Audit Report on the Accounts of District Government Bannu

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BANNU EDUCATION FACILITIES - KPK Lebgend College

70°30'0"E 70°40'0"E 70°50'0"E BANNU EDUCATION FACILITIES - KPK LeBgend College ! !> !> !> Town Ship, Bannu !> High School !>!> !>!> !> UNIVERSITY OF !> !B SCIENCE AND !> !> FR BANNU !>!>!> !> TECHNOLOGY, BANNU !> Higher Secondary !>!>!> !> !> !> !> !!> N. WAZIRASTAN !>!> !> ! !>!> !> KGN G G P S K O T K A U M A R !>!> !>!> !> ! B ! R !> ! !> d Masjid School S H A H (C H A S H M I) !>!> !>!> !> !> !> !> !> at Rd BB DISTRICT oTh !> Nizam KARAK K JAIL !> !> !>!> !> U !> !> Middle School !> !> !> !> T !> Baza!>r!> !> !> A ! ! Boza N !> !> D !> !>!> A Sa A Khel !> d !> !> G !> !>!>!> !> Model Primary School !> !> R G G P S K O TK A G U L !> !> r L !>!> !> aw !> A !> !> a !> A !> !> !> !>!> B !> R A U F K H A N P IR B A n !> !> GPS Z!>INDI K H E L D O M E L Sheri !> !> Primary School GGPS L !> !> GG!>PS R A KILLA !> !!> d SITTI !> !> G !> GPS LANDI L!>AN!DI !> Kula KILLA N !> !!> GMS DABAK KILLA KILLA !> !> !> !> A !>!> !>!!>!> ! GGPS ABADI GGPS ARAL GMPS !> !> !> !> T Technical Institute T SYED KHEL K GGPS WANDA HATI KHEL ! !!> !>!> GUL AHMED ! GPS ZARI !> SYED!> REHMAN U !>!> !> !> !>!> !> !> R GHAFAR !> !> !> !>!> ! !> !B !> !> R KAS KALA!> d GUL FAQEER GPS SHER !> KHUJARI !> !> !> !> R A !> !> !>!>!> !> GPS B GPS KURRM !> I !> !> !> !> R !> !> !> !> !> !> !> A !> !> !> V M !> !> !> !> al ALI BEZEN!B !> !!> !> University R E !> !> !> !> !> h !> JAM!>EER BIZEN KHEL U GARHI !> R GPS SOH!>BAT !> !> !>!>!> A M!> !>!> !> !>!>!>T !> !> !> !> KHEL !> H N !> !> !>a !> !> !>!> - !> !>!>!> !> !> S L !> m KHAN S!>U!>R!>ANI u !>!> !>!> !> !!> !> !> -

Audit Report on the Accounts of Local Governments District Bannu Audit

AUDIT REPORT ON THE ACCOUNTS OF LOCAL GOVERNMENTS DISTRICT BANNU AUDIT YEAR 2018-19 AUDITOR GENERAL OF PAKISTAN TABLE OF CONTENTS Abbreviation…………………………………………..…………………..………i Preface ................................................................................................................. ii EXECUTIVE SUMMARY ................................................................................. iii SUMMARY TABLES & CHARTS ................................................................... vii I: Audit Work Statistics ...................................................................................... vii II: Audit observations Classified by Categories .................................................. vii III: Outcome Statistics ...................................................................................... viii IV: Table of Irregularities pointed out ................................................................. ix V: Cost Benefit Ratio .......................................................................................... ix CHAPTER-1 ....................................................................................................... 1 1.1 Local Governments Bannu ............................................................................. 1 1.1.1 Introduction .......................................................................................... 1 1.1.2 Comments on Budget and Accounts (Variance Analysis) .................... 5 1.1.3 Comments on the status of compliance with DAC / TAC Directives ..... 7 1.2 DISTRICT -

