Double Digit Growth in Revenue, Profit and Dividend

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Interactive PDF

Annual Report and Accounts 2017/18 Interactive PDF User guide This PDF allows you to find information and navigate around this document more easily. Links in this PDF The table of contents, key page references and URLs (e.g. www.whitbread.co.uk) are linked in this PDF. Clicking on them will take you to the corresponding page in the document or web page online by opening a new window in your default web browser. You can also navigate the document using the buttons described below. Guide to buttons Back to user guide Sear ch this PDF Print options Pr eceding page Ne xt page Las t visited page WorldReginfo - 2bee309d-1aec-49bd-b06a-6de4a08a90dc Delivering on our strategy... Annual Report & Accounts 2017/18 WorldReginfo - 2bee309d-1aec-49bd-b06a-6de4a08a90dc ...to bring customers brands they love Our vision We will grow brands that customers love by building a strong Customer Heartbeat and innovating to stay ahead. Our Winning Teams delight customers so they come back time and again which, along with our focus on Everyday Efficiency, drives Profitable Growth. We are passionate about being a Force for Good in our communities, helping everyone to live and work well. In this document Overview Consolidated accounts 2017/18 01 Financial highlights 92 Directors’ responsibility statement 02 Business overview 93 Independent auditor’s report 101 Consolidated financial statements Strategic report 107 Notes to the consolidated 04 Chairman’s statement financial statements 06 Chief Executive’s review 08 Business Model Company accounts 2017/18 10 Key performance -

Interactive PDF Whitbread PLC Annual Report and Accounts 2013/14

Whitbread PLC Annual report and accounts 2013/14 Interactive PDF User guide This PDF allows you to find information and navigate around this document more easily. Links in this PDF Words and numbers that are underlined are links – clicking on them will take you to further information within the document or to a web page (which opens in a new window) if they are a url (e.g www.whitbread.co.uk). Guide to buttons Back to user guide Search this PDF Print options Preceding page Next page Last visited page Annual Report and Accounts 2013/14 “ Making everyday experiences special” Overview Financial highlights Whitbread has delivered another year of strong double–digit growth in sales, profit and dividend. p1/5 More on our financial performance p4 Chairman’s statement p6 Chief Executive’s review p38 Finance Director’s review Total revenue Underlying basic EPS2 report Strategic £2,294.3m +13.0% 179.02p +20.1% m p m p p6/43 m p m p Underlying profit 2 before tax Full–year dividend £411.8m +16.5% 68.80p +19.9% m p m p Governance m p m p 3 4 Group return on capital Cash flow from operations p44/81 13.9%1 to 15.3% £526.0m to £601.3m Net debt Group like for like sales £471.1m to £391.6m Up 4.2% 1 Restated for the impact of IAS 19 (revised 2011). 3 Return on capital is the return on invested capital 2013/14 accounts Consolidated See Note 2 of the consolidated financial statements which is calculated by dividing the underlying profit for 2012/13. -

Annual Report and Accounts 2011/12 Contents

Annual Report and Accounts 2011/12 Contents Introduction Business Governance Consolidated Company review accounts accounts 1 Financial highlights 2 Chairman’s statement 22 Board of directors 45 2011/12 93 2011/12 consolidated Company 4 Chief Executive’s 24 Directors’ report accounts accounts review 28 Corporate 8 Strategic approach governance 9 – Team engagement 35 Remuneration report 12 – Customer heartbeat 15 – Profitable growth 17 – Good Together 18 Finance Director’s review 20 Risk management Group at a glance Premier Inn Premier Inn is the UK’s Premier Inn bedrooms largest budget hotel have an en-suite bathroom, chain, with more than TV with Freeview, and 626 47,000 rooms across WiFi internet access. Hotels the UK and Ireland. Over All our hotels have a bar 75% of the UK population and restaurant, either live within five miles of a inside the building, or Premier Inn. next to it, offering a wide range of dishes. Overseas we have three hotels in Dubai, one in Premier Inn has been Abu Dhabi and two in named the UK’s ‘best value India with more on the way. hotel chain’ by YouGov. Restaurants Beefeater Grill Brewers Fayre Table Table Taybarns Beefeater Grill’s expert Brewers Fayre serves Our Table Table restaurants Taybarns is the chefs have been serving the nation’s favourite offer a range of pub ultimate eatery, with up our famous steaks pub food, at great value classics served by friendly great choice, value for nearly 40 years. Our prices, in a family friendly staff at great prices. and convenience. It warm and welcoming environment. -

