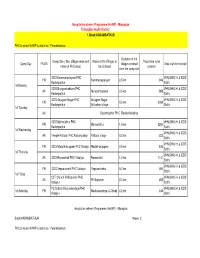

Study on Para-Transit in Chennai

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

List of Village Panchayats in Tamil Nadu District Code District Name

List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 1 Kanchipuram 1 Kanchipuram 1 Angambakkam 2 Ariaperumbakkam 3 Arpakkam 4 Asoor 5 Avalur 6 Ayyengarkulam 7 Damal 8 Elayanarvelur 9 Kalakattoor 10 Kalur 11 Kambarajapuram 12 Karuppadithattadai 13 Kavanthandalam 14 Keelambi 15 Kilar 16 Keelkadirpur 17 Keelperamanallur 18 Kolivakkam 19 Konerikuppam 20 Kuram 21 Magaral 22 Melkadirpur 23 Melottivakkam 24 Musaravakkam 25 Muthavedu 26 Muttavakkam 27 Narapakkam 28 Nathapettai 29 Olakkolapattu 30 Orikkai 31 Perumbakkam 32 Punjarasanthangal 33 Putheri 34 Sirukaveripakkam 35 Sirunaiperugal 36 Thammanur 37 Thenambakkam 38 Thimmasamudram 39 Thilruparuthikundram 40 Thirupukuzhi List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 41 Valathottam 42 Vippedu 43 Vishar 2 Walajabad 1 Agaram 2 Alapakkam 3 Ariyambakkam 4 Athivakkam 5 Attuputhur 6 Aymicheri 7 Ayyampettai 8 Devariyambakkam 9 Ekanampettai 10 Enadur 11 Govindavadi 12 Illuppapattu 13 Injambakkam 14 Kaliyanoor 15 Karai 16 Karur 17 Kattavakkam 18 Keelottivakkam 19 Kithiripettai 20 Kottavakkam 21 Kunnavakkam 22 Kuthirambakkam 23 Marutham 24 Muthyalpettai 25 Nathanallur 26 Nayakkenpettai 27 Nayakkenkuppam 28 Olaiyur 29 Paduneli 30 Palaiyaseevaram 31 Paranthur 32 Podavur 33 Poosivakkam 34 Pullalur 35 Puliyambakkam 36 Purisai List of Village Panchayats in Tamil Nadu District Code District Name Block Code Block Name Village Code Village Panchayat Name 37 -

Particulars of Some Temples of Kerala Contents Particulars of Some

Particulars of some temples of Kerala Contents Particulars of some temples of Kerala .............................................. 1 Introduction ............................................................................................... 9 Temples of Kerala ................................................................................. 10 Temples of Kerala- an over view .................................................... 16 1. Achan Koil Dharma Sastha ...................................................... 23 2. Alathiyur Perumthiri(Hanuman) koil ................................. 24 3. Randu Moorthi temple of Alathur......................................... 27 4. Ambalappuzha Krishnan temple ........................................... 28 5. Amedha Saptha Mathruka Temple ....................................... 31 6. Ananteswar temple of Manjeswar ........................................ 35 7. Anchumana temple , Padivattam, Edapalli....................... 36 8. Aranmula Parthasarathy Temple ......................................... 38 9. Arathil Bhagawathi temple ..................................................... 41 10. Arpuda Narayana temple, Thirukodithaanam ................. 45 11. Aryankavu Dharma Sastha ...................................................... 47 12. Athingal Bhairavi temple ......................................................... 48 13. Attukkal BHagawathy Kshethram, Trivandrum ............. 50 14. Ayilur Akhileswaran (Shiva) and Sri Krishna temples ........................................................................................................... -

