Empty to Alive: the Next Use for Department Store Space

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2012 FINALISTS ICSC Is Proud to Announce the Finalists of the 2012 U.S

2012 FINALISTS ICSC is proud to announce the finalists of the 2012 U.S. MAXI Awards. The U.S. MAXI Awards honor outstanding marketing campaigns from all over the United States. Chosen by a panel of industry professionals, these finalists represent excellence throughout the industry. The 2012 U.S. Maxi Awards will be presented at ICSC’s first-ever NOI + Conference in Orlando, Florida, September 5, 2012. TRADITIONAL MARKETING - ADVERTISING Single Center Pooches Pose at The Brickyard’s PUParazzi! The Brickyard Shopping Center Chicago, Illinois Owner: Retail Properties of America, Inc. Management Company: RPAI US Management, LLC The Gateway provides Daily Dish The Gateway Salt Lake City, Utah Owner: Retail Properties of America, Inc. Management Company: RPAI, Southwest Management Favorite Label Consumer Campaign Natick Mall Natick, Massachusetts Owner/Management Company: General Growth Properties Home for the Holidays Promotional Campaign Southlake Town Square Southlake, Texas Owner: Retail Properties of America Inc Management Company: RPAI Southwest Management LLC Company 2011 Hillsdale’s South End Renovation Bohannon Development Company San Mateo, California MORE Holiday Advertising CBL & Associates Properties, Inc. Chattanooga, Tennessee Joint Center Club Estrellas E-Magazine The Shops at La Cantera and North Star Mall San Antonio, Texas Management Company: General Growth Properties TRADITIONAL MARKETING - BUSINESS-TO-BUSINESS (B2B) Single Center The Writing’s on the Wall West Acres Shopping Center Fargo, North Dakota Owner/Management Company: West Acres Development, LLP Company Think Retail. Create Value. DDR Corp. Beachwood, Ohio Keep The Dollars In Dallas United Commercial Realty Dallas, Texas TRADITIONAL MARKETING - CAUSE RELATED MARKETING Single Center Queen for a Day Aspen Grove Littleton, Colorado Owner/Management Company: DDR Corp. -

Prom 2018 Event Store List 1.17.18

State City Mall/Shopping Center Name Address AK Anchorage 5th Avenue Mall-Sur 406 W 5th Ave AL Birmingham Tutwiler Farm 5060 Pinnacle Sq AL Dothan Wiregrass Commons 900 Commons Dr Ste 900 AL Hoover Riverchase Galleria 2300 Riverchase Galleria AL Mobile Bel Air Mall 3400 Bell Air Mall AL Montgomery Eastdale Mall 1236 Eastdale Mall AL Prattville High Point Town Ctr 550 Pinnacle Pl AL Spanish Fort Spanish Fort Twn Ctr 22500 Town Center Ave AL Tuscaloosa University Mall 1701 Macfarland Blvd E AR Fayetteville Nw Arkansas Mall 4201 N Shiloh Dr AR Fort Smith Central Mall 5111 Rogers Ave AR Jonesboro Mall @ Turtle Creek 3000 E Highland Dr Ste 516 AR North Little Rock Mc Cain Shopg Cntr 3929 Mccain Blvd Ste 500 AR Rogers Pinnacle Hlls Promde 2202 Bellview Rd AR Russellville Valley Park Center 3057 E Main AZ Casa Grande Promnde@ Casa Grande 1041 N Promenade Pkwy AZ Flagstaff Flagstaff Mall 4600 N Us Hwy 89 AZ Glendale Arrowhead Towne Center 7750 W Arrowhead Towne Center AZ Goodyear Palm Valley Cornerst 13333 W Mcdowell Rd AZ Lake Havasu City Shops @ Lake Havasu 5651 Hwy 95 N AZ Mesa Superst'N Springs Ml 6525 E Southern Ave AZ Phoenix Paradise Valley Mall 4510 E Cactus Rd AZ Tucson Tucson Mall 4530 N Oracle Rd AZ Tucson El Con Shpg Cntr 3501 E Broadway AZ Tucson Tucson Spectrum 5265 S Calle Santa Cruz AZ Yuma Yuma Palms S/C 1375 S Yuma Palms Pkwy CA Antioch Orchard @Slatten Rch 4951 Slatten Ranch Rd CA Arcadia Westfld Santa Anita 400 S Baldwin Ave CA Bakersfield Valley Plaza 2501 Ming Ave CA Brea Brea Mall 400 Brea Mall CA Carlsbad Shoppes At Carlsbad -

