Tata Steel Limited

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pre- Feasibility Report 1. Executive Summary

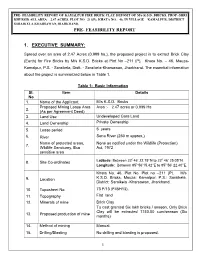

PRE- FEASIBILITY REPORT OF KAMALPUR FIRE BRICK CLAY DEPOSIT OF M/s K.S.D. BRICKS, PROP.-SHRI KHURSID ALI, AREA – 2.47 ACRES, PLOT NO –211(P), KHATA NO.– 46, IN VILLAGE – KAMALPUR, DISTRICT – SARAIKELA-KHARSAWAN,JHARKHAND. PRE- FEASIBILITY REPORT 1. EXECUTIVE SUMMARY: Spread over an area of 2.47 Acres (0.999 ha.), the proposed project is to extract Brick Clay (Earth) for Fire Bricks by M/s K.S.D. Bricks at Plot No –211 (P), Khata No. – 46, Mauza- Kamalpur, P.S. - Saraikela, Distt. - Saraikela-Kharsawan, Jharkhand. The essential information about the project is summarized below in Table 1. Table 1: Basic Information Sl. Item Details No 1. Name of the Applicant M/s K.S.D. Bricks Proposed Mining Lease Area Area :- 2.47 acres or 0.999 Ha 2. (As per Agreement Deed) 3. Land Use Undeveloped Gora Land 4. Land Ownership Private Ownership 5. Lease period 5 years 6. River Sona River (250 m approx.) Name of protected areas, None as notified under the Wildlife (Protection) 7. Wildlife Sanctuary, Eco Act, 1972 sensitive area 0 0 8. Site Co-ordinates Latitude: Between 22 46’ 22.15’’N to 22 46’ 25.05’’N. Longitude: Between 850 56’15.42’’E to 850 56’ 22.40’’E. Khata No. 46, Plot No. Plot no –211 (P), M/s 9. Location K.S.D. Bricks, Mouza: Kamalpur, P.S.: Saraikela, District: Saraikela -Kharsawan, Jharkhand. 10. Toposheet No. 73 F/13 (F45H13). 11. Topography Flat land 12. Minerals of mine Brick Clay To cast granted Six lakh bricks / season, Only Brick Clay will be extracted 1740.00 cum/season (Six 13. -

Selection of Consultancy Firm for Preparation of Comprehensive Mobility Plan for Jamshedpur(UA) Under Urban Infrastructure &

Selection of Consultancy Firm For Preparation Of Comprehensive Mobility Plan for Jamshedpur(UA) Under Urban Infrastructure & Governance (UIG)-JnNURM June, 2009 URBAN DEVELOPMENT DEPARTMENT, GOVT. OF JHARKHAND, 4TH FLOOR, PROJECT BHAWAN, DHURWA, RANCHI- 834004 Comprehensive Mobility Plan (CMP) for Jamshedpur(UA) City of Jharkhand 1. BACKGROUND Jamshedpur(UA) : Introduction Jamshedpur is one of the oldest and the largest existing Company town in the world. It was the benchmark development for post independent Indian industrial cities such as Bhilai, Rourkela and Durgapur, which were established in completely rural areas. A city founded by the late Jamshedji Nusserwanji Tata, Jamshedpur then known as Sakchi was home to the first private Iron and Steel Company of India. The Jamshedpur Block was established in the 1952 and constitutes of rural & urban areas having one Municipality and two Notified Area Committees namely Jugsalai Municipality, Jamshedpur Notified Area Committee and Mango Notified Area Committee. Tata Nagar was the sole urban node for many decades till villages within its vicinity transformed into urban agglomerations. The Jamshedpur City Development Plan has been conceived for an area of 149.225 Sq. Kms, which has a present (2006) population of approximately 12Lakhs. The area covered under Jamshedpur CDP includes three Notified Area Committees (Jamshedpur Notified Area, Adityapur Notified Area, Mango Notified Area), one Municipality (Jugsalai Municipality) and eight other fringe towns / urban outgrowths (which includes the -