Iryna Staieva Bakalářská Práce

VYSOKÁ ŠKOLA HOTELOVÁ V PRAZE 8, SPOL. S.R.O. Iryna Staieva Franchising jako strategie vstupu na trh Bakalářská práce 2017 FRANCHISING JAKO STRATEGIE VSTUPU NA TRH Bakalářská prace Iryna Staieva Vysoká škola hotelová v Praze 8, spol. s.r.o. Katedra Hotelnictví Studijní obor: Hotelnictví Vedoucí bakalařské práce: doc. Ing. Lenka Turnerová Datum odevzdání bakalářské práce: 23.11.2017 E-mail: [email protected] Praha 2017 2 Bachelor’s Dissertation Franchising as a market entry strategy Iryna Staieva The Institute of Hospitality Management in Prague 8, Ltd. Department of hospitality managment Major: Hospitality Management Thesis Advisor: doc. Ing. Lenka Turnerová Date of Submission: 23.11.2017 E-mail: [email protected] Prague 2017 3 Prohlašuji, že jsem bakalářskou práce na téma Franchising jako strategie vstupu na trh zpracovala samostatně a veškerou použitou literaturu a další podkladové materiály, které jsem použila, uvádím v seznamu použitých zdrojů a že svázaná a elektronická podoba práce je shodná. V souladu s § 47b zákona č. 111/1998 Sb., o vysokých školach v platném znění souhlasím se zveřejněním své bakalářské práce, a to v nezkrácené formě, v elektrnické podobě ve veřejně přístupné databázi Vysoké školy hotelové v Praze 8, spol. s.r.o. Iryna Staieva jméno a příjmení autora V Praze dne 23.11.2017 4 Abstrakt V teoretické části své práce vysvětlím různé formy a strategii vstupu na nové trhy, vyhodnotím franchising a jeho charakteristiky. Ve stejné části provedu rozbor právních aspektů a specifik franchisingu na území České republiky. V praktické části své práce provedu analýzu franchisingu jako strategii vstupu na nový trh na příkladu trhu horkých nápojů České republiky, rozberu franchisingové koncepty obchodních společností Starbucks a Costa Coffee. -

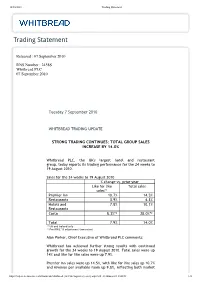

Trading Statement

18/03/2021 Trading Statement Trading Statement Released : 07 September 2010 RNS Number : 2438S Whitbread PLC 07 September 2010 Tuesday 7 September 2010 WHITBREAD TRADING UPDATE STRONG TRADING CONTINUES: TOTAL GROUP SALES INCREASE BY 14.0% Whitbread PLC, the UK's largest hotel and restaurant group, today reports its trading performance for the 24 weeks to 19 August 2010. Sales for the 24 weeks to 19 August 2010 % change vs. prior year Like for like Total sales sales*¹ Premier Inn 10.7% 14.5% Restaurants 3.9% 4.3% Hotels and 7.8% 10.1% Restaurants Costa 8.3%*² 28.0%*² Total 7.9% 14.0% *¹ UK and Ireland only *² Pre IFRIC 13 adjustment (see notes) Alan Parker, Chief Executive of Whitbread PLC comments: Whitbread has achieved further strong results with continued growth for the 24 weeks to 19 August 2010. Total sales were up 14% and like for like sales were up 7.9%. Premier Inn sales were up 14.5%, with like for like sales up 10.7% and revenue per available room up 9.8%, reflecting both market https://otp.tools.investis.com/clients/uk/whitbread_plc1/rns/regulatory-story.aspx?cid=612&newsid=354596 1/4 18/03/2021 Trading Statement growth and a continued improvement in our market share. Like for like occupancy for the 24 weeks continued its recovery to 79.2%, up 9.5 percentage points. Our initiatives to increase market share have proved very successful. Premier Inn's Business Account sales have increased by over 20% as companies continue to be attracted by our great prices, consistent room quality and largest choice of locations. -