Thiruvallur District

DISTRICT DISASTER MANAGEMENT PLAN FOR 2017 TIRUVALLUR DISTRICT tmt.E.sundaravalli, I.A.S., DISTRICT COLLECTOR TIRUVALLUR DISTRICT TAMIL NADU 2 COLLECTORATE, TIRUVALLUR 3 tiruvallur district 4 DISTRICT DISASTER MANAGEMENT PLAN TIRUVALLUR DISTRICT - 2017 INDEX Sl. DETAILS No PAGE NO. 1 List of abbreviations present in the plan 5-6 2 Introduction 7-13 3 District Profile 14-21 4 Disaster Management Goals (2017-2030) 22-28 Hazard, Risk and Vulnerability analysis with sample maps & link to 5 29-68 all vulnerable maps 6 Institutional Machanism 69-74 7 Preparedness 75-78 Prevention & Mitigation Plan (2015-2030) 8 (What Major & Minor Disaster will be addressed through mitigation 79-108 measures) Response Plan - Including Incident Response System (Covering 9 109-112 Rescue, Evacuation and Relief) 10 Recovery and Reconstruction Plan 113-124 11 Mainstreaming of Disaster Management in Developmental Plans 125-147 12 Community & other Stakeholder participation 148-156 Linkages / Co-oridnation with other agencies for Disaster 13 157-165 Management 14 Budget and Other Financial allocation - Outlays of major schemes 166-169 15 Monitoring and Evaluation 170-198 Risk Communications Strategies (Telecommunication /VHF/ Media 16 199 / CDRRP etc.,) Important contact Numbers and provision for link to detailed 17 200-267 information 18 Dos and Don’ts during all possible Hazards including Heat Wave 268-278 19 Important G.Os 279-320 20 Linkages with IDRN 321 21 Specific issues on various Vulnerable Groups have been addressed 322-324 22 Mock Drill Schedules 325-336 -

Ambattur Assembly Tamil Nadu Factbook

Editor & Director Dr. R.K. Thukral Research Editor Dr. Shafeeq Rahman Compiled, Researched and Published by Datanet India Pvt. Ltd. D-100, 1st Floor, Okhla Industrial Area, Phase-I, New Delhi- 110020. Ph.: 91-11- 43580781, 26810964-65-66 Email : [email protected] Website : www.electionsinindia.com Online Book Store : www.datanetindia-ebooks.com Report No. : AFB/TN-008-0619 ISBN : 978-93-5313-704-5 First Edition : January, 2018 Third Updated Edition : June, 2019 Price : Rs. 11500/- US$ 310 © Datanet India Pvt. Ltd. All rights reserved. No part of this book may be reproduced, stored in a retrieval system or transmitted in any form or by any means, mechanical photocopying, photographing, scanning, recording or otherwise without the prior written permission of the publisher. Please refer to Disclaimer at page no. 167 for the use of this publication. Printed in India No. Particulars Page No. Introduction 1 Assembly Constituency - (Vidhan Sabha) at a Glance | Features of Assembly 1-2 as per Delimitation Commission of India (2008) Location and Political Maps Location Map | Boundaries of Assembly Constituency - (Vidhan Sabha) in 2 District | Boundaries of Assembly Constituency under Parliamentary 3-9 Constituency - (Lok Sabha) | Ward-wise Winner Parties- 2019, 2016, 2014, 2011 and 2009 Administrative Setup 3 District | Sub-district | Towns | Villages | Inhabited Villages | Uninhabited 10 Villages | Village Panchayat | Intermediate Panchayat Demographics 4 Population | Households | Rural/Urban Population | Ward by Population Size -

