Annual Report 2011 03

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Religion in China BKGA 85 Religion Inchina and Bernhard Scheid Edited by Max Deeg Major Concepts and Minority Positions MAX DEEG, BERNHARD SCHEID (EDS.)

Religions of foreign origin have shaped Chinese cultural history much stronger than generally assumed and continue to have impact on Chinese society in varying regional degrees. The essays collected in the present volume put a special emphasis on these “foreign” and less familiar aspects of Chinese religion. Apart from an introductory article on Daoism (the BKGA 85 BKGA Religion in China prototypical autochthonous religion of China), the volume reflects China’s encounter with religions of the so-called Western Regions, starting from the adoption of Indian Buddhism to early settlements of religious minorities from the Near East (Islam, Christianity, and Judaism) and the early modern debates between Confucians and Christian missionaries. Contemporary Major Concepts and religious minorities, their specific social problems, and their regional diversities are discussed in the cases of Abrahamitic traditions in China. The volume therefore contributes to our understanding of most recent and Minority Positions potentially violent religio-political phenomena such as, for instance, Islamist movements in the People’s Republic of China. Religion in China Religion ∙ Max DEEG is Professor of Buddhist Studies at the University of Cardiff. His research interests include in particular Buddhist narratives and their roles for the construction of identity in premodern Buddhist communities. Bernhard SCHEID is a senior research fellow at the Austrian Academy of Sciences. His research focuses on the history of Japanese religions and the interaction of Buddhism with local religions, in particular with Japanese Shintō. Max Deeg, Bernhard Scheid (eds.) Deeg, Max Bernhard ISBN 978-3-7001-7759-3 Edited by Max Deeg and Bernhard Scheid Printed and bound in the EU SBph 862 MAX DEEG, BERNHARD SCHEID (EDS.) RELIGION IN CHINA: MAJOR CONCEPTS AND MINORITY POSITIONS ÖSTERREICHISCHE AKADEMIE DER WISSENSCHAFTEN PHILOSOPHISCH-HISTORISCHE KLASSE SITZUNGSBERICHTE, 862. -

Identification of Clematidis Radix Et Rhizoma and Its Adulterants by Core Haplotype Based on the ITS Sequences

Identification of Clematidis radix et Rhizoma and its adulterants by core haplotype based on the ITS sequences Yi-Mei Zang1, Ya Gao2, Ying Liu3, Chun-Sheng Liu3 1Beijing City University, Beijing, China 2Chengde Center for Disease Prevention and Contral, Chengde, China 3School of Chinese Pharmacy, Beijing University of Chinese Medicine, Beijing, China Corresponding author: Chun Sheng Liu E-mail: [email protected] Genet. Mol. Res. 17 (2): gmr16039905 Received February 27, 2018 Accepted April 07, 2018 Published April 15, 2018 DOI: http://dx.doi.org/10.4238/gmr16039905 Copyright © 2018 The Authors. This is an open-access article distributed under the terms of the Creative Commons Attribution ShareAlike (CC BY-SA) 4.0 License. ABSTRACT. To develop a method to identify Clematidis radix et Rhizoma using sequence similarity and sequence-specific genetic polymorphisms based on the ITS sequences. DNA was extracted from leaves of Clematis mandshurica Rupr and C. hexapetala using a DNA extraction kit. ITS sequences were amplified by PCR, and analyzed in Contig Express, DNAman, and MEGA 5.0. The core haplotype was determined, and similarities between the core and other haplotypes were calculated. In total, 138 ITS sequences of C. mandshurica were obtained with a length of 611 bp. The similarity threshold between C. mandshurica and counterfeit species was 99%. Using specific mutation sites, we could identify C. chinensis, C. hexapetala, and C. mandshurica rapidly and accurately. A new DNA-based method has been established to rapidly and accurately identify Clematidis radix et Rhizoma. Key words: Clematidis radix et Rhizoma; Core haplotype; Identification threshold; Mutation sites INTRODUCTION Clematidis radix et Rhizoma is the dry radix and rhizome of Clematis chinensis Osbeck, C. -

Shengjing Bank Co., Ltd.* (A Joint Stock Company Incorporated in the People's Republic of China with Limited Liability) Stock Code: 02066 Annual Report Contents