Interactive PDF Whitbread PLC Annual Report And

Whitbread PLC Annual report and accounts 2014/15 Interactive PDF User guide This PDF allows you to find information and navigate around this document more easily. Links in this PDF Words and numbers that are underlined are links — clicking on them will take you to further information within the document or to a web page (which opens in a new window) if they are a url (e.g www.whitbread.co.uk). Guide to buttons Back to user guide Search this PDF Print options Preceding page Next page Last visited page WorldReginfo - 605fe8d1-eaa4-4c8d-9189-0753cd555395 Annual Report and Accounts 2014/15 “ Making everyday experiences special” WorldReginfo - 605fe8d1-eaa4-4c8d-9189-0753cd555395 Financial highlights Whitbread has delivered another year of strong growth in revenue, profit and dividend. More on our financial performance p6 Chairman’s statement p8 Chief Executive’s review p42 Finance Director’s review Total revenue Group like for like sales £2,608.1m +13.7% Up 6.5% m m m m Profit before tax Underlying profit1 before tax £463.8m +33.7% £488.1m +18.5% m m m m m m m m Cash generated from operations Net debt £606.4m to £714.2m £391.6m to £583.2m Net assets Group return on capital2 £1,783.0m to £1,977.9m 15.3% to 15.7% Full–year dividend Underlying basic EPS1 82.15p +19.4% 213.67p +19.4% p p p p p p p p 1 Underlying profit excluding amortisation of acquired 2 Return on capital is the return on invested capital intangibles, exceptional items and the impact of the which is calculated by dividing the underlying profit pension finance cost as accounted for under IAS 19. -

Whitbread Preliminary Results

18/03/2021 Whitbread Preliminary Results Whitbread Preliminary Results Released : 30 April 2013 RNS Number : 5337D Whitbread PLC 30 April 2013 DOUBLE DIGIT INCREASE IN REVENUE, PROFIT AND DIVIDEND NEW GROWTH MILESTONES FOR 2018 Whitbread PLC results for the financial year to 28 February 2013 Financial Highlights · Total revenue up 14.2% to £2,030.0 million (2011/12: £1,778.0 million). · Group like for like sales1 up 3.7%. · Underlying profit2 before tax up 11.4% to £356.5 million (2011/12: £320.1 million). · Underlying basic EPS up 12.0% to 150.45p (2011/12: 134.35p). · Full year dividend up 12.0% to 57.40p (2011/12: 51.25p). · Whitbread Hotels and Restaurants profits3 up 5.9% to £313.1 million, Costa profits3 up 29.3% to £90.1 million. · Premier Inn total sales up 13.1% and like for like sales1 up 3.1%. · Costa total sales up 24.1% and like for like sales1 up 6.8%. · Group return on capital4 up 0.4%pts to 14.0%. · Strong cash flow from operations5 of £526.0 million funded capital investment of £343.6 million and supports a 12.0% dividend growth. · Year end net debt down by £33.2 million to £471.1 million. Statutory Highlights · Profit after tax and exceptional items up 13.3% to £301.3 million (2011/12: £266.0 million). · Total basic EPS 170.89p up 12.8% (2011/12: 151.53p). New 2018 Growth Milestones · Premier Inn UK6 rooms to grow by 45% to c75,000 in 2018. · Costa system sales to double to around £2.0 billion in 2018. -

