1.1. Software

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2014 Registration Document Annual Financial Report Contents

2014 REGISTRATION DOCUMENT ANNUAL FINANCIAL REPORT CONTENTS 1 4 Presentation of the Company Financial Information 129 and its activities 5 4.1 Analysis on Capgemini 2014 Group consolidated 1.1 Milestones in the Group’s history and its values 6 results AFR 130 1.2 The Group’s activities 8 4.2 Consolidated accounts AFR 136 1.3 Main Group subsidiaries and simplified 4.3 Comments on the Cap Gemini S.A. Financial organization chart 13 Statements AFR 195 1.4 The market and the competitive environment 15 4.4 Cap Gemini S.A. financial statements AFR 197 1.5 2014, a year of strong growth 17 4.5 Other financial and accounting information AFR 221 1.6 The Group’s investment policy, financing policy and market risks AFR 25 1.7 Risk analysis AFR 26 5 CAP GEMINI and its shareholders 223 2 5.1 Cap Gemini S.A. Share Capital AFR 224 5.2 Cap Gemini S.A. and the stock market 229 Corporate governance 5.3 Current ownership structure 233 and Internal control 33 5.4 Share buyback program AFR 235 2.1 Organization and activities of the Board of Directors AFR 35 6 2.2 General organization of the Group AFR 54 2.3 Compensation of executive corporate officers AFR 58 2.4 Internal control and risk management Report of the Board of Directors procedures AFR 70 and draft resolutions 2.5 Statutory Auditors’ report prepared in accordance with Article L.225-235 of the French Commercial of the Combined Shareholders’ Code on the report prepared by the Chairman Meeting of May 6, 2015 237 of the Board of Directors AFR 79 6.1 Resolutions presented at the Ordinary Shareholders’ -

Carbon Footprint & Energy Transition Report

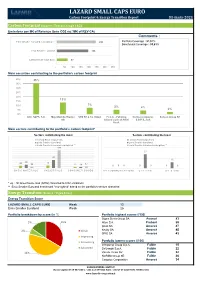

LAZARD SMALL CAPS EURO Carbon Footprint & Energy Transition Report 31-mars-2021 Carbon Footprint (Source : Trucost, scope 1&2) Emissions per M€ of Revenue (tons CO2 éq.*/M€ of REV CA) Comments : Emix Smaller Euroland reweighted ** 242 Portfolio Coverage : 97,51% Benchmark Coverage : 93,61% Emix Smaller Euroland 196 Lazard Small Caps Euro 67 - 50 100 150 200 250 300 350 Main securities contributing to the portfolio's carbon footprint 40% 35% 35% 30% 25% 20% 13% 15% 10% 7% 5% 4% 5% 2% 0% Altri, SGPS, S.A. Mayr-Melnhof Karton STO SE & Co. KGaA F.I.L.A. - Fabbrica Corticeira Amorim, Surteco Group SE AG Italiana Lapis ed Affini S.G.P.S., S.A. S.p.A. Main sectors contributing to the portfolio's carbon footprint* Sectors contributing the most Sectors contributing the least Lazard Small Caps Euro Lazard Small Caps Euro Emix Smaller Euroland Emix Smaller Euroland Emix Smaller Euroland reweighted ** Emix Smaller Euroland reweighted ** 193 27 87 12 35 28 24 13 17 12 11 00 0 0 0 0 0 BASIC MATERIALS INDUSTRIALS CONSUMER GOODS TELECOMMUNICATIONS UTILITIES OIL & GAS * eq. : All Greenhouse Gas (GHG) converted to CO2 emissions ** Emix Smaller Euroland benchmark "reweighted" based on the portfolio's sectors allocation Energy Transition (Source : Vigeo Eiris) Energy Transition Score LAZARD SMALL CAPS EURO Weak 13 Emix Smaller Euroland Weak 25 Portfolio breakdown by score (in %) Portfolio highest scores (/100) Sopra Steria Group SA Avancé 83 5% 10% Alten S.A. Probant 59 Ipsos SA Amorcé 47 2% Weak Nexity SA Amorcé 45 SPIE SA Amorcé 43 Improving Portfolio lowest scores (/100) Convincing Interpump Group S.p.A. -

