India Real Estate H2, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Village Panchayats in Tamil Nadu District Code District Name

List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 1 Kanchipuram 1 Kanchipuram 1 Angambakkam 2 Ariaperumbakkam 3 Arpakkam 4 Asoor 5 Avalur 6 Ayyengarkulam 7 Damal 8 Elayanarvelur 9 Kalakattoor 10 Kalur 11 Kambarajapuram 12 Karuppadithattadai 13 Kavanthandalam 14 Keelambi 15 Kilar 16 Keelkadirpur 17 Keelperamanallur 18 Kolivakkam 19 Konerikuppam 20 Kuram 21 Magaral 22 Melkadirpur 23 Melottivakkam 24 Musaravakkam 25 Muthavedu 26 Muttavakkam 27 Narapakkam 28 Nathapettai 29 Olakkolapattu 30 Orikkai 31 Perumbakkam 32 Punjarasanthangal 33 Putheri 34 Sirukaveripakkam 35 Sirunaiperugal 36 Thammanur 37 Thenambakkam 38 Thimmasamudram 39 Thilruparuthikundram 40 Thirupukuzhi List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 41 Valathottam 42 Vippedu 43 Vishar 2 Walajabad 1 Agaram 2 Alapakkam 3 Ariyambakkam 4 Athivakkam 5 Attuputhur 6 Aymicheri 7 Ayyampettai 8 Devariyambakkam 9 Ekanampettai 10 Enadur 11 Govindavadi 12 Illuppapattu 13 Injambakkam 14 Kaliyanoor 15 Karai 16 Karur 17 Kattavakkam 18 Keelottivakkam 19 Kithiripettai 20 Kottavakkam 21 Kunnavakkam 22 Kuthirambakkam 23 Marutham 24 Muthyalpettai 25 Nathanallur 26 Nayakkenpettai 27 Nayakkenkuppam 28 Olaiyur 29 Paduneli 30 Palaiyaseevaram 31 Paranthur 32 Podavur 33 Poosivakkam 34 Pullalur 35 Puliyambakkam 36 Purisai List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 37 -

Thiruvallur District

DISTRICT DISASTER MANAGEMENT PLAN FOR 2017 TIRUVALLUR DISTRICT tmt.E.sundaravalli, I.A.S., DISTRICT COLLECTOR TIRUVALLUR DISTRICT TAMIL NADU 2 COLLECTORATE, TIRUVALLUR 3 tiruvallur district 4 DISTRICT DISASTER MANAGEMENT PLAN TIRUVALLUR DISTRICT - 2017 INDEX Sl. DETAILS No PAGE NO. 1 List of abbreviations present in the plan 5-6 2 Introduction 7-13 3 District Profile 14-21 4 Disaster Management Goals (2017-2030) 22-28 Hazard, Risk and Vulnerability analysis with sample maps & link to 5 29-68 all vulnerable maps 6 Institutional Machanism 69-74 7 Preparedness 75-78 Prevention & Mitigation Plan (2015-2030) 8 (What Major & Minor Disaster will be addressed through mitigation 79-108 measures) Response Plan - Including Incident Response System (Covering 9 109-112 Rescue, Evacuation and Relief) 10 Recovery and Reconstruction Plan 113-124 11 Mainstreaming of Disaster Management in Developmental Plans 125-147 12 Community & other Stakeholder participation 148-156 Linkages / Co-oridnation with other agencies for Disaster 13 157-165 Management 14 Budget and Other Financial allocation - Outlays of major schemes 166-169 15 Monitoring and Evaluation 170-198 Risk Communications Strategies (Telecommunication /VHF/ Media 16 199 / CDRRP etc.,) Important contact Numbers and provision for link to detailed 17 200-267 information 18 Dos and Don’ts during all possible Hazards including Heat Wave 268-278 19 Important G.Os 279-320 20 Linkages with IDRN 321 21 Specific issues on various Vulnerable Groups have been addressed 322-324 22 Mock Drill Schedules 325-336 -

