Chennai Urban Land Market Assessment

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Tamil Nadu Sustainable Urban Development Project Final EA for SWD to Selected Areas of Coc

Tamil Nadu Sustainable Urban Development Project Final EA for SWD to selected areas of CoC Public Disclosure Authorized Tamil Nadu Sustainable Urban Development Project (TNSUDP) Storm Water Drainage Project for the Selected Areas of Chennai Corporation Public Disclosure Authorized Tamil Nadu Sustainable Urban Development Project Public Disclosure Authorized Final Environmental Assessment Report Public Disclosure Authorized January 2015 Storm Water Drains Department, Corporation of Chennai 1 Tamil Nadu Sustainable Urban Development Project Final EA for SWD to selected areas of CoC Executive Summary 1. INTRODUCTION 1. Government of Tamil Nadu has proposed to implement the World Bank supported Tamil Nadu Sustainable Urban Development program (TNSUDP) to improve the delivery of urban services. The provision of Storm Water Drains to selected areas of Corporation of Chennai is one of the sub-projects proposed to be implemented by the Corporation of Chennai (CoC). This component is coordinated by Government of Tamil Nadu with Tamil Nadu Urban Infrastructure Financial Services Ltd. (TNUIFSL), Chennai as the fund Manager. This sub project is proposed to be implemented along the roadsides and canals and doesn’t involve any Land Acquisition and required land is owned by the Corporation of Chennai. 2. PROJECT DESCRIPTION 2. The Storm Water Drainage project for the selected areas of Corporation of Chennai proposed to be taken up under the TNSUDP involves construction of storm water drains and canals in the project area. This sub project proposed to be implemented in the 4 Zones of the CoC. The total length of the drains to be constructed is about 270.33 kilometres including the 11.05 km length in the canals. -

India's Covid Cases Escalating at the Fastest Pace in Asia

Follow us on: RNI No. APENG/2018/764698 @TheDailyPioneer facebook.com/dailypioneer Established 1864 Published From ANALYSIS 7 MONEY 8 SPORTS 11 VIJAYAWADA DELHI LUCKNOW MUCH ADO 9 OUT OF 10 STARTUPS BLEEDING NEVER DOUBTED MYSELF BHOPAL RAIPUR CHANDIGARH ABOUT NOTHING IN INDIA, SAYS NASSCOM SURVEY IN GAME SITUATIONS: KOHLI BHUBANESWAR RANCHI DEHRADUN HYDERABAD *Late City Vol. 2 Issue 197 VIJAYAWADA, WEDNESDAY MAY 20, 2020; PAGES 12 `3 *Air Surcharge Extra if Applicable VARALAXMI DISMISSES MARRIAGE RUMOURS { Page 12 } www.dailypioneer.com CONG CALLS MEET ON MIGRANTS' MAMATA CONFIRMS PARTICIPATION IN SC REFUSES TO TRANSFER CASES TO CBI, CHINESE LAB BELIEVES NEW DRUG CAN PLIGHT, CHANGES IN LABOUR LAWS OPPN MEETING ON CORONAVIRUS CRISIS GRANTS PROTECTION TO ARNAB GOSWAMI ‘STOP COVID WITHOUT VACCINE’ he Congress has called a meeting of like-minded opposition parties on Friday est Bengal Chief Minister Mamata Banerjee Tuesday confirmed her n partial relief to Republic TV Editor-in-Chief Arnab Goswami, the Chinese laboratory has been developing a drug it believes has the power to Tto discuss the plight of migrant workers and the changes in labour laws by Wparticipation in the opposition parties' virtual meet convened by the Supreme Court Tuesday quashed all criminal investigations related to Abring the coronavirus pandemic to a halt. The outbreak first emerged in China some states, sources said. Congress president Sonia Gandhi will chair the Congress to discuss the COVID-19 situation and the impact of the lockdown. Ithe news show on Palghar mob-lynching except the initial one that is late last year before spreading across the world, prompting an international race meeting of leaders of opposition parties, the sources said on Tuesday. -

From Deluge to Displacement the Impact of Post-Flood Evictions and Resettlement in Chennai

