Tracing: a General Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Beyond Unconscionability: the Case for Using "Knowing Assent" As the Basis for Analyzing Unbargained-For Terms in Standard Form Contracts

Beyond Unconscionability: The Case for Using "Knowing Assent" as the Basis for Analyzing Unbargained-for Terms in Standard Form Contracts Edith R. Warkentinet I. INTRODUCTION People who sign standard form contracts' rarely read them.2 Coun- sel for one party (or one industry) generally prepare standard form con- tracts for repetitive use in consecutive transactions.3 The party who has t Professor of Law, Western State University College of Law, Fullerton, California. The author thanks Western State for its generous research support, Western State colleague Professor Phil Merkel for his willingness to read this on two different occasions and his terrifically helpful com- ments, Whittier Law School Professor Patricia Leary for her insightful comments, and Professor Andrea Funk for help with early drafts. 1. Friedrich Kessler, in a pioneering work on contracts of adhesion, described the origins of standard form contracts: "The development of large scale enterprise with its mass production and mass distribution made a new type of contract inevitable-the standardized mass contract. A stan- dardized contract, once its contents have been formulated by a business firm, is used in every bar- gain dealing with the same product or service .... " Friedrich Kessler, Contracts of Adhesion- Some Thoughts About Freedom of Contract, 43 COLUM. L. REV. 628, 631-32 (1943). 2. Professor Woodward offers an excellent explanation: Real assent to any given term in a form contract, including a merger clause, depends on how "rational" it is for the non-drafter (consumer and non-consumer alike) to attempt to understand what is in the form. This, in turn, is primarily a function of two observable facts: (1) the complexity and obscurity of the term in question and (2) the size of the un- derlying transaction. -

Tracing Is a Process Not a Remedy

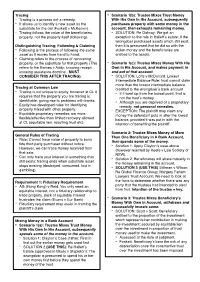

Tracing - Scenario 1(b): Trustee Mixes Trust Money - Tracing is a process not a remedy. With His Own In His Account, subsequently - It allows us to identify a new asset as the purchases property with some money in the substitute for the old (Foskett v McKeown). account, then exhausts remaining money. - Tracing follows the value of the beneficiaries - SOLUTION: Re Oatway: We get an property, not the property itself (following). exception to the rule in Hallett’s estate: if the wrongdoer purchased assets which still exist, Distinguishing Tracing; Following & Claiming then it is presumed that he did so with the - Following is the process of following the same stolen money and the beneficiaries are asset as it moves from hand to hand. entitled to the assets. - Claiming refers to the process of recovering property, or the substitute for that property (This - Scenario 1(c): Trustee Mixes Money With His refers to the Barnes v Addy; knowing receipt, Own In His Account, and makes payment in knowing assistance doctrine - MUST and out of that account. CONSIDER THIS AFTER TRACING). - SOLUTION: Lofts v McDonald: Lowest Intermediate Balance Rule: trust cannot claim more than the lowest intermediate balance Tracing at Common Law - credited to the wrongdoer’s bank account Tracing is not unique to equity, however at CL it - If it went up from the lowest point, that is requires that the property you are tracing is not the trust’s money. identifiable, giving rise to problems with banks. - - Although you are deprived of a proprietary Equity has developed rules for identifying remedy, not personal remedies. -

Asset Tracing in the British Virgin Islands

Article Asset Tracing in the British Virgin Islands In this article, we will discuss some of the tools available to a party in the British Virgin Islands to seek to recover property, or proceeds of property, which have been misappropriated. It is not surprising that in some cases, the identity of the wrongdoer or the whereabouts of the misappropriated property is unknown. Against that background, it is worth noting that while a BVI, and whether there has been any past judgment which company incorporated in the BVI is required to maintain may shed light on assets held by the company. In addition, certain records at the office of its registered agent (such as upon application the BVI Land Registry can provide certain its memorandum and articles of association, register of details regarding the owner of BVI land or real estate. directors, register of members, minutes of members’ and However, this requires the applicant to first be able to directors’ meetings and copies of resolutions), there is no identify the location or owner of the land. A party may also right for the public to inspect such records. Indeed, obtain certain information regarding vessels registered under confidentiality of corporate documents and information is a BVI flag from the BVI Ship Registry. one of the key attractions of incorporating a company in the BVI. BVI companies are not generally required to maintain or What is “tracing”? file statutory accounts, or meet any particular set of international accounting standards. Under section 98 of the Tracing consists of a series of rules developed by equity to BVI Business Companies Act 2004, all that a company is deal with situations where assets have been required to maintain are records “sufficient to show and misappropriated and the wrongdoer is not in a position to explain the company’s transactions” and which “will, at any compensate, or money compensation is not adequate. -