Disaster Preparedness and Response

DISASTER PREPAREDNESS AND RESPONSE Lessons from Tsunami Report of the National Consultation 14–16 February 2006 Disaster Preparedness and Response: Lessons from Tsunami Report of the National Consultation 14 - 16 February 2006 Organised by Supported by This National Consultation was dedicated to the memory of the several who lost their lives in the Tsunami of December 2004 and in honour of Mr. Karl Kübel, founder of Karl Kübel institutions worldwide, philanthropist and a pioneering spirit of international development cooperation, who expired in Bensheim, Germany on 10th February 2006 x2 Introduction Massive ocean waves unleashed by an undersea earthquake, measuring 8.9 on the Richter scale, that had its epicentre 250 kilometres southeast of Banda Aceh in Sumatra in Indonesia, the most powerful in 40 years, cut a swathe of destruction in a coastal arc across South Asia and South-East Asia on the morning of 26th December 2004. The total death toll stood at 159,260 with 17,958 missing, according to figures compiled by the United Nations Office for the Coordination of Humanitarian Affairs in mid-January 2005. In India, the Tamil Nadu coast and the Andaman and Nicobar islands took the brunt of the tsunami, or killer wave, strikes. The toll in Tamil Nadu stood at more than 3,500, including 160 deaths in Chennai, the State capital. About 2,000 persons were killed in Nagapattinam district alone, which has been a victim of cyclones year after year. The ferocity of the waves that hit Nagapattinam town was unimaginable. Water entered 1.5 km inside the town. Communications and electricity supply were cut off in the affected areas. -

Branch Libraries List

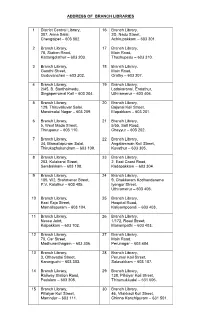

ADDRESS OF BRANCH LIBRARIES 1 District Central Library, 16 Branch Library, 307, Anna Salai, 2D, Nadu Street, Chengalpet – 603 002. Achirupakkam – 603 301. 2 Branch Library, 17 Branch Library, 78, Station Road, Main Road, Kattangolathur – 603 203. Thozhupedu – 603 310. 3 Branch Library, 18 Branch Library, Gandhi Street, Main Road, Guduvancheri – 603 202. Orathy – 603 307. 4 Branch Library, 19 Branch Library, 2/45, B. Santhaimedu, Ladakaranai, Endathur, Singaperrumal Koil – 603 204. Uthiramerur – 603 406. 5 Branch Library, 20 Branch Library, 129, Thiruvalluvar Salai, Bajanai Koil Street, Maraimalai Nagar – 603 209. Elapakkam – 603 201. 6 Branch Library, 21 Branch Library, 5, West Mada Street, 5/55, Salt Road, Thiruporur – 603 110. Cheyyur – 603 202. 7 Branch Library, 22 Branch Library, 34, Mamallapuram Salai, Angalamman Koil Street, Thirukazhukundram – 603 109. Kuvathur – 603 305. 8 Branch Library, 23 Branch Library, 203, Kulakarai Street, 2, East Coast Road, Sembakkam – 603 108. Kadapakkam – 603 304. 9 Branch Library, 24 Branch Library, 105, W2, Brahmanar Street, 9, Chakkaram Kodhandarama P.V. Kalathur – 603 405. Iyengar Street, Uthiramerur – 603 406. 10 Branch Library, 25 Branch Library, East Raja Street, Hospital Road, Mamallapuram – 603 104. Kaliyampoondi – 603 403. 11 Branch Library, 26 Branch Library, Nesco Joint, 1/172, Road Street, Kalpakkam – 603 102. Manampathi – 603 403. 12 Branch Library, 27 Branch Library, 70, Car Street, Main Road, Madhuranthagam – 603 306. Perunagar – 603 404. 13 Branch Library, 28 Branch Library, 3, Othavadai Street, Perumal Koil Street, Karunguzhi – 603 303. Salavakkam – 603 107. 14 Branch Library, 29 Branch Library, Railway Station Road, 138, Pillaiyar Koil Street, Padalam – 603 308. -

