Mergers & Acquisitions Leverage

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2014 Registration Document Annual Financial Report Contents

2014 REGISTRATION DOCUMENT ANNUAL FINANCIAL REPORT CONTENTS 1 4 Presentation of the Company Financial Information 129 and its activities 5 4.1 Analysis on Capgemini 2014 Group consolidated 1.1 Milestones in the Group’s history and its values 6 results AFR 130 1.2 The Group’s activities 8 4.2 Consolidated accounts AFR 136 1.3 Main Group subsidiaries and simplified 4.3 Comments on the Cap Gemini S.A. Financial organization chart 13 Statements AFR 195 1.4 The market and the competitive environment 15 4.4 Cap Gemini S.A. financial statements AFR 197 1.5 2014, a year of strong growth 17 4.5 Other financial and accounting information AFR 221 1.6 The Group’s investment policy, financing policy and market risks AFR 25 1.7 Risk analysis AFR 26 5 CAP GEMINI and its shareholders 223 2 5.1 Cap Gemini S.A. Share Capital AFR 224 5.2 Cap Gemini S.A. and the stock market 229 Corporate governance 5.3 Current ownership structure 233 and Internal control 33 5.4 Share buyback program AFR 235 2.1 Organization and activities of the Board of Directors AFR 35 6 2.2 General organization of the Group AFR 54 2.3 Compensation of executive corporate officers AFR 58 2.4 Internal control and risk management Report of the Board of Directors procedures AFR 70 and draft resolutions 2.5 Statutory Auditors’ report prepared in accordance with Article L.225-235 of the French Commercial of the Combined Shareholders’ Code on the report prepared by the Chairman Meeting of May 6, 2015 237 of the Board of Directors AFR 79 6.1 Resolutions presented at the Ordinary Shareholders’ -

Aon Plc 2020 10-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 ____________________________________________________________________________ FORM 10-K (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number: 1-7933 ___________________________________________________________________________________________ Aon plc (Exact name of registrant as specified in its charter) IRELAND 98-1539969 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) Metropolitan Building, James Joyce Street, Dublin 1, Ireland D01 K0Y8 (Address of principal executive offices) (Zip Code) +353 1 266 6000 (Registrant’s Telephone Number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of Each Class Trading Symbol Name of Each Exchange on Which Registered Class A Ordinary Shares, $0.01 nominal value AON New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: NONE ________________________________________________________________________________________________________________________________________________________________________________ Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Carbon Footprint & Energy Transition Report

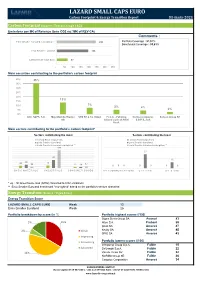

LAZARD SMALL CAPS EURO Carbon Footprint & Energy Transition Report 31-mars-2021 Carbon Footprint (Source : Trucost, scope 1&2) Emissions per M€ of Revenue (tons CO2 éq.*/M€ of REV CA) Comments : Emix Smaller Euroland reweighted ** 242 Portfolio Coverage : 97,51% Benchmark Coverage : 93,61% Emix Smaller Euroland 196 Lazard Small Caps Euro 67 - 50 100 150 200 250 300 350 Main securities contributing to the portfolio's carbon footprint 40% 35% 35% 30% 25% 20% 13% 15% 10% 7% 5% 4% 5% 2% 0% Altri, SGPS, S.A. Mayr-Melnhof Karton STO SE & Co. KGaA F.I.L.A. - Fabbrica Corticeira Amorim, Surteco Group SE AG Italiana Lapis ed Affini S.G.P.S., S.A. S.p.A. Main sectors contributing to the portfolio's carbon footprint* Sectors contributing the most Sectors contributing the least Lazard Small Caps Euro Lazard Small Caps Euro Emix Smaller Euroland Emix Smaller Euroland Emix Smaller Euroland reweighted ** Emix Smaller Euroland reweighted ** 193 27 87 12 35 28 24 13 17 12 11 00 0 0 0 0 0 BASIC MATERIALS INDUSTRIALS CONSUMER GOODS TELECOMMUNICATIONS UTILITIES OIL & GAS * eq. : All Greenhouse Gas (GHG) converted to CO2 emissions ** Emix Smaller Euroland benchmark "reweighted" based on the portfolio's sectors allocation Energy Transition (Source : Vigeo Eiris) Energy Transition Score LAZARD SMALL CAPS EURO Weak 13 Emix Smaller Euroland Weak 25 Portfolio breakdown by score (in %) Portfolio highest scores (/100) Sopra Steria Group SA Avancé 83 5% 10% Alten S.A. Probant 59 Ipsos SA Amorcé 47 2% Weak Nexity SA Amorcé 45 SPIE SA Amorcé 43 Improving Portfolio lowest scores (/100) Convincing Interpump Group S.p.A. -