BU16D00400-1-No R/Wall & 1-No P/Wall at UC Bharat 875,000

DISTRICT Project Description BE 2018-19 Final Budget Releases Expenditure BANNU BU16D00400-1-No R/Wall & 1-No P/Wall at UC Bharat 875,000 875,000 875,000 875,000 BANNU BU16D00401-Const. of R/Wall & P/Band at UC Kakki-I 875,000 875,000 875,000 875,000 BANNU BU16D00402-Const. of R/Wall & P/Band at UC ShamshiKhel 134,000 134,000 134,000 134,000 BANNU BU16D00403-Const. of R/Wall & P/Band at UC Mandew 875,000 875,000 875,000 875,000 BANNU BU16D00404-Const. of R/Wall & P/Band at UC KhanderKhan khel 875,000 875,000 875,000 875,000 BANNU BU16D00405-Const. of R/Wall & P/Band at UC SlemaSikander Khel 875,000 875,000 875,000 875,000 BANNU BU16D00406-Const. of R/Wall & P/Band at UC Nurar 825,000 825,000 825,000 825,000 BANNU BU16D00407-Const. of R/Wall & P/Band at UC ShamshiKhel 184,000 184,000 184,000 184,000 BANNU BU16D00408-Const. of R/Wall & P/Band at UC JhanduKhel 825,000 825,000 825,000 825,000 BANNU BU16D00409-Const. of R/Wall & P/Band/Pond at UCDomel 865,000 865,000 865,000 865,000 BANNU BU16D00410-Const. of R/Wall & P/Band at UC MamaKhel 875,000 875,000 875,000 875,000 BANNU BU16D00411-Const. of R/Wall & P/Band/Pond at UCAsperka Waziran 875,000 875,000 875,000 875,000 BANNU BU16D00412-Const. of R/Wall & P/Band UC ZerakiPirba Khel 595,000 595,000 595,000 595,000 BANNU BU16D00413-Const. -

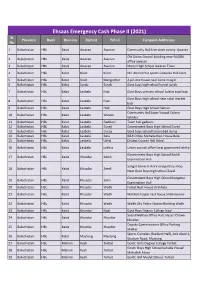

UPDATED CAMPSITES LIST for EECP PHASE-2.Xlsx

Ehsaas Emergency Cash Phase II (2021) Sr. Province Bank Division Distrcit Tehsil Campsite Addresses No. 1 Balochistan HBL Kalat Awaran Awaran Community Hall Live stock colony Awaran Old Union Council building near NADRA 2 Balochistan HBL Kalat Awaran Awaran office awaran 3 Balochistan HBL Kalat Awaran Awaran Model High School Awaran Town 4 Balochistan HBL Kalat Kalat Kalat Mir Ahmed Yar sports Complex Hall kalat 5 Balochistan HBL Kalat Kalat Mangochar A private house near Jame masjid 6 Balochistan HBL Kalat Surab Surab Govt boys high school hostel surab 7 Balochistan HBL Kalat Lasbela Hub Govt Boys primary school Adalat road hub Govt Boys high school near sabzi market 8 Balochistan HBL Kalat Lasbela Hub hub 9 Balochistan HBL Kalat Lasbela Hub Govt Boys High School Sakran Community Hall Jaam Yousuf Colony 10 Balochistan HBL Kalat Lasbela Winder Winder 11 Balochistan HBL Kalat Lasbela Gaddani Town hall gaddani 12 Balochistan HBL Kalat Lasbela Dureji Government Boys High School Dureji 13 Balochistan HBL Kalat Lasbela Dureji Govt boys school hasanabad dureji 14 Balochistan HBL Kalat Lasbela Bela B&R Office Mohalla Rest House Bela 15 Balochistan HBL Kalat Lasbela Uthal District Council Hall Uthal 16 Balochistan HBL Kalat Lasbela Lakhra Union council office local goverment lakhra Government Boys High School Karkh 17 Balochistan HBL Kalat Khuzdar Karkh Examination Hall Sangat General store and poltary shop 18 Balochistan HBL Kalat Khuzdar Zeedi Near Govt Boys high school Zeedi Government Boys High School Norgama 19 Balochistan HBL Kalat Khuzdar Zehri Examination Hall 20 Balochistan HBL Kalat Khuzdar Wadh Forest Rest House Drakhala 21 Balochistan HBL Kalat Khuzdar Wadh Mohbat Faqeer rest house Shahnoorani 22 Balochistan HBL Kalat Khuzdar Wadh Wadh City Police Station Building Wadh 23 Balochistan HBL Kalat Khuzdar Naal Govt Boys Degree College Naal Social Welfare Office Hall, Hazari Chowk 24 Balochistan HBL Kalat Khuzdar Khuzdar khuzdar. -