Trading Statement

18/03/2021 Trading Statement Trading Statement Released : 04 March 2010 RNS Number : 0576I Whitbread PLC 04 March 2010 Thursday 4 March 2010 TRADING UPDATE WHITBREAD DEMONSTRATES FURTHER POSITIVE MOMENTUM Whitbread PLC, the UK's largest hotel and restaurant group, today reports trading performance for the 51 weeks to 18 February 2010. Sales for the 51 weeks to 18 February 2010 % sales change vs. prior year Q4 (to week 51) 51 weeks to 18/02/10 Like Total Like for Total for like like Premier Inn 1.7 8.5 (4.6) 2.8 Pub Restaurants 1.3 2.1 1.8 (0.6)* Whitbread Hotels and Restaurants 1.5 5.5 (1.9) 1.3 Costa 9.5 19.9 5.3 21.0 Total 3.0 9.0 (0.7) 5.4 *including the 44 sites disposed of in September 2008 Alan Parker, Chief Executive of Whitbread PLC comments: Whitbread's trading performance continues to be robust. In the last quarter all our businesses have demonstrated further positive momentum with like for like sales growth. At Premier Inn, like for like sales in the last three months have been positive, up 1.7% on last year. Revpar at Premier Inn https://otp.tools.investis.com/clients/uk/whitbread_plc1/rns/regulatory-story.aspx?cid=612&newsid=354553 1/3 18/03/2021 Trading Statement showed continued outperformance versus competitors. Year to date, regional revpar was -6.9% against -10.2% for the total regional hotel market. Our plan to target the leisure market aggressively is progressing well with both our £29 Premier Offers and dynamic pricing delivering occupancy growth at weekends and holiday periods. -

Interim Management Statement

18/03/2021 Interim Management Statement Interim Management Statement Released : 22 June 2010 RNS Number : 9933N Whitbread PLC 22 June 2010 Tuesday 22 June 2010 WHITBREAD AGM AND INTERIM MANAGEMENT STATEMENT STRONG START TO THE YEAR: TOTAL GROUP SALES INCREASE BY 13.5% Whitbread PLC, the UK's largest hotel and restaurant group, today reports its trading performance for the 13 weeks to 3rd June 2010 at its Annual General Meeting. Sales for the 13 weeks to 3rd June 2010 % change vs. prior year Like for like sales*¹ Total sales Premier Inn 10.5% 14.1% Pub Restaurants 3.6% 4.2% Whitbread Hotels 7.4% 9.7% and Restaurants Costa 8.5%*² 26.9% Total 7.6% 13.5% *¹ UK and Ireland only *² Pre IFRIC 13 adjustment (see notes) Alan Parker, Chief Executive of Whitbread PLC comments: Whitbread has started the new financial year strongly, with continued momentum and good like for like sales. In the first quarter, total sales were up 13.5% and like for like sales were up 7.6%. https://otp.tools.investis.com/clients/uk/whitbread_plc1/rns/regulatory-story.aspx?cid=612&newsid=354578 1/4 18/03/2021 Interim Management Statement Premier Inn sales were up 14.1%, with like for likes up 10.5%. Like for like revenue per available room at Premier Inn was up 9.1% with occupancy of 75.7% achieved reflecting both an improvement in the market and a significant increase in share. Our outperformance was driven by increased marketing and the full implementation of dynamic pricing with improved value for money awareness. -

Annual Report and Accounts 2009/10 Annual Report and Accounts 2009/10

Annual Report and Accounts 2009/10 and Accounts Annual Report Annual Report and Accounts 2009/10 www.whitbread.co.uk Designed and produced by Columns Design, www.columnsdesign.com It is important that our Annual Report is produced in an environmentally responsible manner, including the sourcing of materials. The material used in this report is certified as 100% recycled by the Forest Stewardship Council. The Annual Report was printed by Royle Print Limited, a carbon- neutral printing company. It was originated, printed and bound on one production site and only required electric transportation between processes. Under the framework of ISO 14001 Royle Print takes a structured approach to measure, improve and audit its environmental status on an ongoing basis. The main areas targeted for continual reduction arise from use of solvents, energy consumption and waste generation. Royle Print is also Forest Stewardship Council (FSC) chain-of-custody certified. When you have finished with this report please dispose of it in your recycled paper waste. Annual Report 2009/10 The Whitbread Way Forward Our aim is to build the best large-scale hospitality brands in the world by becoming the most customer focused organisation there is. Anywhere. We’ll do this by providing outstanding value and making everyday experiences feel special – so that our customers come back time and time again. Contents Financial highlights 1 Group at a glance 2 Chairman’s statement 4 Business review – 6 Chief Executive 6 Our strategy 10 Our people 12 Our customers 14 Hotels and Restaurants 16 Costa 24 Finance Director 28 Corporate responsibility 30 Key performance indicators 32 Group risks and uncertainties 34 Board of directors 36 Senior management 38 Directors’ report 39 Corporate governance report 43 Remuneration report 47 Accounts 2009/10 57 1 Financial highlights Whitbread has performed strongly in the most challenging hotel and restaurant trading conditions for a generation. -