Shengjing Bank Co., Ltd.* (A joint stock company incorporated in the People's Republic of China with limited liability) Stock Code: 02066 Annual Report Contents 1. Company Information 2 8. Directors, Supervisors, Senior 68 2. Financial Highlights 4 Management and Employees 3. Chairman’s Statement 7 9. Corporate Governance Report 86 4. Honours and Awards 8 10. Report of the Board of Directors 113 5. Management Discussion and 9 11. Report of the Board of Supervisors 121 Analysis 12. Social Responsibility Report 124 5.1 Environment and Prospects 9 13. Internal Control 126 5.2 Development Strategies 10 14. Independent Auditor’s Report 128 5.3 Business Review 11 15. Financial Statements 139 5.4 Financial Review 13 16. Notes to the Financial Statements 147 5.5 Business Overview 43 17. Unaudited Supplementary 301 5.6 Risk Management 50 Financial Information 6. Significant Events 58 18. Organisational Chart 305 7. Change in Share Capital and 60 19. The Statistical Statements of All 306 Shareholders Operating Institution of Shengjing Bank 20. Definition 319 * Shengjing Bank Co., Ltd. is not an authorised institution within the meaning of the Banking Ordinance (Chapter 155 of the Laws of Hong Kong), not subject to the supervision of the Hong Kong Monetary Authority, and not authorised to carry on banking and/or deposit-taking business in Hong Kong. COMPANY INFORMATION Legal Name in Chinese 盛京銀行股份有限公司 Abbreviation in Chinese 盛京銀行 Legal Name in English Shengjing Bank Co., Ltd. Abbreviation in English SHENGJING BANK Legal Representative ZHANG Qiyang Authorised Representatives ZHANG Qiyang and ZHOU Zhi Secretary to the Board of Directors ZHOU Zhi Joint Company Secretaries ZHOU Zhi and KWONG Yin Ping, Yvonne Registered and Business Address No. -

Table of Codes for Each Court of Each Level

Table of Codes for Each Court of Each Level Corresponding Type Chinese Court Region Court Name Administrative Name Code Code Area Supreme People’s Court 最高人民法院 最高法 Higher People's Court of 北京市高级人民 Beijing 京 110000 1 Beijing Municipality 法院 Municipality No. 1 Intermediate People's 北京市第一中级 京 01 2 Court of Beijing Municipality 人民法院 Shijingshan Shijingshan District People’s 北京市石景山区 京 0107 110107 District of Beijing 1 Court of Beijing Municipality 人民法院 Municipality Haidian District of Haidian District People’s 北京市海淀区人 京 0108 110108 Beijing 1 Court of Beijing Municipality 民法院 Municipality Mentougou Mentougou District People’s 北京市门头沟区 京 0109 110109 District of Beijing 1 Court of Beijing Municipality 人民法院 Municipality Changping Changping District People’s 北京市昌平区人 京 0114 110114 District of Beijing 1 Court of Beijing Municipality 民法院 Municipality Yanqing County People’s 延庆县人民法院 京 0229 110229 Yanqing County 1 Court No. 2 Intermediate People's 北京市第二中级 京 02 2 Court of Beijing Municipality 人民法院 Dongcheng Dongcheng District People’s 北京市东城区人 京 0101 110101 District of Beijing 1 Court of Beijing Municipality 民法院 Municipality Xicheng District Xicheng District People’s 北京市西城区人 京 0102 110102 of Beijing 1 Court of Beijing Municipality 民法院 Municipality Fengtai District of Fengtai District People’s 北京市丰台区人 京 0106 110106 Beijing 1 Court of Beijing Municipality 民法院 Municipality 1 Fangshan District Fangshan District People’s 北京市房山区人 京 0111 110111 of Beijing 1 Court of Beijing Municipality 民法院 Municipality Daxing District of Daxing District People’s 北京市大兴区人 京 0115 -