Union Council Level

Southern K.P. Districts- Union Council Level Sher Kot Urban-4 Chorlaki Usterzai Bahadar Kot 2 Muhammad Zai Urban-3 Urban-1 Nusrat Khel Urban-2 Urban-5 Kech Banda Raisan Togh Bala Urban-6 Khan Bari Darband Ganjiano Shah Pur Kalli Bahadar Kot 1 Billitang Gumbat Sur Gul Naryab Kharmatu Khushal Garh Kahi Kotki Jarma Tora Warai Hangu Togh Serai Darsamand Dhoda Doaba HA N G U Kohat Lachi Rural Mandoori Thall Rural Muhammad Khawja Lachi Urban KO H A T Sudal Thall Urban Karbogha Dallan Gurguri Teri Jatta Ismail Khil Banda Daud Shah Empty Shakardara Urban Shakardara Nari Panos Bahadur Khel Sabir Abad Mittha Khel Karak Karak Rehmat Abad KA R A K Esak Chuntra Latambar Ghundai Mir.k.khel Chukara Dabli Aral Hathi Khel Warana Lalozai Sikandar Dand Shaho Khel Bala Kha Amandi Umar Khan 1 Asperka Wazir Ahmad Abad Chagarmash Kheli Mu Nizam Darma Khel Baloch Amandi Umar Shahbaz Azmat Khel 1 Khan 2 Hinjal Takhat Nasrati Khawaja Karab Kalli Baka Khel Muhammad Khan WazirMad Mandan Shahbaz Azmat Khel 2 Thatti Nasrati Mitta Killa Khel Masti Khel Khel Jhando Khel Jehangiri Mandew Mira Khel B A NN U Mandan Shaamshi Khel Nurar Bharat Zargar Mama Khel Azim Killa Bannu Khojary Bannu Ghoriwala Lewan Dardariz Sharawah Kaki Landidak Nar Jafar Khan Mama Khel. Jani Khel Lalozai Sikandar Khel Bala Kha Mash Masti Khani Dand Shaho Asperka Wazir Tikhtee Khel. Marmandi Azeem. Amandi Umar Khan 1 Ghundi Khan Khel. Chagarmash Kheli Mu Kot Kashmir Nizam Darma Khel Baloch Landiwah Kachi Kamar Muhammad Khan Wazir Shahbaz Azmat Khel 1 Baist Khel Amandi Umar Khan 2 Bakhmal Ahmaed Zai LA K K I Hinjal Dharka Soliman Khel Shahbaz Azmat Khel 2 MA R W A T Khawaja Mad Mandan Jhando Khel Tajazai Baka Khel Mitta Khel Killa Khel Masti Khel Pahar Khel Thal Behram Khel Mira Khel Kharu Khel Pacca Lakki Marwat Bego Khel. -

1 Annexure - D Names of Village / Neighbourhood Councils Alongwith Seats Detail of Khyber Pakhtunkhwa

1 Annexure - D Names of Village / Neighbourhood Councils alongwith seats detail of Khyber Pakhtunkhwa No. of General Seats in No. of Seats in VC/NC (Categories) Names of S. Names of Tehsil Councils No falling in each Neighbourhood Village N/Hood Total Col Peasants/Work S. No. Village Councils (VC) S. No. Women Youth Minority . district Council Councils (NC) Councils Councils 7+8 ers 1 2 3 4 5 6 7 8 9 10 11 12 13 Abbottabad District Council 1 1 Dalola-I 1 Malik Pura Urban-I 7 7 14 4 2 2 2 2 Dalola-II 2 Malik Pura Urban-II 7 7 14 4 2 2 2 3 Dabban-I 3 Malik Pura Urban-III 5 8 13 4 2 2 2 4 Dabban-II 4 Central Urban-I 7 7 14 4 2 2 2 5 Boi-I 5 Central Urban-II 7 7 14 4 2 2 2 6 Boi-II 6 Central Urban-III 7 7 14 4 2 2 2 7 Sambli Dheri 7 Khola Kehal 7 7 14 4 2 2 2 8 Bandi Pahar 8 Upper Kehal 5 7 12 4 2 2 2 9 Upper Kukmang 9 Kehal 5 8 13 4 2 2 2 10 Central Kukmang 10 Nawa Sher Urban 5 10 15 4 2 2 2 11 Kukmang 11 Nawansher Dhodial 6 10 16 4 2 2 2 12 Pattan Khurd 5 5 2 1 1 1 13 Nambal-I 5 5 2 1 1 1 14 Nambal-II 6 6 2 1 1 1 Abbottabad 15 Majuhan-I 7 7 2 1 1 1 16 Majuhan-II 6 6 2 1 1 1 17 Pattan Kalan-I 5 5 2 1 1 1 18 Pattan Kalan-II 6 6 2 1 1 1 19 Pattan Kalan-III 6 6 2 1 1 1 20 Sialkot 6 6 2 1 1 1 21 Bandi Chamiali 6 6 2 1 1 1 22 Bakot-I 7 7 2 1 1 1 23 Bakot-II 6 6 2 1 1 1 24 Bakot-III 6 6 2 1 1 1 25 Moolia-I 6 6 2 1 1 1 26 Moolia-II 6 6 2 1 1 1 1 Abbottabad No. -