Adityapur Industrial Area ,Saraikela-Kharsawan

IN . HACTARE / ACRE 1.TOTAL LAND AREA 280.00 ACRE 2.ADMINISTRATIVE AREA NIL 3.COMMON FACILITY AREA 14.505 ACRE 4.NET INDUSTRIAL AREA 83.865 ACRE 5.OTHER AREA NIL MASTER PLAN A . INTERNAL INFRASTRUCTURE POWER POLE / SUBSTATION - YES ICT--- PROP ADITYAPUR INDUSTRIAL AREA PHASE - 6 STP - NO CETP - PROP WATER SUPLLY/ WATER TREATMENT - PROP STROM WATER DRAINAGE /COVERED - OPENED- PROP RUN OFF USED FOR RAIN WATER HARVESTING - YES ROADS - YES B . EXTERNAL INFRASTRUCTURE LOGISTIC TERMINAL - 8 KM SS M-12P(A) POWER SUB STATION - 3 KM NS KANDRA ADITYAPUR ROAD SOLID WASTE DISPOSAL/ TREATMENT SITE 6 KM M-12P(B) BUS STOP - 0 KM M-13P(A) M-13P(B) RAIL - 3 KM NS PORTS - MAPPED WITH GIS M-14 AIR PORTS - 215 KM ES M-14 M-15 60' 0'' WIDE ROAD M-10 NS-05P(B) NS-06 A-31 M-09 C CATEGORY A-32 M-01P(A) . HAZARDOUS /POLLUTING 60' 0'' WIDE ROADA-33 NON HAZARDOUS/NON POLUTING M-21P(A) WEIGH-BRIDGE 80' 0'' WIDE ROAD MIXED - YES A-34P(A) M-01P(B) NS-19 A-34P(B) COMMON FACILITY NS-20P(A) A-35 M-01P(C) COMMON FACILITY CENTER - CLS NS-20P(B) NS-12 M-02P(A) M-21P(B) DORMITORY FOR LODGING- CLS NS-21 NS-13 M-07P(A) M-02P(B) BANK BRANCH /ATM - CLS NS-14P(A) M-18P(A) NS-22 M-07P(B) CANTEEN / RESTORENT - CLS NS-14P(B) 60' 0'' WIDE ROAD NS-23 NS-14P(C ) M-18P(B) WEIGH BRIDGE FOR CARGO/FREIGHT - PROP M-07P(C) NS-15 M-02P(C) TRUCK PARKING - NO NS-24 SKILL DEVELOPMENT CENTER - CLS NS-16 B-01 D. -

JHARKHAND BIJLI VITRAN NIGAM LTD. (JBVNL) Area Board –JBVNL

JHARKHAND BIJLI VITRAN NIGAM LTD. (JBVNL) (CIN: U40108JH2013SGC001702) Engineering Building, HEC, Dhurwa, Ranchi–4 Email: [email protected] Phone: +91 651 2400760 Fax: 0651-2446055 Area Board –JBVNL Contact Details Office Area Board Type Designation Name Ph. No. Mail Id * General Manager DHANBAD 9431135800 [email protected] General Manager DUMKA 9431135850 [email protected] General Manager GIRIDIH 7541836195 [email protected] Area Board General Manager HAZARIBAGH 9431135700 [email protected] General Manager JAMSHEDPUR 9431135900 [email protected] General Manager MEDININAGAR 9431707400 [email protected] General Manager RANCHI 9431135508 [email protected] Circle Office -(DGM)-JBVNL Contact Details Office Type Designation Circle Name Ph. No. Mail Id Circle Dy. General Manger CHAIBASA 9431135910 [email protected] Circle Dy. General Manger CHAS 9431135806 [email protected] Circle Dy. General Manger DALTONGANJ 9431707401 [email protected] Circle Dy. General Manger DEOGHAR 9431135852 [email protected] Circle Dy. General Manger DHANBAD 9431135805 [email protected] Circle Dy. General Manger DUMKA 9431135854 [email protected] Circle Dy. General Manger GHARWA 9431707402 [email protected] Circle Dy. General Manger GIRIDIH 9431135703 [email protected] Circle Dy. General Manger GUMLA 9431106321 [email protected] Circle Dy. General Manger HAZARIBAGH 9431135702 [email protected] Circle Dy. General Manger JAMSHEDPUR 9431135909 [email protected] Circle Dy. General Manger KODERMA 9431135711 [email protected] Circle Dy. General Manger RAMGARH 9431135701 [email protected] Dy. -