INSITE 99Acres India’S No.1 Property Portal

www.99acres.com CHENNAI RESIDENTIAL MARKET UPDATE JULY-SEPTEMBER 2019 Market Sentiment INSITE 99acres India’s No.1 Property Portal FROM CBO’S DESK With the news of an impending provide financing to the many stalled economic slowdown clouding the affordable and mid-income housing market, end-user and investor activity projects in the country cheered plunged evidently in residential real the market. The Government will estate in Jul-Sep 2019. This clubbed contribute Rs 10,000 crore, which with multiple insolvency proceedings is anticipated to benefit around and the on-going financial crunch that 350,000 housing units. Further, most developers are struggling with consecutive repo rate cuts and the kept overall sentiment submissive. mandate around repo rate linked Average weighted prices of residential home loans are seen as housing apartments witnessed meager demand lifters. The impact of alterations quarter on quarter, barring these policy announcements will Hyderabad and Ahmedabad. Rentals, be more evident in the ensuing too, grew insignificantly in the last one festive quarters. year. An inventory overhang of 10 lakh units along with 5.6 lakh delayed homes across the country kept price points under check. On the supply front, the top eight metros saw the launch of around 486 housing projects in Jul-Sep 2019, about 30 percent down from Apr-Jun 2019. While the quarter did not have many laurels to talk about, the Finance Maneesh Upadhyaya Minister’s announcement regarding Chief Business Officer the creation of a special fund to 99acres.com NATIONAL MARKET OUTLOOK INDICATORS Capital Values Rental Values Supply HOME BUYING SENTIMENT Home buying sentiment remained weak due to developer defaults and the NBFC crisis, which dried up funding and slowed the completion of already delayed projects. -

15 Sub Ptt MSB-TBM-CGL DOWN WEEK DAYS

CHENNAI BEACH - TAMBARAM - CHENGALPATTU DOWN WEEK DAYS Train Nos 40501 40001 40503 40505 40507 40701 40509 Kms Stations CJ 0 Chennai Beach d 03:55 04:15 04:35 04:55 05:15 05:30 05:50 2 Chennai Fort d 03:59 04:19 04:39 04:59 05:19 05:34 05:54 4 Chennai Park d 04:02 04:22 04:42 05:02 05:22 05:37 05:57 5 Chennai Egmore d 04:05 04:25 04:45 05:05 05:25 05:40 06:00 7 Chetpet d 04:08 04:28 04:48 05:08 05:28 05:43 06:03 9 Nungambakkam d 04:11 04:31 04:51 05:11 05:31 05:46 06:06 10 Kodambakkam d 04:13 04:33 04:53 05:13 05:33 05:48 06:08 12 Mambalam d 04:15 04:35 04:55 05:15 05:35 05:50 06:10 13 Saidapet d 04:18 04:38 04:58 05:18 05:38 05:53 06:13 16 Guindy d 04:21 04:41 05:01 05:21 05:41 05:56 06:16 18 St.Thomas Mount d 04:24 04:44 05:04 05:24 05:44 05:59 06:19 19 Palavanthangal d 04:27 04:47 05:07 05:27 05:47 06:02 06:22 21 Minambakkam d 04:30 04:50 05:10 05:30 05:50 06:05 06:25 22 Tirusulam d 04:32 04:52 05:12 05:32 05:52 06:07 06:27 24 Pallavaram d 04:35 04:55 05:15 05:35 05:55 06:10 06:30 26 Chrompet d 04:38 04:58 05:18 05:38 05:58 06:13 06:33 29 Tambaram Sanatorium d 04:41 05:01 05:21 05:41 06:01 06:16 06:36 30 Tambarm a 05:10 d 04:50 05:30 05:50 06:10 06:25 06:45 34 Perungulathur d 04:56 05:36 05:56 06:16 06:32 06:56 36 Vandalur d 04:59 05:39 05:59 06:19 06:35 06:59 39 Urappakkam d 05:03 05:43 06:03 06:23 06:39 07:03 42 Guduvancheri d 05:07 05:47 06:07 06:27 06:43 07:07 44 Potheri d 05:11 05:51 06:11 06:31 06:47 07:11 46 Kattangulathur d 05:14 05:54 06:14 06:34 06:50 07:14 47 Maraimalai Nagar d 05:16 05:56 06:16 06:36 06:52 07:16 51 Singaperumal -