Sample First Page

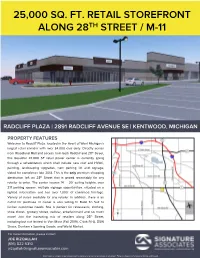

25,000 SQ. FT. RETAIL STOREFRONT ALONG 28TH STREET / M-11 RADCLIFF PLAZA | 2891 RADCLIFF AVENUE SE | KENTWOOD, MICHIGAN PROPERTY FEATURES Welcome to Radcliff Plaza, located in the Heart of West Michigan’s largest retail corridor with over 34,000 cars daily. Directly across from Woodland Mall and access from both Radcliff and 28th Street, this beautiful 47,000 SF retail power center is currently going through a rehabilitation which shall include new roof and HVAC, painting, landscaping upgrades, new parking lot and signage, slated for completion late 2018. This is the only premium shopping destination left on 28th Street that is priced reasonably for any retailer to enter. The center houses 14’ – 20’ ceiling heights, over 217 parking spaces, multiple signage opportunities, situated on a lighted intersection and has over 1,000’ of combined frontage. Variety of suites available for any retailer. In addition, there is an outlot for purchase or owner is also willing to Build To Suit to further customize needs. Site is perfect for restaurants, clothing, shoe stores, grocery stores, cellular, entertainment and so much more! Join the increasing mix of retailers along 28th Street, including but not limited to Von Mour (Fall 2019), Chick Fil-A, DSW Shoes, Dunham’s Sporting Goods, and World Market. For more information, please contact: JOE RIZQALLAH (616) 822 6310 [email protected] Information is subject to verification and no liability for errors or omissions is assumed. Price is subject to change and listing withdrawal. 2,162-25,185 2891 Radcliff Avenue SE – Kentwood, Michigan Square Feet Retail For Sale or Lease AVAILABLE Site Plan For more information, please contact: JOE RIZQALLAH SIGNATURE ASSOCIATES 1188 East Paris Ave SE, Suite 220 (616) 822 6310 Grand Rapids, MI 49546 [email protected] www.signatureassociates.com Information is subject to verification and no liability for errors or omissions is assumed. -

Q2 Investor Update

Q2 INVESTOR UPDATE PREIT Malls ABOUT PREIT Our community-centric retail and leisure real estate solutions maximize opportunities for the communities we serve, connecting people to jobs and businesses to customers. Our portfolio is located primarily in densely-populated, high businesses barrier-to-entry markets attractive to a wide array of uses. Recognizing the role we play, we optimize our real estate to create the most sustainable business model for each community, in turn MAXIMIZING THE VALUE OF OUR customers jobs PORTFOLIO FOR STAKEHOLDERS. PREIT has spent the last decade creating a stronger portfolio that meets the needs of the modern consumer through thriving disposition of 19 lower-productivity properties, repositioning communities 19 anchor boxes with over 3 dozen new tenants and securing a differentiated tenant base that is comprised of 30% “open air” tenancy. 2 Q2 FINANCIAL HIGHLIGHTS Same store NOI is up 62% Total liquidity of $104.9 million at end of Q2 FFO per share exceeding plan at $0.10, up 267% over the 2020 quarter Core Mall June sales +16% over June 3 Q2 OPERATING HIGHLIGHTS Core Mall Rolling 12 sales are est. to have reached a new high at $549 per sq Total Core Mall leased ft, an increase of space at 92.6% 1.3% over last reported comp sales in Feb. 2020 Construction is underway 500,000 sq ft of leases for Aldi to open its first signed for future openings, store in our portfolio at expected to contribute Dartmouth Mall in annual gross rent of $10.8 Dartmouth, MA in Q3 million 2021 4 RECENT ACTIVITY Phoenix Theatres signed a lease to replace former theater at Woodland Mall in Grand Rapids HomeGoods will replace the former Bed Bath & Beyond space at Cumberland Mall New retailer, Turn 7 signed to replace the former Lord & Taylor at Moorestown Mall Our properties welcomed 15 new tenants across the portfolio in Q2, accounting for over 120,000 square feet of leased space Retailers expanding in portfolio: Aerie/Offline, Rose & Remington, Windsor, Purple and more. -