6D Bus Time Schedule & Line Route

6D bus time schedule & line map 6D Foreshore Estate View In Website Mode The 6D bus line (Foreshore Estate) has 3 routes. For regular weekdays, their operation hours are: (1) Foreshore Estate: 5:00 AM - 9:00 PM (2) Thiruvanmiyur: 4:45 AM - 9:40 PM (3) Tollgate: 4:55 AM - 9:55 PM Use the Moovit App to ƒnd the closest 6D bus station near you and ƒnd out when is the next 6D bus arriving. Direction: Foreshore Estate 6D bus Time Schedule 29 stops Foreshore Estate Route Timetable: VIEW LINE SCHEDULE Sunday 5:00 AM - 9:00 PM Monday 5:00 AM - 9:00 PM Tollgate Tuesday 5:00 AM - 9:00 PM Cross Road Wednesday 5:00 AM - 9:00 PM Lakshmi Kovil Thursday 5:00 AM - 9:00 PM Tondiarpet Friday 5:00 AM - 9:00 PM Tondiarpet Cholera Hospital Saturday 5:00 AM - 9:00 PM Agasthiya Theatre Washermenpet 6D bus Info Sir Thiyagaraya College Direction: Foreshore Estate Stops: 29 Trip Duration: 40 min Maharani Theatre Line Summary: Tollgate, Cross Road, Lakshmi Kovil, Tondiarpet, Tondiarpet Cholera Hospital, Agasthiya Pandian Theatre Theatre, Washermenpet, Sir Thiyagaraya College, Maharani Theatre, Pandian Theatre, Cemetery Road, Cemetery Road Rsrm Hospital, Royapuram, Royampuram Railway Station, Clive Battery, Chennai Beach, Parrys Corner, Rsrm Hospital Reserve Bank Of India, Secretariat, Island Ground, Anna Square Bus Terminal, Marina Beach, Kannagi Royapuram Statue, Ice House, Queen Mary's College (Q.M.C.), North Terminus Road, Chennai Light House, Santhome Church, Santhome P.O, Pattinampakkam/Foreshore Estate Royampuram Railway Station Clive Battery Chennai Beach -

Camp Day FN/AN Camp Site ( Site, Village Name and Name of PHC Area)

Hospital on wheels Programme (HoWP) - Microplan Thiruvallur Health District 1.Block:KADAMBATHUR PHC to which HoWP is attached : Perambakkam Distance of the Camp Site ( Site, Village name and Name of the Villages to Population to be Camp Day FN/AN villages covered Area staff to involved name of PHC area) be Covered covered from the camp site ICDS Kamavarpalayam PHC VHN,SHN, HI & ICDS FN Kammavarpalyam 0.5 km 946 Kadampathur Staffs 1st Monday ICDS Nungambakkam PHC VHN,SHN, HI & ICDS AN Nungambakkam 0.5 km 988 Kadampathur Staffs ICDS Anjugam Nagar PHC Anjugam Nagar, VHN,SHN, HI & ICDS FN 0.5 km 2360 Kadampathur Adikathur village Staffs 1st Tuesday AN Kadambathur PHC Review Meeting ICDS Mellnalathur PHC VHN,SHN, HI & ICDS FN Mellnalathur 1.0 km 3264 Kadampathur Staffs 1st Wednesday VHN,SHN, HI & ICDS AN Temple Pattarai PHC Kadampathur Pattarai village 0.3 km 532 Staffs VHN,SHN, HI & ICDS FN ICDS Madathukuppam PHC Vidaiyur Madathukuppam 0.5 km 510 Staffs 1st Thursday VHN,SHN, HI & ICDS AN ICDS Raman koil PHC Vidaiyur Raman koil 1.0 km 1141 Staffs VHN,SHN, HI & ICDS FN ICDS Veppanchetti PHC Vidaiyur Veppanchettai 0.2 km 494 Staffs 1st Friday CST Church Phillispuram PHC VHN,SHN, HI & ICDS AN Phillispuram 0.2 km 455 Vidaiyur Staffs PU School Madurakandigai PHC VHN,SHN, HI & ICDS 1st Saturday FN Madurakandigai & Chenji 0.2 km 345 Vidaiyur Staffs Hospital on wheels Programme (HoWP) - Microplan Block:KADAMBATHUR Week: 2 PHC to which HoWP is attached : Perambakkam Distance of the Camp Site ( Site, Village name and Name of the Villages to Population -

