Audit Report on the Accounts of Local Governments District Bannu Audit

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BANNU EDUCATION FACILITIES - KPK Lebgend College

70°30'0"E 70°40'0"E 70°50'0"E BANNU EDUCATION FACILITIES - KPK LeBgend College ! !> !> !> Town Ship, Bannu !> High School !>!> !>!> !> UNIVERSITY OF !> !B SCIENCE AND !> !> FR BANNU !>!>!> !> TECHNOLOGY, BANNU !> Higher Secondary !>!>!> !> !> !> !> !!> N. WAZIRASTAN !>!> !> ! !>!> !> KGN G G P S K O T K A U M A R !>!> !>!> !> ! B ! R !> ! !> d Masjid School S H A H (C H A S H M I) !>!> !>!> !> !> !> !> !> at Rd BB DISTRICT oTh !> Nizam KARAK K JAIL !> !> !>!> !> U !> !> Middle School !> !> !> !> T !> Baza!>r!> !> !> A ! ! Boza N !> !> D !> !>!> A Sa A Khel !> d !> !> G !> !>!>!> !> Model Primary School !> !> R G G P S K O TK A G U L !> !> r L !>!> !> aw !> A !> !> a !> A !> !> !> !>!> B !> R A U F K H A N P IR B A n !> !> GPS Z!>INDI K H E L D O M E L Sheri !> !> Primary School GGPS L !> !> GG!>PS R A KILLA !> !!> d SITTI !> !> G !> GPS LANDI L!>AN!DI !> Kula KILLA N !> !!> GMS DABAK KILLA KILLA !> !> !> !> A !>!> !>!!>!> ! GGPS ABADI GGPS ARAL GMPS !> !> !> !> T Technical Institute T SYED KHEL K GGPS WANDA HATI KHEL ! !!> !>!> GUL AHMED ! GPS ZARI !> SYED!> REHMAN U !>!> !> !> !>!> !> !> R GHAFAR !> !> !> !>!> ! !> !B !> !> R KAS KALA!> d GUL FAQEER GPS SHER !> KHUJARI !> !> !> !> R A !> !> !>!>!> !> GPS B GPS KURRM !> I !> !> !> !> R !> !> !> !> !> !> !> A !> !> !> V M !> !> !> !> al ALI BEZEN!B !> !!> !> University R E !> !> !> !> !> h !> JAM!>EER BIZEN KHEL U GARHI !> R GPS SOH!>BAT !> !> !>!>!> A M!> !>!> !> !>!>!>T !> !> !> !> KHEL !> H N !> !> !>a !> !> !>!> - !> !>!>!> !> !> S L !> m KHAN S!>U!>R!>ANI u !>!> !>!> !> !!> !> !> -

Office of Chief Engineer (Centre) Communication

OFFICE OF CHIEF ENGINEER (CENTRE) COMMUNICATION & WORKS DEPARTMENT KHYBER PAKHTUNKHWA PESHAWAR 1-Police Road Peshawar Email address [email protected] 091-9211225 FAX 091-9223437 No.CEC/GST/ 7-4 / 1 0 0 Dated / / 2020 To The Executive Engineer, C&W Division Bannu. Subject: AOM&R / SPECIAL REPAIR OF C&W ROADS FOR THE YEAR 2019-20 IN DISTRICT BANNU. SH: PACKAGE-II. 1. KHAN AZAD MUGHAL KHEL ROAD NEAR PS GHORIWALA BANNU. 2. MAIN BANNU KAKKI ROAD. 3. MAIN KHUJARI ROAD TO PIR KHEL VIA HAKIM ZABA KHEL. 4. MAIN MUSA KHEL ROAD TO BAIDALI KILLA (NEK NAWAZ AND JAHANZEB KHAN). 5. MANDORI ABDULLAH SHAH ROAD FROM D.I.KHAN ROAD AZIM GUL MAMA HOUSE. 6. REMAINING PORTION OF QALANDAR KHEL ROAD NEAR PS MIRA KHEL. 7. CONSTRUCTION OF GHANI BAIST KHEL LINK ROAD FROM MITHA KHEL ROAD UPTO MUHAMMAD RIAZ QABRISTAN. 8. REPAIR & REH: OF MAIN SHAHBAZ AZMAT KHEL ROAD NEAR GHANDALI. 9. REPAIR OF ROAD FROM HIGHWAY LINK ROAD TO WALIGAI ROAD. Reference: S.E. C&W Circle Bannu letter No. 1527/4-G(A) dated 15-06-2020. As recommended by Procurement Committee, the discounted bid amounting Rs. 36,535,500/- (Rupees Thirty Six Million, Five Hundred Thirty Five Thousand & Five Hundred Only) based on the lowest rate viz 03% Below (Three percent Below on BOQ Cost based on MRS-2019) offered by M/S Mushtaq & Co, Government Contractor for the subject cited work is hereby approved on the basis of documents submitted by you and forwarded through Superintending Engineer C&W Circle Bannu, subject to the following conditions:- 1. -