Tech Procurement in the UK Justice Sector

Tech Procurement in the UK Justice Sector December 2020 Trusted Insight on Government Contracts and Spend Trusted by suppliers, the public sector, and the media — Corporate Government Media 550+ Press citations since Jan 2019 “Serious-minded business data provider Tussell” Matthew Vincent 22nd September 2018 2 | Trends and Opportunities in the Justice Sector We transform open data into useful data – so you don’t have to — Open data Third party data Useful data Use cases CONTRACT DATA Public Sector Aggregate Get better value from TED (EU) suppliers Companies House Contracts Finder (UK), Sell2Wales, PCS Match Digital Marketplace Suppliers Normalise Win government Circa 70 local portals contracts Cleanse SPEND DATA Moody’s Analytics 6800+ Central Gov’t, Press Local Gov’t & NHS Machine Scrutinise public bodies learn spending 3 | Trends and Opportunities in the Justice Sector Total data coverage: Justice — Spend Contracts Q1 2016 – Q2 2020 Q1 2015 – Q3 2020 864,000 invoices 7,000 contracts £28bn spend value £17bn contract value 43 buyers 100 buyers 31,000 suppliers 2,600 suppliers 4 | Trends and Opportunities in the Justice Sector Questions Tussell will answer — 1. How big is the market? 2. What’s the breakdown by sub-sector? 3. Can new entrants break through? 4. Has demand recovered from Covid? 5. How can I position my firm for future rebids? 5 | Procurement in the UK EdTech market Technology spend in the justice sector in the five years from 2016-2020 was £3bn in total, an average of £597m per annum Spend data £728M £710M Average: £597M £578M -

Top Companies for Leaders 2011 Study Insights and Best Practices Asia Pacifi C

Consulting Talent & Rewards Top Companies for Leaders 2011 Study Insights and Best Practices Asia Pacifi c Aon Hewitt I Consulting 1 About Aon Hewitt's Top Companies for Leaders (TCFL) study is one of the the Study most comprehensive studies on organizational leadership practices around the globe. 478 organizations participated in the 2011 global study. Our fi rst study results, published in 2002, uncovered a link between fi nancial success and great leadership practices and identifi ed differentiating elements found only in Top Companies. We conducted this study again in 2003, 2005, 2007 and 2009. The data derived from these fi ve studies provided the foundation for our 2011 study which we believe to be the most comprehensive global study available on leadership to date. Aon Hewitt conducted the 2007, 2009 and 2011 Top Companies for Leaders studies in partnership with FORTUNE and The RBL Group. 2 Top Companies For Leaders 2011 Study Executive Organizations that have great leadership practices demonstrate strong fi nancial results over the long term. Leadership is the single most valuable competitive advantage today. While it helps in gaining an Summary edge over competition, it proves to be even more valuable as economies go through ups and downs. It was within this economic context that Aon Hewitt and its study partners - The RBL Group and FORTUNE - undertook the 2011 Top Companies for Leaders study. Globally, 478 companies participated in the research of which 152 companies were from Asia Pacifi c (APAC). A comprehensive evaluation process comprising of a scan of leadership practices and policies of organizations, in-depth interviews with HR leaders, CEOs and senior leaders, and fi nally blind judging from the shortlist, culminated in the Global Top Companies for Leaders. -