World Bank Document

Procurement Plan for Liaoning Medium City Infrastructure Project (LMCIP) in China Project information: Public Disclosure Authorized Public Disclosure Authorized Country: China Borrower: The People’s Republic of China. Project Name: Liaoning Medium City Infrastructure Project (LMCIP) Loan/Credit No.: 4831-CHA Project ID: P099992 Project Implementing Agency (PIA): Liaoning Urban Construction and Renewal Project Office (LUCRPO) in Liaoning Province and city PMOs in cities of Fushun, Benxi, Liaoyang, Jinzhou, Panjin, and Dengta . Bank’s approval Date of the procurement Plan [Original:During Loan negotiation in May 2006; Revision 1:…] Date of General Procurement Notice: April 3, 2006 Period covered by this procurement plan: 2006-2009 Public Disclosure Authorized Public Disclosure Authorized The prior review thresholds for LMCI Project: Table A Civil Works Goods Consultant Consultant services services Firm Individual Above USD 5 million 500K 200K 50K In addition, the Bank will review the first contract procured under each category. The procurement method thresholds for LMCI Project : Public Disclosure Authorized Public Disclosure Authorized Table B Civil Goods Consultant services Works Public Disclosure Authorized Public Disclosure Authorized ICB >15 >500K >300K(short list not more than million 2 from a country) NCB advertisement >2 >300K <300K (shortlist can be only on a national million from national consultants) newspaper NCB advertisement <2 <300K >200K: QCBS on a provincial million <200K: CQS or Individual newspaper Consultant (IC) Shopping -

Study on GIS Visualization in Evaluation of the Human Living Environment in Shenyang-Dalian Urban Agglomeration

Hindawi Publishing Corporation Scientifica Volume 2016, Article ID 7462832, 10 pages http://dx.doi.org/10.1155/2016/7462832 Research Article Study on GIS Visualization in Evaluation of the Human Living Environment in Shenyang-Dalian Urban Agglomeration Kang Hou, Jieting Zhou, Xuxiang Li, and Shengbin Ge School of Human Settlements and Civil Engineering, Xi’an Jiaotong University, Xi’an 710049, China Correspondence should be addressed to Xuxiang Li; [email protected] Received 7 December 2015; Revised 1 March 2016; Accepted 31 March 2016 Academic Editor: Francisco Ayuga Copyright © 2016 Kang Hou et al. This is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited. Analysis of human living environmental quality of Shenyang-Dalian urban agglomerations has important theoretical and practical significance in rapid development region. A lot of investigations have been carried for Shenyang-Dalian urban agglomerations, including 38 counties. Based on the carrying capacity of resources, natural and socioeconomic environmental factors and regional changes of human living environmental evaluation are analyzed with the application of geographic information systems (GIS) software. By using principal component analysis (PCA) model and natural breaks classification (NBC) method, the evaluation results are divided into five categories. The results show thatuman theh living environmental evaluation (HLEE) indexes of Dalian, Shenyang, and Liaoyang are higher than other counties. Among these counties, the human living environmental evaluation (HLEE) indexes of coastal counties are significantly higher than inland counties. The range of the human living environmental evaluation index in most of the study area is at III, IV,and V levels, accounting for 80.01%. -