ORIENTAL BANK of COMMERCE.Pdf

STATE DISTRICT BRANCH ADDRESS CENTRE IFSC CONTACT1 CONTACT2 CONTACT3 MICR_CODE D NO 10-86, MAIN RD, OPP MUNICIPAL CORPORATION, ANDHRA MANCHERIAL, MANCHERIY 011- PRADESH ADILABAD MANCHERIAL ANDHRA PRADESH AL ORBC0101378 23318423 12-2-990, PLOT NO 66, MAIN ROAD, ANDHRA SAINAGAR, ANANTAPU 040- PRADESH ANANTAPUR ANANTHAPUR ANANTHAPUR R ORBC0101566 23147010 D.NO.383,VELLORE ROAD, ANDHRA GRAMSPET,CHITTOO 970122618 PRADESH CHITTOOR CHITTOOR R-517002 CHITTOOR ORBC0101957 5 EC ANDHRA TIRUMALA,TIRU TTD SHOPPING 0877- PRADESH CHITTOOR PATI COMPLEXTIRUMALA TIRUPATI ORBC0105205 2270340 P.M.R. PLAZA, MOSQUE ROADNEAR MUNICIPAL ANDHRA OFFICETIRUPATI, 0877- PRADESH CHITTOOR TIRUPATI A.P.517501 TIRUPATI ORBC0100909 2222088 A P TOURISM HOTEL COMPOUND, OPP S P 08562- ANDHRA BUNGLOW,CUDDAPA 255525/255 PRADESH CUDDAPAH CUDDAPAH H,PIN - 516001 CUDDAPAH ORBC0101370 535 D.NO 3-2-1, KUCHI MANCHI AMALAPURAM, AGRAHARAM, BANK ANDHRA EAST DIST:EAST STREET, DISTT: AMALAPUR 08856- PRADESH GODAVARI GODAVARI EAST GODAVARI , AM ORBC0101425 230899 25-6-40, GROUND FLOORGANJAMVARI STREET, KAKINADADIST. ANDHRA EAST EAST GODAVARI, 0884- PRADESH GODAVARI KAKINADA A.P.533001 KAKINADA ORBC0100816 2376551 H.NO.13-1-51 ANDHRA EAST GROUND FLOOR PRADESH GODAVARI KAKINADA MAIN ROAD 533 001 KAKINADA ORBC0101112 5-8-9,5-8-9/1,MAIN ROAD, BESIDE VANI MAHAL, MANDAPETA, DISTT. ANDHRA EAST EAST GODAVARI, PIN MANDAPET 0855- PRADESH GODAVARI MANDAPETA - 533308 A ORBC0101598 232900 8-2A-121-122, DR. M. GANGAIAHSHOPPIN G COMPLEX, MAIN ANDHRA EAST ROADRAJAHMUNDR RAJAHMUN 0883- PRADESH GODAVARI -

DIPS-Saraikela-Kharsawan.Pdf

Contents S. No. Topic Page No. 1. General Characteristics of the District 1 1.1 Location & Geographical Area 1 1.2 Topography 1 1.3 Availability of Minerals. 1 1.4 Forest 2 1.5 Administrative set up 2 2. District at a glance 2 2.1 Existing Status of Industrial Area in the District Seraikela-Kharasawan 5 3. Industrial Scenario Of Seraikela-Kharasawan 5 3.1 Industry at a Glance 5 3.2 Year Wise Trend Of Units Registered 6 3.3 Details Of Existing Micro & Small Enterprises & Artisan Units In 6 The District 3.4 Large Scale Industries / Public Sector undertakings 7 3.5 Major Exportable Item 8 3.6 Growth Trend 8 3.7 Vendorisation / Ancillarisation of the Industry 8 3.8 Medium Scale Enterprises 8 3.8.1 List of the units in Seraikela-Kharasawan & near by Area 8 3.8.2 Major Exportable Item 12 3.9 Service Enterprises 12 3.9.1 Coaching Industry 12 3.9.2 Potentials areas for service industry 12 3.10 Potential for new MSMEs 12 4. Existing Clusters of Micro & Small Enterprise 13 4.1 Detail Of Major Clusters 13 4.1.1 Manufacturing Sector 13 4.1.2 Service Sector 13 4.2 Details of Identified cluster 13 5. General issues raised by industry association during the course of 14 meeting 6. Steps to set up MSMEs 15 7. Additional information if any 16 ii Brief Industrial Profile of Saraikela-Kharsawan District 1. General Characteristics of the District This district was carved out from West Singhbhum district in 2001. -