Tech Procurement in the UK Justice Sector

Tech Procurement in the UK Justice Sector December 2020 Trusted Insight on Government Contracts and Spend Trusted by suppliers, the public sector, and the media — Corporate Government Media 550+ Press citations since Jan 2019 “Serious-minded business data provider Tussell” Matthew Vincent 22nd September 2018 2 | Trends and Opportunities in the Justice Sector We transform open data into useful data – so you don’t have to — Open data Third party data Useful data Use cases CONTRACT DATA Public Sector Aggregate Get better value from TED (EU) suppliers Companies House Contracts Finder (UK), Sell2Wales, PCS Match Digital Marketplace Suppliers Normalise Win government Circa 70 local portals contracts Cleanse SPEND DATA Moody’s Analytics 6800+ Central Gov’t, Press Local Gov’t & NHS Machine Scrutinise public bodies learn spending 3 | Trends and Opportunities in the Justice Sector Total data coverage: Justice — Spend Contracts Q1 2016 – Q2 2020 Q1 2015 – Q3 2020 864,000 invoices 7,000 contracts £28bn spend value £17bn contract value 43 buyers 100 buyers 31,000 suppliers 2,600 suppliers 4 | Trends and Opportunities in the Justice Sector Questions Tussell will answer — 1. How big is the market? 2. What’s the breakdown by sub-sector? 3. Can new entrants break through? 4. Has demand recovered from Covid? 5. How can I position my firm for future rebids? 5 | Procurement in the UK EdTech market Technology spend in the justice sector in the five years from 2016-2020 was £3bn in total, an average of £597m per annum Spend data £728M £710M Average: £597M £578M -

Projet De Note En Réponse) Which Was Filed with the French Autorité Des Marchés Financiers on 23 September 2019 and Which Remains Subject to Its Review

This document is an unofficial English-language translation of the draft response document (projet de note en réponse) which was filed with the French Autorité des marchés financiers on 23 September 2019 and which remains subject to its review. In the event of any differences between this unofficial English- language translation and the official French draft response document, the official French draft response document shall prevail. The draft offer and this draft response document remain subject to the French Financial Market's Authority review. DRAFT DOCUMENT PREPARED BY IN RESPONSE TO THE PUBLIC TENDER OFFER FOR THE SHARES OF THE COMPANY ALTRAN TECHNOLOGIES LAUNCHED BY This draft response document (projet de note en réponse) was filed with the French Financial Markets Authority (the "AMF") on 23 September 2019, in accordance with the provisions of Article 231-26 of the AMF's general regulation. It was prepared in accordance with Article 231-19 of the AMF's general regulation. The draft offer and this draft response document remain subject to the review of the AMF. Important notice Pursuant to Articles 231-19 and 261-1 et seq. of the AMF's general regulation, the report of Finexsi, acting in its capacity as independent expert, is included in this draft response document. This draft response document (the "Draft Response Document") is available on the websites of ALTRAN (www.altran.com) and the AMF (www.amf-france.org) and may be obtained free of charge from Altran Technologies' registered office at 96, avenue Charles de Gaulle, 92200 Neuilly-sur-Seine – FRANCE. In accordance with the provisions of Article 231-28 of the AMF's general regulation, information relating to Altran Technologies, in particular legal, financial and accounting information, will be filed with the AMF and made available to the public in the same manner no later than the day before the opening of the tender offer. -

