Sponsored By

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wacoal Holdings Corp. Fundamental Company

+44 20 8123 2220 [email protected] Wacoal Holdings Corp. Fundamental Company Report Including Financial, SWOT, Competitors and Industry Analysis https://marketpublishers.com/r/W7133F8C68FBEN.html Date: September 2021 Pages: 50 Price: US$ 499.00 (Single User License) ID: W7133F8C68FBEN Abstracts Wacoal Holdings Corp. Fundamental Company Report provides a complete overview of the company’s affairs. All available data is presented in a comprehensive and easily accessed format. The report includes financial and SWOT information, industry analysis, opinions, estimates, plus annual and quarterly forecasts made by stock market experts. The report also enables direct comparison to be made between Wacoal Holdings Corp. and its competitors. This provides our Clients with a clear understanding of Wacoal Holdings Corp. position in the Clothing, Textiles and Accessories Industry. The report contains detailed information about Wacoal Holdings Corp. that gives an unrivalled in-depth knowledge about internal business-environment of the company: data about the owners, senior executives, locations, subsidiaries, markets, products, and company history. Another part of the report is a SWOT-analysis carried out for Wacoal Holdings Corp.. It involves specifying the objective of the company's business and identifies the different factors that are favorable and unfavorable to achieving that objective. SWOT-analysis helps to understand company’s strengths, weaknesses, opportunities, and possible threats against it. The Wacoal Holdings Corp. financial analysis covers the income statement and ratio trend-charts with balance sheets and cash flows presented on an annual and quarterly basis. The report outlines the main financial ratios pertaining to profitability, margin analysis, asset turnover, credit ratios, and company’s long- Wacoal Holdings Corp. -

Management's Discussion and Analysis

FACTS Management’s Discussion and Analysis Wacoal Holdings Corp. and Subsidiaries Financial information contained in this section is based on the consoli- OVERVIEW OF STATUS OF BUSINESS PERFORMANCE, ETC. dated financial statements included in this integrated report, prepared in Status of Financial Position and Operation Results Status accordance with generally accepted accounting principles in the United of Financial Position States (U.S. GAAP). Total assets at the fiscal year ended March 31, 2019 (fiscal 2019) was The Wacoal Group consists of one holding company (the Company), ¥281,767 million, a decrease of ¥16,767 million compared with the end 57 consolidated subsidiaries, and eight equity-method affiliates. The of the previous fiscal year, due to a decrease in investments resulting Wacoal Group manufactures, wholesales, and—for certain products— from a decrease in market value and impairment charges on goodwill. retails women’s foundation garments and lingerie, nightwear, children’s Total liabilities at the end of fiscal 2019 was ¥60,623 million, a underwear, outerwear and sportswear, hosiery, and other textile products. decrease of ¥414 million compared with the end of the previous fiscal Other operations include restaurant businesses, cultural and service- year, due to decreases in trade payables and deferred tax liabilities, related operations, and the construction of interiors for commercial despite an increase in short-term bank loans and a recognition of premises. refund liabilities. Total Wacoal Holdings Corp. shareholders’ equity at the end of fiscal OVERVIEW 2019 was ¥216,494 million, a decrease of ¥16,218 million compared We are a leading designer, manufacturer, and marketer in Japan of with the end of the previous fiscal year, due to cash dividend payments, women’s intimate apparel, with the largest share of the Japanese market repurchase of treasury stock, and decreases in pension liability for foundation garments and lingerie. -