Effects of Urbanization on Pollution: a Case Study of Jamshedpur

International Journal of Research in all Subjects in Multi Languages Vol. 7, Issue: 10, Oct.: 2019 [Author: Dr. Md. Reyaz][Subject: Geography] (IJRSML) ISSN: 2321 - 2853 \\\\\\ Effects of Urbanization on Pollution: A case study of Jamshedpur DR MD REYAZ Assistant Professor, Department of Geography, Karim City College, Jamshedpur Abstract: The industrial township was created in 1907 to serve the Tata Steel works in the tribal villages of Sakchi. Previously it was called Sakchi but its name was changed by Lord Chelmsford. The old railway station was known as Kalimati railway station whose name is now changed to Tatanagar junction. Jamshedpur city has outgrown beyond such essential facilities as water supply, electricity, sewer system, drainage, transportation, sanitation services particularly outside the Tata owned area. It is the largest city in state of Jharkhand. From last few decades due to heavily industrialization, deforestation and migration this township is facing some severe problems. The aim of this research paper is to highlight the problems faced due to heavily industrialization, Urbanization, deforestation and migration. Secondary data were collected from JUSCO and other reliable resources. Keywords: Urbanization, Lithosphere change, Geomorphic, population pollution, crowding 1. Introduction Jamshedpur, India's premiere steel city has a picturesque location on the confluence of the two rivers the Subarnarekha and its tributary the Kharkai, in an undulating micaschist plain surrounded by rugged hills and hillocks of the Jharkhand particularly the Chotanagpur plateau. The industrial township was created in 1907 to serve the Tata Steel works in the tribal villages of SAKCHI.1 In the north beyond the Subarnarekha lies a range of hills known as the Dalma range (926 m) dominating the whole landscape. -

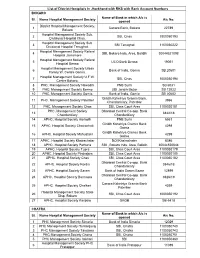

List of District Hostpitals in Jharkhand with RKS with Bank Account Numbers BOKARO Name of Bank in Which A/C Is Sl

List of District Hostpitals In Jharkhand with RKS with Bank Account Numbers BOKARO Name of Bank in which A/c is Sl. Name Hospital Management Society A/c No. opened District Hospital Management Society, 1 Canara Bank, Bokaro 22789 Bokaro Hospital Management Society Sub. 2 SBI, Chas 1000050193 Divisional Hospital Chas. Hospital Management Society Sub. 3 SBI Tenughat 1100050222 Divisional Hospital Tenughat. Hospital Management Society Referal 4 SBI, Bokaro Inds, Area, Balidih 30044521098 Hospital Jainamore Hospital Management Society Referal 5 UCO Bank Bermo 19051 Hospital Bermo Hospital Management Society Urban 6 Bank of India, Gomia SB 20601 Family W. Centre Gomia. Hospital Management Society U.F.W. 7 SBI, Chas 1000050194 Centre Bokaro. 8 PHC. Management Society Nawadih PNB Surhi SB 6531 9 PHC. Management Society Bermo UBI Jaridih Bazar SB 12022 10 PHC. Management Society Gomia Bank of India, Gomia SB 20602 Giridih Kshetriya Gramin Bank, 11 PHC. Management Society Paterber 3966 Chandankiary, Paterbar 12 PHC. Management Society Chas SBI, Chas Court Area 1100020181 PHC. Management Society Dhanbad Central Co-opp. Bank 13 3844/18 Chandankiary Chandankiary 14 APHC. Hospital Society Harladih PNB Surhi 6551 Giridih Kshetriya Gramin Bank 15 APHC. Hospital Society Chatrochati 4298 Goima Giridih Kshetriya Gramin Bank 16 APHC. Hospital Society Mahuatanr 4299 Goima 17 APHC. Hospital Society Khairachatar BOI Khairachater 8386 18 APHC. Hospital Society Pathuria SBI , Bokaro Inds. Area, Balidih 30044520844 19 APHC. Hospital Society Tupra SBI, Chas Court Area 1100050179 20 APHC. Hospital Society Pindrajora SBI, Chas Court Area 1100050180 21 APHC. Hospital Society Chas SBI, Chas Court Area 1100050182 Dhanbad Central Co-opp. -