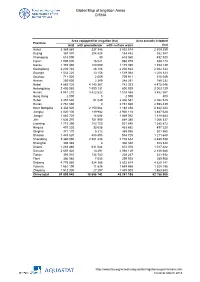

Global Map of Irrigation Areas CHINA

Global Map of Irrigation Areas CHINA Area equipped for irrigation (ha) Area actually irrigated Province total with groundwater with surface water (ha) Anhui 3 369 860 337 346 3 032 514 2 309 259 Beijing 367 870 204 428 163 442 352 387 Chongqing 618 090 30 618 060 432 520 Fujian 1 005 000 16 021 988 979 938 174 Gansu 1 355 480 180 090 1 175 390 1 153 139 Guangdong 2 230 740 28 106 2 202 634 2 042 344 Guangxi 1 532 220 13 156 1 519 064 1 208 323 Guizhou 711 920 2 009 709 911 515 049 Hainan 250 600 2 349 248 251 189 232 Hebei 4 885 720 4 143 367 742 353 4 475 046 Heilongjiang 2 400 060 1 599 131 800 929 2 003 129 Henan 4 941 210 3 422 622 1 518 588 3 862 567 Hong Kong 2 000 0 2 000 800 Hubei 2 457 630 51 049 2 406 581 2 082 525 Hunan 2 761 660 0 2 761 660 2 598 439 Inner Mongolia 3 332 520 2 150 064 1 182 456 2 842 223 Jiangsu 4 020 100 119 982 3 900 118 3 487 628 Jiangxi 1 883 720 14 688 1 869 032 1 818 684 Jilin 1 636 370 751 990 884 380 1 066 337 Liaoning 1 715 390 783 750 931 640 1 385 872 Ningxia 497 220 33 538 463 682 497 220 Qinghai 371 170 5 212 365 958 301 560 Shaanxi 1 443 620 488 895 954 725 1 211 648 Shandong 5 360 090 2 581 448 2 778 642 4 485 538 Shanghai 308 340 0 308 340 308 340 Shanxi 1 283 460 611 084 672 376 1 017 422 Sichuan 2 607 420 13 291 2 594 129 2 140 680 Tianjin 393 010 134 743 258 267 321 932 Tibet 306 980 7 055 299 925 289 908 Xinjiang 4 776 980 924 366 3 852 614 4 629 141 Yunnan 1 561 190 11 635 1 549 555 1 328 186 Zhejiang 1 512 300 27 297 1 485 003 1 463 653 China total 61 899 940 18 658 742 43 241 198 52 -

Annual Report Is Published

Contents 1. Company Information 2 8. Directors, Supervisors, Senior 73 2. Financial Highlights 4 Management and Employees 3. Chairman’s Statement 7 9. Corporate Governance Report 90 4. Honours and Awards 8 10. Report of the Board of Directors 117 5. Management Discussion and 9 11. Report of the Board of Supervisors 125 Analysis 12. Social Responsibility Report 128 5.1 Analysis of Overall 9 13. Internal Control 130 Operations 14. Independent Auditor’s Report 132 5.2 Financial Review 11 15. Financial Statements 142 5.3 Business Overview 44 16. Notes to the Financial Statements 150 5.4 Risk Management 52 17. Unaudited Supplementary 302 5.5 Environmental Outlook and 58 Financial Information Development Strategy 18. Organisational Chart 306 6. Significant Events 60 19. The Statistical Statements of All 307 7. Change in Share Capital and 64 Operating Institution of Shengjing Shareholders Bank 20. Definition 323 * Shengjing Bank Co., Ltd. is not an authorised institution within the meaning of the Banking Ordinance (Chapter 155 of the Laws of Hong Kong), not subject to the supervision of the Hong Kong Monetary Authority, and not authorised to carry on banking and/or deposit-taking business in Hong Kong. Chapter 1 Company Information COMPANY INFORMATION Legal Name in Chinese 盛京銀行股份有限公司 Abbreviation in Chinese 盛京銀行 Legal Name in English Shengjing Bank Co., Ltd. Abbreviation in English SHENGJING BANK Legal Representative QIU Huofa Authorised Representatives QIU Huofa and ZHOU Zhi Secretary to the Board of Directors ZHOU Zhi Joint Company Secretaries -

China – Liaoning Province - Dengta County – Prisons – Detention Centres

Refugee Review Tribunal AUSTRALIA RRT RESEARCH RESPONSE Research Response Number: CHN33628 Country: China Date: 5 August 2008 Keywords: China – Liaoning Province - Dengta County – Prisons – Detention centres This response was prepared by the Research & Information Services Section of the Refugee Review Tribunal (RRT) after researching publicly accessible information currently available to the RRT within time constraints. This response is not, and does not purport to be, conclusive as to the merit of any particular claim to refugee status or asylum. This research response may not, under any circumstance, be cited in a decision or any other document. Anyone wishing to use this information may only cite the primary source material contained herein. Questions Please provide information on reform through labour and detention centres or jails with names similar to Dengta Prison that were operating as places of detention or imprisonment in July 1999 to June 2000. RESPONSE Please provide information on reform through labour and detention centres or jails with names similar to Dengta Prison that were operating as places of detention or imprisonment in July 1999 to June 2000. A prison in Dengta City in Liaoning Province is listed in the Laogai Handbook: 2005-2006. The Handbook indicates that the prison in Dengta was established in 1949, is known both as the Huazi Prison and as the Liaoyang No.1 Prison and also operates as a commercial enterprise known as the Xinsheng Cement Plant. The Handbook indicates that there are more than sixty Laogai (reform through labour) camps in Liaoning Province as well as detention centres at the village, township and county levels. -