Bannu DRC Rapid Needs Assessment II November 2014

Rapid Needs Assessment II Summary of Findings - November 2014 Displaced Populations of North Waziristan Agency in District Bannu Union Councils: Koti Sadat, Fatma Khel, Bazar Ahmad Khan, Ghoriwala, Amandi, Kausar Fateh Khel, Bharat, Nar Jaffer & Khaujari Monitoring & Evaluation Unit, Danish Refugee Council, Pakistan 0 | 14 For further details please contact: [email protected] ; [email protected] DRC| DANISH REFUGEE COUNCIL Acronyms CoRe Community Restoration cluster DRC Danish Refugee Council FATA Federally Administered Tribal Areas FDMA FATA Disaster Management Authority GoP Government of Pakistan IVAP IDP Vulnerability Assessment & Profiling KII Key Informant Interviews KP Khyber Pakhtunkhwa MIRA Multi-sector Initial Rapid Assessment NADRA National Database & Registration Authority NWA North Waziristan Agency PDMA Provincial Disaster Management Authority PKR Pakistan Rupee RRS Return and Rehabilitation Strategy TDPs Temporarily Dislocated Persons UC Union Council UNHCR United Nations High Commissioner for Refugees UNICEF United Nations International Children's Emergency Fund UNOCHA United Nations Office for the Coordination of Humanitarian Affairs Monitoring & Evaluation Unit, Danish Refugee Council, Pakistan 1|14 For further details please contact: [email protected] ; [email protected] DRC| DANISH REFUGEE COUNCIL Introduction The present report provides a snapshot of some of the most pressing needs as of the 24th of November 2014 among the Temporarily Dislocated Persons1 (TDPs) from North Waziristan Agency (NWA) in nine union councils (UCs) of District Bannu: Koti Sadat, Fatma Khel, Bazar Ahmad Khan, Ghoriwala, Amandi, Kausar Fateh Khel, Bharat, Nar Jaffar & Khaujari. This report is based on the second2 Bannu rapid needs assessment conducted by Danish Refugee Council (DRC) in late November 2014, which focused specifically on needs within winterization, shelter and livelihoods – both in place of displacement and origin. -

Usg Humanitarian Assistance to Pakistan in Areas

USG HUMANITARIAN ASSISTANCE TO CONFLICT-AFFECTED POPULATIONS IN PAKISTAN IN FY 2009 AND TO DATE IN FY 2010 Faizabad KEY TAJIKISTAN USAID/OFDA USAID/Pakistan USDA USAID/FFP State/PRM DoD Amu darya AAgriculture and Food Security S Livelihood Recovery PAKISTAN Assistance to Conflict-Affected y Local Food Purchase Populations ELogistics Economic Recovery ChitralChitral Kunar Nutrition Cand Market Systems F Protection r Education G ve Gilgit V ri l Risk Reduction a r Emergency Relief Supplies it a h Shelter and Settlements C e Food For Progress I Title II Food Assistance Shunji gol DHealth Gilgit Humanitarian Coordination JWater, Sanitation, and Hygiene B and Information Management 12/04/09 Indus FAFA N A NWFPNWFP Chilas NWFP AND FATA SEE INSET UpperUpper DirDir SwatSwat U.N. Agencies, E KohistanKohistan Mahmud-e B y Da Raqi NGOs AGCJI F Asadabad Charikar WFP Saidu KUNARKUNAR LowerLower ShanglaShangla BatagramBatagram GoP, NGOs, BajaurBajaur AgencyAgency DirDir Mingora l y VIJaKunar tro Con ImplementingMehtarlam Partners of ne CS A MalakandMalakand PaPa Li Î! MohmandMohmand Kabul Daggar MansehraMansehra UNHCR, ICRC Jalalabad AgencyAgency BunerBuner Ghalanai MardanMardan INDIA GoP e Cha Muzaffarabad Tithwal rsa Mardan dd GoP a a PeshawarPeshawar SwabiSwabi AbbottabadAbbottabad y enc Peshawar Ag Jamrud NowsheraNowshera HaripurHaripur AJKAJK Parachinar ber Khy Attock Punch Sadda OrakzaiOrakzai TribalTribal AreaArea Î! Adj.Adj. PeshawarPeshawar KurrumKurrum AgencyAgency Islamabad Gardez TribalTribal AreaArea AgencyAgency Kohat Adj.Adj. KohatKohat Rawalpindi HanguHangu Kotli AFGHANISTAN KohatKohat ISLAMABADISLAMABAD Thal Mangla reservoir TribalTribal AreaArea AdjacentAdjacent KarakKarak FATAFATA BannuBannu us Bannu Ind " WFP Humanitarian Hub NorthNorth WWaziristanaziristan BannuBannu SOURCE: WFP, 11/30/09 Bhimbar AgencyAgency SwatSwat" TribalTribal AreaArea " Adj.Adj. -