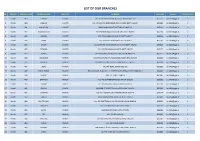

List of Our Branches

LIST OF OUR BRANCHES SR REGION BRANCH CODE BRANCH NAME DISTRICT ADDRESS PIN CODE E-MAIL CONTACT NO 1 Ranchi 419 DORMA KHUNTI VILL+PO-DORMA,VIA-KHUNTI,DISTT-KHUNTI-835 227 835227 [email protected] 0 2 Ranchi 420 JAMHAR KHUNTI VILL-JAMHAR,PO-GOBINDPUR RD,VIA-KARRA DISTT-KHUNTI. 835209 [email protected] 0 3 Ranchi 421 KHUNTI (R) KHUNTI MAIN ROAD,KHUNTI,DISTT-KHUNTI-835 210 835210 [email protected] 0 4 Ranchi 422 MARANGHADA KHUNTI VILL+PO-MARANGHADA,VIA-KHUNTI,DISTT-KHUNTI 835210 [email protected] 0 5 Ranchi 423 MURHU KHUNTI VILL+PO-MURHU,VIA-KHUNTI, DISTT-KHUNTI 835216 [email protected] 0 6 Ranchi 424 SAIKO KHUNTI VILL+PO-SAIKO,VIA-KHUNTI,DISTT-KHUNTI 835210 [email protected] 0 7 Ranchi 425 SINDRI KHUNTI VILL-SINDRI,PO-KOCHASINDRI,VIA-TAMAR,DISTT-KHUNTI 835225 [email protected] 0 8 Ranchi 426 TAPKARA KHUNTI VILL+PO-TAPKARA,VIA-KHUNTI, DISTT-KHUNTI 835227 [email protected] 0 9 Ranchi 427 TORPA KHUNTI VILL+PO-TORPA,VIA-KHUNTI, DISTT-KHUNTI-835 227 835227 [email protected] 0 10 Ranchi 444 BALALONG RANCHI VILL+PO-DAHUTOLI PO-BALALONG,VIA-DHURWA RANCHI 834004 [email protected] 0 11 Ranchi 445 BARIATU RANCHI HOUSING COLONY, BARIATU, RANCHI P.O. - R.M.C.H., 834009 [email protected] 0 12 Ranchi 446 BERO RANCHI VILL+PO-BERO, RANCHI-825 202 825202 [email protected] 0 13 Ranchi 447 BIRSA CHOWK RANCHI HAWAI NAGAR, ROAD NO. - 1, KHUNTI ROAD, BIRSA CHOWK, RANCHI - 3 834003 [email protected] 0 14 Ranchi 448 BOREYA RANCHI BOREYA, KANKE, RANCHI 834006 [email protected] 0 15 Ranchi 449 BRAMBEY RANCHI VILL+PO-BRAMBEY(MANDER),RANCHI-835205 835205 [email protected] 0 16 Ranchi 450 BUNDU -

