Organic Agriculture in Albania Sector Study 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Datë 06.03.2021

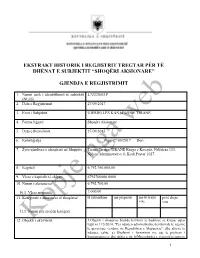

EKSTRAKT HISTORIK I REGJISTRIT TREGTAR PËR TË DHËNAT E SUBJEKTIT “SHOQËRI AKSIONARE” GJENDJA E REGJISTRIMIT 1. Numri unik i identifikimit të subjektit L72320033P (NUIS) 2. Data e Regjistrimit 27/09/2017 3. Emri i Subjektit UJËSJELLËS KANALIZIME TIRANË 4. Forma ligjore Shoqëri Aksionare 5. Data e themelimit 27/09/2017 6. Kohëzgjatja Nga: 27/09/2017 Deri: 7. Zyra qëndrore e shoqërisë në Shqipëri Tirane Tirane TIRANE Rruga e Kavajës, Ndërtesa 133, Njësia Administrative 6, Kodi Postar 1027 8. Kapitali 6.792.760.000,00 9. Vlera e kapitalit të shlyer: 6792760000.0000 10. Numri i aksioneve: 6.792.760,00 10.1 Vlera nominale: 1.000,00 11. Kategoritë e aksioneve të shoqërisë të zakonshme me përparësi me të drejte pa të drejte vote vote 11.1 Numri për secilën kategori 12. Objekti i aktivitetit: 1.Objekti i shoqerise brenda territorit te bashkise se krijuar sipas ligjit nr.l 15/2014, "Per ndarjen administrative-territoriale te njesive te qeverisjes vendore ne Republiken e Shqiperise", dhe akteve te ndarjes, eshte: a) Sherbimi i furnizimit me uje te pijshem i konsumatoreve dhe shitja e tij; b)Mirembajtja e sistemit/sistemeve 1 te furnizimit me ujë te pijshem si dhe të impianteve te pastrimit te tyre; c)Prodhimi dhe/ose blerja e ujit per plotesimin e kerkeses se konsumatoreve; c)Shërbimi i grumbullimit, largimit dhe trajtimit te ujerave te ndotura; d)Mirembajtja e sistemeve te ujerave te ndotura, si dhe të impianteve të pastrimit të tyre. 2.Shoqeria duhet të realizojë çdo lloj operacioni financiar apo tregtar që lidhet direkt apo indirect me objektin e saj, brenda kufijve tè parashikuar nga legjislacioni në fuqi. -

The Contribution of Organic Sector in the Albanian Agriculture

The contribution of organic sector in the Albanian agriculture Elvira Leksinaj 1, Gianni Cicia 2, Luigi Cembalo 2, Teresa Del Giudice 2, Maksim Meço 1, 1 Taulant Nelaj 1Faculty of Economy and Agribusiness, Tirana, Albania, e-mail: [email protected] 2University of Naples “Federico II”, Naples, Italy, e-mail: [email protected] Paper prepared for presentation at the 113 th EAAE Seminar “A resilient European food industry and food chain in a challenging world”, Chania, Crete, Greece, date as in: September 3 - 6, 2009 Copyright 2009 by [Elvira Leksinaj 1, Gianni Cicia 2, Luigi Cembalo 2, Teresa Del Giudice 2, Maksim Meço 1, Taulant Nelaj 1]. All rights reserved. Readers may make verbatim copies of this document for non-commercial purposes by any means, provided that this copyright notice appears on all such copies. 1 The contribution of organic sector in the Albanian agriculture Elvira Leksinaj 1, Gianni Cicia 2, Luigi Cembalo 2, Teresa Del Giudice 2, Maksim Meço 1, 1 Taulant Nelaj 1Faculty of Economy and Agribusiness, Tirana, Albania, e-mail: [email protected] 2University of Naples “Federico II”, Naples, Italy, e-mail: [email protected] Abstract What is nowadays known as organic farming in Albania is at an initial phase. It is mainly located in the so called “marginal areas” by small farms. Organic market in Albania can be considered as at a very starting stage with small niches marketing point but with a growing interest of consumers for fresh productions with limited processing activities. The conditions for a better partaking in the country’s markets is, however, desirable since commercial and trade between Albania and other countries, mainly EU’s, is readily growing. -