Faculty : Electrical Engineering S.NO

Faculty : Electrical Engineering S.NO. Ref. No Name of the Department College/Organisation Research Area Email Supervisor 1 2462/C11/93 Mohan M R Dept. of College of Engg., Anna Generation scheduling, - Electrical and University, Chennai Distribution Network and Electronics Power Quality Engg. 2 59.102.05 Gnanamani A Microbiology Central Leather Microbial Enzymes, [email protected] Division Institute of Technology, Microbial By Products and Chennai Plant Products 3 59.111.14 Sujit Kumar Bag Dept. of Arulmigu Kalasalingam Control Systems, Neural Electrical and College of Engg., Networking, Image Electronics Krishnan Koil Processing, Signal Engg. Processing 4 59.111.13 Devaraj D Dept. of Arulmigu Kalasalingam Power System Engg. [email protected] Electrical and College of Engg., Electronics Krishnan Koil Engg. 5 57.1.140 Anbalagan P Dept. of Coimbatore Institute of Power Systemprotection - Electrical and Technology, Computerapplications Electronics Coimbatore Engg. 6 - Abdullah Khan Dept. of B.S.A. Crescent Engg. Power System Engg. - Electrical and College, Chennai Electronics Engg. 7 - Dharmalingam K Dept. of R.M.D. Engg. College, High Voltage Engg. - Electrical and Gummidipondi Electronics Engg. 8 - Paranjothi S R Dept. of Rajalakshmi Engg. Electrical Engg. [email protected] Electrical and College, Chennai Electronics Engg. 9 PhD./2003 Uma G Dept. of College of Engg., Anna ElectricalEngg. [email protected] Electrical and University, Chennai Electronics Engg. 10 59.101.04 Vanaja Ranjan P Dept. of College of Engg., Anna Instrumentation Engg. [email protected] Electrical and University, Chennai Anddigital Electronics Signalprocessing Engg. 11 58.101.04 Kumidini Devi R P Dept. of College of Engg., Anna Power System Engg. -

