Full Text of the Decision Regarding the Completed Acquisition by Lookers

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FTSE Factsheet

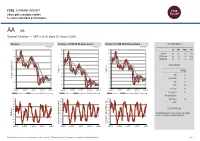

FTSE COMPANY REPORT Share price analysis relative to sector and index performance AA AA. General Retailers — GBP 0.25 at close 03 August 2020 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 03-Aug-2020 03-Aug-2020 03-Aug-2020 0.7 140 140 1D WTD MTD YTD 130 130 Absolute 4.6 4.6 4.6 -57.0 0.6 Rel.Sector 2.4 2.4 2.4 -48.8 120 120 Rel.Market 2.5 2.5 2.5 -46.1 110 110 0.5 100 100 VALUATION 90 0.4 90 80 Trailing Relative Price Relative Relative Price Relative 80 70 0.3 PE 1.6 70 Absolute Price (local currency) (local Price Absolute 60 EV/EBITDA 8.0 60 50 0.2 PB -ve 50 40 PCF 0.7 0.1 40 30 Div Yield 2.6 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Aug-2019 Nov-2019 Feb-2020 May-2020 Aug-2020 Price/Sales 0.1 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Net Debt/Equity - 100 90 90 Div Payout 4.6 90 80 80 ROE - 80 70 70 70 Index) Share Share Sector) Share - - 60 60 60 DESCRIPTION 50 50 50 40 40 The principal activity of the Company is providing 40 RSI RSI (Absolute) service of consumer roadside assistance. -

In This Issue...And More!

Autumn 2019 The VoiceThe OfficialNFDA magazine for the Industry In this issue... Brexit Guidance Drive My Career Feature Latest Consumer and Dealer Attitude Surveys ...and more! The Voice interviews Stuart Hodson, Glyn Hopkin Operations Director AML19_FPAD(Register)v2.qxp_Layout 1 06/09/2019 17:04 Page 1 Welcome to the Autumn NFDA Membership is shaping up to be the Edition of the Voice Details Update Automotive Management LIVE best day you’ll spend away from your business this year Following the official launch of theElectric Vehicle Approved (EVA) scheme in May, over 90% of the slots available to dealerships have already been filled. The auditing process is progressing well and the dealerships that have obtained their EVA accreditation have started to display EVA branded material. Please email [email protected] for more information. In September, we published the NFDA Dealer Attitude Survey Summer 2019. Overall, there Sue Robinson was a minor decline in dealers’ satisfaction Director, NFDA levels with their respective manufacturers. To ensure our data is fully compliant with Lexus topped the survey with the highest GDPR we are required to maintain and update Dear Colleague, average score across all questions while the information we hold for our member Honda saw the biggest improvement. organisations. It would be extremely helpful if As we enter the final quarter of the year, there NFDA members could provide the following remains uncertainty surrounding Brexit. The In December, the final round of our regional meetings will take place. These meetings will information for their company, especially, where UK is about a month away from its planned there have recently been changes. -

BMW & Mini, 501 Dunstable Road, Luton, LU4

HIGH QUALITY PRIME CAR SHOWROOM INVESTMENT SHOWROOM CAR PRIME HIGH QUALITY BMW & Mini 501 DUNSTABLE ROAD � LUTON � LU4 8QN A14 Northampton A428 CAMBRIDGE Investment Summary. Location.A5 A11 Bedford M1 A1 A421 Excellently positioned fronting A43 Situated on the Madford onto the A505, the main arterial Retail Park, 2 miles north west Milton Keynes route which leads directly from of Luton Town Centre, 20 miles the M1 (J11), 1 mile to the west, to south east of Milton Keynes A6 the centre of Luton M11 A5 A10 Two adjoining modern glazed showrooms, refurbished in 2016 Floor Area: 37,400 sq ft Stevenage Luton 80 display bays (293 in total) Site Area: 2.3 acres A41 A418 11 Workshops and large parking (29% site coverage) provisions Aylesbury A1(M) M1 Single let to Ivor Holmes Limited A41 Harlow Guaranteed by Specialist Cars 21 21a Holdings Limited (D&B Rating AWULT: 17.8 yrs (to expiry) 4A1) M40 AGA from Pendragon PLC until Watford M25 Dec 2031 M25 Marketing Rent: RPI-linked annual rent reviews £ £310,277 pa (£7.85 psf) capped at 2.77% pa Refurbished in 2016 by the Tenure: Freehold tenant at a cost of £2 million Proposal We are instructed to seek offers for the freehold interest in excess of £5,550,000 subject to contract and exclusive of VAT. A purchase at this level would refl ect an attractiveNet Initial Yield of 5.25% and a low capital value of £148 per sq ft, after deducting purchasers costs of 6.61%. Site Plan. Site *boundary for indicative purposes only 2 BMW & MINI � 501 DUNSTABLE ROAD, LUTON, LU4 8QN 17 16 TO LONDON M1 LUTON STATION 15 J11 14 TO LONDON Sovereign Park 12 13 Bilton Way 9 Industrial Estate 10 11 Local 7 8 Occupiers. -