The BG News February 25, 2005

Bowling Green State University ScholarWorks@BGSU BG News (Student Newspaper) University Publications 2-25-2005 The BG News February 25, 2005 Bowling Green State University Follow this and additional works at: https://scholarworks.bgsu.edu/bg-news Recommended Citation Bowling Green State University, "The BG News February 25, 2005" (2005). BG News (Student Newspaper). 7406. https://scholarworks.bgsu.edu/bg-news/7406 This work is licensed under a Creative Commons Attribution-Noncommercial-No Derivative Works 4.0 License. This Article is brought to you for free and open access by the University Publications at ScholarWorks@BGSU. It has been accepted for inclusion in BG News (Student Newspaper) by an authorized administrator of ScholarWorks@BGSU. State University FRIDAY February 25, 2005 OSCAR NIGHTS The 77th Annual Academy PM SHOWERS Awards will announce HIGH: 33 LOW 20 winners; PAGE 8 www.bgnews.com independent student press VOLUME 99 ISSUE 121 USG: cheating policy unfair Students accused of time the unidentified stu- ^«%^M H\ - \~ r3 ui! dent involved in this case was cheating need more accused of cheating, he is being dismissed from BGSU for two •mt ^ ^»'—' -^ ^LM0V"ll"HB>MIB*m rights, USG says ■-—** years — unfairly, according to Malkin. By Bridget Triarp REPORTER Malkin said this student's work was taken by classmates USG passed a series of reso- and turned in to his instructor lutions this week that defend without his consent. the rights of students who are "Intent is not a defense," accused of cheating under the Malkin said. "You can't say I University academic honesty policy. didn't intend for it to get stolen — that's not a defense. -

2017 Annual Report Simon Property Group, Inc

WorldReginfo - b17aae64-640b-4ba7-878c-aa92dcbb46fe - WorldReginfo 2017 ANNUAL REPORT ANNUAL 2017 SIMON PROPERTY GROUP, INC. 2017 ANNUAL REPORT INNOVATING THE FUTURE OF THE SHOPPING EXPERIENCE CONTENTS From the Chairman & CEO ii Financial Highlights iv Sustainability Highlights xi Investment Highlights xii Board of Directors & Management xiv 10-K 1 Management’s Discussion & Analysis 55 Financial Statements 75 Simon Property Group, Inc. (NYSE: SPG) is an S&P100 company and a global leader in the ownership of premier shopping, dining, entertainment and mixed-use destinations. WorldReginfo - b17aae64-640b-4ba7-878c-aa92dcbb46fe ICONIC SHOPPING FOR EVERY STYLE AND TASTE THE SHOPS AT CLEARFORK Ft. Worth, Texas WorldReginfo - b17aae64-640b-4ba7-878c-aa92dcbb46fe ii SIMON PROPERTY GROUP, INC. FROM THE CHAIRMAN & CEO Dear Fellow Shareholders, As we enter our 25th year as a public company (58th year in total!), I could start this letter describing how we have changed for the better, but the real purpose of this letter is to reinforce to you, our shareholders, that we are focused on the future. Certainly our success in transforming our business since 1993 (our first year as a public company) is a good indicator that we are always adjusting and improving. Our organization lives for challenges, is driven to succeed, and is among the best-of-breed. We started our public company as a middle market mall company with 56 regional malls that were 85% occupied and generated approximately $250 in sales per square foot. Then our change began and I assure you will always continue. David Simon We led our industry in leasing, development ■ Industry-leading financial results. -

