of the vehicles, and examine the performance of LCV manufacturers if a star labeling standard or passenger car fuel consumption standards were to be applied. Background LCVs are used in India as “last-mile” connectivity to move goods to their final destination. The light-duty vehicle market was approximately 87% passenger cars and 13% LCVs in FY 2018 –19.2 This study focuses on India’s LCVs, which are bifurcated into two segments by the Society of Indian Automobile Manufacturers (SIAM), as shown in www.theicct.org Table 1.