Top 100 Contents

2 3 THE MANUFACTURER TOP 100 CONTENTS CONTENTS INTRODUCTORY PAGES Background 4 Foreword by Daniel Kirmatzis, Head of Digital and Communities The Manufacturer 5 Cranfield University andThe Manufacturer: Driving Excellence, by Professor Mark Jolly 7 Manufacturing Heroes, by Rosa Wilkinson, HVMC 8 Recognising Talent, by Dan Kirkpatrick, Trust Hunter 9 Judging Panel 10 Judging Criteria 13 What it means to be a member of The Manufacturer Top 100 14 The Pledge 15 THE MANUFACTURER TOP 100 16-52 Sponsored by: 2 3 THE MANUFACTURER TOP 100 BACKGROUND BACKGROUND EDITORIAL WHY? We first had the idea forThe Out of the 100 judged to have made Daniel Kirmatzis Manufacturer Top 100 in 2013. There the cut, 20 have been highlighted as Tom Lane was a growing recognition in academic Exemplars, people who make a truly [email protected] studies and parliamentary reports that exceptional contribution to the sector every day. OPERATIONS LEAD there was a lack of visible role models Alice Green in the industry. [email protected] WHAT’S NEXT? All 100 are WHAT? The Top 100 was our catalysts for change. They strive for PRODUCTION response. We wanted to provide innovation, the newest technologies Stuart Moody a showcase for the most inspiring and pioneering business models. They Denise Burrows individuals in industry, to illustrate acclimatise, pivot and plunge forward the enthusiasm and commitment as the markets and competition around present in modern manufacturing and them evolve. They are the driving force to underscore the exciting, well-paid behind the country’s manufacturing and rewarding careers that exist in the renaissance, and to understand their sector. -

2002 Ford Motor Company Annual Report

2228.FordAnnualCovers 4/26/03 2:31 PM Page 1 Ford Motor Company Ford 2002 ANNUAL REPORT STARTING OUR SECOND CENTURY STARTING “I will build a motorcar for the great multitude.” Henry Ford 2002 Annual Report STARTING OUR SECOND CENTURY www.ford.com Ford Motor Company G One American Road G Dearborn, Michigan 48126 2228.FordAnnualCovers 4/26/03 2:31 PM Page 2 Information for Shareholders n the 20th century, no company had a greater impact on the lives of everyday people than Shareholder Services I Ford. Ford Motor Company put the world on wheels with such great products as the Model T, Ford Shareholder Services Group Telephone: and brought freedom and prosperity to millions with innovations that included the moving EquiServe Trust Company, N.A. Within the U.S. and Canada: (800) 279-1237 P.O. Box 43087 Outside the U.S. and Canada: (781) 575-2692 assembly line and the “$5 day.” In this, our centennial year, we honor our past, but embrace Providence, Rhode Island 02940-3087 E-mail: [email protected] EquiServe Trust Company N.A. offers the DirectSERVICE™ Investment and Stock Purchase Program. This shareholder- paid program provides a low-cost alternative to traditional retail brokerage methods of purchasing, holding and selling Ford Common Stock. Company Information The URL to our online Investor Center is www.shareholder.ford.com. Alternatively, individual investors may contact: Ford Motor Company Telephone: Shareholder Relations Within the U.S. and Canada: (800) 555-5259 One American Road Outside the U.S. and Canada: (313) 845-8540 Dearborn, Michigan 48126-2798 Facsimile: (313) 845-6073 E-mail: [email protected] Security analysts and institutional investors may contact: Ford Motor Company Telephone: (313) 323-8221 or (313) 390-4563 Investor Relations Facsimile: (313) 845-6073 One American Road Dearborn, Michigan 48126-2798 E-mail: [email protected] To view the Ford Motor Company Fund and the Ford Corporate Citizenship annual reports, go to www.ford.com. -