Interactive PDF Whitbread PLC Annual Report and Accounts 2014/15

Whitbread PLC Annual report and accounts 2014/15 Interactive PDF User guide This PDF allows you to find information and navigate around this document more easily. Links in this PDF Words and numbers that are underlined are links — clicking on them will take you to further information within the document or to a web page (which opens in a new window) if they are a url (e.g www.whitbread.co.uk). Guide to buttons Back to user guide Search this PDF Print options Preceding page Next page Last visited page Annual Report and Accounts 2014/15 “ Making everyday experiences special” Financial highlights Whitbread has delivered another year of strong growth in revenue, profit and dividend. More on our financial performance p6 Chairman’s statement p8 Chief Executive’s review p42 Finance Director’s review Total revenue Group like for like sales £2,608.1m +13.7% Up 6.5% m m m m Profit before tax Underlying profit1 before tax £463.8m +33.7% £488.1m +18.5% m m m m m m m m Cash generated from operations Net debt £606.4m to £714.2m £391.6m to £583.2m Net assets Group return on capital2 £1,783.0m to £1,977.9m 15.3% to 15.7% Full–year dividend Underlying basic EPS1 82.15p +19.4% 213.67p +19.4% p p p p p p p p 1 Underlying profit excluding amortisation of acquired 2 Return on capital is the return on invested capital intangibles, exceptional items and the impact of the which is calculated by dividing the underlying profit pension finance cost as accounted for under IAS 19. -

60705 Whitbread Interims 2010 SHOW BOOK.Pptx

Interim Results 2010/11 19 October 2010 1 WorldReginfo - 20d918fe-2d6a-4615-8cdd-b4ab68419400 Anthony Habgood Chairman 2 WorldReginfo - 20d918fe-2d6a-4615-8cdd-b4ab68419400 Christopher Rogers Group Finance Director 3 WorldReginfo - 20d918fe-2d6a-4615-8cdd-b4ab68419400 Summary H1 2010/11 H1 2010/11 H1 2009/10 Change Underlying profit before tax £151.8m £118.2m 28.4% Profit before tax, £146.0m £110.5m 32.1% pre-exceptional EPS underlying (diluted) 61.27p 47.33p 29.5% Proposed interim dividend 11.25p 9.65p 16.6% 4 WorldReginfo - 20d918fe-2d6a-4615-8cdd-b4ab68419400 Summary – Profit & loss H1 2010/11 £m H1 2010/11 H1 2009/10 Change Revenue 1 805.4 703.3 14.5% Profit from operations 173.6 140.0 24.0% Central costs (10.2) (9.2) (10.9)% Interest (11.6) (12.6) 7.9% Underlying profit before tax 151.8 118.2 28.4% 1 includes exceptional revenue of £5.0m in respect of VAT refund on gaming machine income 5 WorldReginfo - 20d918fe-2d6a-4615-8cdd-b4ab68419400 Summary – Underlying profit & loss H1 2010/11 £m H1 2010/11 H1 2009/10 Change Underlying profit before tax 151.8 118.2 28.4% Pension finance cost - IAS 19 (5.8) (7.7) 24.7% Profit before tax, 146.0 110.5 32.1% pre-exceptional Taxation (42.7) (34.1) (25.2)% Net profit, pre-exceptionals 103.3 76.4 35.2% Exceptionals 12.7 (3.3) Profit for the year 116.0 73.1 58.7% 6 WorldReginfo - 20d918fe-2d6a-4615-8cdd-b4ab68419400 Revenue by business segment H1 2010/11 £m H1 2010/11 H1 2009/10 Change Hotels & Restaurants 608.0 548.8 10.8% Costa 198.5 155.4 27.7% Less: inter-segment 1 (1.1) (0.9) (22.2)% Revenue