BU16D00400-1-No R/Wall & 1-No P/Wall at UC Bharat 875,000

DISTRICT Project Description BE 2018-19 Final Budget Releases Expenditure BANNU BU16D00400-1-No R/Wall & 1-No P/Wall at UC Bharat 875,000 875,000 875,000 875,000 BANNU BU16D00401-Const. of R/Wall & P/Band at UC Kakki-I 875,000 875,000 875,000 875,000 BANNU BU16D00402-Const. of R/Wall & P/Band at UC ShamshiKhel 134,000 134,000 134,000 134,000 BANNU BU16D00403-Const. of R/Wall & P/Band at UC Mandew 875,000 875,000 875,000 875,000 BANNU BU16D00404-Const. of R/Wall & P/Band at UC KhanderKhan khel 875,000 875,000 875,000 875,000 BANNU BU16D00405-Const. of R/Wall & P/Band at UC SlemaSikander Khel 875,000 875,000 875,000 875,000 BANNU BU16D00406-Const. of R/Wall & P/Band at UC Nurar 825,000 825,000 825,000 825,000 BANNU BU16D00407-Const. of R/Wall & P/Band at UC ShamshiKhel 184,000 184,000 184,000 184,000 BANNU BU16D00408-Const. of R/Wall & P/Band at UC JhanduKhel 825,000 825,000 825,000 825,000 BANNU BU16D00409-Const. of R/Wall & P/Band/Pond at UCDomel 865,000 865,000 865,000 865,000 BANNU BU16D00410-Const. of R/Wall & P/Band at UC MamaKhel 875,000 875,000 875,000 875,000 BANNU BU16D00411-Const. of R/Wall & P/Band/Pond at UCAsperka Waziran 875,000 875,000 875,000 875,000 BANNU BU16D00412-Const. of R/Wall & P/Band UC ZerakiPirba Khel 595,000 595,000 595,000 595,000 BANNU BU16D00413-Const. -