FROM DELUGE TO DISPLACEMENT The Impact of Post-flood Evictions and Resettlement in Chennai Information and Resource HOUSING AND LAND Centre for the Deprived RIGHTS NETWORK Urban Communities GREEN PUBLIC PROCUREMENT GREEN PUBLIC PROCUREMENT: Policy and Practice within the European Union and India Authors: Ms Barbara Morton, Mr Rajan Gandhi Reviewed by: Mr Wandert Benthem and Dr Johan Bentinck (Euroconsult Mott MacDonald) Copy Editing by: Mr Surit Das Suggested Citation: From Deluge to Displacement: The Impact of Post-flood Evictions and Resettlement in Chennai, Information and Resource Centre for the Deprived Urban Communities, and Housing and Land Rights Network, Refer to the document on the project website (http://www.apsfenvironment.in/) for the hyperlinked New Delhi, 2017 version. Survey Team: Kannagi Nagar Pothu Nalla Sangam (Kannagi Nagar Residents’ Welfare Association) and Furthervolunteers information from various non-government organizations working in these settlements Euroconsult Mott MacDonald: www.euroconsult.mottmac.nl, www.mottmac.com Study Author: Vanessa Peter (with inputs from Shivani Chaudhry) Information about the European Union is available on the Internet. It can be accessed through the EEditor:uropa Shivani server Chaudhry(www.europa.eu) and the website of the Delegation of the European Union to India (http://eeas.europa.eu/delegations/india/index_en.htm). Published by: LHousingegal notices: and Land Rights Network G-18/1 Nizamuddin West EuropeanLower Ground Union Floor TNewhis Delhipublication – 110013, has INDIA been produced with the assistance of the European Union. The content of thiswww.hlrn.org.in publication is the sole responsibility of the Technical Assistance Team and Mott MacDonald in [email protected] with DHI and can in no way be taken to reflect the views of the European Union or the Delegation+91-11-4054-1680 of the European Union to India. -

1.Climate Resilient Green Economy: Prospects

INTERNATIONAL REVIEW OF BUSINESS AND ECONOMICS ISSN 2474 -5146 (Online) 1.CLIMATE RESILIENT GREEN ECONOMY: PROSPECTS Dr.R.RAGAPRIYA, I.A.S.,Managing Director, Gulbarga Electric Supply Company, Government of Karnataka. Prof.D.RUDRAPPAN, President, AMECA, Former Joint Director of Collegiate Education, Govt. of Tamil Nadu, Professor, Department of Development Economics, Ethiopian Civil Service University, Ethiopia. “The size and extent of the climate change ecosystem services were found to be degraded threats are new. It is arguably the biggest or used unsustainably. The gap between challenge humanity faces today. This the rich and poor has also been increasing- means that we must act urgently and seize between 1990 and 2005, income disparity opportunities quickly. One such opportunity (measured by the gap between the highest is renewable energy,” – President of the 72nd and lowest income earners) rose in more than UN General Assembly. two-thirds of countries. ABSTRACT The persistence of poverty and degradation of new political climate has grown in many the environment can be traced to a series of Acountries around the world, thanks to market and institutional failures that make the the strong base in science and widening prevailing economic theory far less effective public awareness of climate change and than it otherwise would be in advancing its risks. Clean energy revolution has been sustainable development ambitions. These taking place all over the developed countries, market and institutional failures are well underscored by the steady expansion of known to economists, but little progress has the renewable energy sector. The adoption been made to address them. For example, of Renewable Energy Technologies (RETs) there are not sufficient mechanisms to constituted a win-win situation, as renewable ensure that polluters pay the full cost of is not only green and job-generating, but their pollution. -