Destination Shopping Defining “Destination” Retail in the New American Suburbs

Destination Shopping Defining “Destination” Retail in the New American Suburbs Barrett S. Lane University of Pennsylvania CPLN 500: Prof. Eugenie L. Birch TA: Amy Lynch 8 December 2010 As the suburbanization movement took hold in the years following World War II, so did the way in which retail and commercial centers catered to their audience. For years, the idea of shopping at one location to get all of one’s necessary goods was conceptualized by large downtown department stores, such as Sears & Roebuck or H.M. Macy & Co. But as retailers found more and more of their audience fleeing the cities to the suburbs, they realized that they needed to follow suit in order to maintain profits and keep their companies competitive. Now, just as the way in which individuals and families have changed their patterns of living in the suburbs, retailers and commercial developers have begun to retool their approach to catering to the suburban consumer. In the postwar years and through the 1960s and 1970s, traditional shopping centers and shopping malls were the norm across suburbs, featuring an array of different retailers anchored by one or two big box retailers or department stores. However, by the 1980s and 1990s, commercial developers began to find their niche; setting up different kinds of retail centers for different consumer groups and classes. The evolution of power centers, fashion centers, entertainment centers, and “shopping villages” reflected the changing pattern of suburban growth and the specialization that consumers now demanded from retail. Ultimately, creating retail in the suburbs and later in cities revolved around creating “destinations” in retail, and the change seen in America’s suburbs, cities, and suburban business districts forced retailers and developers to continually challenge and redefine what they saw as “destination shopping”, using consumer markets and tastes to retool their strategy. -

City Commission Agenda Materials

City of East Grand Rapids YouTube Livestream: Regular City Commission Meeting https://bit.ly/2xXlLvn Agenda Begins at 6 pm. June 21, 2021 – 6:00 p.m. (EGR Community Center – 750 Lakeside Drive) Citizens may attend the meeting in person or virtually. 1. Call to Order. Virtual attendance/ participation information: 2. Approval of Agenda. https://www.eastgr.org/CivicAlerts.aspx?AID=781 3. Public Comment. 4. Report of Mayor, City Commissioners and City Manager. Regular Agenda Items 5. Zoning variance hearing on the request of Mark Gurney & Mary Yurko of 910 Rosewood to allow the enlargement of an accessory building to 1,180 sq. feet instead of the 720 sq. feet allowed (public hearing required; action requested). 6. Parks Improvement Debt Millage (public comment invited; action requested). a. Joint Resolution with East Grand Rapids Schools Regarding Playground Equipment Replacement. b. Resolution Authorizing Ballot Proposal for Park Improvement Bonds. 7. Advisory Board appointments for FY 2021-22 (no hearing required; approval requested). 8. Determination of annual required contribution and funding plan for Defined Benefit Plan (no hearing required; action requested). 9. Contract for reconfiguration of the Lakeside/Lakeside/Greenwood intersection (no hearing required; approval requested). 10. Purchase of wetlands mitigation credits (no hearing required; approval requested). 11. Contract for legal representation services (no hearing required; approval requested). 12. Discussion of work session date for Chapter 79C: Marijuana Establishments and Facilities (no hearing required; action requested). 13. Discussion of ordinance change to establish a separate Zoning Board of Appeals Facilities (no hearing required; action requested). Consent Agenda Items (no hearing required; approval requested unless noted). -