AUTOMOTIVE MANAGEMENT June 2018 £8.00

AUTOMOTIVE MANAGEMENT www.am-online.com June 2018 £8.00 NEW MOT RULES / P6 Tougher test may boost workshop volumes SUBARU / P34 We have turned a corner, says MD Chris Graham DIGITAL DEALER / P41 Technology to help you in new sales, used sales and aftersales STEPHEN BRIGHTON – HEPWORTH MOTOR GROUP / P24 ‘WE WANT TO GROW, BUT NOT AT ANY COST’ adRocket Using the iConsent module, on average customers select the following marketing options: FP_AM_Advert1605id3486601.pdf 16.05.2018 15:56 EDITOR’S LETTER he label ‘Made in Germany’ has long been regarded as a stamp of quality, given the country’s reputation for engineering and attention to detail. However, it seems that ‘Decided by Germany’ is becoming a painful reality for some UK franchised dealers. BMW has received a public thrashing during an inquest into a fatal car crash in the early hours of Christmas Day, 2016. Woking Coroner’s Court heard that the crash occurred after Narayan Gurung, a former Gurkha in his 60s, swerved to avoid an unlit BMW, which had broken down on a major road. T It emerged at the inquest that BMW had known about an electrical fault that caused some cars to stall and lose their lights since 2011. It had recalled vehicles in some other countries, but not in the UK. Shamefully, it did not recall them until after Gurung’s death. Even then, it recalled 36,410 cars, fewer than 10% of the number the DVSA asked for. BMW UK was unable to explain the delay at the inquest, except to say that recall “decisions are made in Germany” and the fault was not considered “critical”. -

Auto 04 Temp.Qxd

FORD AUTOTEAM THE MAGAZINE FOR ALL FORD DEALER STAFF ISSUE 3/2016 EDITORIAL Changing Times It’s all change for the management team at the Henry Ford Academy. Stuart Harris has moved on to a new position within Ford of Europe and, as I move into his role, I hope to continue with his goal of driving up training standards. Also joining the team is new Academy Principle, Kevin Perks, who brings with him a lifetime of automotive industry experience. Dan Savoury, the new Vice Principal, joined the Academy earlier this year and also has a wealth of industry and training experience that will help us continue to improve our training which, in turn, benefits your business. I hope to use the experience gained in my previous sales and marketing roles within Ford to help our training continue to grow in scope and quality. It is a really exciting time to be a part of the Ford family; with new vehicles joining the range and new technology transforming the industry more widely. Good training is vital to our success and we continue to strive to achieve the highest standards and keep you up to date with this rapidly changing industry, from the technical training for the All-new Ford Mustang detailed on page 4, to ensuring our Commercial Vehicle Sales staff can give their customers the best advice with courses such as Commercial Vehicle Type Approval and Legislation on page 30. The success of our training programmes is demonstrated in this issue, with Chelsea Riddle from TrustFord in Bradford a great example of what the Ford Masters Apprenticeship scheme offers to young people, or the success that Mike Gates from Dinnages Ford in Burgess Hill has achieved with a university scholarship through the Henry Ford Academy. -

Don't Leave Your Cars Sitting in the Dark. Put Them in The

AM100 Top 100 table FOR MORE DETAILS SEE PAGE 26 Headline sponsors Rank (2012) Name T/O 2013 (£,000) T/O 2012 (£,000) Outlets 2013 Outlets 2012 Total cars Total LCV Rank (2012) Name T/O 2013 (£,000) T/O 2012 (£,000) Outlets 2013 Outlets 2012 Total cars Total LCV Rank (2012) Name T/O 2013 (£,000) T/O 2012 (£,000) Outlets 2013 Outlets 2012 Total cars Total LCV Rank (2012) Name T/O 2013 (£,000) T/O 2012 (£,000) Outlets 2013 Outlets 2012 Total cars Total LCV 1 (1) Pendragon Plc 3,635,100 3,465,800 238 222 246,100 n/a 26 (26) Eastern Western Motor Group 346,000 325,000 27 27 n/a n/a 51 (61) Motorline 199,769 166,290 21 20 11,965 n/a 76 (75) Brindley Garages 135,000 140,000 18 17 n/a n/a 2 (2) Sytner Group 3,001,000 2,500,000 141 138 105,224 n/a 27 (31) Harwoods 340,898 276,814 16 15 8,021 n/a 52 (58) Johnsons Cars 194,200 171,000 23 22 13,409 n/a 77 (80) Macrae & Dick 134,802 127,709 11 10 n/a n/a 3 (3) Arnold Clark Automobiles 2,604,080 2,253,071 197 154 202,377 n/a 28 (23) Park’s Motor Group 340,000 340,000 37 29 n/a n/a 53 (59) Caffyns Plc 191,760 170,192 14 18 n/a n/a 78 (87) Jacksons Bournemouth 134,000 117,791 10 8 4,296 n/a 4 (5) Lookers Plc 2,163,100 1,898,500 118 109 n/a n/a 29 (22) Pentagon Motor Holdings 339,990 377,753 29 25 25,128 4,861 54 (50) Donnelly Bros Garages (Dungannon) 189,000 185,000 30 32 11,033 2,257 79 (95) Heritage Automotive 130,618 101,146 12 12 n/a n/a 5 (4) Inchcape Retail 2,096,400 2,023,200 113 116 n/a n/a 30 (44) Peter Vardy 312,941 206,982 10 9 13,229 389 55 (52) CEM Day 186,205 181,000 11 11 8,202 3,096 80 -