Baseline Assessment Report of the Lake Ohrid Region – Albania Annex

TOWARDS STRENGTHENED GOVERNANCE OF THE SHARED TRANSBOUNDARY NATURAL AND CULTURAL HERITAGE OF THE LAKE OHRID REGION Baseline Assessment report of the Lake Ohrid region – Albania (available online at http://whc.unesco.org/en/lake-ohrid-region) Annex XXIII Bibliography on cultural values and heritage, agriculture and tourism aspects of the Lake Ohrid region prepared by Luisa de Marco, Maxim Makartsev and Claudia Spinello on behalf of ICOMOS. January 2016 BIBLIOGRAPHY1 2015 The present bibliography focusses mainly on the cultural values and heritage, agriculture and tourism aspects of the Lake Ohrid region (LOR). It should be read in conjunction to the Baseline Assessment report prepared in a joint collaboration between ICOMOS and IUCN (available online at http://whc.unesco.org/en/lake-ohrid-region) The bibliography includes all the relevant titles from the digital catalogue of the Albanian National Library for the geographic terms connected to LOR. The bibliography includes all the relevant titles from the systematic catalogue since 1989 to date, for the categories 9-908; 91-913 (4/9) (902. Archeology; 903. Prehistory. Prehistoric remains, antiquities. 904. Cultural remains of the historic times. 908. Regional studies. Studies of a place. 91. Geography. The exploration of the land and of specific places. Travels. Regional geography). It also includes the relevant titles found on www.scholar.google.com with summaries if they are provided or if the text is available. Three bibliographies for archaeology and ancient history of Albania were used: Bep Jubani’s (1945-1971); Faik Drini’s (1972-1983); V. Treska’s (1995-2000). A bibliography for the years 1984-1994 (authors: M.Korkuti, Z. -

GTZ-Regional Sustainable Development Tirana 2002

GTZ GmbH German Technical Cooperation, Eschborn Institute of Ecological and Regional Development (IOER), Dresden Towards a Sustainable Development of the Tirana – Durres Region Regional Development Study for the Tirana – Durres Region: Development Concept (Final Draft) Tirana, February 2002 Regional Development Study Tirana – Durres: Development Concept 1 Members of the Arqile Berxholli, Academy of Sci- Stavri Lami, Hydrology Research Working Group ence Center and authors of Vladimir Bezhani, Ministry of Public Perparim Laze, Soil Research In- studies Works stitute Salvator Bushati, Academy of Sci- Fioreta Luli, Real Estate Registra- ence tion Project Kol Cara, Soil Research Institute Irena Lumi, Institute of Statistics Gani Deliu, Tirana Regional Envi- Kujtim Onuzi, Institute of Geology ronmental Agency Arben Pambuku, Civil Geology Ali Dedej, Transport Studies Insti- Center tute Veli Puka, Hydrology Research Llazar Dimo, Institute of Geology Center Ilmi Gjeci, Chairman of Maminas Ilir Rrembeci, Regional Develop- Commune ment Agency Fran Gjini, Mayor of Kamza Mu- Thoma Rusha, Ministry of Eco- nicipality, nomic Cooperation and Trade Farudin Gjondeda, Land and Wa- Skender Sala, Center of Geo- ter Institute graphical Studies Elena Glozheni, Ministry of Public Virgjil Sallabanda, Transport Works Foundation Naim Karaj, Chairman of National Agim Selenica, Hydro- Commune Association Meteorological Institute Koco Katundi, Hydraulic Research Agron Sula , Adviser of the Com- Center mune Association Siasi Kociu, Seismological Institute Mirela Sula, -

The Role of Agriculture in Economic Development in Albania

International Journal of Economics, Commerce and Management United Kingdom ISSN 2348 0386 Vol. IX, Issue 6, June 2021 http://ijecm.co.uk/ THE ROLE OF AGRICULTURE IN ECONOMIC DEVELOPMENT IN ALBANIA Ardian Cerava Faculty of Agriulture, University ‘Fan S. Noli’, Korça, Albania [email protected] Eneida Përmeti Çifligu Faculty of Agriulture, University ‘Fan S. Noli’, Korça, Albania Ilir Sosoli Faculty of Agriulture, University ‘Fan S. Noli’, Korça, Albania Abstract Agriculture plays a major role in the Albanian economy in this article we have tried to analyze and give examples of how important agriculture is and its role in the Albanian economy. It occupies an important place in the gross domestic product and this is clearly shown in the following explanation. Agriculture in Albania as you will see below is a very important part of the Albanian economy. In our country, although agriculture accounts for 18.9% of GDP and a large share of exports, it is mainly limited to small family operations and subsistence agriculture due to lack of modern equipment, unclear property rights, such as and small spread, inefficient land parcels .etc .If the right investment are made in agriculture we will see that the percentage that it contributes in the county economy it will be much higher. Keywords: agriculture, economic development, GDP, Albania Licensed under Creative Common Page 304 International Journal of Economics, Commerce and Management, United Kingdom INTRODUCTION The analysis of the role of agriculture in the development process has always been a matter of priority research in development economics studies, albeit with somewhat different ups and downs and interpretations. -