SNO APP.No Name Contact Address Reason 1 AP-1 K

SNO APP.No Name Contact Address Reason 1 AP-1 K. Pandeeswaran No.2/545, Then Colony, Vilampatti Post, Intercaste Marriage certificate not enclosed Sivakasi, Virudhunagar – 626 124 2 AP-2 P. Karthigai Selvi No.2/545, Then Colony, Vilampatti Post, Only one ID proof attached. Sivakasi, Virudhunagar – 626 124 3 AP-8 N. Esakkiappan No.37/45E, Nandhagopalapuram, Above age Thoothukudi – 628 002. 4 AP-25 M. Dinesh No.4/133, Kothamalai Road,Vadaku Only one ID proof attached. Street,Vadugam Post,Rasipuram Taluk, Namakkal – 637 407. 5 AP-26 K. Venkatesh No.4/47, Kettupatti, Only one ID proof attached. Dokkupodhanahalli, Dharmapuri – 636 807. 6 AP-28 P. Manipandi 1stStreet, 24thWard, Self attestation not found in the enclosures Sivaji Nagar, and photo Theni – 625 531. 7 AP-49 K. Sobanbabu No.10/4, T.K.Garden, 3rdStreet, Korukkupet, Self attestation not found in the enclosures Chennai – 600 021. and photo 8 AP-58 S. Barkavi No.168, Sivaji Nagar, Veerampattinam, Community Certificate Wrongly enclosed Pondicherry – 605 007. 9 AP-60 V.A.Kishor Kumar No.19, Thilagar nagar, Ist st, Kaladipet, Only one ID proof attached. Thiruvottiyur, Chennai -600 019 10 AP-61 D.Anbalagan No.8/171, Church Street, Only one ID proof attached. Komathimuthupuram Post, Panaiyoor(via) Changarankovil Taluk, Tirunelveli, 627 761. 11 AP-64 S. Arun kannan No. 15D, Poonga Nagar, Kaladipet, Only one ID proof attached. Thiruvottiyur, Ch – 600 019 12 AP-69 K. Lavanya Priyadharshini No, 35, A Block, Nochi Nagar, Mylapore, Only one ID proof attached. Chennai – 600 004 13 AP-70 G. -

Notification for the Posts of Gramin Dak Sevaks Cycle – Iii/2020-2021 Tamilnadu Circle

NOTIFICATION FOR THE POSTS OF GRAMIN DAK SEVAKS CYCLE – III/2020-2021 TAMILNADU CIRCLE STC/12-GDSONLINE/2020 DATED 01.09.2020 Applications are invited by the respective engaging authorities as shown in the annexure ‘I’against each post, from eligible candidates for the selection and engagement to the following posts of Gramin Dak Sevaks. I. Job Profile:- (i) BRANCH POSTMASTER (BPM) The Job Profile of Branch Post Master will include managing affairs of Branch Post Office, India Posts Payments Bank ( IPPB) and ensuring uninterrupted counter operation during the prescribed working hours using the handheld device/Smartphone/laptop supplied by the Department. The overall management of postal facilities, maintenance of records, upkeep of handheld device/laptop/equipment ensuring online transactions, and marketing of Postal, India Post Payments Bank services and procurement of business in the villages or Gram Panchayats within the jurisdiction of the Branch Post Office should rest on the shoulders of Branch Postmasters. However, the work performed for IPPB will not be included in calculation of TRCA, since the same is being done on incentive basis.Branch Postmaster will be the team leader of the Branch Post Office and overall responsibility of smooth and timely functioning of Post Office including mail conveyance and mail delivery. He/she might be assisted by Assistant Branch Post Master of the same Branch Post Office. BPM will be required to do combined duties of ABPMs as and when ordered. He will also be required to do marketing, organizing melas, business procurement and any other work assigned by IPO/ASPO/SPOs/SSPOs/SRM/SSRM and other Supervising authorities. -

