United Kingdom Minerals Yearbook 2009

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TEACHERS' RETIREMENT SYSTEM of the STATE of ILLINOIS 2815 West Washington Street I P.O

Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Performed as Special Assistant Auditors for the Auditor General, State of Illinois Teachers’ Retirement System of the State of Illinois Compliance Examination For the Year Ended June 30, 2020 Table of Contents Schedule Page(s) System Officials 1 Management Assertion Letter 2 Compliance Report Summary 3 Independent Accountant’s Report on State Compliance, on Internal Control over Compliance, and on Supplementary Information for State Compliance Purposes 4 Independent Auditors’ Report on Internal Control over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance with Government Auditing Standards 8 Schedule of Findings Current Findings – State Compliance 10 Supplementary Information for State Compliance Purposes Fiscal Schedules and Analysis Schedule of Appropriations, Expenditures and Lapsed Balances 1 13 Comparative Schedules of Net Appropriations, Expenditures and Lapsed Balances 2 15 Comparative Schedule of Revenues and Expenses 3 17 Schedule of Administrative Expenses 4 18 Schedule of Changes in Property and Equipment 5 19 Schedule of Investment Portfolio 6 20 Schedule of Investment Manager and Custodian Fees 7 21 Analysis of Operations (Unaudited) Analysis of Operations (Functions and Planning) 30 Progress in Funding the System 34 Analysis of Significant Variations in Revenues and Expenses 36 Analysis of Significant Variations in Administrative Expenses 37 Analysis -

Coal Production

Coal Production A B C D E F G H I J K L M N O P Q R S T U V W X Y Z AA AB AC AD AE AF AG AH AI AJ AK 1 2 Summary of coal production entered on entity worksheets 3 Richard Heede 4 Climate Mitigation Services 5 22-May-13 6 7 8 1850s 1860s 1850 1851 1852 1853 1854 1855 1856 1857 1858 1859 1860 1861 1862 1863 1864 1865 1866 1867 1868 1869 1870 1871 9 Coal 10 11 12 13 1 Alpha Natural Resources, USA 14 15 2 Anglo American, UK 16 17 3 Arch Coal Company, USA 18 19 4 British Coal Corporation, UK 20 21 5 BP Coal, UK 22 23 6 BHP Billiton, Australia 24 25 7 China, Peoples Republic 26 27 8 Coal India, India 28 29 9 ConocoPhillips, USA 30 31 10 Consol Energy, USA 0.03 0.05 0.1 0.1 0.1 0.2 0 0 32 33 11 Cyprus Amax, USA 34 35 12 Czechoslovakia 36 37 13 Czech Republic + Slovakia 38 39 14 ExxonMobil, USA 40 41 15 FSU (Former Soviet Union) 42 43 16 Kazakhstan 44 45 17 Kerr-McGee Coal (Anadarko), USA 46 47 18 Kiewit Mining Group, USA 48 49 19 Luminant, USA 50 51 20 Massey Energy, USA 52 53 21 Murray Coal, USA 54 55 22 North American Coal Corp., USA 56 57 23 North Korea 58 59 24 Occidental, USA 60 61 25 Peabody Energy, USA 62 63 26 Pittsburgh & Midway Coal (Chevron) 64 65 27 Poland 66 67 28 Rio Tinto, Australia 68 69 29 RAG (Ruhrkohle AG), Germany 70 71 30 Russian Federation (not including FSU) 72 73 31 RWE, Germany 74 75 32 Sasol, South Africa 76 77 33 Singareni Collieries Company, India 78 79 34 UK Coal, UK 80 81 35 Ukraine 82 83 36 Westmoreland Coal, USA 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.1 0.2 0.2 0.2 0.2 0.2 0.2 0.2 0.3 0.3 0.4 84 85 37 Xstrata, Switzerland -