USER GROUP »Governance, Risk, Compliance in Der IT« 14

USER GROUP »Governance, Risk, Compliance in der IT« 14. Arbeitstreffen Leipzig, 26./27. April 2018 THEMENSCHWERPUNKT „Governance, Risk & Control von IT-Sourcing und Cloud Computing: Anforde- rungen, Herausforderungen und Lösungsansätze“ FACHLICHE LEITUNG Prof. Dr. Nils Urbach Universität Bayreuth MITGLIEDER DER USER GROUP MEDIENPARTNER ORGANISATORISCHES TERMIN 26./27. April 2018 ANSPRECHPARTNER Yvonne Weißflog Seite | 2 T +49 341 98988-422 F +49 341 98988-9444 E [email protected] VERANSTALTUNGSORT Alte Essig-Manufactur Paul-Gruner-Straße 44 | 04107 Leipzig T +49 341 2 67 80 I www.michaelis-leipzig.de/de/alte-essig- manufactur/ ABENDVERANSTALTUNG Weinwirtschaft Leipzig Thomaskirchhof 13/14 | 04109 Leipzig T +49 341 49614606 I www.weinwirtschaft-leipzig.de HOTEL Eine Auswahl an Übernachtungsmöglichkeiten finden Sie unter: www.softwareforen.de/hotelempfehlungen Bitte nutzen Sie die Buchungscodes des jeweiligen Hotels, um auf die vergünstigten Konditionen der Leipziger Foren zuzugreifen. User Group »Governance, Risk, Compliance in der IT« www.softwareforen.de/it-governance RÜCKBLICK ARBEITSTREFFEN 13. Arbeitstreffen – 23./24. November 2017 Policies vs. Geschäftsziele: IT-GRC im Spannungsfeld von Effektivität und angemessener Regelungstiefe Seite | 3 12. Arbeitstreffen – 04./05. Mai 2017 Tools & Co: Automatisierung von IT-GRC - Wie bitte? Anforderungen, Möglichkeiten & Erfahrungsberichte 11. Arbeitstreffen – 10./ 11. November 2016 IT-Konsumerisierung, Cloud Computing und Schatten-IT: Neue Anforde- rungen an das GRC im Zeitalter der Digitalisierung? 10. Arbeitstreffen – 21./22. April 2016 Flexibilität vs. Kontrolle: Erfahrungen und Best Practices aus den aktuellen Anforderungen an die IT-Compliance 9. Arbeitstreffen – 26./ 27. November 2015 SIEM – Schluss mit dem Unwissen über die Gefahr? 8. Arbeitstreffen – 5./6. Mai 2015 Management und Controlling von IT-Risiken 7. -

Empresas Adjudicatarias Del Acuerdo Marco Para El Servicio De Desarrollo De Sistemas De Información

Empresas adjudicatarias del acuerdo marco para el servicio de desarrollo de sistemas de información. AM 26/2011. - ALTEN SOLUCIONES PRODUCTOS AUDITORIA E INGENIERIA, S.A.U. ** - ATOS ORIGIN S.A.E. ** - BULL ESPAÑA, S.A. ** - CAPGEMINI ESPAÑA, S.L. ** - EVERIS SPAIN, S.L.U. ** - HEWLETT PACKARD ESPAÑOLA, S.L. ** - IBERMÁTICA, S.A. ** - IBM GLOBAL SERVICES ESPAÑA, S.A) ** - INFORMÁTICA EL CORTE INGLÉS, S.A ** - INGENIERIA DE SOFTWARE AVANZADO, S.A ** - SADIEL TECNOLOGIAS DE LA INFORMACIÓN, S.A. * - SERESCO, S.A. * - SERIKAT, CONSULTORÍA E INFORMÁTICA, S.A. ** - SOPRA GROUP INFÓRMATICA, S.A. ** - TECNOCOM ESPAÑA SOLUTIONS, S.L ** - UTE ACCENTURE, S.L.- ACCENTURE OUTSOURCING SERVICES, S.A.Y CORITEL, S.A. * - UTE ALTIA CONSULTORES,S.A.-KPMG ASESORES S.L. ** - UTE ALTRAN INNOVACION, S.L.-GESEIN, S.L.-NEORIS ESPAÑA, S.L. ** - UTE AVENTIA IBERIA, S.L Y EPTISA SERVICIOS DE INGENIERIA, S.L.. ** - UTE AXPE CONSULTING S.L.-ORACLE IBERICA, S.R.L. ** - UTE B2B (COMERCIO ELECTRÓNICO B2B 2OOO, S.A.-TAISA SYVALUE,S.L.- ALBA TECHNOLOGY, S.L. REALTECH SYSTEM CONSULTING, S.L. -INDENOVA, .-TECNICOS ASOCIADO * - UTE BILBOMATICA, S.A & CIBERNOS & GRUPO EIDOS ** - UTE DELOITTE, S.L.-DELOITTE CONSULTING, S.L.-DXD APLICATIONS, IT SOLUTIONS ** - UTE ENTEL IT CONSULTING, S.A. ENTEL IBAI CONSULTING, S.A. NOVASOFT INGENIERIA, S.L. SYSTEMS MAINTENANCE SERVICES EUROPA, S.A. ** - UTE FUJITSU TECHNOLOGY SOLUTIONS, S.A.-DELAWARE CONSULTORIA, S.L. ** - UTE G9 ( BLOM SISTEMAS GEOESPACIALES, S.L.U. EXIS INVERSIONES EN CONSULTORÍA INFORMÁTICA Y TECNOLOGÍA, S.A.-INTELIGENCIA SISTEMÁTICA 4, S.L., ARISTA * - UTE GMV SOLUCIONES GLOBALES DE INTERNET, S.A. GMV AEROSPACE AND DEFENCE, S.A. -