Global Factory List As of August 3Rd, 2020

Global Factory List as of August 3rd, 2020 Target is committed to providing increased supply chain transparency. To meet this objective, Target publishes a list of all tier one factories that produce our owned-brand products, national brand products where Target is the importer of record, as well as tier two apparel textile mills and wet processing facilities. Target partners with its vendors and suppliers to maintain an accurate factory list. The list below represents factories as of August 3rd, 2020. This list is subject to change and updates will be provided on a quarterly basis. Factory Name State/Province City Address AMERICAN SAMOA American Samoa Plant Pago Pago 368 Route 1,Tutuila Island ARGENTINA Angel Estrada Cla. S.A, Buenos Aires Ciudad de Buenos Aires Ruta Nacional N 38 Km. 1,155,Provincia de La Rioja AUSTRIA Tiroler Glashuette GmbH Werk: Schneegattern Oberosterreich Lengau Kobernauserwaldstrase 25, BAHRAIN WestPoint Home Bahrain W.L.L. Al Manamah (Al Asimah) Riffa Building #1912, Road # 5146, Block 951,South Alba Industrial Area, Askar BANGLADESH Campex (BD) Limited Chittagong zila Chattogram Building-FS SFB#06, Sector#01, Road#02, Chittagong Export Processing Zone,, Canvas Garments (Pvt.) Ltd Chittagong zila Chattogram 301, North Baizid Bostami Road,,Nasirabad I/A, Canvas Building Chittagong Asian Apparels Chittagong zila Chattogram 132 Nasirabad Indstrial Area,Chattogram Clifton Cotton Mills Ltd Chittagong zila Chattogram CDA plot no-D28,28-d/2 Char Ragmatia Kalurghat, Clifton Textile Chittagong zila Chattogram 180 Nasirabad Industrial Area,Baizid Bostami Road Fashion Watch Limited Chittagong zila Chattogram 1363/A 1364 Askarabad, D.T. Road,Doublemoring, Chattogram, Bangladesh Fortune Apparels Ltd Chittagong zila Chattogram 135/142 Nasirabad Industrial Area,Chattogram KDS Garment Industries Ltd. -

Minimum Wage Standards in China August 11, 2020

Minimum Wage Standards in China August 11, 2020 Contents Heilongjiang ................................................................................................................................................. 3 Jilin ............................................................................................................................................................... 3 Liaoning ........................................................................................................................................................ 4 Inner Mongolia Autonomous Region ........................................................................................................... 7 Beijing......................................................................................................................................................... 10 Hebei ........................................................................................................................................................... 11 Henan .......................................................................................................................................................... 13 Shandong .................................................................................................................................................... 14 Shanxi ......................................................................................................................................................... 16 Shaanxi ...................................................................................................................................................... -

Liaoning Small Cities and Towns Development Demonstration Sector

LIAONING CITIES AND TOWNS SYSTEM PLAN COMPOSITIVE REPORT Selected parts (2003-2020) The People’s Government of Liaoning Province April 2003 2 Social Economic and Civil Development Strategies 2.1 Social Economic Development Strategy According to the master plan of central government, China will start the implementation of the third stage. The modernization will become true in the middle of 21st century. Considering the development process of Liaoning, the reconstruction of the old industrial base will be completed basically in 2005 and the socialism market economy system will be established basically too in 2010. The way of economic growth will be changed totally and GDP will be doubled comparing with the growth in 2000. Up to 2020, Shenyang, Dalian and Anshan will achieve basic modernization in 2020. Guiding Ideology The Development is still the main point and the reform must be continued. The relationship between reform, development and stability should be coordinated well. Institutional and technical innovation is always emphasized. The living standard of people is tried to be improved. The healthy, sustainable and coordinative development of social economy should be ensured. Overall Strategy The development is the main subject and the economic restructuring is one important line. The reform and scientific development will provide good foundation for improving the living standard of people. The government will support the development of education and scientific research and try to achieve sustainable development in order to promote the overall social economic development and keep the stability of the society. One Main Subject Development is the main subject. The government will focus on promoting the healthy and sustainable development of economy and try to improve the socialism market economic structure further.