Tamil Nadu H2

Annexure – H 2 Notice for appointment of Regular / Rural Retail Outlet Dealerships IOCL proposes to appoint Retail Outlet dealers in the State of Tamil Nadu as per following details: Name of location Estimated Minimum Dimension (in Finance to be Fixed Fee / monthly Type of Mode of Security Sl. No Revenue District Type of RO Category M.)/Area of the site (in Sq. arranged by the Minimum Sales Site* Selection Deposit M.). * applicant Bid amount Potential # 1 2 3 4 5 6 7 8 9a 9b 10 11 12 (Regular/Rural) (SC/SC CC (CC/DC/CFS) Frontage Depth Area Estimated Estimated (Draw of Rs. in Lakhs Rs. in 1/SC PH/ST/ST working fund Lots/Bidding) Lakhs CC 1/ST capital required PH/OBC/OBC requireme for CC 1/OBC nt for developme PH/OPEN/OPE operation nt of N CC 1/OPEN of RO Rs. in infrastruct CC 2/OPEN Lakhs ure at RO PH) Rs. in Lakhs 1 Alwarpet Chennai Regular 150 SC CFS 20 20 400 0 0 Draw of Lots 0 3 2 Andavar Nagar to Choolaimedu, Periyar Pathai Chennai Regular 150 SC CFS 20 20 400 0 0 Draw of Lots 0 3 3 Anna Nagar Chennai Regular 200 Open CC 20 20 400 25 10 Bidding 30 5 4 Anna Nagar 2nd Avenue Main Road Chennai Regular 200 SC CFS 20 20 400 0 0 Draw of Lots 0 3 5 Anna Salai, Teynampet Chennai Regular 250 SC CFS 20 20 400 0 0 Draw of Lots 0 3 6 Arunachalapuram to Besant nagar, Besant ave Road Chennai Regular 150 SC CFS 20 20 400 0 0 Draw of Lots 0 3 7 Ashok Nagar to Kodambakam power house Chennai Regular 150 SC CFS 20 20 400 0 0 Draw of Lots 0 3 8 Ashok Pillar to Arumbakkam Metro Chennai Regular 200 Open DC 13 14 182 25 60 Draw of Lots 15 5 9 Ayanavaram -

Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu

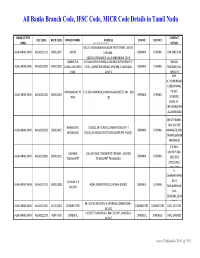

All Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu NAME OF THE CONTACT IFSC CODE MICR CODE BRANCH NAME ADDRESS CENTRE DISTRICT BANK www.Padasalai.Net DETAILS NO.19, PADMANABHA NAGAR FIRST STREET, ADYAR, ALLAHABAD BANK ALLA0211103 600010007 ADYAR CHENNAI - CHENNAI CHENNAI 044 24917036 600020,[email protected] AMBATTUR VIJAYALAKSHMIPURAM, 4A MURUGAPPA READY ST. BALRAJ, ALLAHABAD BANK ALLA0211909 600010012 VIJAYALAKSHMIPU EXTN., AMBATTUR VENKATAPURAM, TAMILNADU CHENNAI CHENNAI SHANKAR,044- RAM 600053 28546272 SHRI. N.CHANDRAMO ULEESWARAN, ANNANAGAR,CHE E-4, 3RD MAIN ROAD,ANNANAGAR (WEST),PIN - 600 PH NO : ALLAHABAD BANK ALLA0211042 600010004 CHENNAI CHENNAI NNAI 102 26263882, EMAIL ID : CHEANNA@CHE .ALLAHABADBA NK.CO.IN MR.ATHIRAMIL AKU K (CHIEF BANGALORE 1540/22,39 E-CROSS,22 MAIN ROAD,4TH T ALLAHABAD BANK ALLA0211819 560010005 CHENNAI CHENNAI MANAGER), MR. JAYANAGAR BLOCK,JAYANAGAR DIST-BANGLAORE,PIN- 560041 SWAINE(SENIOR MANAGER) C N RAVI, CHENNAI 144 GA ROAD,TONDIARPET CHENNAI - 600 081 MURTHY,044- ALLAHABAD BANK ALLA0211881 600010011 CHENNAI CHENNAI TONDIARPET TONDIARPET TAMILNADU 28522093 /28513081 / 28411083 S. SWAMINATHAN CHENNAI V P ,DR. K. ALLAHABAD BANK ALLA0211291 600010008 40/41,MOUNT ROAD,CHENNAI-600002 CHENNAI CHENNAI COLONY TAMINARASAN, 044- 28585641,2854 9262 98, MECRICAR ROAD, R.S.PURAM, COIMBATORE - ALLAHABAD BANK ALLA0210384 641010002 COIIMBATORE COIMBATORE COIMBOTORE 0422 2472333 641002 H1/H2 57 MAIN ROAD, RM COLONY , DINDIGUL- ALLAHABAD BANK ALLA0212319 NON MICR DINDIGUL DINDIGUL DINDIGUL -