Strategjia E Zhvillimit Të Qendrueshëm Bashkia Tiranë 2018

STRATEGJIA E ZHVILLIMIT TË QENDRUESHËM TË BASHKISË TIRANË 2018 - 2022 DREJTORIA E PËRGJITSHME E PLANIFIKIMIT STRATEGJIK DHE BURIMEVE NJERËZORE BASHKIA TIRANË Tabela e Përmbajtjes Përmbledhje Ekzekutive............................................................................................................................11 1. QËLLIMI DHE METODOLOGJIA...............................................................................................................12 1.1 QËLLIMI...........................................................................................................................................12 1.2 METODOLOGJIA..............................................................................................................................12 1.3 PARIMET UDHËHEQËSE..................................................................................................................14 2. TIRANA NË KONTEKSTIN KOMBËTAR DHE NDËRKOMBËTAR.................................................................15 2.1 BASHKËRENDIMI ME POLITIKAT DHE PLANET KOMBËTARE...........................................................15 2.2 KONKURUESHMËRIA DHE INDIKATORËT E SAJ...............................................................................13 2.2.1 Burimet njerëzore dhe cilësia e jetës......................................................................................13 2.2.2 Mundësitë tregtare dhe potenciali prodhues.........................................................................14 2.2.3 Transport...............................................................................................................................15 -

Women Entrepreneurs in Albania

SEED Working Paper No. 21 InFocus Programme on Boosting Employment through Small EnterprisE Development Job Creation and Enterprise Department Series on Women’s Entrepreneurship Development and Gender in Enterprises — WEDGE Women Entrepreneurs in Albania by Mimoza Bezhani International Training Centre of the ILO, International Labour Office · Geneva Turin, Italy Copyright © International Labour Organization 2001 First published 2001 Publications of the International Labour Office enjoy copyright under Protocol 2 of the Universal Copyright Convention. Nevertheless, short excerpts from them may be reproduced without authorization, on condition that the source is indicated. For rights of reproduction or translation, application should be made to the Publications Bureau (Rights and Permissions), International Labour Office, CH-1211 Geneva 22, Switzerland. The International Labour Office welcomes such applications. Libraries, institutions and other users registered in the United Kingdom with the Copyright Licensing Agency, 90 Tottenham Court Road, London W1T 4LP [Fax: (+44) (0)20 7631 5500; e-mail: [email protected]], in the United States with the Copyright Clearance Center, 222 Rosewood Drive, Danvers, MA 01923 [Fax: (+1) (978) 750 4470; e-mail: [email protected]] or in other countries with associated Reproduction Rights Organizations, may make photocopies in accordance with the licences issued to them for this purpose. ILO Women Entrepreneurs in Albania Geneva, International Labour Office, 2001 ISBN 92-2-112758-3 Based on original document: Biznesi i Gruas në Shqipëri = L’imprenditorialità femminile in Albania, published by the International Training Centre of the ILO, Turin, 1999 (without ISBN). The designations employed in ILO publications, which are in conformity with United Nations practice, and the presentation of material therein do not imply the expression of any opinion whatsoever on the part of the International Labour Office concerning the legal status of any country, area or territory or of its authorities, or concerning the delimitation of its frontiers. -