Estta272541 03/17/2009 in the United States Patent And

Trademark Trial and Appeal Board Electronic Filing System. http://estta.uspto.gov ESTTA Tracking number: ESTTA272541 Filing date: 03/17/2009 IN THE UNITED STATES PATENT AND TRADEMARK OFFICE BEFORE THE TRADEMARK TRIAL AND APPEAL BOARD Proceeding 91183558 Party Plaintiff Temple University -- Of the Commonwealth System of Higher Education Correspondence Leslie H Smith Address Liacouras & Smith, LLP 1515 Market Street, Suite 808 Philadelphia, PA 19102 UNITED STATES [email protected] Submission Motion for Summary Judgment Filer's Name Leslie H Smith Filer's e-mail [email protected] Signature /Leslie H Smith/ Date 03/17/2009 Attachments TEMPLE WORKOUT GEAR SJ Motion with Exhibits and Certif of Service.pdf ( 75 pages )(1933802 bytes ) IN THE UNITED STATES PATENT AND TRADEMARK OFFICE BEFORE THE TRADEMARK TRIAL AND APPEAL BOARD In the Matter of Application No. 77/038246 Published in the Official Gazette on December 18, 2007 Temple University – Of The Commonwealth: System of Higher Education, : : Opposer, : Opposition No. 91183558 : v. : : BCW Prints, Inc., : : Applicant. : SUMMARY JUDGMENT MOTION OF OPPOSER TEMPLE UNIVERSITY – OF THE COMMONWEALTH SYSTEM OF HIGHER EDUCATION TABLE OF CONTENTS Page I. INTRODUCTION…………………………………………………………… 2 II. UNDISPUTED FACTS……………………………………………………… 3 III. THE UNDISPUTED FACTS ESTABLISH A LIKELIHOOD OF CONFUSION BETWEEN THE TEMPLE MARKS AND OPPOSER’S TEMPLE WORKOUT GEAR (AND DESIGN) TRADEMARK…………… 7 A. Likelihood of Confusion is a Question of Law Appropriate for Summary Judgment………………………………………………………………….. 7 B. Under the du Pont Test, the Undisputed Facts Establish A Likelihood of Confusion between Temple’s TEMPLE Marks and Opposer’s TEMPLE WORKOUT GEAR (and design) Mark…………………………………… 7 1. The TEMPLE Marks and the TEMPLE WORKOUT GEAR (and design) Mark Are Similar in Appearance, Sound, Connotation, and Commercial Impression………………………… 8 2. -

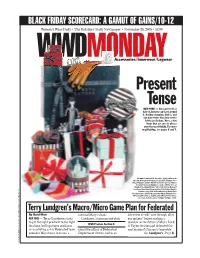

Present Tense NEW YORK — You Can Love It Or Hate It, but You Can’T Get Around It

BLACK FRIDAY SCORECARD: A GAMUT OF GAINS/10-12 WWDWomen’s Wear Daily • The Retailers’MONDAY Daily Newspaper • November 28, 2005 • $2.00 Accessories/Innerwear/Legwear Present Tense NEW YORK — You can love it or hate it, but you can’t get around it. Holiday shopping, that is, and you have fewer than four weeks left to get it done. Here, a few items that are sure to please even the most finicky. For more on gift-giving, see pages 6 and 7. Clockwise from top left: chocolates from La Maison du Chocolat at Bergdorf Goodman, $6 and $17; Tiffany & Co.’s 18k gold bangle, $3,950; Valentino’s leather gloves, $435 at Bergdorf Goodman; Dyptique’s candle, $80 for three at Bergdorf Goodman; Hermès’ silk scarf, $320 at Bergdorf Goodman; Henri Bendel’s snow globe, $48; Sutton Studio’s cashmere scarf, $98 at Bloomingdale’s; Monica Rich Kosann’s frame, $295 at Bergdorf Goodman; Tiffany & Co.’s 18-karat gold necklace, $2,850, and at Bergdorf Goodman, an ornament, $30, and Jar Parfums’ perfume, $765. Terry Lundgren’s Macro/Micro Game Plan for Federated By David Moin national Macy’s chain. interview he will “sort through all of NEW YORK — Terry Lundgren wants Lundgren, chairman and chief our options’’ before making a to get the right products to the right decision on the future of May’s Lord ICSC Preview. Section II. locations, buff up stores and focus & Taylor division and defended the on marketing as his Federated team executive officer of Federated conversion of Chicago’s venerable remakes May stores to create a Department Stores, said in an See Lundgren’s, Page 8 PHOTO BY ROBERT ROXANNE ROBINSON-ESCRIOUT AND SHOSHANNA FISCHHOFF MITRA; STYLED BY 2 WWD, MONDAY, NOVEMBER 28, 2005 WWD.COM New Additions to the Armani Family MILAN — Two new stars are shining in Giorgio WWDMONDAY Armani’s constellation of products: a deluxe watch Armani’s Borgo 21. -

Comparison of Adult Brassier Between Korea and Japan -Based on the Information on the Internet ・