PRCS (NHQ) Sit-Rep (4) (Idps Response Operations) Dated. 3Rd July, 2014

PRCS (NHQ) Sit-Rep (4) (IDPs Response Operations) Dated. 3rd July, 2014 Background-Situation 1. As a result of the recently announced full fledge military operation in North Waziristan Agency of Federally Administered Tribal Area (FATA), a large number of families have been displaced to the settled districts of KP. District Bannu being the neighboring settled district with NWA, has received majority of the influx. The Government has imposed curfew on North Waziristan – Bannu road, as such, no new registrations have taken place since 24 June. So the accumulated figure remains same as 24th June 2014. The number of people displaced from North Waziristan Agency (NWA) 38,296 Families (470,336 Ind) , with more than 74 per cent of them women and children (males: 123,290, females: 148,244 and children 198,802). Out of these displaced population only 45 families decided to stay in Bakka khel Camp. Most of them proceeded towards District Bannu while some of them moved towards Karak, Lakki Marwat, Kohat, Fateh Jhang, Jhand, Tala Gang, Peshawar and Rawalpindi.. (Source: FDMA). 2. The information compiled up to date by UNOCHA, shows that around 70% of the families in displacement are carrying their animals (poultry, small and large ruminants) with them. Some of the families have managed to transport them in vehicles, but others have done it by foot, due to the high prices asked by transporters. This has led to the death of some animals during the displacement. 3. PRCS Continued Response to the Situation of IDPs Health care and ambulance services; As of 02nd of July, total 4,755 IDPs patients were given basic treatment at PRCS free medical camp. -

Abbreviations and Acronyms

PART III] THE GAZETTE OF PAKISTAN, EXTRA., JANUARY 14, 2019 21(1) ISLAMABAD, MONDAY, JANUARY 14, 2019 PART III Other Notifications, Orders, etc. ELECTION COMMISSION OF PAKISTAN NOTIFICATION Islamabad, the 9th January, 2019 SUBJECT:—NOTIFICATION OF THE RETURNED CANDIDATES IN RESPECT OF LOCAL GOVERNMENT 8TH BYE- ELECTIONS IN KP PROVINCE No. F. 27(1)/2018-LGE-KPK(Vol-I).—In exercise of powers conferred upon it under Article 140A of the Constitution of the Islamic Republic of Pakistan, Section-86 of Khyber Pakhtunkhwa Local Government Act 2013, read with Rule-41 (4) of the Khyber Pakhtunkhwa Local Councils (Conduct of Elections) Rules, 2014, and all other Powers enabling it in that behalf, the Election Commission of Pakistan is pleased to notify hereunder, for information of general public, the names of returned candidates against the vacant seats in various Local Councils of KP Province elected in the Local Government 8th Bye-Election held on 23rd December, 2018 in Khyber Pakhtunkhwa Province:— 21(1-15) Price: Rs. 20.00 [42(2019)/Ex. Gaz.] 21(2) THE GAZETTE OF PAKISTAN, EXTRA., JANUARY 14, 2019 [PART III Name of Father/Husband Category of S.No Returned Address Name Seat Candidate DISTRICT PESHAWAR Ward Sikandar Town (Town Council-I) Faqeer 1 Afzal Khan General Gulbahar No.03, Peshawar Muhammad Ward Asia (Town Council-I) Garhi Mir Ahmad Shah, Ramdas, 2 Shah Zeb Muhammad Hanif General Peshawar Ward Yakatoot-I (Town Council-I) Shehbaz Town, Wazir Bagh 3 Bakhtiar Ahmad Sahibzada General Road, Peshawar Ward Akhoonabad (Town Council-I) Haider -