Containment Area Details

TIRUVALLUR DISTRICT CONTAINMENT AREA DETAILS Name of the Sl.No Hotspot area Containment Zone Taluk 1 Tiruvallur Pattialpettai PUNNAPAKKAM PULLARAMBAKKAM THIRUPATCHUR PALLIARAIKUPPAM PIRIYANKUPPAM SELAI IKKADU KAKKALUR KALIYANAKUPPAM THANDALAM THANNEERKULAM THOZHUR PUTLUR ADIGATHUR VENGATHUR MELNALLATHUR TIRUVALLUR – A TIRUVALLUR – B (Pungathur) PERUMBAKKAM PERIYAKUPPAM 2 AVADI No.102, TNHB Avadi AVADI MUNICIPALITY (PART) Corporation VELLANUR (PART) THANDARAI (PART) VILINJIYAMBAKKAM AMBATTUR (PART) AVADI PALERIPATTU AYAPPAKKAM PARUTHIPATTU KANNAPALAYAM VAYALANALLUR (PART) MELPAKKAM SUNDARACHOLAVARAM KOLADI VEERARAGAVAPURAM SENNEERKUPPAM 3 Gummidipoondi Kavarapettai PALESWARANKANDIGAI (Telugu Colony Road, Opposite Panchayat Office) ENADIMELPAKKAM NANGPALLAM GUMMIDIPOONDI (NEW) PART VERKADU GURUVATTUCHERI APLAVARAM PARANAMBEDU ARASUR (PART) SOMBATTU THANDALACHERI KIL MUDALAMBEDU KILIKKODI KATTAVOOR (PART) ANNAPPANAICKENKUPPAM (PART) MEL MUDALAMBEDU THIRUPPAIR KANAKALAVALLIPURAM PONDAVAKKAM (PART) SEUNDAPURAM ELIAMBEDU SEVITTUPANAPAKKAM PUDUVOYAL PONNERI (PART) VAIRAVANKUPPAM VADAKKANALLUR DURANALLUR 4 Gummidipoondi Arambakkam NAIDUKUPPAM ARAMBAKKAM POOVALAI 5 Ponneri 1.Ariyanvoyal, KANIAMBAKKAM (PART) 2.Minjur Town KADAMANJERI VAYALUR (PART) MERATTOOR DEVADANAM (PART) THINAIPAKKAM THOTTAKADU ANUPPAMAPATTU (PART) VELLAMPAKKAM NEIDAVOYAL ARIYANVOYAL NALUR VANNIPAKKAM (PART) KOLLATTI NAYAR (PART) MADIYUR VAZHUIGAIMEDU SEEMAPURAM ATHIPATTU (PART) PERIAMULLAVOYAL CHINNAMULLAVOYAL VALLUR (PART) 6 Gummidipoondi Gummidipoondi NATHAM (PART) (GNT -

Tamil Nadu Sustainable Urban Development Project Final EA for SWD to Selected Areas of Coc

Tamil Nadu Sustainable Urban Development Project Final EA for SWD to selected areas of CoC Public Disclosure Authorized Tamil Nadu Sustainable Urban Development Project (TNSUDP) Storm Water Drainage Project for the Selected Areas of Chennai Corporation Public Disclosure Authorized Tamil Nadu Sustainable Urban Development Project Public Disclosure Authorized Final Environmental Assessment Report Public Disclosure Authorized January 2015 Storm Water Drains Department, Corporation of Chennai 1 Tamil Nadu Sustainable Urban Development Project Final EA for SWD to selected areas of CoC Executive Summary 1. INTRODUCTION 1. Government of Tamil Nadu has proposed to implement the World Bank supported Tamil Nadu Sustainable Urban Development program (TNSUDP) to improve the delivery of urban services. The provision of Storm Water Drains to selected areas of Corporation of Chennai is one of the sub-projects proposed to be implemented by the Corporation of Chennai (CoC). This component is coordinated by Government of Tamil Nadu with Tamil Nadu Urban Infrastructure Financial Services Ltd. (TNUIFSL), Chennai as the fund Manager. This sub project is proposed to be implemented along the roadsides and canals and doesn’t involve any Land Acquisition and required land is owned by the Corporation of Chennai. 2. PROJECT DESCRIPTION 2. The Storm Water Drainage project for the selected areas of Corporation of Chennai proposed to be taken up under the TNSUDP involves construction of storm water drains and canals in the project area. This sub project proposed to be implemented in the 4 Zones of the CoC. The total length of the drains to be constructed is about 270.33 kilometres including the 11.05 km length in the canals. -

