Case Fsl Cory

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Antitrust Implications of Computer Reservations Systems (CRS's) Derek Saunders

Journal of Air Law and Commerce Volume 51 | Issue 1 Article 5 1985 The Antitrust Implications of Computer Reservations Systems (CRS's) Derek Saunders Follow this and additional works at: https://scholar.smu.edu/jalc Recommended Citation Derek Saunders, The Antitrust Implications of Computer Reservations Systems (CRS's), 51 J. Air L. & Com. 157 (1985) https://scholar.smu.edu/jalc/vol51/iss1/5 This Comment is brought to you for free and open access by the Law Journals at SMU Scholar. It has been accepted for inclusion in Journal of Air Law and Commerce by an authorized administrator of SMU Scholar. For more information, please visit http://digitalrepository.smu.edu. THE ANTITRUST IMPLICATIONS OF COMPUTER RESERVATIONS SYSTEMS (CRS's) DEREK SAUNDERS THE PASSAGE of the Airline Deregulation Act' dramat- ically altered the airline industry. Market forces, rather than government agencies, 2 began to regulate the indus- try. The transition, however, has not been an easy one. Procedures and relationships well suited to a regulated in- dustry are now viewed as outdated, onerous, and even anticompetitive. The current conflict over carrier-owned computer res- ervation systems (CRS's) represents one instance of these problems.3 The air transportation distribution system re- lies heavily on the use of CRS's, particularly since deregu- lation and the resulting increase in airline activity. 4 One I Pub. L. No. 95-504, 92 Stat. 1705 (codified at 49 U.S.C.A. § 1401 (Supp. 1984)). 2 Competitive Market Investigation, CAB Docket 36,595 (Dec. 16, 1982) at 3. For a discussion of deregulation in general and antitrust problems specifically, see Beane, The Antitrust Implications of Airline Deregulation, 45 J. -

Credit Travel Rewards Catalog Available, You Will Be Advised to Make an Alternate Selection Or May Return Your Points to Your Account

ScoreCard® Bonus Point Program Rules 4) Reservations shall also be subject to airline availability for advance gift shop purchases, gambling, beauty salon/barber shop/spa services, 1. As provided in these rules (“Rules”), account holders (“You” or “you”) earn (1) Point in the ScoreCard® fare category seating , non-refundable type tickets for the travel dates laundry, photographs, email, internet and fax, etc.) are the responsibility Program (“Program”) for every dollar in qualifying purchases that you: (i) charge to an eligible credit card specified. 5) ScoreCard travel services reserves the right to choose the of the Cardholder. 4) Cruises are non-refundable, non-cancelable and non- account covered by the Program (“Account”); and (ii) that appears on your statement during the Program Period. Purchases that are returned do not qualify for Points. No Points are earned for finance charges, fees, airline and routing on which to reserve and ticket Cardholders. transferable. Once redeemed, Bonus Points may not be added back to your cash advances, convenience checks, ATM withdrawals, foreign transaction currency conversion charges or ScoreCard account. 5) Please check with ScoreCard travel representatives Universal First Class/Business Class Ticket insurance charges posted to your account. Contact your financial institution (“Sponsor”) for full details on the Item Points Item # Item Points Item # for any documentation requirements or other restrictions associated Program Period dates during which you are eligible to earn Points. Cardholder is responsible for any overages above the maximum ticket with cruises. It is the guest’s responsibility to obtain appropriate 2. Points can be used to order the merchandise/travel awards (“Award(s)”) available in the current Program. -

Validating Carrier, Interline, and GSA

Validating Carrier, Interline, and GSA Developer Administration Guide August 2014 W Q2 © 2012-2014, Sabre Inc. All rights reserved. This documentation is the confidential and proprietary intellectual property of Sabre. Any unauthorized use, reproduction, preparation of derivative works, performance, or display of this document, or software represented by this document, without the express written permission of Sabre Inc. is strictly prohibited. Sabre and the Sabre logo design and Sabre Travel Network and the Sabre Travel Network logo design are trademarks and/or service marks of an affiliate of Sabre. All other trademarks, service marks, and trade names are owned by their respective companies. DOCUMENT REVISION INFORMATION The following information is to be included with all versions of the document. Project Project Name Number Prepared by Date Prepared Revised by Date Revised Revision Reason Edition No. Revised by Date Revised Revision Reason Edition No. Revised by Date Revised Revision Reason Edition No. • • • Table of Contents 1 Getting Started 1.1 Introduction .................................................................................................................................................... 1-1 1.2 Summary of Changes .................................................................................................................................... 1-1 1.3 About This Guide ........................................................................................................................................... 1-2 2 -