Adityapur Industrial Area,Large Sector Category

MASTER PLAN IN . HACTARE / ACRE ADITYAPUR INDUSTRIAL AREA,LARGE SECTOR CATEGORY 1.TOTAL LAND AREA 1050.00 ACRE WEIGH-BRIDGE HAZARDOUS /POLLUTING 2.ADMINISTRATIVE AREA 0.85 ACRE NON HAZARDOUS/NON POLUTING 3.COMMON FACILITY AREA 22.87 ACRE MIXED - YES 4.NET INDUSTRIAL AREA 1026.28 ACRE 5.OTHER AREA NIL A B C D. INTERNAL INFRASTRUCTURE . EXTERNAL INFRASTRUCTURE . COMMON FACILITY SAFETY POWER POLE / SUBSTATION - PROP LOGISTIC TERMINAL - 10 KM ES COMMON FACILITY CENTER - PROP FIRE SAFETY - PROP ICT---PROP POWER SUB STATION - 0 KM DORMITORY FOR LODGING - PR AIR QUALITY MONOTRING STATION - PROP STP - NO SOLID WASTE DISPOSAL/ TREATMENT SITE - 26KM BANK BRANCH /ATM - PROP CETP - PROP BUS STOP - 0 KM CANTEEN / RESTORENT - PROP WATER SUPLLY/ WATER TREATMENT - YES RAIL- 10 KM ES WEIGH BRIDGE FOR CARGO/FREIGHT - PROP STROM WATER DRAINAGE /COVERED - OPENED-Y PORTS - MAPPED WITH GIS TRUCK PARKING - NO RUN OFF USED FOR RAIN WATER HARVESTING- P AIR PORTS - 135 KM WS SKILL DEVELOPMENT CENTER- PROP ROADS - YES CFC - (ADMINISTRATION AREA, COMMON FACILITY AREA) XITE SCHOOL N 47 S S 44 48 51 49 50 43 KANDRA ADITYAPUR ROAD S 54 KALIKAPUR (T.NO.50) S 70 S GREENERY FOOT PATHWAY PATHWAY FOOT GAS PIPE LINE LINE PIPE GAS ELECTRICAL LINE / CABLE CABLE / LINE ELECTRICAL R O A D R O A D FOOT PATHWAY PATHWAY FOOT WATER PIPELINE N.T.P.C POWER GRID TISCO ADITYAPUR HOSING COLONY (50.00 ACRES) WIDE ROAD DRAINAGE LINE / FLOOD CONTROL DRAIN DRAIN CONTROL FLOOD / LINE DRAINAGE GREENERY J.S.E.B B KANDRA ADITYAPUR ROAD OPEN SPACE H MAL METALLIKS HOMESHED AREA OF VILL:- RAMCHANDRAPUR -

East Singhbhum District, Jharkhand State

भजू ल सचू ना पस्ु तिका डﴂभूम जिला, झारख ﴂपूर्बी स घ Ground Water Information Booklet East Singhbhum District, Jharkhand State AUTO FLOW BORE WELL LOCATED AT VILLAGE KUDADA के न्द्रीय भूमिजल बो셍 ड Central Ground water Board जल संसाधन िंत्रालय Ministry of Water Resources (भारि सरकार) रा煍य एकक कायाडलय, रााँची (Govt. of India) िध्य-पर्वू ी क्षेत्र State Unit Office,Ranchi पटना Mid-Eastern Region Patna मसिंबर 2013 September 2013 1 भूजल सूचना पुस्तिका डﴂभूम जिला, झारख ﴂपूर्बी स घ Ground Water Information Booklet East Singhbhum District, Jharkhand State Prepared By ुनिल टोꥍपो (वैज्ञानिक ख ) Sunil Toppo (Scientist B) रा煍य एकक कायाडलय, रााँची िध्य-पूर्वी क्षेत्र,पटना State Unit Office, Ranchi Mid Eastern Region, Patna 2 GROUND WATER INFORMATION OF EAST SINGHBHUM DISTRICT, JHARKHAND STATE Contents Sr. Chapter Pages No. 1.0 Introduction 8 1.1 Introduction 8 1.2 Demography 9 1.3 Physiography and Drainage 9 1.4 Irrigation 10 1.5 Previous Studies 10 2.0 2.0 Climate and rainfall 11 3.0 3.0 Soil 11 4.0 4.0 Geology 11 5.0 Ground Water Scenario 13 5.1 Hydrogeology 13 5.1.1 Depth to water level 13 5.1.2 Seasonal fluctuation 14 5.1.3 Exploratory wells 14 5.1.4 Long term water level trend 14 5.2 Ground water resource 15 5.3 Ground Water Quality 15 5.4 Status of ground water development 15 6.0 Ground water management strategy 16 6.1 Ground water development 16 6.2 Water conservation and artificial recharge 16 7.0 Ground water related issue and problems 17 8.0 Awareness and training activity 17 8.1 The mass awareness programme (MAP) 17 8.2 Participation in exhibition, mela, fair etc. -