IJCC, V이 . 7, No. 2, 112-122(2004) 36 Comparison of Adult Brassier between Korea and Japan -Based on the Information on the Internet ・ Mi-Sun Joen, Myung-Ja Park and Kyu-Hye Lee* Department of Clothing and Textiles, Hanyang University (Received June 3, 2004 : Accepted November 13, 2004) Abstract A brassier supports and protects breasts and makes a better shape of the upper half of the body through shaping breasts. A brassier, therefore, is recognized as the key underwear for female. Recently, the distri bution structure and channels of the brassiere industry is diversified from conventional type of markets to department stores, convenience stores, and internet shopping mall. Studies on the sales of brassieres via internet, however, is not sufficient even though the market size has been dramatically increased thursdays. The study on the size structure (including the size and the materials fabric of brassieres circulating via internet) is especially rare. Therefore, this study tries to comply with increasing requests of consumers through comparing brassier brands on internet. In depth, this study compares cases of Korea and Japan in terms of availability of website on sales, quality indication like materials and functions, and size. The results indicated that there were three companies in Korea which run a website and make a sale through a website. All three Japanese companies operate a website and make sales on a website as well. In terms of size, Korean companies diversify their size of products in two ways. It varies from A cup to D cup based on cup size, and 65 to 100 according to its entire size. -

Consolidated Business Results for the First Quarter of the Fiscal Year Ending March 31, 2014 [U.S

[Translation] Consolidated Business Results for the First Quarter of the Fiscal Year Ending March 31, 2014 [U.S. GAAP] July 31, 2013 Listed Company: Wacoal Holdings Corp. Stock Exchanges: Tokyo Code Number: 3591 (URL: http://www.wacoalholdings.jp/) Representative: Position: President and Representative Director Name: Yoshikata Tsukamoto For Inquiries: Position: Senior Managing Director Name: Ikuo Otani Tel: +81 (075) 682-1010 Scheduled quarterly report submission date: August 14, 2013 Scheduled dividend payment start date: - Supplementary materials regarding quarterly business results: None Explanatory meeting regarding quarterly business results: None (Amounts less than 1 million yen have been rounded) 1. First Quarter of the Fiscal Year Ending March 31, 2014 (April 1, 2013 – June 30, 2013) (1) Consolidated Business Results (% indicates increase (decrease) from the corresponding period of the previous fiscal year) Net Sales Operating Income Pre-tax Net Income Net Income Attributable to Wacoal Holdings Corp. Millions of Yen % Millions of Yen % Millions of Yen % Millions of Yen % First Quarter ended 47,961 10.6 5,038 27.9 5,575 42.2 3,570 29.7 June 30, 2013 First Quarter ended 43,362 1.1 3,939 (2.8) 3,921 (12.3) 2,752 (1.3) June 30, 2012 (Note) Quarterly comprehensive income: 8,013 million yen (increase of 455.7%) for the first quarter ended June 30, 2013 1,442 million yen (decrease of 58.4%) for the first quarter ended June 30, 2012 Net Income Diluted Net Income Attributable to Attributable to Wacoal Holdings Wacoal Holdings Corp. Per Share Corp. Per Share Yen Yen First Quarter ended 25.35 25.30 June 30, 2013 First Quarter ended 19.54 19.51 June 30, 2012 (2) Consolidated Financial Condition Total Total Total Equity Shareholders’ Total Assets Shareholders’ Shareholders’ (Net Assets) Equity Per Share Equity Equity Ratio Millions of Yen Millions of Yen Millions of Yen % Yen As of June 30, 2013 255,957 192,027 189,787 74.1 1,347.50 As of the end of Fiscal 253,803 188,004 185,840 73.2 1,319.47 Year (March 31, 2013) 2. -