Investor Update May 2017

INVESTOR UPDATE M AY 2 0 1 7 1 PREIT: Company Overview Strong market position with quality properties concentrated in mid-Atlantic’s top MSAs 23 million square feet dedicated to retail, dining and entertainment with an increasingly strong and diversified anchor mix Early-mover advantage in rapidly-changing retail environment has created differentiated platform Small scale creates outsized growth opportunities through: • Redevelopment and remerchandising • Anchor transformation • Densification 2 Geography PHILADELPHIA WASHINGTON DC Valley Mall Francis Scott Key Mall Willow Grove Park Plymouth Meeting Mall Exton Square Mall Fashion Outlets Moorestown Mall Springfield Mall Cherry Hill Mall Mall at Prince Georges Gloucester Premium Outlets Cumberland Mall Springfield Town Center PREIT’s portfolio is primarily located along the east coast with a concentration in the mid-Atlantic’s top MSA’s - Philadelphia and Washington DC. 3 Successful Transformation • Concentrated portfolio in densely populated, high barrier-to-entry markets CREATED A FOCUSED MARKET • Focused on high-quality, well-located assets in Top MSAs STRATEGY • 40% of NOI generated from Top 5 assets with sales PSF of $588 • Significantly reduced risk profile through strategic disposition program • $720 million raised OPTIMIZED PORTFOLIO • Sold 16 low-productivity malls with 2 more coming to market • Capitalizing on opportunities to improve quality through remerchandising and redevelopment • Lifestyle Experience: ~20% of space committed to dining & entertainment REVITALIZING CORE ASSETS -

State City Shopping Center Address

State City Shopping Center Address AK ANCHORAGE 5TH AVENUE MALL SUR 406 W 5TH AVE AL FULTONDALE PROMENADE FULTONDALE 3363 LOWERY PKWY AL HOOVER RIVERCHASE GALLERIA 2300 RIVERCHASE GALLERIA AL MOBILE BEL AIR MALL 3400 BELL AIR MALL AR FAYETTEVILLE NW ARKANSAS MALL 4201 N SHILOH DR AR FORT SMITH CENTRAL MALL 5111 ROGERS AVE AR JONESBORO MALL @ TURTLE CREEK 3000 E HIGHLAND DR STE 516 AR LITTLE ROCK SHACKLEFORD CROSSING 2600 S SHACKLEFORD RD AR NORTH LITTLE ROCK MC CAIN SHOPG CNTR 3929 MCCAIN BLVD STE 500 AR ROGERS PINNACLE HLLS PROMDE 2202 BELLVIEW RD AZ CHANDLER MILL CROSSING 2180 S GILBERT RD AZ FLAGSTAFF FLAGSTAFF MALL 4600 N US HWY 89 AZ GLENDALE ARROWHEAD TOWNE CTR 7750 W ARROWHEAD TOWNE CENTER AZ GOODYEAR PALM VALLEY CORNERST 13333 W MCDOWELL RD AZ LAKE HAVASU CITY SHOPS @ LAKE HAVASU 5651 HWY 95 N AZ MESA SUPERST'N SPRINGS ML 6525 E SOUTHERN AVE AZ NOGALES MARIPOSA WEST PLAZA 220 W MARIPOSA RD AZ PHOENIX AHWATUKEE FOOTHILLS 5050 E RAY RD AZ PHOENIX CHRISTOWN SPECTRUM 1727 W BETHANY HOME RD AZ PHOENIX PARADISE VALLEY MALL 4510 E CACTUS RD AZ TEMPE TEMPE MARKETPLACE 1900 E RIO SALADO PKWY STE 140 AZ TUCSON EL CON SHPG CNTR 3501 E BROADWAY AZ TUCSON TUCSON MALL 4530 N ORACLE RD AZ TUCSON TUCSON SPECTRUM 5265 S CALLE SANTA CRUZ AZ YUMA YUMA PALMS S C 1375 S YUMA PALMS PKWY CA ANTIOCH ORCHARD @SLATTEN RCH 4951 SLATTEN RANCH RD CA ARCADIA WESTFLD SANTA ANITA 400 S BALDWIN AVE CA BAKERSFIELD VALLEY PLAZA 2501 MING AVE CA BREA BREA MALL 400 BREA MALL CA CARLSBAD PLAZA CAMINO REAL 2555 EL CAMINO REAL CA CARSON SOUTHBAY PAV @CARSON 20700 AVALON -