Relatório De Contas 2020 Aon Reinsurance, S.A

Relatório de contas 2020 Aon Reinsurance, S.A Relatório de Gestão Aon Reinsurance, SA Exercício findo em 31 de dezembro de 2020 AON REINSURANCE, S.A. EXERCÍCIO DE 2020 RELATÓRIO DE GESTÃO A sociedade Aon Reinsurance, S.A. tem por objeto a corretagem de resseguros, consultadoria de seguros e, por último, a aquisição de participações no capital de outras sociedades, desde que previamente autorizadas pelo Instituto de Investimento Estrangeiro. GOVERNO SOCIETÁRIO O capital social da sociedade no montante de 100.000 euros, representado por 20.000 ações de valor nominal de 5 Euros, encontra-se integralmente subscrito e realizado, sendo subscrito em 100% pela sociedade Aon Portugal, S.A.. As ações são nominativas, sendo representadas por títulos de uma, cinco, dez, cinquenta e cem ações. Os acionistas gozam direito de preferência na alienação onerosa das ações mesmo a favor de outros acionistas. A administração da Sociedade é exercida por um Conselho de Administração, composto por um número ímpar de membros, de três a nove, eleitos pela Assembleia Geral, que designará também o respetivo presidente, por um período de quatro anos podendo ser reeleitos uma ou mais vezes. O Conselho de Administração reunirá, pelo menos, duas vezes em cada exercício. Compete ao Conselho de Administração, dentro dos limites da lei e dos estatutos da sociedade, deliberar sobre qualquer assunto de administração da sociedade e, nomeadamente, sobre: a) Relatório e contas anuais; b) Aquisição, alienação e oneração de bens imóveis; c) Abertura ou encerramento de estabelecimentos; d) Modificações importantes na organização da Empresa; e) Mudança da sede social e aumento de capital; e f) Aquisição ou alienação de participações sociais de outras sociedades, nos termos legais. -

Workplace Pensions

INDEPENDENT PUBLICATION BY RACONTEUR.NET #0504 28 / 02 / 2018 WORKPLACE PENSIONS FINANCIAL PLANNING TECHNOLOGY CAN BE WHEN DERISKING IS 03 TARGETS SAVINGS GAP 13 THE ‘WOW MOMENT’ 14 THE SAFEST OPTION LOOKING for the key to PENSIONS ENGAGEMENT? Discover how to unlock better retirement outcomes. Call 0344 573 0033 or visit aon.com/pensionsengagement Aon Hewitt Limited and Aon Consulting Limited are authorised and regulated by the Financial Conduct Authority. Aon Hewitt Limited Registered in England & Wales. Registered No: 4396810. Registered Office: The Aon Centre, The Leadenhall Building, 122 Leadenhall Street, London EC3V 4AN. Aon Consulting Limited Registered in England & Wales. Registered No: 03127195. Registered Office: Briarcliff House, Kingsmead, Farnborough GU14 7TE. RACONTEUR.NET 03 FINANCIAL WELLBEING WORKPLACE PENSIONS Holistic fi nancial planning Distributed in Navigating through to target savings gap Published in association with Employers and pension providers are increasingly off ering lifetime uncertain waters fi nancial planning in a bid to engage staff in saving for retirement for pension fund CONTRIBUTORS TIM COOPER broader workplace packages will become more common as compa- inancial wellness has become nies need them to attract the best TIM COOPER VIRGINIA a buzz phrase in the last few talent, he says. Award-winning MATTHEWS years. For employers, it refers Mr Tran says Willis Towers sponsors, trustees freelance financial Freelance writer to anything that supports the Watson’s research shows that the journalist, he and editor, -

Participating Organisations | June 2021 Aon Rewards Solutions Proprietary and Confidential

Aon Rewards Solutions Proprietary and Confidential Participating organisations | June 2021 Aon Rewards Solutions Proprietary and Confidential Participating organisations 1. .au Domain Administration 44. Alexion Pharmaceuticals Limited Australasia Pty Ltd 2. [24]7.ai 45. Alfa Financial Software 3. 10X Genomics* Limited 4. 4 Pines Brewing Company 46. Alibaba Group Inc 5. 8X8 47. Alida* 6. A.F. Gason Pty Ltd* 48. Align Technology Inc. 7. A10 Networks 49. Alkane Resources Limited 8. Abacus DX 50. Allianz Australia Ltd 9. AbbVie Pty Ltd 51. Allscripts 10. Ability Options Ltd 52. Alteryx 11. Abiomed* 53. Altium Ltd 12. AC3 54. Amazon.com 55. AMEC Foster Wheeler 13. ACCELA* Australia Pty Ltd 14. Accenture Australia Ltd 56. Amgen Australia Pty Ltd 15. AccorHotels 57. AMP Services Limited 16. Acer Computer Australia Pty Ltd* 58. AMSC 17. Achieve Australia Limited* 59. Analog Devices 18. Achmea Australia 60. Anaplan 19. ACI Worldwide 61. Ancestry.com 62. Anglo American Metallurgical 20. Acquia Coal Pty Ltd 21. Actian Corporation 63. AngloGold Ashanti Australia 22. Activision Blizzard Limited* 23. Adaman Resources 64. ANZ Banking Group Ltd 24. Adcolony 65. Aon Corporation Australia 25. A-dec Australia 66. APA Group 26. ADG Engineers* 67. Apollo Endosurgery Inc. 27. Adherium Limited 68. APPEN LTD 28. Administrative Services 69. Appian* 29. Adobe Systems Inc 70. Apple and Pear Australia Ltd* 30. ADP 71. Apple Pty Ltd 31. Adtran 72. Apptio 32. Advanced Micro Devices 73. APRA AMCOS 33. Advanced Sterlization 74. Aptean Products* 75. Aptos* 34. AECOM* 76. Apttus 35. AEMO 77. Aquila Resources 36. Aeris Resources Limited 78. Arcadis 37. -