The Cultural Discourses of Breast Cancer Narratives

0/-*/&4637&: *ODPMMBCPSBUJPOXJUI6OHMVFJU XFIBWFTFUVQBTVSWFZ POMZUFORVFTUJPOT UP MFBSONPSFBCPVUIPXPQFOBDDFTTFCPPLTBSFEJTDPWFSFEBOEVTFE 8FSFBMMZWBMVFZPVSQBSUJDJQBUJPOQMFBTFUBLFQBSU $-*$,)&3& "OFMFDUSPOJDWFSTJPOPGUIJTCPPLJTGSFFMZBWBJMBCMF UIBOLTUP UIFTVQQPSUPGMJCSBSJFTXPSLJOHXJUI,OPXMFEHF6OMBUDIFE ,6JTBDPMMBCPSBUJWFJOJUJBUJWFEFTJHOFEUPNBLFIJHIRVBMJUZ CPPLT0QFO"DDFTTGPSUIFQVCMJDHPPE Mammographies Mammographies The Cultural Discourses of Breast Cancer Narratives Mary K. DeShazer The University of Michigan Press Ann Arbor Copyright © by the University of Michigan 2013 All rights reserved This book may not be reproduced, in whole or in part, including illustrations, in any form (beyond that copying permitted by Sections 107 and 108 of the U.S. Copyright Law and except by reviewers for the public press), without written permission from the publisher. Published in the United States of America by The University of Michigan Press Manufactured in the United States of America c Printed on acid- free paper 2016 2015 2014 2013 4 3 2 1 A CIP catalog record for this book is available from the British Library. Library of Congress Cataloging-in- Pu blication Data DeShazer, Mary K. Mammographies : the cultural discourses of breast cancer narratives / Mary K. DeShazer. pages cm Includes bibliographical references and index. ISBN 978- 0- 472- 11882- 3 (cloth : alk. paper) — ISBN 978- 0- 472- 02923- 5 (e- book) 1. Breast—R adiography—Cr oss-c ultural studies. 2. Breast— Imaging—Cr oss-c ultural studies. 3. Ethnicity—H ealth aspects. 4. Transcultural medical care. I. Title. RG493.5.R33D47 2013 618.1'907572— dc23 2013000021 In memory of my beloved friends Lynda Hart Billy McClain Dolly A. McPherson Elizabeth Phillips Acknowledgments Since I could never have written a book about postmillennial representa- tions of breast cancer without the creative visions of the writers, photog- raphers, and scholars whose work I analyze in Mammographies, I must first express my gratitude to them for providing me with inspiration. -

Interfilière Shanghai 2021 第17届上海国际贴身时尚原辅料展

INTERFILIÈRE SHANGHAI 2021 第17届上海国际贴身时尚原辅料展 ——亚太地区首选时尚内衣、运动服及泳装原辅料商贸平台 2021年8月26-27日 上海展览中心 目录 01 展会回顾 03 专业买家 05 媒体 02 04 06 平台概况 展会概况 同期活动 INTERFILIERE INTERFILIERE——全球领先的贴身时尚行业平台 巴黎 纽约 上海 深圳 • 举办专业展会50余年, 服务全球市场 Evolution Guide • 打造领先的产业平台, Evolutio Evolution Guide Evolutio & Color Card 全年提供市场咨询 & Color Card CONNECT S/S F/W n Guide n在线资讯平台 Guide 趋势指南及色卡 趋势指南及色卡 春/夏 秋/冬 • 创立行业大奖,推动产 品创新,培育行业人才 INTERFEEL’ Awards YOUNG LABEL AWARDS 国际贴身时尚原辅料大奖 新晋品牌大赛 3 展会回顾——INTERFILIÈRE SHANGHAI 2019 关键数字 同期活动 8场 10,000m2 论坛/会议 展示面积 5场 150家 时尚流行趋势发 参展商 布 5,000名 10场 专业观众 品牌发布 *以上数字来源于INTERFILIERE SHANGHAI 2019展后报告。 展会回顾——INTERFILIÈRE SHANGHAI 2019 5,000名高端专业观众造访2019展会现场。 专业观众中80%是决策者 采购总监、设计总监、产品研发总监、销售总监、营 销总监、出口业务总监、首席执行官、董事总经理 专业观众来自45个国家 • 82%来自中国和中国香港 • 13%来自亚洲其他国家 • 5%来自亚洲以外国家 专业观众寄语 “展会无疑为中国品牌的发展提供了高端的国际平台。他们高 效和专业的服,让我能够采购理想的产品并与优质的供应商联 系。十分庆幸在这个行业中拥有INTERFILIERE这个专业平台, 总是能够达到我的期望!” ——周滢滢女士, 创始人, ATOG “在过去的7年中,我们的品牌获得了INTERFILIERE的长期 支持,一直在为我们提供许多国际资源以帮助我们成长。” ——刘小璐女士,首席执行官及创始人,内外NEIWAI 展会概况——INTERFILIÈRE SHANGHAI 2021 • 2021年8月26-27日(星期四-星期五) • 上海展览中心(上海市延安中路1000号) • 12,000平方米展示面积,180家参展商 • 致力于打造亚太地区首选时尚内衣、运动服及 泳装原辅料商贸平台 聚焦三大贴身原辅料应用市场 • 贴身时尚行业的风向标,服务中国及亚太市场17年 • 引领行业流行趋势,拓展多元化国内外专业买家 内 衣 运 动 服 泳 装 • 凭借全球网络,帮助优质中国企业进入国际高端市场 我 纺织品设 面料/纤维 蕾丝/刺绣 计/流行趋 们 势 的 专 OEM/ODM 纺织机械 业 辅料/配饰 制造商 及技术 范 畴 高端专业买家邀请 按职务: 时尚内衣品牌观众 • 设计师 • 产品研发 参展商与行业顶尖品牌现场互动 • 原辅料采购 • 企业决策层 泳装品牌观众 按公司类型: • 品牌方 • 品牌代理商 • OEM/ODM制造商 • 采购办事处Buying Office 运动品牌观众 • 进出口贸易商 • B2B电商平台 • 买手店 • 设计院校 • 专业流行趋势机构 • 行业协会 • 新闻传媒 • 投资商 *以上信息来源于INTERFILIERE中国优质买家库。 … 高端专业买家——您更有机会遇到如下优质客户 品牌方 品牌方 -