KPK PRISONS DEPARTMENT (KPK-PDHQ) (219)Result for The

KPK PRISONS DEPARTMENT (KPK-PDHQ) (219)Result for the post of Male Warder (BPS - 05) Zone 4 PAKISTAN TESTING SERVICE MERIT LIST MALE (ZONE-4) 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 Higher Total Obtained Marks of Higher Matric Experience Interview Grand Sr # Name Father Name Contact # District Address DOB Height Chest Runnning Matric Division Qualification Screening Screening Column Qualification Marks Marks Marks Total Marks Marks Marks 13+14+17 1 Kamran Ali Shah Ahmad Ali Shah 03339742753 Bannu Shaikhan Essaki, Shaikhan District Bannu August 23, 1991 5x10.5 36-37.5 Pass 1st Division Masters and Above 70 12 100 66 148 4 152 2 Muneeb Iqbal Khan Muhammad Iqbal Khan 03359768978 Bannu Zalim Mandan P.O Bada Mir Abas Mandan Bannu Sep 14 1991 5x7.5 35-36.5 Pass 1st Division Masters and Above 70 12 100 64 146 4 150 Vill Sermkhel Dist Lakki Marwat P O And Teh 3 Ali Raza Khadim Raza 03169544622 Lakki Marwat August 9, 1998 6x00 35-36 Pass 1st Division Intermediate/HSSC 70 6 100 69 145 4 149 Sarai Naurang 4 Muhammad Hassan Ibrahim Khan 03409046354 Dera Ismail Khan Mohallah Masti Khel Teh D.I K Mar 20 1995 5x7 34-35 Pass 1st Division Graduation 70 8 100 66 144 4 148 M Qutab Colony Near Nawab Qabar City 1 Tank 5 Muhammad Jamshaid Mir Wali Khan 03459845061 Tank March 27, 1991 5x8 35-37 Pass 1st Division Graduation 70 8 100 65 143 4 147 K.P.K Vill Narazad Naurang P/O Serai Naurang Distt 6 Naveed Ullah Hassan Khan 03315282037 Lakki Marwat Mar 18 1990 5x8 37-39 Pass 1st Division Masters and Above 70 12 100 61 143 4 147 Lakki Marwat 7 Atteef -

Sne (Fresh) Vol-Iv Part-A2 (District)

SCHEDULE OF NEW EXPENDITURE FOR 2017 – 18 CURRENT VOL-IV PART-A/2 (FRESH) (DISTRICT) GOVERNMENT OF KHYBER PAKHTUNKHWA FINANCE DEPARTMENT REFERENCE TO PAGES DEVOLVED ENTITIES S.No DISTRICT NAME PAGE # 1 ABBOTTABAD 1 – 82 2 BANNU 83 – 223 3 BATTAGRAM 224 – 239 4 BUNER 240 – 406 5 CHARSADDA 407 – 521 6 CHITRAL 522 – 590 7 D.I. KHAN 591 – 658 8 DIR LOWER 659 – 830 (i) GENERAL ABSTRACT OF BUDGET ESTIMATES CURRENT EXPENDITURE (PROVINCIAL) SNE FRESH 2017-18 POSTS BUDGET ESTIMATES S.NO. DEPARTMENT 2016-17 2016-17 1 GENERAL ADMINISTRATION 30 10,609,000 2 FINANCE, TREASURIES & LOCAL FUND AUDIT 21 7,674,000 PLANNING & DEVELOPMENT AND BUREAU OF 3 5 3,091,000 STATISTICS 4 INFORMATION TECHNOLOGY 13 5,623,000 5 REVENUE & ESTATE 4 1,134,000 6 EXCISE AND TAXATION 46 11,990,000 7 HOME 43 13,588,000 8 JAILS & CONVICTS SETTLEMENT 49 16,693,000 9 POLICE 2,222 1,436,808,000 10 ADMINISTRATION OF JUSTICE 58 34,035,000 11 HIGHER EDUCATION, ARCHIVES & LIBRARIES 616 243,504,000 12 HEALTH 674 235,213,000 13 COMMUNICATION & WORKS 1 977,000 14 PUBLIC HEALTH ENGINEERING 53 9,699,000 15 AGRICULTURE 21 7,660,000 16 ANIMAL HUSBANDRY 19 13,700,000 17 ENVIRONMENT AND FORESTRY 39 14,704,000 18 FORESTRY (WILDLIFE) 75 25,661,000 19 FISHERIES 37 11,672,000 20 IRRIGATION 51 14,646,200 21 POPULATION WELFARE 61 31,540,000 22 LABOUR 32 9,788,000 23 ZAKAT & USHER 7 7,746,000 24 SPORTS, CULTURE, TOURISM & MUSEUMS 71 20,388,000 25 HOUSING 10 2,867,000 26 ENERGY & POWER 47 18,380,000 27 TRANSPORT & MASS TRANSIT 40 10,408,000 28 ELEMENTARY AND SECONDARY EDUCATION 10 5,010,000 29 RELIEF -