Continued Improvement in Business Activity in Q1 2021

Press release Continued improvement in business activity in Q1 2021 . Revenue growth totalling 2.2% 1 . Clear improvement in organic revenue growth (-0.5%) with respect to the past three quarters . Buoyant market conditions confirming the outlook of a return to organic revenue growth starting in Q2 2021 Paris, 28 April 2021, 7:00 a.m. – Sopra Steria generated revenue of €1,165.2 million in the first quarter of 2021, representing growth of 2.2%. Changes in scope had a positive impact of €32.9 million. The impact of currency fluctuations was virtually neutral (-€1.4 million). At constant scope and exchange rates, revenue contracted slightly (0.5%). Sopra Steria: Consolidated revenue – Q1 2021 Organic Total €m / % Q1 2021 Q1 2020 growth growth Revenue 1,165.2 1,140.1 -0.5% 2.2% Comments on Q1 2021 business activity Market conditions were buoyant in Q1 2021. Business activity was brisk and improved with respect to previous quarters. The public sector and defence remained highly active. As an illustration, several major contracts in these two sectors were announced during the quarter: Brasidas (a unique new information system for ensuring the operational readiness of aeronautics equipment) for the French Defence Ministry, cybersecurity for the EU agencies eu-LISA and Frontex, the development of a centralised border control system for the French Interior Ministry, and the development of a national road traffic information system for Highways England. All the other vertical markets, to varying extents, saw improved trends. In this context, and with downtime lower than in Q1 2020, recruitment picked up again starting at the beginning of the year. -

(EC HARRIS) £23317.00 Asset Clearing Aug-16 Balanc

Service Unit Supplier Amount Account Name Period Balance Sheet ARCADIS LLP (E C HARRIS) £23,317.00 Asset Clearing Aug-16 Balance Sheet AURA GRAPHICS LTD (SSDM) £713.00 Asset Clearing Aug-16 Balance Sheet AURA GRAPHICS LTD (SSDM) £1,101.50 Asset Clearing Aug-16 Balance Sheet REDACTED - LAW ENFORECEMENT £3,475.00 Asset Clearing Aug-16 Balance Sheet REDACTED - LAW ENFORECEMENT £9,763.00 Asset Clearing Aug-16 Balance Sheet FORD MOTOR COMPANY LTD £11,760.02 Asset Clearing Aug-16 Balance Sheet HONDA UK £5,824.27 Asset Clearing Aug-16 Balance Sheet MICHELMORES LLP £2,158.00 Asset Clearing Aug-16 Balance Sheet MIDDLESBROUGH BOROUGH COUNCIL £1,500.00 Asset Clearing Aug-16 Balance Sheet PATCHSAVE SOLUTIONS LTD £997.90 Asset Clearing Aug-16 Balance Sheet PATCHSAVE SOLUTIONS LTD £737.08 Asset Clearing Aug-16 Balance Sheet PCC FOR NORTH YORKSHIRE £3,176.17 Asset Clearing Aug-16 Balance Sheet PCC FOR NORTH YORKSHIRE £2,708.60 Asset Clearing Aug-16 Balance Sheet PCC FOR NORTH YORKSHIRE £3,641.09 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO £8,770.74 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO £12,199.91 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO £12,199.91 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO £12,199.91 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO £12,199.91 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO £12,199.91 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO £12,199.91 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO £12,199.91 Asset Clearing Aug-16 Balance Sheet PEUGEOT MOTOR CO -