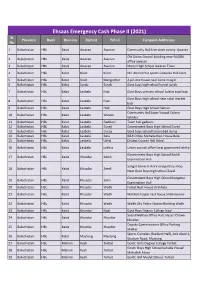

UPDATED CAMPSITES LIST for EECP PHASE-2.Xlsx

Ehsaas Emergency Cash Phase II (2021) Sr. Province Bank Division Distrcit Tehsil Campsite Addresses No. 1 Balochistan HBL Kalat Awaran Awaran Community Hall Live stock colony Awaran Old Union Council building near NADRA 2 Balochistan HBL Kalat Awaran Awaran office awaran 3 Balochistan HBL Kalat Awaran Awaran Model High School Awaran Town 4 Balochistan HBL Kalat Kalat Kalat Mir Ahmed Yar sports Complex Hall kalat 5 Balochistan HBL Kalat Kalat Mangochar A private house near Jame masjid 6 Balochistan HBL Kalat Surab Surab Govt boys high school hostel surab 7 Balochistan HBL Kalat Lasbela Hub Govt Boys primary school Adalat road hub Govt Boys high school near sabzi market 8 Balochistan HBL Kalat Lasbela Hub hub 9 Balochistan HBL Kalat Lasbela Hub Govt Boys High School Sakran Community Hall Jaam Yousuf Colony 10 Balochistan HBL Kalat Lasbela Winder Winder 11 Balochistan HBL Kalat Lasbela Gaddani Town hall gaddani 12 Balochistan HBL Kalat Lasbela Dureji Government Boys High School Dureji 13 Balochistan HBL Kalat Lasbela Dureji Govt boys school hasanabad dureji 14 Balochistan HBL Kalat Lasbela Bela B&R Office Mohalla Rest House Bela 15 Balochistan HBL Kalat Lasbela Uthal District Council Hall Uthal 16 Balochistan HBL Kalat Lasbela Lakhra Union council office local goverment lakhra Government Boys High School Karkh 17 Balochistan HBL Kalat Khuzdar Karkh Examination Hall Sangat General store and poltary shop 18 Balochistan HBL Kalat Khuzdar Zeedi Near Govt Boys high school Zeedi Government Boys High School Norgama 19 Balochistan HBL Kalat Khuzdar Zehri Examination Hall 20 Balochistan HBL Kalat Khuzdar Wadh Forest Rest House Drakhala 21 Balochistan HBL Kalat Khuzdar Wadh Mohbat Faqeer rest house Shahnoorani 22 Balochistan HBL Kalat Khuzdar Wadh Wadh City Police Station Building Wadh 23 Balochistan HBL Kalat Khuzdar Naal Govt Boys Degree College Naal Social Welfare Office Hall, Hazari Chowk 24 Balochistan HBL Kalat Khuzdar Khuzdar khuzdar. -

1 TRIBE and STATE in WAZIRISTAN 1849-1883 Hugh Beattie Thesis

1 TRIBE AND STATE IN WAZIRISTAN 1849-1883 Hugh Beattie Thesis presented for PhD degree at the University of London School of Oriental and African Studies 1997 ProQuest Number: 10673067 All rights reserved INFORMATION TO ALL USERS The quality of this reproduction is dependent upon the quality of the copy submitted. In the unlikely event that the author did not send a com plete manuscript and there are missing pages, these will be noted. Also, if material had to be removed, a note will indicate the deletion. uest ProQuest 10673067 Published by ProQuest LLC(2017). Copyright of the Dissertation is held by the Author. All rights reserved. This work is protected against unauthorized copying under Title 17, United States C ode Microform Edition © ProQuest LLC. ProQuest LLC. 789 East Eisenhower Parkway P.O. Box 1346 Ann Arbor, Ml 48106- 1346 2 ABSTRACT The thesis begins by describing the socio-political and economic organisation of the tribes of Waziristan in the mid-nineteenth century, as well as aspects of their culture, attention being drawn to their egalitarian ethos and the importance of tarburwali, rivalry between patrilateral parallel cousins. It goes on to examine relations between the tribes and the British authorities in the first thirty years after the annexation of the Punjab. Along the south Waziristan border, Mahsud raiding was increasingly regarded as a problem, and the ways in which the British tried to deal with this are explored; in the 1870s indirect subsidies, and the imposition of ‘tribal responsibility’ are seen to have improved the position, but divisions within the tribe and the tensions created by the Second Anglo- Afghan War led to a tribal army burning Tank in 1879. -

IVAP Analysis Report April 2015

IVAP Analysis Report April 2015 IVAP is proudly funded by ECHO and DFID Background to KP/FATA Complex Emeregency The Federally Administered Tribal Areas (FATA) is a semi-autonomous tribal region in northwestern Pakistan. It borders Afghanistan as well as Pakistan’s Khyber Pakhtunkhwa and Baluchistan provinces. More than 5 million people have been registered with the government and/or UNHCR as an internally displaced person (IDP) at some point since 2008 due to violent clashes in the country’s northwest region made up of FATA and Khyber Pakhtunkhwa (KP) province. The 2014 military operations in North Waziristan and Khyber Agencies aggravated the situation, leading to the displacement of a further 233,000 families (approximately 1.4 million people). According to latest estimates from the UNHCR (2014), there are currently 1.6 million registered IDPs in KP/FATA. The vast majority of IDPs in KP/FATA chose to live in host communities (97%) rather than in camps for cultural reasons, including the privacy of females and difficult living conditions in the camps. The rest, who often have no other option, live in IDP camps (3%) (WFP). OCHA and other sources put the proportion of displaced families living outside of camps at 90% (OCHA, 18 June 2014; NYT, 20 June 2014; Al-Jazeera, 26 June 2014; IDMC, 12 June 2013, p.6). Displacement is difficult in Pakistan, which is ranked 146th on the list of 186 countries covered by the Human Development Index (UNDP, 24 July 2014, p.159). An estimated one fifth of its population are poor across the country, while in the KP/FATA a staggering one third of the population are poor (FDMA/UNDP, 2012, p.5; HDR, 2013, p.18; HPG, May 2013, p.21; UNDP, 27 October 2011). -