Top 50 Management Andstrategy Consulting Firms

© 2008 AGI-Information Management Consultants May be used for personal purporses only or by libraries associated to dandelon.com network. VAULT GUIDE TO THE TOP 50 MANAGEMENT ANDSTRATEGY CONSULTING FIRMS MARCY LERNER AND THE STAFF OF VAULT UNIVERSlf&T ST. QALLEN HOCHSCHULE FUR WIRTSCHAFTS-, ,ECHTS- UNO SOZIALWISSENSCHAFTEN @ 2004 Vault 1°C. BlBLlOTHEK Table of Contents INTRODUCTION 1 A Guide to This Guide ....................................... .I THE VAULT PRESTIGE RANKINGS 7 Ranking Methodology ........................................ 9 TheVault50 ...............................................10 Practice Area Ranking Methodology ............................ 12 THE VAULT QUALITY OF LIFE RANKINGS 17 Quality of Life Ranking Methodology ........................... 19 Quality of Life: Top 10 ....................................... 20 OVERVIEW OF THE CONSULTING INDUSTRY 27 The State of Consulting ...................................... 29 Practice Areas .............................................. 31 THE VAULT 50 35 1. McKinsey & Company .................................... 36 2 . Boston Consulting Group ................................. SO 3 . Bain& Company ........................................ 60 4 . Booz Allen Hamilton ..................................... 72 5 . Gartner ................................................ 88 6 . Monitor Group .......................................... 94 7 . Mercer Management Consulting ........................... 104 8 . Deloitte ............................................... 114 9 . Mercer Oliver -

2020 Aon Impact Report Contents

2020 Aon Impact Report Contents 4 Welcome 39 Taking Care of Others 42 Innovating To Support Clients Through Volatile Times 5 Our Commitment 48 Helping Communities Recover, Reopen and Thrive 53 Taking Action to Deepen Diversity within Businesses 6 Our Firm and Communities 6 In the Business of Better Decisions 7 Our Solutions 59 Preparing for the Future 9 Driving a One Firm Vision 62 Leading with a Strong Foundation 11 Taking Bold Steps to Establish a New Standard of 68 Reducing Environmental Footprint Client Leadership 74 Protecting Assets, Data and Ensuring Privacy 78 Building Resilient Communities Around the World 16 Taking Care of Our Own 19 Protecting our 50,000 colleagues 88 Impact by the Numbers 24 Investing in Workforce Resilience 31 Prioritizing Our Ongoing Commitment to Inclusion and Diversity The goals, targets and commitments discussed in this report are aspirational. As such, no guarantees or promises are made that these goals, targets and commitments will be met. Statistics and metrics included in this report are in part dependent on the use of estimates and assumptions based on historical levels and projections and are therefore subject to change. This report has not been externally assured or verified by an independent third party. This report is not comprehensive and, for that reason, should be read in conjunction with our filings with the Securities and Exchange Commission, including our Annual Reports on Form 10-K and Quarterly Reports on Form 10-Q, particularly the “Forward-Looking Statements” and “Risk Factors” sections of these filings) and our proxy statements, all of which can be found at ir.aon.com. -