Cerrejón Coal Mine Colombia

Cerrejón coal mine Colombia Sectors: Coal Mining Active This profile is actively maintained Send feedback on this profile By: BankTrack Created before Nov 2016 Last update: May 19 2021 Contact: Alex Scrivener, Policy Officer, Global Justice Now Project website Status Planning Design Agreement Construction Operation Closure Decommission Sectors Coal Mining Location Status Planning Design Agreement Construction Operation Closure Decommission Website http://www.cerrejon.com/site/ About Cerrejón coal mine The Cerrejón coal mine in La Guajira, Colombia, is the largest in Latin America and one of the largest in the world. Its steady expansion since its founding in 1976 has led to the destruction of whole villages populated by local indigenous and Afro-Colombian people. The extracted coal is almost exclusively for export to rich countries with local people seeing few benefits. The mine is owned by three giant UK-listed mining companies: BHP Billiton, Anglo American and Glencore. All of which receive billions of pounds in finance from UK banks and pension funds. Roche, Chancleta, Tamaquitos, Manantial, Tabaco, Palmarito, El Descanso, Caracoli, Zarahita, Patilla. These are the names of just some of the communities that have been devastated or simply wiped off the map by the Cerrejón mining project. Latest developments Anglo American to exit from Cerrejon shareholding, BHP Group to follow Feb 25 2021 Glencore leaving, passing mining contracts to Republic of Colombia Feb 4 2021 Impacts Social and human rights impacts While the Cerrejón mining company's promotional material gives the impression that it is helping the displaced communities, the reality is that the mining company has used underhand tactics to buy off individuals and sow internal division within the communities. -

A Last Chance for Coal Making Carbon Capture and Storage a Reality

a last chance for coal making carbon capture and storage a reality foreword by Rt Hon Margaret Beckett MP Jon Gibbins & Hannah Chalmers David Hawkins Graeme Sweeney Jules Kortenhorst Linda McAvan MEP Alain Berger Ruud Lubbers Frances O’Grady Mike Farley Matthew Lockwood Ben Caldecott & Thomas Sweetman Keith Allott Karla Hill & Tim Malloch Sheryl Carter compiled and edited by Chris Littlecott This publication is part of Green Alliance’s climate change theme (www.green-alliance.org.uk/climatechange), which is kindly supported by Shell. Green Alliance’s work on the financing of CCS demonstration projects is kindly supported by BP. The views expressed in this publication remain those of the individual authors alone, and do not necessarily reflect the views of Green Alliance or its sponsors. Acknowledgments Many thanks to all those who have advised and assisted in the preparation of this publication, particularly Rebecca Collyer, Mark Johnston and Jesse Scott. Special thanks are due to Catherine Beswick, Karen Crane, Maureen Murphy, Rebekah Phillips and Faye Scott for their invaluable editorial input. a last chance for coal making carbon capture and storage a reality Edited by Chris Littlecott ISBN 978-1-905869-15-2 © Green Alliance 2008 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, without the prior permission in writing of Green Alliance. Within the UK, exceptions are allowed in respect of any fair dealing for the purposes of private research or study, or criticism or review, as permitted under the Copyright, Design and Patents Act, 1988, or in the case of reprographic reproduction in accordance with the terms of the licenses issued by the Copyright Licensing Agency. -

Accordance with the Generally Accepted Accounting Principles

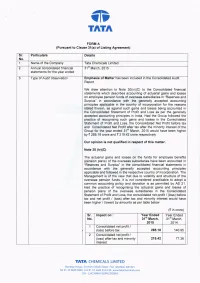

TI'I TNTN FORM A (Pu6uant to Clause 31(a) of Listing Agreement) Sr Particu lars Details No. 1 Name of the Company Tata Chemicals Limited 2. Annual consolidated financial 31 March, 2015 statements for the year ended 3. Type of Audit observation Emphasis of Matter has been included in the Consolidated Audit Report. We draw atlention to Note 3o(ivxc) to the Consolidated financial statements which describes accounting of actuarial gains and losses on employee pension funds of overseas subsidiaries in "Reserves and Surplus" in accordance with the generally accepted accounting principles applicable in the country of incorporation for the reasons stated therein, as against such gains and losses being accounted in the Consolidated Statement of Profit and Loss as per the generally accepted accounting principles in lndia. Had the Group followed the practice of recognising such gains and losses in the Consolidated Statement of Profit and Loss, the Consolidated Net Profit before tax and Consolidated Net Profit after tax after the minority interest of the Group for the year ended 31"r March, 2015 would have been higher by { 285.18 crore and { 219.42 crore respectively. Our opinion is not qualified in respect o, this matter. Note 30 (ivXC) The actuarial gains and losses on the funds for employee benefits (pension plans) of the overseas subsidiaries have been accounted in "ReseNes and Surplus" in the consolidated financial statements in accordance with the generally accepted accounting principles applicable and followed in the respective country of incorporation. The Management is of the view that due to volatility and structure of the overseas pension funds, it is not considered practicable to adopt a common accounting policy and deviation is as permifted by AS 21. -