SNO APP.No Name Contact Address Reason 1 AP-1 K

SNO APP.No Name Contact Address Reason 1 AP-1 K. Pandeeswaran No.2/545, Then Colony, Vilampatti Post, Intercaste Marriage certificate not enclosed Sivakasi, Virudhunagar – 626 124 2 AP-2 P. Karthigai Selvi No.2/545, Then Colony, Vilampatti Post, Only one ID proof attached. Sivakasi, Virudhunagar – 626 124 3 AP-8 N. Esakkiappan No.37/45E, Nandhagopalapuram, Above age Thoothukudi – 628 002. 4 AP-25 M. Dinesh No.4/133, Kothamalai Road,Vadaku Only one ID proof attached. Street,Vadugam Post,Rasipuram Taluk, Namakkal – 637 407. 5 AP-26 K. Venkatesh No.4/47, Kettupatti, Only one ID proof attached. Dokkupodhanahalli, Dharmapuri – 636 807. 6 AP-28 P. Manipandi 1stStreet, 24thWard, Self attestation not found in the enclosures Sivaji Nagar, and photo Theni – 625 531. 7 AP-49 K. Sobanbabu No.10/4, T.K.Garden, 3rdStreet, Korukkupet, Self attestation not found in the enclosures Chennai – 600 021. and photo 8 AP-58 S. Barkavi No.168, Sivaji Nagar, Veerampattinam, Community Certificate Wrongly enclosed Pondicherry – 605 007. 9 AP-60 V.A.Kishor Kumar No.19, Thilagar nagar, Ist st, Kaladipet, Only one ID proof attached. Thiruvottiyur, Chennai -600 019 10 AP-61 D.Anbalagan No.8/171, Church Street, Only one ID proof attached. Komathimuthupuram Post, Panaiyoor(via) Changarankovil Taluk, Tirunelveli, 627 761. 11 AP-64 S. Arun kannan No. 15D, Poonga Nagar, Kaladipet, Only one ID proof attached. Thiruvottiyur, Ch – 600 019 12 AP-69 K. Lavanya Priyadharshini No, 35, A Block, Nochi Nagar, Mylapore, Only one ID proof attached. Chennai – 600 004 13 AP-70 G. -

CHENNAI PPN LIST of HOSPITALS PIN S No HOSPITAL NAME Address CITY STATE CODE 1 Abhijay Hospital (P) Ltd