USER GROUP »Governance, Risk, Compliance in Der IT« 14

USER GROUP »Governance, Risk, Compliance in der IT« 14. Arbeitstreffen Leipzig, 26./27. April 2018 THEMENSCHWERPUNKT „Governance, Risk & Control von IT-Sourcing und Cloud Computing: Anforde- rungen, Herausforderungen und Lösungsansätze“ FACHLICHE LEITUNG Prof. Dr. Nils Urbach Universität Bayreuth MITGLIEDER DER USER GROUP MEDIENPARTNER ORGANISATORISCHES TERMIN 26./27. April 2018 ANSPRECHPARTNER Yvonne Weißflog Seite | 2 T +49 341 98988-422 F +49 341 98988-9444 E [email protected] VERANSTALTUNGSORT Alte Essig-Manufactur Paul-Gruner-Straße 44 | 04107 Leipzig T +49 341 2 67 80 I www.michaelis-leipzig.de/de/alte-essig- manufactur/ ABENDVERANSTALTUNG Weinwirtschaft Leipzig Thomaskirchhof 13/14 | 04109 Leipzig T +49 341 49614606 I www.weinwirtschaft-leipzig.de HOTEL Eine Auswahl an Übernachtungsmöglichkeiten finden Sie unter: www.softwareforen.de/hotelempfehlungen Bitte nutzen Sie die Buchungscodes des jeweiligen Hotels, um auf die vergünstigten Konditionen der Leipziger Foren zuzugreifen. User Group »Governance, Risk, Compliance in der IT« www.softwareforen.de/it-governance RÜCKBLICK ARBEITSTREFFEN 13. Arbeitstreffen – 23./24. November 2017 Policies vs. Geschäftsziele: IT-GRC im Spannungsfeld von Effektivität und angemessener Regelungstiefe Seite | 3 12. Arbeitstreffen – 04./05. Mai 2017 Tools & Co: Automatisierung von IT-GRC - Wie bitte? Anforderungen, Möglichkeiten & Erfahrungsberichte 11. Arbeitstreffen – 10./ 11. November 2016 IT-Konsumerisierung, Cloud Computing und Schatten-IT: Neue Anforde- rungen an das GRC im Zeitalter der Digitalisierung? 10. Arbeitstreffen – 21./22. April 2016 Flexibilität vs. Kontrolle: Erfahrungen und Best Practices aus den aktuellen Anforderungen an die IT-Compliance 9. Arbeitstreffen – 26./ 27. November 2015 SIEM – Schluss mit dem Unwissen über die Gefahr? 8. Arbeitstreffen – 5./6. Mai 2015 Management und Controlling von IT-Risiken 7. -

Insurance Brokers Insurance Top Top Best’S Review Landscape As Best’S of Jardine Lloyd Thompson Group Plc in Septemberthompson Group Lloyd Jardine of April 2019

July 2019 www.bestreview.com AM Best’s Monthly Insurance Magazine LEADERSTHE Top Global Ranking Global Broker Insurance Brokers Hub jumps three spots to Top 20 Global Brokers No. 5 and Epic Insurance Ranked by 2018 Total Revenue Brokers & Consultants 2018 2017 2018 Total debuts in the top 20. Ranking Ranking Broker Revenue 1 1 Marsh & McLennan Cos. $14.95 billion by Jeff Roberts 2 2 Aon Plc. $10.77 billion ergers and consolidation. 3 3 Willis Towers Watson $8.61 billion Consolidation and mergers. 4 4 Arthur J. Gallagher & Co. $6.93 billion M The white-hot mergers 5 8 Hub International Ltd. $2.15 billion and acquisitions market continued 6 5 BB&T Insurance Holdings Inc. $2.03 billion unabated in a record-breaking 2018. 7 6 Brown & Brown Inc. $2.01 billion An unprecedented 631 transactions 8 7 Jardine Lloyd Thompson Group plc $1.94 billion in the United States and Canada were 9 10 Lockton Inc. $1.72 billion tracked last year, according to Optis Partners, a Chicago-based financial 10 9 USI Insurance Services $1.68 billion consulting firm specializing in the 11 13 Acrisure LLC $1.40 billion insurance industry. 12 11 Alliant Insurance Services Inc. $1.35 billion MarshBerry, a consulting and advisory 13 12 NFP Corp. $1.25 billion firm for the insurance distribution space, 14 15 AssuredPartners Inc. $1.23 billion counted 580 announced U.S. brokerage 15 14 AmWINS Group Inc. $1.09 billion transactions in 2018, a 4% increase from a then-record 557 in 2017. 16 16 CBIZ Inc.