Occurrence of Microfungi As Litter Colonizers and Endophytes in Varied Plant Species from the Western Ghats Forests, Goa, India

Mycosphere 4 (3): 567–582 (2013) ISSN 2077 7019 www.mycosphere.org Article Mycosphere Copyright © 2013 Online Edition Doi 10.5943/mycosphere/4/3/10 Occurrence of microfungi as litter colonizers and endophytes in varied plant species from the Western Ghats forests, Goa, India D’Souza MA* and Bhat DJ1 * Department of Botany, Dhempe College of Arts & Science, Miramar, Goa-403 002, India Email: [email protected] 1Department of Botany, Goa University, Goa-403 206, India D’Souza MA, Bhat DJ 2013 – Occurrence of microfungi as litter colonizers and endophytes in varied plant species from the Western Ghats forests, Goa, India. Mycosphere 4(3), 567–582, Doi 10.5943/mycosphere/4/3/10 Abstract In this study 30 widely distributed plant species from the Western Ghat forest in Goa were randomly selected and were studied with regard to their fungal association as endophytes and litter colonizers. This effort resulted in the recovery of more than 6500 isolates of microfungi which were assignable to 675 species of fungi belonging to 275 genera which included properly recognized Mucorales(1), Ascomycetes (18), Hyphomycetous asexual fungi (289), Coelomycetous asexual fungi (22) and undetermined taxa (77), besides a sizable number of non-sporulating forms (268). Species of endophytes (53) and litter colonizers (77) were selected for enzyme studies. Ten taxa occurred both as endophytes and litter colonizers. Endophytes and litter colonizers showed different enzyme profiles indicating that habit and habitat dictated enzyme activity. Several recovered fungi were new to science and some have already been described as new species and are elaborated here in this paper. -

000.3Rd IMM Cover Page

SOUTH ASIA CO-OPERATIVE ENVIRONMENT PROGRAMME SOUTH ASIAN SEAS PROGRAMME SOUTH ASIAN SEAS PROGRAMME 3rd Intergovernmental Meeting of Ministers Thimphu, Bhutan 26th August 2005 REPORT OF THE THIRD MINISTERIAL MEETING OF THE SOUTH ASIAN SEAS PROGRAMME SOUTH ASIAN SEAS PROGRAMME REPORT OF THE THIRD INTERGOVERNMENTAL MINISTERIAL MEETING Para No. CONTENTS Page No. 1 Introduction 1 2 Attendance 1 3 Inauguration 1 4 Election of Office Bearers 2 5 Agenda 2 6 Statement by Heads of the Delegations 2 7 Other Statements 2 Presentation of the Report of the Meeting of the National Focal 8 2 Poinsts by the Rapporteur Endorsement of Recommendations agreed upon at Meeting of 9 2 National Focal Points A Institutional 3 B Project & Programme Matters 3 C Financial 4 10 Adoption of the Report 5 11 Concluding Session 6 SOUTH ASIAN SEAS PROGRAMME Third Intergovernmental Meeting of Ministers (IMM) 26th August 2005 Thimphu, Bhutan LIST OF ANNEXES ANNEX PAGE TITLE NO NO I List of Participants 7 II Inaugural Address - Hon A. H. M Fowzie, MP, Minister of Environment & Natural Resources, Government of Sri 11 Lanka Welcome Address - Dr. A. A. Boaz , Director General, III 13 SACEP IV Agenda 15 V Country Statement by Mr. Jafar Ahmed Chowdhury, Secretary, Ministry of Environment & Forests, Government 16 of the People’s Republic of Bangladesh VI Country Statement – Government of India 18 VII Country Statement by Hon. Ahmed Abdullah Minister for Environment, Energy and Water 20 Republic of Maldives VIII Country Statement by Hon. A.H.M. Fowzie, MP Minister of Environment & Natural Resources, 22 Government of Sri Lanka Statement by Mr.