08-06-2021 Airline Ticket Matrix (Doc 141)

Airline Ticket Matrix 1 Supports 1 Supports Supports Supports 1 Supports 1 Supports 2 Accepts IAR IAR IAR ET IAR EMD Airline Name IAR EMD IAR EMD Automated ET ET Cancel Cancel Code Void? Refund? MCOs? Numeric Void? Refund? Refund? Refund? AccesRail 450 9B Y Y N N N N Advanced Air 360 AN N N N N N N Aegean Airlines 390 A3 Y Y Y N N N N Aer Lingus 053 EI Y Y N N N N Aeroflot Russian Airlines 555 SU Y Y Y N N N N Aerolineas Argentinas 044 AR Y Y N N N N N Aeromar 942 VW Y Y N N N N Aeromexico 139 AM Y Y N N N N Africa World Airlines 394 AW N N N N N N Air Algerie 124 AH Y Y N N N N Air Arabia Maroc 452 3O N N N N N N Air Astana 465 KC Y Y Y N N N N Air Austral 760 UU Y Y N N N N Air Baltic 657 BT Y Y Y N N N Air Belgium 142 KF Y Y N N N N Air Botswana Ltd 636 BP Y Y Y N N N Air Burkina 226 2J N N N N N N Air Canada 014 AC Y Y Y Y Y N N Air China Ltd. 999 CA Y Y N N N N Air Choice One 122 3E N N N N N N Air Côte d'Ivoire 483 HF N N N N N N Air Dolomiti 101 EN N N N N N N Air Europa 996 UX Y Y Y N N N Alaska Seaplanes 042 X4 N N N N N N Air France 057 AF Y Y Y N N N Air Greenland 631 GL Y Y Y N N N Air India 098 AI Y Y Y N N N N Air Macau 675 NX Y Y N N N N Air Madagascar 258 MD N N N N N N Air Malta 643 KM Y Y Y N N N Air Mauritius 239 MK Y Y Y N N N Air Moldova 572 9U Y Y Y N N N Air New Zealand 086 NZ Y Y N N N N Air Niugini 656 PX Y Y Y N N N Air North 287 4N Y Y N N N N Air Rarotonga 755 GZ N N N N N N Air Senegal 490 HC N N N N N N Air Serbia 115 JU Y Y Y N N N Air Seychelles 061 HM N N N N N N Air Tahiti 135 VT Y Y N N N N N Air Tahiti Nui 244 TN Y Y Y N N N Air Tanzania 197 TC N N N N N N Air Transat 649 TS Y Y N N N N N Air Vanuatu 218 NF N N N N N N Aircalin 063 SB Y Y N N N N Airlink 749 4Z Y Y Y N N N Alaska Airlines 027 AS Y Y Y N N N Alitalia 055 AZ Y Y Y N N N All Nippon Airways 205 NH Y Y Y N N N N Amaszonas S.A. -

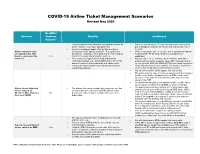

COVID-19 Airline Ticket Management Scenarios Revised May 2020

COVID-19 Airline Ticket Management Scenarios Revised May 2020 Do ARC’s Scenario Systems Benefits Challenges Support? • Ticket number is easily identified, stored and retrieved by • Tracking unused tickets: To track unused tickets, agents may airline, agency, corporation and passenger. pay a third party, maintain an internal tool or manually retrieve • Agency exchanges happen often so this scenario is the data. Airline maintains value already part of the agency workflow. The agency can • Airlines may not be able to extend e-ticket expiration (being able on original ticket. (The perform the exchange in their GDS and the ticketing data to maintain the ET for longer than their standard ticket ticket is considered the Yes is fed to their mid- and back-office systems. expiration). voucher.) • ARC’s systems support this method and allow for • Agency may need to exchange ticket manually. GDS auto- refunds/exchanges (e.g., ticket validity) up to 39 months pricing tool may not be available. Note: ARC understands that based on carrier e-ticket expiration and validity rules. as of early June 2020, the GDSs/ATPCO have made updates to • Tracing the end-to-end life of the transaction is simple allow auto-pricing tools to be utilized. This ability is dependent (old and new tickets). on the airline being able to extend ticket expiration. • Not all airlines and/or GDSs support this functionality. • The airline may not have a consistent way to notify the customer that the value has been transferred to an EMD, as the travel agency’s e-mail address (instead of the passenger’s) may be stored in the PNR • The airline-issued EMD is not reported to ARC, so ARC does not recognize the airline-issued EMD for future exchanges. -