Internal Rules and Regulations of the Board of Directors

IRR Version 22/10/2020 SOPRA STERIA GROUP Société Anonyme with share capital of €20,547,701 326 820 065 RCS ANNECY Registered office: PAE Les Glaisins, Annecy-le-Vieux, 74940 Annecy – France Head office: 6 avenue Kleber, 75116 Paris – France INTERNAL RULES AND REGULATIONS OF THE BOARD OF DIRECTORS Introduction The Board of Directors of Sopra Steria Group operates according to the rules established by law, the Company’s Articles of Association and the recommendations contained in the AFEP- MEDEF corporate governance code to which the Company refers. Its organisational and operating methods are set out in these internal rules and regulations. The internal rules and regulations of the Board of Directors are not part of the Articles of Association of Sopra Steria Group. They are not binding on third parties. They may not be invoked by third parties or Sopra Steria Group shareholders against Sopra Steria Group or its company officers. These internal rules and regulations apply to all company officers (Directors, Executive Management), as well as any Non-Voting Directors, Works Council representatives, persons invited to meetings in connection with the items on the agenda of the Board of Directors, members of the Company’s Executive Committee, and, more generally, any person with access to the documents (preparatory or final) produced for meetings of the Board of Directors and/or its Committees. These internal rules and regulations were last amended at the Board of Directors’ meeting on 22 October 2020. Page 1 of 15 IRR Version 22/10/2020 Table of articles Article 1 – Role of the Board of Directors ............................................................................................. -

IDC Fintech Rankings Top 100

IDC FinTech Rankings Top 100 Ranking Company Ranking Company Ranking Company 1 FIS 42 Sopra Banking Software 82 Nucleus Software IDC Financial Insights 2 Tata Consultancy Services Limited 43 Sinosoft Company Limited 83 Diasoft 3 NTT DATA 44 IPC 84 Novantas, Inc. FinTech Rankings 4 Fiserv 45 Experian 85 Kasasa Top 25 Enterprise 5 Cognizant Technology Solutions 46 Pegasystems Inc. 86 Celero 6 SS&C Technologies 47 GFT Technologies SE 87 Capital Asset Planning, Inc. 7 Infosys Limited 48 Ping An Technology 88 Doxim Ranking Company 8 NCR Corporation 49 Yunnan Nantian Electronics Information Corp.,LTD. 89 TAS Group E1 IBM 9 Diebold Nixdorf 50 Murex 90 BPC Banking Technologies E2 Microsoft 10 Global Payments 51 Pactera Jinxin 91 MX E3 Dell 11 NRI (Nomura Research Institute, Ltd. ) 52 CRIF S.p.A. 92 ARGO Data Resource Corporation E4 Deloitte 12 Finastra 53 Refinitiv 93 Sinqia E5 Accenture 13 Jack Henry & Associates, Inc. 54 Yusys Technologies Co., Ltd. 94 xQuant Company, Ltd. E6 Cisco Systems, Inc. 14 Ingenico 55 BearingPoint 95 DCI (Data Center Inc) E7 Intel 15 CoreLogic 56 Bottomline Technologies 96 Baker Hill E8 DXC Technology 16 TransUnion 57 Q2 Holdings, Inc. (Q2) 97 ARCA E9 Oracle 17 Broadridge Financial Solutions, Inc 58 Fundbox 98 Zhejiang Bangsun Technology CO.,Ltd. E10 Capgemini 18 Moody’s Analytics, Inc. 59 EVERTEC, Inc. 99 Featurespace E11 Hitachi, Ltd. 19 Equifax 60 Computer Services, Inc. (CSI) 100 VSoft E12 Fujitsu 20 ACI Worldwide 61 Simplex Inc. E13 Hewlett Packard Enterprise 21 SAS 62 Intellect Design Arena Ltd E14 SAP SE 22 Virtu Financial 63 Linedata Services E15 Wipro Limited 23 Worldline 64 Silverlake Axis Limited E16 Atos 24 Black Knight 65 NeoXam E17 Amazon (AWS) 25 GLORY 66 OneConnect E18 HCL Technologies 26 Genpact 67 nCino E19 CGI 27 FICO 68 Calypso Technology, Inc. -