India Real Estate H2, 2020

Research years in INDIyears in A INDIA IndiaIndia RealReal Estate Estate Residential and Office - July - December 2020 INDIA REAL ESTATE INDIA REAL ESTATE Mumbai HO Knight Frank (India) Pvt. Ltd. Paville House, Near Twin Towers, Off. Veer Savarkar Marg, Prabhadevi, Mumbai 400 025, India 022 6745 0101 / 4928 0101 Bengaluru Knight Frank (India) Pvt. Ltd. 204 & 205, 2nd Floor, Embassy Square, #148 Infantry Road, Bengaluru 560001, India 080 40732600 / 22385515 Pune Knight Frank (India) Pvt. Ltd. Unit No.701, Level 7, Pentagon Towers P4, Magarpatta City, Hadapsar, Pune 411 013, India 020 67491500 / 30188500 Chennai Knight Frank (India) Pvt. Ltd. 1st Floor, Centre block, Sunny Side, 8/17, Shafee Mohammed Road, Nungambakkam, Chennai 600 006 044 4296 9000 Gurgaon Knight Frank (India) Pvt. Ltd. Office Address: 1505-1508, 15th Floor, Tower B, Signature Towers South City 1, Gurgaon 122 001, India 0124 4782700 Hyderabad Western Dallas Centre, 5th floor, Office #3, Hyderabad Knowledge City, Survey No. 83/1, Raidurg, Serilingampally Mandal, Ranga Reddy District, Telangana Hyderabad - 500 032 040 4455 4141 Kolkata Knight Frank (India) Pvt. Ltd. PS Srijan Corporate Park Unit Number – 1202A, 12th Floor, Block – EP & GP, Plot Number - GP 2, Sector – V, Salt Lake, Kolkata 700 091 033 66521000 Ahmedabad Knight Frank (India) Pvt. Ltd. Unit Nos. 407 & 408, Block ‘C’, The First, B/H Keshav Baugh Party Plot, Vastrapur, Ahmedabad – 380015 079 48940259 / 40380259 www.knightfrank.co.in/research 2 INDIA REAL ESTATE Foreword Shishir Baijal Chairman and Managing Director he year 2020 had reflections of both COVID-19 pandemic As we embark upon 2021, market developments in the last few associated disturbances in the beginning as well as months have enthused strong hope among market stakeholders. -

District Statistical Hand Book Chennai District 2016-2017

Government of Tamil Nadu Department of Economics and Statistics DISTRICT STATISTICAL HAND BOOK CHENNAI DISTRICT 2016-2017 Chennai Airport Chennai Ennoor Horbour INDEX PAGE NO “A VIEW ON ORGIN OF CHENNAI DISTRICT 1 - 31 STATISTICAL HANDBOOK IN TABULAR FORM 32- 114 STATISTICAL TABLES CONTENTS 1. AREA AND POPULATION 1.1 Area, Population, Literate, SCs and STs- Sex wise by Blocks and Municipalities 32 1.2 Population by Broad Industrial categories of Workers. 33 1.3 Population by Religion 34 1.4 Population by Age Groups 34 1.5 Population of the District-Decennial Growth 35 1.6 Salient features of 1991 Census – Block and Municipality wise. 35 2. CLIMATE AND RAINFALL 2.1 Monthly Rainfall Data . 36 2.2 Seasonwise Rainfall 37 2.3 Time Series Date of Rainfall by seasons 38 2.4 Monthly Rainfall from April 2015 to March 2016 39 3. AGRICULTURE - Not Applicable for Chennai District 3.1 Soil Classification (with illustration by map) 3.2 Land Utilisation 3.3 Area and Production of Crops 3.4 Agricultural Machinery and Implements 3.5 Number and Area of Operational Holdings 3.6 Consumption of Chemical Fertilisers and Pesticides 3.7 Regulated Markets 3.8 Crop Insurance Scheme 3.9 Sericulture i 4. IRRIGATION - Not Applicable for Chennai District 4.1 Sources of Water Supply with Command Area – Blockwise. 4.2 Actual Area Irrigated (Net and Gross) by sources. 4.3 Area Irrigated by Crops. 4.4 Details of Dams, Tanks, Wells and Borewells. 5. ANIMAL HUSBANDRY 5.1 Livestock Population 40 5.2 Veterinary Institutions and Animals treated – Blockwise. -