Khyber Pakhtunkhwa Reconstruction Program: Mid-Term Performance Evaluation Report

Khyber Pakhtunkhwa Reconstruction Program: Mid-Term Performance Evaluation Report October 20, 2014 This publication was produced at the request of the United States Agency for International Development by Tariq Husain, Aftab Ismail Khan, David Garner, and Ahmed Ali Khattak. It was prepared independently by Management Systems International (MSI) under the Monitoring and Evaluation Program (MEP). ACKNOWLEDGMENTS The authors would like to express their thanks to all those who facilitated the work of the team and enabled it to complete this evaluation. These include, but are not limited to, the following: Jamshed ul Hasan, Peshawar office Director of the Monitoring and Evaluation Program, who participated in evaluation team meetings, provided information and insight on institutional and infrastructure issues, and facilitated secondary data collection; Maqsood Jan, Shehla Said, and Hina Tabassum, who worked diligently under challenging conditions to collect qualitative data for the evaluation through individual interviews and focus group discussions; Officials of the Provincial Reconstruction, Rehabilitation and Settlement Authority (PaRRSA), Government of Khyber Pakhtunkhwa, who shared their valuable time and insights with the evaluation team, provided a wealth of information through discussion and relevant documents and arranged successful field visits in three districts of Malakand Division; Officials of the Elementary and Secondary Education Department, who provided school-level data from the Education Management Information System; -

Union Council Level

Southern K.P. Districts- Union Council Level Sher Kot Urban-4 Chorlaki Usterzai Bahadar Kot 2 Muhammad Zai Urban-3 Urban-1 Nusrat Khel Urban-2 Urban-5 Kech Banda Raisan Togh Bala Urban-6 Khan Bari Darband Ganjiano Shah Pur Kalli Bahadar Kot 1 Billitang Gumbat Sur Gul Naryab Kharmatu Khushal Garh Kahi Kotki Jarma Tora Warai Hangu Togh Serai Darsamand Dhoda Doaba HA N G U Kohat Lachi Rural Mandoori Thall Rural Muhammad Khawja Lachi Urban KO H A T Sudal Thall Urban Karbogha Dallan Gurguri Teri Jatta Ismail Khil Banda Daud Shah Empty Shakardara Urban Shakardara Nari Panos Bahadur Khel Sabir Abad Mittha Khel Karak Karak Rehmat Abad KA R A K Esak Chuntra Latambar Ghundai Mir.k.khel Chukara Dabli Aral Hathi Khel Warana Lalozai Sikandar Dand Shaho Khel Bala Kha Amandi Umar Khan 1 Asperka Wazir Ahmad Abad Chagarmash Kheli Mu Nizam Darma Khel Baloch Amandi Umar Shahbaz Azmat Khel 1 Khan 2 Hinjal Takhat Nasrati Khawaja Karab Kalli Baka Khel Muhammad Khan WazirMad Mandan Shahbaz Azmat Khel 2 Thatti Nasrati Mitta Killa Khel Masti Khel Khel Jhando Khel Jehangiri Mandew Mira Khel B A NN U Mandan Shaamshi Khel Nurar Bharat Zargar Mama Khel Azim Killa Bannu Khojary Bannu Ghoriwala Lewan Dardariz Sharawah Kaki Landidak Nar Jafar Khan Mama Khel. Jani Khel Lalozai Sikandar Khel Bala Kha Mash Masti Khani Dand Shaho Asperka Wazir Tikhtee Khel. Marmandi Azeem. Amandi Umar Khan 1 Ghundi Khan Khel. Chagarmash Kheli Mu Kot Kashmir Nizam Darma Khel Baloch Landiwah Kachi Kamar Muhammad Khan Wazir Shahbaz Azmat Khel 1 Baist Khel Amandi Umar Khan 2 Bakhmal Ahmaed Zai LA K K I Hinjal Dharka Soliman Khel Shahbaz Azmat Khel 2 MA R W A T Khawaja Mad Mandan Jhando Khel Tajazai Baka Khel Mitta Khel Killa Khel Masti Khel Pahar Khel Thal Behram Khel Mira Khel Kharu Khel Pacca Lakki Marwat Bego Khel. -