2013 ANNUAL REPORT the UK’S Leading Car Retailer CONTENTS

2013 ANNUAL REPORT The UK’s leading car retailer CONTENTS AT A GLANCE 2 OUR OPERATIONAL AND FINANCIAL HIGHLIGHTS 7 OUR CHAIRMAN 11 OUR MARKETS AND BUSINESSES 12 Our Markets 12 Our Businesses 20 OUR BUSINESS MODEL AND STRATEGY 26 Business Model 26 STRATEGIC REVIEW Strategy 28 Key Performance Indicators 30 Risk Overview and Management 34 Our People 38 OPERATIONAL AND FINANCIAL REVIEW 40 Operational Review 40 Financial Review 44 DIRECTORS' REPORTS 50 Board of Directors 51 Chairman's Corporate Governance Letter to Shareholders 52 Corporate Governance Report 53 Corporate Social Responsibility Report 59 Committee Reports 62 Directors' Remuneration Report 68 GOVERNANCE Directors' Report 90 Directors' Responsibility Statement 96 INDEPENDENT AUDITORS REPORT 98 FINANCIAL STATEMENTS 102 Consolidated Income Statement 102 Consolidated Statement of Comprehensive Income 103 Consolidated Statement of Changes in Equity 104 Consolidated Balance Sheet 105 Consolidated Cash Flow Statement 106 Reconciliation of Net Cash Flow to Movement in Net Debt 107 FINANCIALS Notes to the Financial Statements 108 Company Balance Sheet 171 Reconciliation of Movements in Shareholders’ Funds of the Company 172 Notes to the Financial Statements of the Company 173 Shareholder Information 180 5 Year Group Review 181 AT A GLANCE THE UK’S LEADING AUTOMOTIVE RETAILER Pendragon’s principal markets are the retailing of new and used vehicles and the service and repair of vehicles (aftersales). Pendragon also operates in the dealership management system, leasing and wholesales parts markets. Brands Stratstone California 02 Mercedes-Benz GL 63 AMG available from Stratstone.com 02 AT A GLANCE What we do The UK's leading automotive retailer in the UK with 225 franchise points selling new and used vehicles and conducting service and repair activity (aftersales). -

Full Property Address Primary Liable

Full Property Address Primary Liable party name 2019 Opening Balance Current Relief Current RV Write on/off net effect 119, Westborough, Scarborough, North Yorkshire, YO11 1LP The Edinburgh Woollen Mill Ltd 35249.5 71500 4 Dnc Scaffolding, 62, Gladstone Lane, Scarborough, North Yorkshire, YO12 7BS Dnc Scaffolding Ltd 2352 4900 Ebony House, Queen Margarets Road, Scarborough, North Yorkshire, YO11 2YH Mj Builders Scarborough Ltd 6240 Small Business Relief England 13000 Walker & Hutton Store, Main Street, Irton, Scarborough, North Yorkshire, YO12 4RH Walker & Hutton Scarborough Ltd 780 Small Business Relief England 1625 Halfords Ltd, Seamer Road, Scarborough, North Yorkshire, YO12 4DH Halfords Ltd 49300 100000 1st 2nd & 3rd Floors, 39 - 40, Queen Street, Scarborough, North Yorkshire, YO11 1HQ Yorkshire Coast Workshops Ltd 10560 DISCRETIONARY RELIEF NON PROFIT MAKING 22000 Grosmont Co-Op, Front Street, Grosmont, Whitby, North Yorkshire, YO22 5QE Grosmont Coop Society Ltd 2119.9 DISCRETIONARY RURAL RATE RELIEF 4300 Dw Engineering, Cholmley Way, Whitby, North Yorkshire, YO22 4NJ At Cowen & Son Ltd 9600 20000 17, Pier Road, Whitby, North Yorkshire, YO21 3PU John Bull Confectioners Ltd 9360 19500 62 - 63, Westborough, Scarborough, North Yorkshire, YO11 1TS Winn & Co (Yorkshire) Ltd 12000 25000 Des Winks Cars Ltd, Hopper Hill Road, Scarborough, North Yorkshire, YO11 3YF Des Winks [Cars] Ltd 85289 173000 1, Aberdeen Walk, Scarborough, North Yorkshire, YO11 1BA Thomas Of York Ltd 23400 48750 Waste Transfer Station, Seamer, Scarborough, North Yorkshire, -