Draft Energy Bill: Pre–Legislative Scrutiny

House of Commons Energy and Climate Change Committee Draft Energy Bill: Pre–legislative Scrutiny First Report of Session 2012-13 Volume III Additional written evidence Ordered by the House of Commons to be published on 24 May, 12, 19 and 26 June, 3 July, and 10 July 2012 Published on Monday 23 July 2012 by authority of the House of Commons London: The Stationery Office Limited The Energy and Climate Change Committee The Energy and Climate Change Committee is appointed by the House of Commons to examine the expenditure, administration, and policy of the Department of Energy and Climate Change and associated public bodies. Current membership Mr Tim Yeo MP (Conservative, South Suffolk) (Chair) Dan Byles MP (Conservative, North Warwickshire) Barry Gardiner MP (Labour, Brent North) Ian Lavery MP (Labour, Wansbeck) Dr Phillip Lee MP (Conservative, Bracknell) Albert Owen MP (Labour, Ynys Môn) Christopher Pincher MP (Conservative, Tamworth) John Robertson MP (Labour, Glasgow North West) Laura Sandys MP (Conservative, South Thanet) Sir Robert Smith MP (Liberal Democrat, West Aberdeenshire and Kincardine) Dr Alan Whitehead MP (Labour, Southampton Test) The following members were also members of the committee during the parliament: Gemma Doyle MP (Labour/Co-operative, West Dunbartonshire) Tom Greatrex MP (Labour, Rutherglen and Hamilton West) Powers The Committee is one of the departmental select committees, the powers of which are set out in House of Commons Standing Orders, principally in SO No 152. These are available on the Internet via www.parliament.uk. Publication The Reports and evidence of the Committee are published by The Stationery Office by Order of the House. -

Members Directory | World Coal Association

Become a member Search Coal Reducing CO2 emissions Environmental protection Sustainable societies About WCA News & opinion Resources Members area Members Directory The World Coal Association is the global network for the coal industry. Information on all WCA members is available in this B E C O M E A M E M B E R directory. Corporate Member Anglo American Arch Coal Inc Aurizon Banpu BHP Billiton Bowie Resource Partners Caterpillar Global Mining China National Coal Group Glencore Joy Global Karakan Invest LLC Vostsibugol Mitsubishi Development Pty Ltd Orica Ltd Peabody Energy Rio Tinto Energy (MDP) Shenhua Group Corporation Limited Whitehaven Coal Limited Xcoal Energy and Resources Associate Member Andi Assocarboni Associação Brasileira de Carvão Association of British Mining Mineral Equipment Companies (ABMEC) China National Coal Association Coal Association of Canada (CAC) Coal Association of New Zealand Coallmp - Association of Uk Coal Importers Fossil Fuel Foundation German Coal Association (GSVt) Indonesian Coal Mining Association Iranian Mines & Mining Industries (APBI-ICMA) Development & Renovation Organization (IMIDRO) Japan Coal Energy Center (JCOAL) Minerals Council of Australia Mongolian Coal Association National Mining Association (NMA) Queensland Resources Council (QRC) Shaanxi Institute of Geological Survey Svenska Kolinstitutet MOU Coal Utilization Research Council European Association for Coal and VGB Powertech e.V. (CURC) Lignite (EURACOAL) World Coal Association Helpful links Explore Email. [email protected] Reducing CO2 emissions F I N D U S O N Tel. +44 (0) 20 7851 0052 Platform for Accelerating Coal Efficiency Fax. +44 (0) 20 7851 0061 Carbon capture, use and storage Contact us About WCA T H E J O U R N A L O F T H E C O A L I N D U S T R Y Terms & Conditions Media information Cookie policy Unless otherwise specified, images courtesy of Accessibility Shutterstock © 2015 World Coal Association. -