Addresses of DPW Offices, RHSC-As, Msus, Fwcs & Counters in Khyber

Addresses of Service Delivery Network Including Newly Merged Districts (DPW Offices, RHSC-As, MSUs, FWCs & Counters) (Technical Section) Directorate of Population Welfare Department Government of Khyber Pakhtunkhwa (August, 2019) Plot No 18, Sector E-8, Street No 05, Phase 7, Hayatabad. Phone: 091-9219052, Fax: 091-9219066 1 Content S.No Contents Page No 1. Updated Addresses of District Population Welfare Offices in 3 Khyber Pakhtunkhwa 2. Updated Addresses of Reproductive Health Services Outlets 4 (RHSC-As) in Khyber Pakhtunkhwa 3. Updated Addresses of Mobile Service Units in Khyber 5 Pakhtunkhwa 4. Updated Addresses of Family Welfare Centers in Khyber 7 Pakhtunkhwa 5. Updated Addresses of Counters in Khyber Pakhtunkhwa 28 6. Updated Addresses of District Population Welfare Offices in 29 Merged Districts (Erstwhile FATA) 7. Updated Addresses of Reproductive Health Services Outlets 30 (RHSC-As) in Merged Districts (Erstwhile FATA) 8. Updated Addresses of Mobile Service Units in Merged Districts 31 (Erstwhile FATA) 9. Updated Addresses of Family Welfare Centers in Merged Districts 32 (Erstwhile FATA) 2 Updated Addresses of District Population Welfare Offices in Khyber Pakhtunkhwa S.No Name of DPW Office Complete Address Abbottabad Wajid Iqbal House Azam Town Thanda Chowa PMA Road 1 KakulAbbottabad Phone and fax No.0992-401897 2 Bannu Banglow No.21, Defence Officers Colony Bannu Cantt:. (Ph: No.0928-9270330) 3 Buner Mohallah Tawheed Abad Sawari Buner 4 Battagram Opposite Sub-Jail, Near Lahore Scholars Schools System, Tehsil and District Battagram 5 Chitral Village Goldor, P.O Chitral, Teh& District Lower Chitral 6 Charsadda Opposite Excise & Taxation Office Nowshera Road Charsadda 7 D.I Khan Zakori Town, Draban Road, DIKhan 8 Dir Lower Main GT Road Malik Plaza Khungi Paeen Phone. -

Rapid Needs Assessment

Rapid Needs Assessment Summary of Findings September 2014 Displaced populations of North Waziristan Agency in District Bannu (Six Union Councils - Amandi, Bazar Ahmad Khan, Fatma khel, Ghoriwala, Kausar Fateh Khel, and Koti Sadat) September 2014 Displaced populations of North Waziristan Agency in District Bannu (Six Union Councils - Amandi, Bazar Ahmad Khan, Fatma khel, Ghoriwala, Kausar Fateh Khel, and Koti Sadat) September, 2014 Railway Road 10-CII, University Town, Peshawar Tel: 92 (0) 91 570 1896, [email protected] N e e d s A s s e s s m e n t R e p o r t , Displaced Populations of North Waziristan Agency (September, 2014) Introduction This report provides a snapshot of the current situation (as of 9th of September 2014) of displaced persons from North Waziristan Agency (NWA) in six Union Councils (UCs) in District Bannu (Fatmakhel, Ghoriwala, Amandi, Kausar Fateh Khel Bazar Ahmad Khan and Koti Sadat), primarily within WASH, but also with findings relating to Shelter and NFIs. The rapid assessment is primarily intended to inform the planning of DRC’s emergency response and should be seen as such. Since there is a relative dearth of information to inform the response in Bannu we however choose to make our data freely available so that if necessary they can be used for triangulation purposes by other humanitarian actors in Bannu. Primary data was obtained by DRC assessment teams who interviewed TDPs1 and host community members. Reliable secondary sources such as FATA Disaster Management Authority (FDMA), Provincial Disaster Management Authority (PDMA), Khyber Pakhtunkhwa, United Nations Office for the Coordination of Humanitarian Affairs (UNOCHA), provided additional data to this report.