Chennai District Origin of Chennai

DISTRICT PROFILE - 2017 CHENNAI DISTRICT ORIGIN OF CHENNAI Chennai, originally known as Madras Patnam, was located in the province of Tondaimandalam, an area lying between Pennar river of Nellore and the Pennar river of Cuddalore. The capital of the province was Kancheepuram.Tondaimandalam was ruled in the 2nd century A.D. by Tondaiman Ilam Tiraiyan, who was a representative of the Chola family at Kanchipuram. It is believed that Ilam Tiraiyan must have subdued Kurumbas, the original inhabitants of the region and established his rule over Tondaimandalam Chennai also known as Madras is the capital city of the Indian state of Tamil Nadu. Located on the Coromandel Coast off the Bay of Bengal, it is a major commercial, cultural, economic and educational center in South India. It is also known as the "Cultural Capital of South India" The area around Chennai had been part of successive South Indian kingdoms through centuries. The recorded history of the city began in the colonial times, specifically with the arrival of British East India Company and the establishment of Fort St. George in 1644. On Chennai's way to become a major naval port and presidency city by late eighteenth century. Following the independence of India, Chennai became the capital of Tamil Nadu and an important centre of regional politics that tended to bank on the Dravidian identity of the populace. According to the provisional results of 2011 census, the city had 4.68 million residents making it the sixth most populous city in India; the urban agglomeration, which comprises the city and its suburbs, was home to approximately 8.9 million, making it the fourth most populous metropolitan area in the country and 31st largest urban area in the world. -

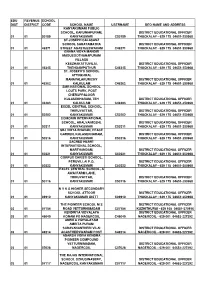

Deo &Ceo Address List

EDU REVENUE SCHOOL DIST DISTRICT CODE SCHOOL NAME USERNAME DEO NAME AND ADDRESS KANYAKUMARI PUBLIC SCHOOL, KARUNIAPURAM, DISTRICT EDUCATIONAL OFFICER 01 01 50189 KANYAKUMARI C50189 THUCKALAY - 629 175 04651-250968 ST.JOSEPH CALASANZ SCHOOL SAHAYAMATHA DISTRICT EDUCATIONAL OFFICER 01 01 46271 STREET AGASTEESWARAM C46271 THUCKALAY - 629 175 04651-250968 GNANA VIDYA MANDIR MADUSOOTHANAPURAM VILLAGE KEEZHAKATTUVILAI, DISTRICT EDUCATIONAL OFFICER 01 01 46345 THENGAMPUTHUR C46345 THUCKALAY - 629 175 04651-250968 ST. JOSEPH'S SCHOOL ATTINKARAI, MANAVALAKURICHY DISTRICT EDUCATIONAL OFFICER 01 01 46362 KALKULAM C46362 THUCKALAY - 629 175 04651-250968 SMR NATIONAL SCHOOL LOUTS PARK, POST CHERUPPALOOR KULASEKHARAM, TEH DISTRICT EDUCATIONAL OFFICER 01 01 46383 KALKULAM C46383 THUCKALAY - 629 175 04651-250968 EXCEL CENTRAL SCHOOL, THIRUVATTAR, DISTRICT EDUCATIONAL OFFICER 01 01 50202 KANYAKUMARI C50202 THUCKALAY - 629 175 04651-250968 COMORIN INTERNATIONAL SCHOOL, ARALVAIMOZHI, DISTRICT EDUCATIONAL OFFICER 01 01 50211 KANYAKUMARI C50211 THUCKALAY - 629 175 04651-250968 SBJ VIDYA BHAVAN, PEACE GARDEN, KULASEKHARAM, DISTRICT EDUCATIONAL OFFICER 01 01 50216 KANYAKUMARI C50216 THUCKALAY - 629 175 04651-250968 SACRED HEART INTERNATIONAL SCHOOL, MARTHANDAM, DISTRICT EDUCATIONAL OFFICER 01 01 50221 KANYAKUMARI C50221 THUCKALAY - 629 175 04651-250968 CORPUS CHRISTI SCHOOL, PERUVILLAI P.O, DISTRICT EDUCATIONAL OFFICER 01 01 50222 KANYAKUMARI C50222 THUCKALAY - 629 175 04651-250968 EXCEL CENTRAL SCHOOL, A AWAI FARM LANE, THIRUVATTAR, DISTRICT EDUCATIONAL OFFICER -