Negativliste. Fossil Energi

Bilag 6. Negativliste. Fossil energi Maj 2017 Læsevejledning til negativlisten: Moderselskab / øverste ejer vises med fed skrift til venstre. Med almindelig tekst, indrykket, er de underliggende selskaber, der udsteder aktier og erhvervsobligationer. Det er de underliggende, udstedende selskaber, der er omfattet af negativlisten. Rækkeetiketter Acergy SA SUBSEA 7 Inc Subsea 7 SA Adani Enterprises Ltd Adani Enterprises Ltd Adani Power Ltd Adani Power Ltd Adaro Energy Tbk PT Adaro Energy Tbk PT Adaro Indonesia PT Alam Tri Abadi PT Advantage Oil & Gas Ltd Advantage Oil & Gas Ltd Africa Oil Corp Africa Oil Corp Alpha Natural Resources Inc Alex Energy Inc Alliance Coal Corp Alpha Appalachia Holdings Inc Alpha Appalachia Services Inc Alpha Natural Resource Inc/Old Alpha Natural Resources Inc Alpha Natural Resources LLC Alpha Natural Resources LLC / Alpha Natural Resources Capital Corp Alpha NR Holding Inc Aracoma Coal Co Inc AT Massey Coal Co Inc Bandmill Coal Corp Bandytown Coal Co Belfry Coal Corp Belle Coal Co Inc Ben Creek Coal Co Big Bear Mining Co Big Laurel Mining Corp Black King Mine Development Co Black Mountain Resources LLC Bluff Spur Coal Corp Boone Energy Co Bull Mountain Mining Corp Central Penn Energy Co Inc Central West Virginia Energy Co Clear Fork Coal Co CoalSolv LLC Cobra Natural Resources LLC Crystal Fuels Co Cumberland Resources Corp Dehue Coal Co Delbarton Mining Co Douglas Pocahontas Coal Corp Duchess Coal Co Duncan Fork Coal Co Eagle Energy Inc/US Elk Run Coal Co Inc Exeter Coal Corp Foglesong Energy Co Foundation Coal -

Carbon Disclosure Project 2011

CDP 2011 Investor CDP 2011 Information Request Carbon Disclosure Project Centrica Module: Introduction Page: Introduction 0.1 Introduction Please give a general description and introduction to your organization About Centrica Our vision is to be the leading integrated energy company in our chosen markets. We source, generate, process, store, trade, save and supply energy and provide a range of related services. We secure and supply gas and electricity for millions of homes and business and offer a range of home energy solutions and low carbon products and services. We have strong brands and distinctive skills which we use to achieve success in our chosen markets of the UK and North America, and for the benefit of our employees, our customers and our shareholders. In the UK, we source, generate, process and trade gas and electricity through our Centrica Energy business division. We store gas through Centrica Storage and we supply products and services to customers through our retail brand British Gas. In North America, Centrica operates under the name Direct Energy, which now accounts for about a quarter of group turnover. We believe that climate change is one of the single biggest global challenges. Energy generation and energy use are significant contributors to man-made greenhouse gas (GHG) emissions, a driver of climate change. As an integrated energy company, we play a pivotal role in helping to tackle climate change by changing how energy is generated and how consumers use energy. Our corporate responsibility (CR) vision is to be the most trusted energy company leading the move to a low carbon future. -

Offshore References

Past, Ongoing and Future Projects OFFSHORE Date Contractor Project Number of Welding Stations (vessel if offshore) Country Pipelines welded Operator 2020 COOEC Lingshui 17-2-SCR 6 Saturnax stations (HYS201) China 404 welds 6.625" (18.3 mm) for CNOOC - 2.93 km of SRC lines - 2.00 km of flowline 2020 TechnipFMC Nam Con Son 2 & SVDN 4 Saturnax stations (G1200) Vietnam Nam Con Son 2: for PetroVietnam (PV GAS) 89 km 26" (1.1 mm) SVDN: 22 km 26" (19.1 mm) 1 km 26" (23.8 mm) 22 km 18" (15.9 mm) 1 km 18" (17.5 mm) Total : 11,053 welds 2020 Sapura Offshore Pegaga Dev. Project 2 Saturnax stations (S3000) Malaysia 324 welds 38" (22.2 mm, X65) - 4 km for Sarawak Shell Berhad 2020 Thien Nam Offshore Services Nam Con Son 2 3 Saturnax stations (Tos Ha Long) Vietnam Total of 2,542 welds: for PetroVietnam 29.7 km 26" (19.1 mm) 0.8 km 26" (23.8 mm) 2020 Sapura Offshore Merakes 4 Saturnax stations (S1200) Indonesia Deepwater lines : for ENI Sepinggan 2,685 welds 18" (26.7 mm, X65) - 32.74 km 2,688 welds 18" (26.7 mm, X65) - 32.78 km Shallow water lines : 1,083 welds 18" (26.7 mm, X65) - 13.22 km 1,074 welds 18" (26.7 mm, X65) - 13.11 km 2020 Sapura Energy ENI Amoca 2 4 Saturnax stations (Sapura 3500) Mexico Total of 3,377 welds: for ENI 10.75" (14.33 mm, X60) 12.75" (20.6 mm, X60) 14" (15.9 mm, X60) Sweet service 2020 GSP Offshore Midia 1 Saturnax stations (Bigfoot 1) Romania 9,970 welds 16" (11.9/12.7/14.3 mm, X52) for Black Sea Oil & Gas 1,463 welds 8.625" (12.7 mm, X52) 2020 Sapura Energy Kirinskoye 1 Saturnax + 2 manual stations (Sapura 1200) Russie -