Albania: Average Precipitation for December

MA016_A1 Kelmend Margegaj Topojë Shkrel TRO PO JË S Shalë Bujan Bajram Curri Llugaj MA LËSI Lekbibaj Kastrat E MA DH E KU KË S Bytyç Fierzë Golaj Pult Koplik Qendër Fierzë Shosh S HK O D Ë R HAS Krumë Inland Gruemirë Water SHK OD RË S Iballë Body Postribë Blerim Temal Fajza PUK ËS Gjinaj Shllak Rrethina Terthorë Qelëz Malzi Fushë Arrëz Shkodër KUK ËSI T Gur i Zi Kukës Rrapë Kolsh Shkodër Qerret Qafë Mali ´ Ana e Vau i Dejës Shtiqen Zapod Pukë Malit Berdicë Surroj Shtiqen 20°E 21°E Created 16 Dec 2019 / UTC+01:00 A1 Map shows the average precipitation for December in Albania. Map Document MA016_Alb_Ave_Precip_Dec Settlements Borders Projection & WGS 1984 UTM Zone 34N B1 CAPITAL INTERNATIONAL Datum City COUNTIES Tiranë C1 MUNICIPALITIES Albania: Average Produced by MapAction ADMIN 3 mapaction.org Precipitation for D1 0 2 4 6 8 10 [email protected] Precipitation (mm) December kilometres Supported by Supported by the German Federal E1 Foreign Office. - Sheet A1 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Data sources 7 8 9 0 1 2 3 4 5 6 7 8 9 0 1 2 - - - 1 1 1 1 1 1 1 1 1 1 2 2 2 The depiction and use of boundaries, names and - - - - - - - - - - - - - F1 .1 .1 .1 GADM, SRTM, OpenStreetMap, WorldClim 0 0 0 .1 .1 .1 .1 .1 .1 .1 .1 .1 .1 .1 .1 .1 associated data shown here do not imply 6 7 8 0 0 0 0 0 0 0 0 0 0 0 0 0 9 0 1 2 3 4 5 6 7 8 9 0 1 endorsement or acceptance by MapAction. -

Perzierja Dhe Hollimi I Produkteve Te Pastrimit Dhe Te Trajtimit Te Ujit Te Pijshem”

PERMBLEDHJE JOTEKNIKE PËR AKTIVITETIN: “Perzierja dhe hollimi I produkteve te pastrimit dhe te trajtimit te ujit te pijshem” Vendodhja: Rruga “Ura Beshirit”, fshati Lalm, Njesia Administrative Vaqarr, Bashkia Tirane. Kërkues: Subjekti: “CHEMICA D’AGOSTINO S.P.A.” dshh Janar, 2021 1 TË PERGJITHSHME Subjekti juridik “CHEMICA D’AGOSTINO S.P.A.” dshh me administrator Z. Leonardo Volpicella, është regjistruar në QKB me NUIS, L21409008V për ushtrimin e veprimtarisë në fusha te ndryshme ku perfshihet edhe: Prodhim, perpunim dhe tregtim te produkteve kimike ne pergjithesi dhe dytesore qe kane perdorim te ndryshem si industriale, ekologjike, farmaceutike, kozmetike dhe shtepiake, detergjent, detersive dhe produkte higjene; produkte per trajtimin e ujerave; produkte per trajtimin dhe riciklimin e mbetjeve urbane dhe/ose industriale dhe toksike; prodhim dhe/ose te materialeve plastike dhe derivate; drejtim, mirembajtje, kontroll, nepermjet menaxhimit te duhur te impianteve te ujerave te pishem me paradisinfektim, aglomerizim, filtrim i shpetje dhe postdezinfektim i ujerave siperfaqesore te lumenjeve, liqeneve dhe te ngjashme nepermjet impianteve te posacme te ngritjes me cfaredolloje fuqie si dhe pastrimin e ujerave shkarkues; ndertim dhe menaxhim i impianteve te pastrimit, dezinfektim i ambienteve, perpunim dhe depozitim per llogari te te treteve te produkteve kimike, kerkim dhe zhvillim i produkteve dhe teknologjive te reja lidhur me objektin e shoqerise. Subjekti “CHEMICA D’AGOSTINO S.P.A.” dshh ushtron aktivitetin e tij në adresën: Rruga “Ura Beshirit”, fshati Lalm, Njesia Administrative Vaqarr, Bashkia Tirane. 2 PËRSHKRIM I PROJEKTIT 2.1 Qëllimi iprojektit Qëllimi i funksionimit te ketij aktiviteti eshte ofrimi i produkteve kimike te nevojshme per tregun vendas. Keto produkte jane te kerkuara nga konsumatori dhe te domosdoshme per mbarefunksionimin e nje sere aktivitetesh dhe ofrimin e disa sherbimeve private ose publike. -

Company Profile Nderpro

Street: Reshit Collaku No. 20/290, Pallatet Shallvare, Nderpro Tirane, Albania w: www.nderpro.com m: [email protected] Mission & Vision ❖ Be the best construction company in Albania. ❖ Be a leader company in the construction industry in Albania, region and further. ❖ Offering sustainable solutions in the construction industry. ❖ Development of the company in a sustainable way by taking all the social responsibilities that belong to us. Our values ❖ Integrity: We are proud to be one of the first construction companies in Albania, starting our activity in the beginning of the ‘90s. Since our beginnings we have applied the same standard and for that we are proud. ❖ Respect: We respect every individual or institution. We try to be good citizens and take every responsibility that belongs to us. ❖ Winning Mentality: We have been performing good since day one and we will continue to do so. Our values ❖ Teamwork: We work in groups to successfully overcome every challenge and offer a sustainable development. ❖ Quality: Our company is a quality leader in the construction industry by implementing modern technologies to offer sustainable development. ❖ Customer Devotement: We see our clients as partners, for this reason we try to offer the best solutions for them. About us ❖ Operating in the Albanian market since early ‘90s. ❖ Formalised in 1998. ❖ Juridical status: Limited Liability Company. ❖ Founded and owned by a sole partner. Our projects ❖ Our projects are divided in two categories: ❖ Public works: Construction of different infrastructure facilities as a subcontractor of public institutions. ❖ C i v i l c o n s t r u c t i o n : Construction of different objects as an investor and development company. -