Mergers & Acquisitions Leverage

Mergers & Acquisitions Mergers & Acquisitions Leverage Transforming insights into M&A solutions Vol. 5 Issue 1 2016 Risk. Reinsurance. Human Resources. Editorial Contents It has been an interesting first year. EMEA specifically showed a 5 year low half of 2016. The global economy at USD 428.4 billion – 14% lower than H1 continues to struggle and the IMF 2015ii. Whether we consider H1 deal values, predicts 2016 global GDP growth quarter-by-quarter performance or cross- at 3.16% i. Major economies in border activity, 2016 is showing a drop from Europe, Asia Pacific, Japan & 2015. However, not all regions have shown a the Middle East continue to be decline. China in particular continues to spend 02 sluggish, while there are some on transactions, and this trend appears set to COVER FEATURE bright spots in the US, Germany continue throughout the near future. Germany and India. The impact of Brexit is also appears to have made a comeback from the yet to be fully predicted or 2015 dip, with increased figures both as a buyer Driving Change in assimilated into the European and indeed the and a seller. global economy. Headwinds on the global Times of Organizational economy will continue to impact the overall With this backdrop of global uncertainty with Transformation investment climate, trade and cross-border pockets of opportunity for cross-border and deals. But for individual countries, the inner in-country deals, this issue brings to you articles The Mantra Unlocked market dynamics will continue to drive industry that will help throw light on various elements. consolidations and some organic growth ‘Driving Change in Times of Organizational outside of home country, etc. -

Mise En Page 1

40, avenue André Morizet 92514 Boulogne-Billancourt Cedex www.alten.fr Technology Consulting and Engineering Business Report 2008 This document and the corresponding business report constitute the ALTEN reference document for the 2008 fiscal year. It was submitted to France’s financial market authority (Autorité des Marchés Financiers) on 3 June 2009 in accordance with Article 212-13 of the Autorité des Marchés Financiers’ general regulations. This Reference Document may be used in connection with a financial transaction if it is accompanied by a prospectus approved by the Autorité des Marchés Financiers. Furthermore, pursuant to Article 28 of Directive No. 809/2004 of the European Commission, the following information is incorporated by reference in this Reference Document: - The company and consolidated financial statements at 31 December 2007, along with the related reports prepared by the Statutory Auditors and presented on pages 137 through 194 of reference document no. D.08-0297 filed with the Autorité des Marchés Financiers on 25 April 2008. - The company and consolidated financial statements at 31 December 2006, along with the related reports prepared by the Statutory Auditors, presented on pages 88 through 149 of reference document no. D.07-0593 filed with the Autorité des Marchés Financiers on 14 June 2007. It was prepared by the issuer under the responsibility of the persons who signed it. Rapport d’activité ALTEN 2007 Sommaire BUSINESS REPORT I - GROUP GOVERNANCE Page Message from the Chairman 5 The Board of Directors and