Rich, Attractive People in Attractive Places Doing Attractive Things

Virginia Commonwealth University VCU Scholars Compass Theses and Dissertations Graduate School 2006 Rich, Attractive People In Attractive Places Doing Attractive Things Tonya Walker Virginia Commonwealth University Follow this and additional works at: https://scholarscompass.vcu.edu/etd Part of the English Language and Literature Commons © The Author Downloaded from https://scholarscompass.vcu.edu/etd/992 This Thesis is brought to you for free and open access by the Graduate School at VCU Scholars Compass. It has been accepted for inclusion in Theses and Dissertations by an authorized administrator of VCU Scholars Compass. For more information, please contact [email protected]. Rich, Attractive People Doing Attractive Things in Attractive Places - A Monologue from Hell - - by Tonya Walker, Master of Fine Arts Candidate Major Director: Tom De Haven, Professor, Department of English Acknowledgement This thesis could not have been completed - completed in the loosest sense of the word - had in not been for the time and involvement of three men. I'd like to thank my mentor David Robbins for his unfailing and passionate disregard of my failings as a writer, my thesis director Tom De Haven for his patient support and stellar suggestions that are easily the best in the book and my husband Philip whose passionate disregard of my failings and patient support are simply the best. Abstract RICH, ATTRACTIVE PEOPLE IN ATTRACTIVE PLACES DOING ATTRACTIVE THINGS By Tonya Walker, M.F.A. A these submitted in partial fulfillment of the requirements for the degree of Master of Fine Arts at Virginia Commonwealth University. Virginia Commonwealth University, 2006 Major Director: Tom De Haven, Professor, Department of English Rich, Attractive People in Attractive Places Doing Attractive Things is a fictional memoir of a dead Manhattan socialite from the 1950's named Sunny Marcus. -

Women with Short Hair Amanda Layne Stephens

Marshall University Marshall Digital Scholar Theses, Dissertations and Capstones 2010 Women with short hair Amanda Layne Stephens Follow this and additional works at: http://mds.marshall.edu/etd Part of the Classics Commons, Comparative Literature Commons, English Language and Literature Commons, and the Feminist, Gender, and Sexuality Studies Commons Recommended Citation Stephens, Amanda Layne, "Women with short hair" (2010). Theses, Dissertations and Capstones. 1075. http://mds.marshall.edu/etd/1075 This Thesis is brought to you for free and open access by Marshall Digital Scholar. It has been accepted for inclusion in Theses, Dissertations and Capstones by an authorized administrator of Marshall Digital Scholar. For more information, please contact [email protected], [email protected]. WOMEN WITH SHORT HAIR A Thesis submitted to The Graduate College of Marshall University In partial fulfillment of the requirements for the degree of Master of Arts Department of English by Amanda Layne Stephens Approved by Dr. Anthony Viola, Ph.D., Committee Chairperson Dr. Jane Hill, Ph.D. Professor Art Stringer, M.F.A. Marshall University May 2010 Keywords: female characters, third-person limited narration, first-person narration, life cycle, repetition, objective correlative, free indirect discourse ii Acknowledgments Without Dr. Anthony Viola, Dr. Jane Hill, and Professor Art Stringer, Women with Short Hair would have never reached its full potential. Dr. Viola provided helpful suggestions during the drafting process and gave me extra time to revise when I needed it, which was often. Dr. Hill pointed out commonalities among my characters and features of my writing style I had not noticed, which helped me understand my collection in new ways. -