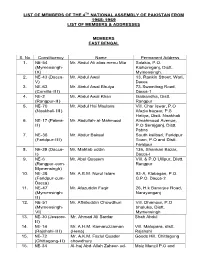

List of Members of the 4Th National Assembly of Pakistan from 1965- 1969 List of Members & Addresses

LIST OF MEMBERS OF THE 4TH NATIONAL ASSEMBLY OF PAKISTAN FROM 1965- 1969 LIST OF MEMBERS & ADDRESSES MEMBERS EAST BENGAL S. No Constituency Name Permanent Address 1. NE-54 Mr. Abdul Ali alias menu Mia Solakia, P.O. (Mymensingh- Kishoreganj, Distt. IX) Mymensingh. 2. NE-43 (Dacca- Mr. Abdul Awal 13, Rankin Street, Wari, V) Dacca 3. NE-63 Mr. Abdul Awal Bhuiya 73-Swamibag Road, (Comilla-III) Dacca-1 4. NE-2 Mr. Abdul Awal Khan Gaibandha, Distt. (Rangpur-II) Rangpur 5. NE-70 Mr. Abdul Hai Maulana Vill. Char Iswar, P.O (Noakhali-III) Afazia bazaar, P.S Hatiya, Distt. Noakhali 6. NE-17 (Pabna- Mr. Abdullah-al-Mahmood Almahmood Avenue, II) P.O Serajganj, Distt. Pabna 7. NE-36 Mr. Abdur Bakaul South kalibari, Faridpur (Faridpur-III) Town, P.O and Distt. Faridpur 8. NE-39 (Dacca- Mr. Mahtab uddin 136, Shankari Bazar, I) Dacca-I 9. NE-6 Mr. Abul Quasem Vill. & P.O Ullipur, Distt. (Rangpur-cum- Rangpur Mymensingh) 10. NE-38 Mr. A.B.M. Nurul Islam 93-A, Klabagan, P.O. (Faridpur-cum- G.P.O. Dacca-2 Dacca) 11. NE-47 Mr. Afazuddin Faqir 26, H.k Banerjee Road, (Mymensingh- Narayanganj II) 12. NE-51 Mr. Aftabuddin Chowdhuri Vill. Dhamsur, P.O (Mymensingh- bhaluka, Distt. VI) Mymensingh 13. NE-30 (Jessore- Mr. Ahmad Ali Sardar Shah Abdul II) 14. NE-14 Mr. A.H.M. Kamaruzzaman Vill. Malopara, distt. (Rajshahi-III) (Hena) Rajshahi 15. NE-72 Mr. A.K.M. Fazlul Quader Goods Hill, Chittagong (Chittagong-II) chowdhury 16. NE-34 Al-haj Abd-Allah Zaheer-ud- Moiz Manzil P.O and (Faridpur-I) Deen (Lal Mian). -

British Intelligence Files on Afghanistan and Its Frontiers, C

Finding Aid British Intelligence Files on Afghanistan and its Frontiers, c. 1888-1946 Published by IDC Publishers, 2003 • Descriptive Summary Creator: India Office Library and Records. Title: British Intelligence Files on Afghanistan and its Frontiers Dates (inclusive): 1888-1946 Dates (bulk): 1906-1941 Abstract: Military and political intelligence on Afghanistan and its frontiers. Languages: Language of materials: English, with a few items in other (also local) languages. Extent: 410 microfiches; 193 files on 37,200 pages. Ordernumber: BIA-1 - BIA-9 • Location of Originals Filmed from the originals held by: British Library, Oriental & India Office Collections (OIOC). • Biography / history note The defence of the North-West Frontier of British India and the status of Afghanistan in the face of real or imagined Russian threats were dominant themes in the political and military strategies of British India for more than a hundred years, beginning with the First Afghan War intervention of 1838-42, when the British frontier had not actually reached Afghanistan. Strategic planning and policy formulation required information – intelligence on the terrain, communications, resources, internal politics, tribal groupings, rivalries, and personalities – to provide both ‘background’ for political relations and practical ‘know-how’ for possible military operations. Before 1922 there was no direct Government of India diplomatic or political representation inside Afghanistan, apart from disastrous attempts to station Residents at Kabul in 1838-42 and 1878-80, while the government in London did not consider Afghanistan to be a nation of a status requiring a diplomatic mission. Between 1882 and 1919, however, a succession of Indian Muslim Agents were posted to Kabul from India, and after the Third Afghan War of 1919-21 full diplomatic relations were finally established.