UK Annual Report 2015 (Including the Transparency Report)

Investing to become the Clear Choice UK Annual Report 2015 (including the Transparency Report) December 2015 KPMG.com/uk Highlights Strategic report Profit before tax and Revenue members’ profit shares £1,958m £383m (2014: £1,909m) (2014: £414m) +2.6% -7% 2013 2014 2015 2013 2014 2015 Average partner Total tax payable remuneration to HMRC £623k £786m (2014: £715K) (2014: £711m) -13% +11% 2013 2014 2015 2013 2014 2015 Contribution Our people UK employees KPMG LLP Annual Report 2015 Annual Report KPMG LLP 11,652 Audit Advisory Partners Tax 617 Community support Organisations supported Audit Tax Advisory Contribution Contribution Contribution £197m £151m £308m (2014: £181m) (2014: £129m) (2014: £324m) 1,049 +9% +17% –5% (2014: 878) © 2015 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Strategic report Contents Strategic report 4 Chairman’s statement 10 Strategy 12 Our business model 16 Financial overview 18 Audit 22 Solutions 28 International Markets and Government 32 National Markets 36 People and resources 40 Corporate Responsibility 46 Our taxes paid and collected 47 Independent limited assurance report Governance 52 Our structure and governance 54 LLP governance 58 Activities of the Audit & Risk Committee in the year 59 Activities of the Nomination & Remuneration Committee in the year KPMG in the UK is one of 60 Activities of the Ethics Committee in the year 61 Quality and risk management the largest member firms 2015 Annual Report KPMG LLP 61 Risk, potential impact and mitigations of KPMG’s global network 63 Audit quality indicators 66 Statement by the Board of KPMG LLP providing Audit, Tax and on effectiveness of internal controls and independence Advisory services. -

Luxury Carmaker Bentley to Axe 1,000 UK Jobs 5 June 2020

Luxury carmaker Bentley to axe 1,000 UK jobs 5 June 2020 Car dealership group Lookers said Thursday that it would axe about 1,500 jobs and shut 12 showrooms. James Bond's favourite carmaker Aston Martin meanwhile cut 500 jobs in response to tumbling demand and ballooning losses at the luxury group that began long before the virus appeared. It comes as car dealerships in England reopened this week as the UK government relaxed COVID-19 measures that slammed the brakes on vehicle sales. Car sales had screeched to a near halt in April and Credit: CC0 Public Domain May after Britain's lockdown imposed on March 23. © 2020 AFP German-owned luxury car brand Bentley on Friday said it would axe around 1,000 jobs in the UK as the market weathers the coronavirus-induced downturn. The carmaker, a Volkswagen division that employs 4,200 workers in Britain, said fallout from the COVID-19 outbreak "hastened" its move to cut almost one-quarter of the UK workforce. "Losing colleagues is not something we are treating lightly but this is a necessary step that we have to take to safeguard the jobs of the vast majority who will remain, and deliver a sustainable business model for the future," said Bentley Motors chairman and chief executive Adrian Hallmark. "COVID-19 has not been the cause of this measure but a hastener," he added. Friday's news caps a grim week for Britain's automotive sector, which has been slammed by tanking demand as a result of the coronavirus lockdown. 1 / 2 APA citation: Luxury carmaker Bentley to axe 1,000 UK jobs (2020, June 5) retrieved 23 September 2021 from https://techxplore.com/news/2020-06-luxury-carmaker-bentley-axe-uk.html This document is subject to copyright.