Procedure 20335E: Air Transportation

Controller’s Office Procedure Procedure 20335e: Air Transportation Rules and procedures for the purchase of air travel services, both on public carriers and charter aircraft are based on the requirement that all expenditures of the University must be necessary and reasonable and that the mechanism of payment must be in accordance with state and university procedures. A. Rates Public transportation rates must not exceed those for tourist/coach class accommodations. Business class or premium coach seating such as comfort plus air travel may be granted for international travel under the following circumstances: When the cost does not exceed the lowest available tourist/coach fare. For travel to Western Europe if the business meeting is conducted within three hours of landing. For transoceanic, intercontinental trips involving flight time of more than eight consecutive hours. If the traveler pays the difference. Business class for rail travel may be granted under the following circumstances: When it does not cost more than the lowest available tourist/coach fare (comparison must be attached to the travel reimbursement request). When reserved coach seats are not offered on the route. If the traveler pays the difference. Reimbursement for first class travel is prohibited. Travelers purchasing first class airline tickets will not be reimbursed for the expense from public funds. Travel Protection Insurance for airline tickets is not an allowable expense. Internet Purchases - Internet travel users must be careful when procuring airline tickets. The Internet sites often list only a class code and the user should know the following code designations: Tourist/Coach – B H K L Q T U V W Y Business Class – C J First Class – A D E F J P A.1 Fly America Act If international travel is being charged to a Federal grant or contract, then the “Fly America Act” applies. -

Civil Aviation and the Federal Government, 1926-1996 (Washington, DC: Federal Aviation Administration, 1998)

1997-2018 Update to FAA Historical Chronology: Civil Aviation and the Federal Government, 1926-1996 (Washington, DC: Federal Aviation Administration, 1998) 1997 January 2, 1997: The Federal Aviation Administration (FAA) issued an airworthiness directive requiring operators to adopt procedures enabling the flight crew to reestablish control of a Boeing 737 experiencing an uncommanded yaw or roll – the phenomenon believed to have brought down USAir Flight 427 at Pittsburgh, Pennsylvania, in 1994. Pilots were told to lower the nose of their aircraft, maximize power, and not attempt to maintain assigned altitudes. (See August 22, 1996; January 15, 1997.) January 6, 1997: Illinois Governor Jim Edgar and Chicago Mayor Richard Daley announced a compromise under which the city would reopen Meigs Field and operate the airport for five years. After that, Chicago would be free to close the airport. (See September 30, 1996.) January 6, 1997: FAA announced the appointment of William Albee as aircraft noise ombudsman, a new position mandated by the Federal Aviation Reauthorization Act of 1996 (Public Law 104-264). (See September 30, 1996; October 28, 1998.) January 7, 1997: Dredging resumed in the search for clues in the TWA Flight 800 crash. The operation had been suspended in mid-December 1996. (See July 17, 1996; May 4, 1997.) January 9, 1997: A Comair Embraer 120 stalled in snowy weather and crashed 18 miles short of Detroit [Michigan] Metropolitan Airport, killing all 29 aboard. (See May 12, 1997; August 27, 1998.) January 14, 1997: In a conference sponsored by the White House Commission on Aviation Safety and Security and held in Washington, DC, at George Washington University, airline executives called upon the Clinton Administration to privatize key functions of FAA and to install a nonprofit, airline-organized cooperative that would manage security issues. -

Flights (Flights Which Have Not Been Canceled) That Qualify for a Refund Must Be Processed by American Airlines Via the Online Refund Request Form