State District City Address Type Jharkhand Bokaro

STATE DISTRICT CITY ADDRESS TYPE AXIS BANK ATM, KHATA NO.211 POLO NO. 1445 MOZA NO. 28 JHARKHAND BOKARO BOKARO THANA NO 108, AGARWAL MEDICINE STORE, BANK MORE CHOWK, OFFSITE GOMIA BOKARO JHARKHAND. 829111. AXIS BANK ATM, MAIN ROAD CHAS, P.O+P.S- CHAS, DIST- BOKARO, JHARKHAND BOKARO BOKARO OFFSITE JHARKHAND - 827013 AXIS BANK ATM, MAIN ROAD CHAS NEAR PETROL PUMP,PO- JHARKHAND BOKARO BOKARO OFFSITE CHAS,DIST-BOKARO,PIN-827013, JHARKHAND AXIS BANK LTD, GROUND FLOOR , THE RAJDOOT HOTEL, NEAR JHARKHAND BOKARO BOKARO K.M.MEMORIAL HOSPITAL,BYE PASS ROAD, CHAS – ONSITE BOKARO,JHARKHAND,PIN CODE: 827013. AXIS BANK LTD, GROUND FLOOR , NEAR HOTEL URVARSHI, MAIN JHARKHAND BOKARO BOKARO ONSITE ROAD PHUSRO BAZAR, JHARKHAND. 829144 AXIS BANK ATM CENTRE MARKET SECTOR 9 PLOT NO C2 BOKARO JHARKHAND BOKARO BOKARO OFFSITE STEEL CITY BOKARO JHARKHAND 827009 AXIS BANK LTD OPPOSITE KALI MANDIR POST OFFICE MORE PO JHARKHAND BOKARO BOKARO ONSITE GOMIA DIST BOKARO JHARKHAND 829111 AXIS BANK ATM KHATA NO 350 PLOT NO 4709 RAKWA 38 DISMIL JHARKHAND BOKARO BOKARO THANA NO 123 MOUJA HOSIR MAIN ROAD SADAM PO HOSIR PS OFFSITE GOMIA DIST BOKARO JHARKHAND 829111 AXIS BANK ATM, HOLDING NO:-148, WARD NO:-17, P.O:-CHATRA, JHARKHAND CHATRA CHATRA P.S:-CHATRA, NEAR OLD PETROL PUMP , MAIN ROAD CHATRA, DIST:- OFFSITE CHATRA, JHARKHAND, PIN-825401 AXIS BANK ATM, KHATA NO:- 117, PLOT NO:- 574, WARD NO;-21, HOLDING NO:- 156A OLD/ 05 NEW, RAKWA:- 2.75 DISMIL, THANA JHARKHAND CHATRA CHATRA NO:- 005, HALKA- 6B, MOUZA:- NAGWA, ANCHAL:- CHATRA, OPP. DC OFFSITE OFFICE NEAR COLLEGE ROAD CHATRA, DIST- CHATRA, JHARKHAND, PIN-825401 AXIS BANK LTD, GROUND & FIRST FLOOR MAIN ROAD PO & PS JHARKHAND CHATRA CHATRA ONSITE CHATRA DIST CHATRA 825401 JHARKHAND AXIS BANK ATM, CIRCULAR ROAD NEAR SATSANG CHOWK,PO- JHARKHAND DEOGHAR BELABAGAN OFFSITE BELABAGAN,DIST-DEOGHAR, 814112 AXIS BANK ATM, AT: ECL, CHITRA, OPP.