Michael Kors® Make Your Move at Sunglass Hut®

Michael Kors® Make Your Move at Sunglass Hut® Official Rules NO PURCHASE OR PAYMENT OF ANY KIND IS NECESSARY TO ENTER OR WIN. A PURCHASE OR PAYMENT WILL NOT INCREASE YOUR CHANCES OF WINNING. VOID WHERE PROHIBITED BY LAW OR REGULATION and outside the fifty United States (and the District of ColuMbia). Subject to all federal, state, and local laws, regulations, and ordinances. This Gift ProMotion (“Gift Promotion”) is open only to residents of the fifty (50) United States and the District of ColuMbia ("U.S.") who are at least eighteen (18) years old at the tiMe of entry (each who enters, an “Entrant”). 1. GIFT PROMOTION TIMING: Michael Kors® Make Your Move at Sunglass Hut® Gift Promotion (the “Gift ProMotion”) begins on Friday, March 22, 2019 at 12:01 a.m. Eastern Time (“ET”) and ends at 11:59:59 p.m. ET on Wednesday, April 3, 2019 (the “Gift Period”). Participation in the Gift Promotion does not constitute entry into any other promotion, contest or game. By participating in the Gift Promotion, each Entrant unconditionally accepts and agrees to comply with and abide by these Official Rules and the decisions of Luxottica of America Inc., 4000 Luxottica Place, Mason, OH 45040 d/b/a Sunglass Hut (the “Sponsor”) and WYNG, 360 Park Avenue S., 20th Floor, NY, NY 10010 (the “AdMinistrator”), whose decisions shall be final and legally binding in all respects. 2. ELIGIBILITY: Employees, officers, and directors of Sponsor, Administrator, and each of their respective directors, officers, shareholders, and employees, affiliates, subsidiaries, distributors, -

The Shops at Nanuet, Along Route 59 at the New York State Thruway, Just 3.5 Miles North of the Bergen/Rockland County Line

200 Nanuet Mall Route 59 NANUET Redevelopment of Nanuet, NY - Rockland County -PLAZA- 225,000 SF Macy’s Property DEMOGRAPHICS TRADE AREA POPULATION DAYTIME WORKFORCE POPULATION 438,385 220,160 TRADE AREA HOUSEHOLDS MEDIAN AGE 143,776 38.6 AVERAGE HOUSEHOLD INCOME MEDIAN HOME VALUE $124,871 Annually $541,427 The Nanuet Plaza is conveniently located with- in The Shops at Nanuet, along Route 59 at the New York State Thruway, just 3.5 miles north of the Bergen/Rockland County line. • The property is located in affluent Rockland County, New York, at the confluence of two major arteries: Route 59 and Middletown Road. • The Shops at Nanuet is convenient from several major routes: I-87 (New York State Thruway)/I-287, Palisades Parkway, Garden State Parkway, and Route 59. • The center is 20 miles north of Manhattan and 13 miles west of White Plains. FEATURED TENENTS OVERVIEW REGAL CINEMAS . D R 24 HOUR FITNESS N PROPOSED W REDEVELOPMENT O T E THE SHOPS AT NANUET DDL ZINBURGER .MI WINE & BURGER BAR S BANCHETTO FEAST SEARS FAIRWAY MARKET VERIZON WIRELESS PATSY’S PIZZERIA TD BANK BJ’S RESTAURANT P.F. CHANG’S & BREWHOUSE SR 59 N AERIAL OVERVIEW The long tenured Macy’s department store that has anchored the Shops at Nanuet will be redeveloped into a new retail space. This presents the opportunity for future tenents to revitalize the existing facade and begin the tranformation of the center. 170'-3" 67'-9" 197'-7" 28'-0" TYP. 365'-11" TYP. 28'-0" 28'-0" TYP. TYP. 28'-0" 365'-7" EXISTING RETAIL ± 103,636 S.F.