Schedule Change Introduction General Information Schedule Change-Rule 240/80 or Schedule Irregularity for delayed flights (flights which have not been canceled) that qualify for a refund must be processed by American Airlines via the online refund request form. Travel agents may not process a refund for a non-refundable ticket on a Rule 240/80 for delayed flights (flights which have not been canceled) via their ARC/BSP. If customer requests a refund refer to the Revenue/'Published Fare online Refund Request Form section below. Definitions: Rule 240 Domestic tariff rules which state AA's obligations to our customers when their flights are changed or canceled as a result of Schedule Change(s)/ Irregularities. Rule 240 applies to travel wholly within the 50 U.S., travel between the U.S. and Canada and travel between the U.S. and Puerto Rico /U.S. Virgin Islands. Rule 240 protects all ticketed customers including AAdvantage, AA codeshare and Travel Agents free/reduced rate. AAirpass® tickets should be handled in the same manner as revenue tickets and are considered ticketed at all times. Rule 80 International tariff rules which state AA's obligations to our customers when their flights are changed or canceled as a result of Schedule Change(s)/Irregularities. Rule 80 applies to all international travel except travel between the U.S. and Canada and/or between the U.S. and Puerto Rico /U.S. Virgin Islands. Rule 80 protects all ticketed customers including AAdvantage, AA codeshare and Travel Agents free/reduced rate. AAirpass® tickets should be handled in the same manner as revenue tickets and are considered ticketed at all times. -

Automated Rules and Footnotes

GLOSSARY OF TERMS All rights reserved The information contained in this document is the property of ATPCO. No part of this document may be reproduced, stored in a retrieval system, or transmitted in any form, or by any means; mechanical, photocopying, recording, or otherwise, without the prior written permission of ATPCO. Under the law, copying includes translating into another language or format. Legal action will be taken against any infringement Copyright © 2002 Airline Tariff Publishing Company. All rights reserved. GLOSSARY OF TERMS TERM DEFINITION ACCOMPANIED The passenger traveling at the fare being validated who is required to travel with another passenger. PASSENGER ACCOMPANYING The passenger who is traveling with the passenger on the fare being validated. PASSENGER ACTION The data within this field will be used as data storage, measurement of provisions, or for later matching/ticket (for validation) issuance. These fields are processed after a match is made to the record. ADD-ON An amount used only with specified/published fares for the construction of constructed/unpublished fares. (Also referred to as an arbitrary or proportional fare.) ADULT A person who has reached his/her 12th birthday as of the date of commencement of travel. AREA IATA divides the world into three Areas, also known as Traffic Conferences (TC). These Areas are: Area 1 – Western Hemisphere Area 2 – Europe, Africa, Middle East Area 3 – Asia, Pacific ASSEMBLY A point in the itinerary where the entire qualifying group assembles and commences transportation as a group. POINT ATPCO Fares published within the US/CA or between US and Canada. This also includes travel between US Virgin DOMESTIC FARE Islands and Puerto Rico and US/CA. -

Reimbursement Rates for Air Travel

United States Department of Agriculture Farm and Foreign MAP 15–004 Agricultural Services SUBJECT: Reimbursement Rates for Air Travel under Generic Promotion Foreign Activities Agricultural Service TO: All Market Access Program (MAP) Participants 1400 Independence Ave, SW Stop 1052 Washington, DC ISSUE 20250-1052 The revised MAP regulations were published on May 17, 2012, and became effective beginning with program year 2013. This program notice is being issued to provide clarity regarding the reimbursement rates for air travel under generic promotion activities. Regulations regarding the reimbursement rates for air travel under generic promotion activities are found at 7 CFR 1485.17(c) (8) (ii), (iii), and (iv). These sections read as follows: §1485.17(c)(8)(ii) CCC generally will not reimburse any portion of air travel, including any fees for modifying the originally purchased ticket, in excess of the full fare economy rate or when the MAP Participant fails to notify the Attaché/Counselor in the destination country in advance of the travel, unless the CCC determines it was impractical to provide such notice. If a traveler flies in business class or a different premium class, the basis for reimbursement will be the full fare economy class rate for the same flight and the MAP Participant shall provide documentation establishing such full fare economy class rate to support its reimbursement claim. If economy class is not offered for the same flight or if the traveler flies on a charter flight, the basis for reimbursement will be the average of the full fare economy class rate for flights offered by three different airlines between the same points on the same date and the MAP Participant shall provide documentation establishing such average of the full fare economy class rates to support its reimbursement claim. -