The Ne Kpost at Home

SB OP --- KEEP IN NEWARK YOUR MONEY FIR S T THE NE KPOST AT HOME Number 37 The Newark Post, Newark, Delaware, Thursday, December 15, 1949 PRICE FIV E CENTS ;Mho(Ii ts To Hold ~Eyes Left' For Santa! Confusion Exists Over ICouncil To Appoint AnJlual Whi te Gift Fire And Police CallS, Ho k" , S Service Sunday Nite Aetna Officials Report A PM Ins" uccessor Serious confusion exists among r esi- - t ectlug Tuesday Singing By Junior And Senior dents here over the police and fire calls, oITici als of the Aetna Fire Com No Candidates Mentioned As Yet Choirs To Mark Traditional pany disclosed this week. Event At 7 P. M. They issued a warning that grave For Vacant Post; Other harm can r esult if fire and police calls Agenda Items Listed are not placed promptly and accurate- The Annua l White Gifts Christmas Service oc the Newark Methodist · Iy. They advised writing these numbers Appointment of a su cce ~ s or to Coun- Church will be held on this Sunday, ~~:. t~~;T~:tt~: ~II~e t~:i~h~s~e 2~~~~c~0~.~ cilman John S. Hopkins, who resig ned occ. 18, at 7 .p. m. The music will in Newark Police call is: 4801. I' centl y. is expected to highlight the clude Ihe si ngin g of "The Magnificat," In a letter carried on the editorial semi-monthly meeting of the Town 'Nunc Domi ttis," "We Three Kings of page, Charles E. Moore, fire recorder, Council at 8 p. m. on Tuesday. Orient Are," an d a soprano solo. -

MANIS YANG BELUM SUDAH Identitas Dan Subjektivitas Pakaian

PLAGIATPLAGIAT MERUPAKAN MERUPAKAN TINDAKAN TINDAKAN TIDAK TIDAK TERPUJI TERPUJI MANIS YANG BELUM SUDAH Identitas dan Subjektivitas Pakaian Bekas di Yogyakarta T e s i s Untuk memenuhi persyaratan mendapatkan gelar Master Humaniora (M. Hum) pada Program Magister Ilmu Religi dan Budaya, Universitas Sanata Dharma, Yogyakarta Oleh: Wahyu HARJANTO 086322013 Program Magister Ilmu Religi dan Budaya Universitas Sanata Dharma Yogyakarta 2013 PLAGIATPLAGIAT MERUPAKAN MERUPAKAN TINDAKAN TINDAKAN TIDAK TIDAK TERPUJI TERPUJI PLAGIATPLAGIAT MERUPAKAN MERUPAKAN TINDAKAN TINDAKAN TIDAK TIDAK TERPUJI TERPUJI PLAGIATPLAGIAT MERUPAKAN MERUPAKAN TINDAKAN TINDAKAN TIDAK TIDAK TERPUJI TERPUJI PERNYATAAN KEASLIAN TESIS Saya mahasiswa Pascasarjana Program Ilmu Religi dan Budaya, Universitas Sanata Dharma: Nama : Wahyu HARJANTO Nomor Mahasiswa : 086322013 bersama ini, menyatakan dengan sesungguhnya bahwa tesis saya yang berjudul MANIS YANG BELUM SUDAH: Identitas dan Subjektivitas Pakaian Bekas di Yogyakarta adalah karya asli saya dan bukan merupakan tulisan ilmiah karya orang lain atau pihak manapun. Tesis ini tidak memuat karya orang lain atau pihak manapun yang pernah diajukan untuk mendapatkan gelar kesarjanaan pada perguruan tinggi lain. Demikian halnya tema penelitian ini sejauh pengetahuan saya belum pernah dikaji oleh pihak manapun dan disajikan dalam artikel ilmiah, jurnal, tesis, disertasi atau karya ilmiah apapun. Apabila terdapat kesamaan tema dengan tulisan atau karya orang lain, tulisan atau karya tersebut semata-mata hanya dipakai sebagai bahan