Negativliste. Fossil Energi

Negativliste. Fossil energi Maj 2021 Udstedende selskab 1 ABJA Investment Co Pte Ltd 2 ABM Investama Tbk PT 3 Aboitiz Equity Ventures Inc 4 Aboitiz Power Corp 5 Abraxas Petroleum Corp 6 Abu Dhabi National Energy Co PJSC 7 AC Energy Finance International Ltd 8 Adams Resources & Energy Inc 9 Adani Electricity Mumbai Ltd 10 Adani Power Ltd 11 Adani Transmission Ltd 12 Adaro Energy Tbk PT 13 Adaro Indonesia PT 14 ADES International Holding PLC 15 Advantage Oil & Gas Ltd 16 Aegis Logistics Ltd 17 Aenza SAA 18 AEP Transmission Co LLC 19 AES Alicura SA 20 AES El Salvador Trust II 21 AES Gener SA 22 AEV International Pte Ltd 23 African Rainbow Minerals Ltd 24 AGL Energy Ltd 25 Agritrade Resources Ltd 26 AI Candelaria Spain SLU 27 Air Water Inc 28 Akastor ASA 29 Aker BP ASA 30 Aker Solutions ASA 31 Aksa Akrilik Kimya Sanayii AS 32 Aksa Enerji Uretim AS 33 Alabama Power Co 34 Alarko Holding AS 35 Albioma SA 36 Alexandria Mineral Oils Co 37 Alfa Energi Investama Tbk PT 38 ALLETE Inc 1 39 Alliance Holdings GP LP 40 Alliance Resource Operating Partners LP / Alliance Resource Finance Corp 41 Alliance Resource Partners LP 42 Alliant Energy Corp 43 Alpha Metallurgical Resources Inc 44 Alpha Natural Resources Inc 45 Alta Mesa Resources Inc 46 AltaGas Ltd 47 Altera Infrastructure LP 48 Altius Minerals Corp 49 Altus Midstream Co 50 Aluminum Corp of China Ltd 51 Ameren Corp 52 American Electric Power Co Inc 53 American Shipping Co ASA 54 American Tanker Inc 55 AmeriGas Partners LP / AmeriGas Finance Corp 56 Amplify Energy Corp 57 Amplify Energy Corp/TX 58 -

Pleistocene and Flandrian Natural Rock Salt Subsidence at Arclid Green, Sandbach, Cheshire Peter Worsley

Pleistocene and Flandrian Natural Rock Salt Subsidence at Arclid Green, Sandbach, Cheshire Peter Worsley Abstract. This applied geological case study concerns the Quaternary geomorphological evolution of a small part of the lowland Cheshire characterised by ‘equifinal subsidence landforms’ resulting from the processes of rock salt dissolution and post Last Glacial Maximum glacial ice meltout. The context relates to environmental issues arising from the quarrying of Chelford Formation industrial ‘silica sands’. Problems related to natural and human induced rock salt dissolution are reviewed. The respective roles of Triassic bedrock halites, collapsed strata, periglacial alluvial sands and multiple glaciation in determining the local stratigraphy and allied landforms are discussed. The morphology and fill of a post glacial subsidence area is examined. It is concluded that natural rock salt dissolution is the principal process influencing the superficial deposits and geomorphology of the study area and that this process has been active over hundreds of thousand years. The deposition and survival of thick silica sands and the glacigenic sediments beneath is probably due to halite dissolution. In eastern Cheshire, a significant part of the lowland A further complicating factor is human induced salt geomorphology is characterised by an excellent subsidence exacerbated by historic shallow mining for example of what, in ‘General Systems Theory’ jargon, salt and wild brine pumping, for example, Ward, would be termed ‘equifinal behaviour’ (Chorley, (1887), Calvert (1915), Cooper (2002), Sherlock 1964), also known as polygenesis. Such behaviour in a (1922), Wallwork (1956, 1960), Waltham (1989), and geomorphological context envisages that different Waltham et al (2005). Following the near universal initial earth surface processes have resulted in similar enforced abandonment of these extraction techniques morphological outcomes.