Media Developmentvol LIV 1/2007

2007(PL2).qxd 1/18/07 10:16 AM Page 1 Media Development Vol LIV 1/2007 3 How do fundamentalists shape media 41 Pentecostalism, media and cultural agendas? discourse in Africa Stewart M. Hoover and Nadia Kaneva Ogbu Kalu 7 From ‘bumkins’to Baghdad:Fumbling 45 The unknown history of televangelism with fundamentalism William F. Fore Steve Rabey FORUMFORUM FORUM 12 Media, politics and fundamentalism in 49 Communication is peace: Latin America WACC’s mission today Dennis Smith Philip Lee 16 From the pulpit to the studio: Islam’s 53 New Convention for Persons with internal battle Disabilities Nabil Echchaibi 56 Congo’s hidden tragedy 20 Women, news and fundamentalism Hugh McCullum Sheila J. Gibbons 60 On the page . 23 Christian fundamentalism and the media in South India Pradip N. Thomas 32 Columbusday, hate speech, and American Indians Tink Tinker In the next issue Mass media in the Middle East and repre- sentations of the Middle East in the media 36 Religion, identity and dialogue will be the focus of the 2/2007 issue of Glory E. Dharmaraj Media Development. 2007(PL2).qxd 1/18/07 10:16 AM Page 2 This issue of Media Of course, we have to distin- EDITORIAL Development is based on the guish between the absolute need proceedings of that conference. for freedom of expression and In 2007 the Creation Museum R. Scott Appleby, co-direc- the mandatory imposition of will open in Kentucky, USA, tor with Martin E. Marty of the controversial beliefs. People dedicated to the proposition renowned Fundamentalism have the right to believe in that the account given in the Project, gave a public lecture angels provided that such a Book of Genesis is literally cor- during the conference called belief does no harm to others. -

![F Uvc T`^^F Zej Dfcgvz]]R TV+ 8`Ge](https://docslib.b-cdn.net/cover/3611/f-uvc-t-f-zej-dfcgvz-r-tv-8-ge-1963611.webp)

F Uvc T`^^F Zej Dfcgvz]]R TV+ 8`Ge

1 6 ,0-7 1-7 7 -!5!56 2*34$0 /"75,78$% , : : 8 '89 :%;9 % 9 8>% ?% ?8?9 ?%8 !> 9 : %9 :% @ !9 8 2 8 ; ? '@; < )" ./ < 91 , !"#"#$%& ! " # $ %&'$% ore than 54,000 persons Mare under community surveillance against the back- drop of coronavirus pandem- ! ic and the health workers are in " regular touch with them, %O !" Health Minister Harsh %' ()* Vardhan informed Parliament + # on Tuesday. People with flu-like , *-./ symptoms but without a his- 0 $%&' tory of travel abroad are under 0 1 community surveillance. ( Informing the Rajya Sabha 2 0 about measures taken to fight 3/ % the pandemic, the Health Minister assured Rajya Sabha 3535 members that any complaint about reported unhygienic ith 137 positive cases by conditions in the quarantine is WTuesday evening and getting due attention. Karti Chidambaram sprang a three deaths, latest in Tuesday Highlighting the role of the surprise in the Lok Sabha by in Maharashtra, the medical fraternity, Harsh complimenting the Union Government has decided to ( Vardhan said, “As one metre Government for its efforts to rope in accredited private labs ) $& social distancing is required to tackle coronavirus and said to conduct tests for the infec- be taken while dealing with $& one should not “play politics” tion and recommended anti- for laboratory testing and pro- head of the Epidemiology and those affected with the virus, I '& over the issue. HIV drug combination vide positive controls for estab- Communicable Diseases at laud doctors and paramedics Rahul has all along been Lopinavir-Ritonavir on case-to- lishing the test as soon as the ICMR, said the testing capac- who are working honestly with ties in their areas and suggest are rare complaints,” he said. -