ENRIQUE BELTRANENA Redefining Low-Cost the Mexican Way at Volaris from LONDON to QUIETER ABETTERWAYTOFLY

REGIONALS Why history could LEISURE Lines blur with CARGO Implications for freighter repeat itself at US feeder airlines Europe’s budget brigade fleet as market recovery falters STRATEGY FOR AIRLINE BOARDROOMS WORLDWIDE OCTOBERXXXXXX 20152014 flightglobal.com/airlines INTERVIEW ENRIQUE BELTRANENA Redefining low-cost the Mexican way at Volaris FROM LONDON TO QUIETER ABETTERWAYTOFLY. boeing.com/commercial Boeing commercial airplanes are quieter than ever, significantly reducing noise near airports. They’re also the world’s most fuel-efficient airplanes, cutting greenhouse gas emissions by up to 25%. And the Boeing ecoDemonstrator program is accelerating the development and use of new technologies to further minimize aviation’s environmental footprint around the world. That’s a better way to fly. URXWHVRQOLQHFRP Plan your 2016 Route Map Routes regional events unite aviation professionals ZLWKDPDUNHWVSHFLȴFIRFXV Connect with decision makers dedicated to \RXUUHJLRQDQGFDSWXUHWKHLQWHUHVWRILQȵXHQWLDO LQGXVWU\SOD\HUVWRGHYHORSQHZDLUVHUYLFHV ([FOXVLYHFRPELQDWLRQRHU 5HJLVWHUIRU\RXUVHOHFWHGUHJLRQDOHYHQWV DQG:RUOG5RXWHVE\WKHVW2FWREHU WRWDNHDGYDQWDJHRIGLVFRXQWHGUDWHV 7RUHJLVWHUIRU\RXUFKRVHQUHJLRQDO HYHQWSOHDVHFRPHWRVWDQG1DW :RUOG5RXWHVRUYLVLWURXWHVRQOLQHFRP 5RXWHV$PHULFDV Routes Asia 5RXWHV(XURSH San Juan, Puerto Rico 0DQLOD3KLOLSSLQHV .UDNµZ3RODQG Ȃ)HEUXDU\ Ȃ0DUFK Ȃ$SULO )RUPRUHLQIRUPDWLRQFRQWDFWVDOO\DQQHFROOLQV#XEPFRP CONTENTS VOLUME 31 NUMBER 8 REGIONALS Why history could LEISURE Lines blur with CARGO Implications for freighter repeat itself at US feeder -

Fundamentals of Travel Rules of Thumb to Get You Going… and Keep You on the Road

Fundamentals of Travel Rules of Thumb To Get You Going… and Keep You on the Road Copyright 2007 © Massachusetts Institute of Technology Course Objectives . At the end of this course participants will be able to: . Understand MIT’s Travel policies . Complete travel documents The basic policy guiding travel expense reimbursement is that the individual traveler should neither gain nor loose personal funds as a result of travel assignments, and that these assignments be planned so that their cost will not exceed budgetary limitations. Thus, each traveler is to be fully reimbursed for all necessary and reasonable expenses incurred in connection with travel on Institute business, but should make efforts to keep all expenses at a sensible minimum. The mode of travel considered reasonable is that which provides adequate standards of comfort, convenience, safety and efficiency. TRAVEL WARNINGS http://web.mit.edu/emergency/ Agenda . Introductions . Travel Agencies . Airline ticket policies . Other transportation modes . Cash travel advance policies . Travel Advance Request form . Per diem policies/Request form . Food . Miscellaneous Expense . MIT Hotel Rates . Special Issues . Travel Voucher Form . Diners Club Card Travel Agencies . Direct charge airfare tickets to cost object . Provides all required documentation for the amount and use of the lowest available fare or data to allow segregation of any cost over the lowest available fare . Will not be tripped up by code sharing . Most discounted rail & airfares have been negotiated directly with the airlines by a consortia MIT belongs to . Familiar with MIT policy . CAO receives a monthly cost savings report further documenting the lowest available air fare requirement for federal reimbursement .