Albania Environmental Performance Reviews

Albania Environmental Performance Reviews Third Review ECE/CEP/183 UNITED NATIONS ECONOMIC COMMISSION FOR EUROPE ENVIRONMENTAL PERFORMANCE REVIEWS ALBANIA Third Review UNITED NATIONS New York and Geneva, 2018 Environmental Performance Reviews Series No. 47 NOTE Symbols of United Nations documents are composed of capital letters combined with figures. Mention of such a symbol indicates a reference to a United Nations document. The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city or area, or of its authorities, or concerning the delimitation of its frontiers or boundaries. In particular, the boundaries shown on the maps do not imply official endorsement or acceptance by the United Nations. The United Nations issued the second Environmental Performance Review of Albania (Environmental Performance Reviews Series No. 36) in 2012. This volume is issued in English only. Information cut-off date: 16 November 2017. ECE Information Unit Tel.: +41 (0)22 917 44 44 Palais des Nations Fax: +41 (0)22 917 05 05 CH-1211 Geneva 10 Email: [email protected] Switzerland Website: http://www.unece.org ECE/CEP/183 UNITED NATIONS PUBLICATION Sales No.: E.18.II.E.20 ISBN: 978-92-1-117167-9 eISBN: 978-92-1-045180-2 ISSN 1020–4563 iii Foreword The United Nations Economic Commission for Europe (ECE) Environmental Performance Review (EPR) Programme provides assistance to member States by regularly assessing their environmental performance. Countries then take steps to improve their environmental management, integrate environmental considerations into economic sectors, increase the availability of information to the public and promote information exchange with other countries on policies and experiences. -

Asatisfaction Survey on Social Services

A SATISFACTION SURVEY ON SOCIAL SERVICES TIRANA, ALBANIA JUNE 2018 Disclaimer This study is commissioned by the United Nations Development Programme (UNDP) in Albania in the framework of “Leave No One Behind” programmes funded by the Swiss Agency for Development and Cooperation. Opinions and views expressed in this report do not necessarily reflect those of the United Nations Development Programme (UNDP), or of the United Nations (UN). Lead researcher: Marsela Dauti, PhD Junior researchers: Olta Kamberi & Xhenson Çela 2 Acknowledgements We are grateful to social service providers that participated in the study, including Community Center for Persons with Disabilities (Bulqizë), Center “Lira” (Berat), Intercultural Community Center (Berat), Center for Community Services for Persons with Disabilities (Durrës), Multifunctional Community Center Nishtulla (Durrës), Daily Center for Persons with Disabilities “Horizont” (Fier), Help for Children Foundation (Fier), Disutni (Korçë), Physical Rehabilitation Center (Korçë), Social Services Center (Kukës), Help for Children Foundation (Krujë), Daily Center for Development (Arrameras, Krujë), Daily Center for Development “Trëndafilat” (Lezhë), Help for Children Foundation (Lezhë), Shenjta Mari Center (Lezhë), Development Center for Persons with Disabilities (Lushnje), Daily Center for Persons with Disabilities (Pogradec), Community Center (Shijak), Intercultural Community Center (Pogradec), Daily Center for Persons with Disabilities (Sarandë), Multifunctional Center no. 4 (Shkodër), Daily Center for Development (Shkodër), Albanian Children Foundation “Domenick Scaglione” (Tiranë), Help the Life Center (Tiranë), Jonathan Center (Tiranë), Multifunctional Center "Shtëpia e Ngjyrave" (ARSIS) (Tiranë), Romani Baxt (Tiranë), Romani Woman of Tomorrow (Tiranë). We thank social service departments in the municipalities of Lezha, Kruja, Fier, Dibër, Përmet, Ura Vajgurore, Korça, Pogradec, Lushnja, Bulqiza, Saranda, Shijak, Tirana, Durrës, Shkodër, Kukës, Berat, and Prrenjas for providing data and support during fieldwork.