CHENNAI PPN LIST OF HOSPITALS PIN S No HOSPITAL NAME Address CITY STATE CODE 1 Abhijay Hospital (P) Ltd. NO.22/2,E.S.I HOSPITAL ROAD,PERAVALLUR Chennai Tamilnadu 600011 2 Aditya Hospital NO.7,BARNBAY ROAD,KILPAUK Chennai Tamilnadu 600010 3 Amma Hospital # 1,SOWRASTRA NAGAR7TH STREET Chennai Tamilnadu 600094 4 Ammayi Eye Hospital NEW # 80 7TH AVENUE, ASHOK NAGAR Chennai Tamilnadu 600083 5 Anand Hospital #201, KAMARAJ SALAI,,MANALI MANALI Chennai Tamilnadu 600068 6 Apollo Hospital ( T.H.Road-Chennai) #645,T.H.ROAD,TONDIARPET Chennai Tamilnadu 600081 7 Appasamy Medicare Centre Pvt Ltd 23-25 FRIENDS AVENUE ARUMBAKKAM,ARUMBAKKAM Chennai Tamilnadu 600106 8 Athipathi Hospital And Research Center PLOT NO 1 100 FT RD TANNI NAGAR,VELACHARY Chennai Tamilnadu 600042 9 B M Hospitals 36 5TH MAIN ROAD THILLAI GANGA,NAGARCHEENAI Chennai Tamilnadu 600061 10 Billroth Hospital Limited #43, LAKSHMI TAKIS ROAD, SHENOY NAGAR Chennai Tamilnadu 600030 NO.28. CATHEDRAL GARDEN 11 Brs Hospital Pvt.Ltd Chennai Tamilnadu 600034 ROADCATHEDRAL,GARDENSROAD 12 Billroth Hospitals - Ra Puram #52, 2ND MAIN ROAD, RAJA ANNAMALAI PURAM Chennai Tamilnadu 600028 15 DR RADHAKRISHNAN SALAI MYLAPORE NEXT,TO CITY 13 C.S.I. Kalyani General Hospital Chennai Tamilnadu 600004 CENTRE 14 Christudas Orthopaedic Speciality Hospital #9.DURAISWAMY NGR. I.A.F. ROAD Chennai Tamilnadu 600059 #327MUTHURANGAM 15 Deepam Hospital ROADTAMBARAM(WEST),KANCHIPURAM WEST Chennai Tamilnadu 600045 TAMBARAM 16 Chennai Meenakshi Multispeciality Hospital Ltd. # 148,LUZ CHURCH ROAD,MALAPORE Chennai Tamilnadu 600004 Hariharan Diabetes And Heartcare Hospitals Pvt 17 24826 29TH STREET NANGANALLUR,NANGANALLUR Chennai Tamilnadu 600061 Ltd 18 Dr Agarwal'S Eye Hospital Ltd No.222,TTK Road, Alwarpet Chennai Tamilnadu 600086 19 Dr.Rabindrans Healthcare Centre (P)Ltd. -

Tamil Nadu Government Gazette

© [Regd. No. TN/CCN/467/2012-14. GOVERNMENT OF TAMIL NADU [R. Dis. No. 197/2009. 2013 [Price: Rs. 54.80 Paise. TAMIL NADU GOVERNMENT GAZETTE PUBLISHED BY AUTHORITY No. 41] CHENNAI, WEDNESDAY, OCTOBER 23, 2013 Aippasi 6, Vijaya, Thiruvalluvar Aandu–2044 Part VI—Section 4 Advertisements by private individuals and private institutions CONTENTS PRIVATE ADVERTISEMENTS Pages Change of Names .. 2893-3026 Notice .. 3026-3028 NOTICE NO LEGAL RESPONSIBILITY IS ACCEPTED FOR THE PUBLICATION OF ADVERTISEMENTS REGARDING CHANGE OF NAME IN THE TAMIL NADU GOVERNMENT GAZETTE. PERSONS NOTIFYING THE CHANGES WILL REMAIN SOLELY RESPONSIBLE FOR THE LEGAL CONSEQUENCES AND ALSO FOR ANY OTHER MISREPRESENTATION, ETC. (By Order) Director of Stationery and Printing. CHANGE OF NAMES 43888. My son, D. Ramkumar, born on 21st October 1997 43891. My son, S. Antony Thommai Anslam, born on (native district: Madurai), residing at No. 4/81C, Lakshmi 20th March 1999 (native district: Thoothukkudi), residing at Mill, West Colony, Kovilpatti, Thoothukkudi-628 502, shall Old No. 91/2, New No. 122, S.S. Manickapuram, Thoothukkudi henceforth be known as D. RAAMKUMAR. Town and Taluk, Thoothukkudi-628 001, shall henceforth be G. DHAMODARACHAMY. known as S. ANSLAM. Thoothukkudi, 7th October 2013. (Father.) M. v¯ð¡. Thoothukkudi, 7th October 2013. (Father.) 43889. I, S. Salma Banu, wife of Thiru S. Shahul Hameed, born on 13th September 1975 (native district: Mumbai), 43892. My son, G. Sanjay Somasundaram, born residing at No. 184/16, North Car Street, on 4th July 1997 (native district: Theni), residing Vickiramasingapuram, Tirunelveli-627 425, shall henceforth at No. 1/190-1, Vasu Nagar 1st Street, Bank be known as S SALMA.