Dispossession by Neglect: Agricultural Land Sales in the Periphery of Chennai

MIDS WORK I NG PA P ER NO. 223 Dispossession by Neglect: Agricultural Land Sales in the Periphery of Chennai M. Vijayabaskar and Ajit Menon Madras Institute of Development Studies July 2016 mids Madras Institute of Development Studies MIDS Working Paper No. 223, July 2016 Dispossession by Neglect: Agricultural Land Sales in the Periphery of Chennai by M. Vijayabaskar and Ajit Menon Rs. 25.00 Madras Institute of Development Studies 79, Second Main Road, Gandhi Nagar Adyar, Chennai 600 020 Tel.: 2441 1574/2589/2295/9771 Fax : 91-44-24910872 [email protected] http://www.mids.ac.in Dispossession by Neglect: Agricultural Land Sales in the Periphery of Chennai* M. Vijayabaskar and Ajit Menon** Abstract The emergence of active land markets in the periphery of Chennai has resulted in large tracts of agricultural land being bought by non- agricultural actors who seek returns primarily on speculation. We argue in this paper that the financialisation of land and consequent spurt in the sale of agricultural land are central to what scholars have termed ‘land grab’. Recent literature on land grabs has focused primarily on processes of accumulation by dispossession and the coercive role of the state. Our contention is that land grabs more commonly occur due to the state under-investing in agriculture, resulting in ‘dispossession by neglect’ of especially marginal and small farmers. Dispossession by neglect better captures the fluid boundary between the coercive and the voluntary in contemporary land grabs. Key Words: Dispossession, Land market, Land grab, Financialisation of land. 1. Introduction Raghavan (name changed) has been practicing as a civil lawyer for several years in metropolitan Chennai, India. -

Tamil Nadu Public Service Commission Bulletin

© [Regd. No. TN/CCN-466/2012-14. GOVERNMENT OF TAMIL NADU [R. Dis. No. 196/2009 2015 [Price: Rs. 280.80 Paise. TAMIL NADU PUBLIC SERVICE COMMISSION BULLETIN No. 18] CHENNAI, SUNDAY, AUGUST 16, 2015 Aadi 31, Manmadha, Thiruvalluvar Aandu-2046 CONTENTS DEPARTMENTAL TESTS—RESULTS, MAY 2015 Name of the Tests and Code Numbers Pages. Pages. Second Class Language Test (Full Test) Part ‘A’ The Tamil Nadu Wakf Board Department Test First Written Examination and Viva Voce Parts ‘B’ ‘C’ Paper Detailed Application (With Books) (Test 2425-2434 and ‘D’ (Test Code No. 001) .. .. .. Code No. 113) .. .. .. .. 2661 Second Class Language Test Part ‘D’ only Viva Departmental Test in the Manual of the Firemanship Voce (Test Code No. 209) .. .. .. 2434-2435 for Officers of the Tamil Nadu Fire Service First Paper & Second Paper (Without Books) Third Class Language Test - Hindi (Viva Voce) (Test Code No. 008 & 021) .. .. .. (Test Code 210), Kannada (Viva Voce) 2661 (Test Code 211), Malayalam (Viva Voce) (Test The Agricultural Department Test for Members of Code 212), Tamil (Viva Voce) (Test Code 213), the Tamil Nadu Ministerial Service in the Telegu (Viva Voce) (Test Code 214), Urdu (Viva Agriculture Department (With Books) Test Voce) (Test Code 215) .. .. .. 2435-2436 Code No. 197) .. .. .. .. 2662-2664 The Account Test for Subordinate Officers - Panchayat Development Account Test (With Part-I (With Books) (Test Code No. 176) .. 2437-2592 Books) (Test Code No. 202).. .. .. 2664-2673 The Account Test for Subordinate Officers The Agricultural Department Test for the Technical Part II (With Books) (Test Code No. 190) .. 2593-2626 Officers of the Agriculture Department Departmental Test for Rural Welfare Officer (With Books) (Test Code No.