Asset Tracing and Recovery Reassessed

Asset tracing and recovery reassessed Nicole Sandells QC Miles Harris 4 New Square Professional Liability & Regulatory Conference 4 February 2020 This material was provided for the 4 New Square Professional Liability & Regulatory Conference on 4 February 2020. It was not intended for use and must not be relied upon in relation to any particular matter and does not constitute legal advice. It has now been provided without responsibility by its authors. 4 NEW SQUARE T: +44 (0) 207 822 2000 LINCOLN’S INN F: +44 (0) 207 822 2001 LONDON WC2A 3RJ DX: LDE 1041 WWW.4NEWSQUARE.COM E: [email protected] Nicole Sandells QC Call: 1994 Silk: 2018 Nicole's practice in recent years has focused heavily on financial and property law, civil fraud, restitution, trusts, probate and equitable remedies alongside Chambers' mainstream professional indemnity work. She has significant experience of unjust enrichment, subrogation, breach of trust and fiduciary duty claims. She is never happier than when finding novel answers to tricky problems. Nicole is described as ‘a mega-brain, with encyclopaedic legal knowledge and the ability to cut through complex legal issues with ease’ and 'a master tactician who is exceptionally bright and has a fantastic ability to condense significant evidential information' (Legal 500). Apparently, she is also “exceptionally bright and a ferocious advocate. She gives tactical advice and is a pleasure to work with. Clients speak extremely highly of her.” “If you want someone to think outside of the box and really come up with an innovative position, then she’s an excellent choice.” – Chambers & Partners, 2020 Professional Negligence. -

Thomas, Et Al. V. Othman, Et

IN THE COURT OF APPEALS FIRST APPELLATE DISTRICT OF OHIO HAMILTON COUNTY, OHIO RICHARD THOMAS, : APPEAL NO. C-160827 TRIAL NO. A-1601001 and : GAIL THOMAS, : O P I N I O N. Plaintiffs-Appellants, : vs. : AKRAM OTHMAN, : and : MARK WOEHLER, : Defendants-Appellees. : Civil Appeal From: Hamilton County Court of Common Pleas Judgment Appealed from is: Affirmed Date of Judgment Entry on Appeal: November 8, 2017 William Flax, for Plaintiffs-Appellants, James R. Hartke, for Defendant-Appellee Akram Othman, George M. Parker, for Defendant-Appellee Mark Woehler. OHIO FIRST DISTRICT COURT OF APPEALS CUNNINGHAM, Presiding Judge. {¶1} Plaintiffs-appellants Richard and Gail Thomas appeal from the judgment of the Hamilton County Court of Common Pleas granting the motion of defendants-appellees Akram Othman and Mark Woehler to dismiss the amended complaint for failure to state a claim upon which relief could be granted, pursuant to Civ.R. 12(B)(6). For the reasons that follow, we affirm. I. Background Facts and Procedure {¶2} This appeal arises from the Thomases’ efforts to recover from Othman and Woehler a portion of the retirement funds the Thomases lost after investing them in a Ponzi scheme operated by Glen Galemmo. According to the allegations in the amended complaint, Galemmo was convicted of securities fraud in the case United States v. Galemmo, Case No. 1:13-CR-00141, for operating a “complex,” multi-year “Ponzi scheme.” The Thomases, Othman, and Woehler were all investors in the scheme, and are all members of the plaintiff class of “Net Losers” investors— investors who lost more than their principal investment—in several civil class-action lawsuits which were referenced in the Thomases’ complaint. -

Unconscionability As a Sword: the Case for an Affirmative Cause of Action

Unconscionability as a Sword: The Case for an Affirmative Cause of Action Brady Williams* Consumers are drowning in a sea of one-sided fine print. To combat contractual overreach, consumers need an arsenal of effective remedies. To that end, the doctrine of unconscionability provides a crucial defense against the inequities of rigid contract enforcement. However, the prevailing view that unconscionability operates merely as a “shield” and not a “sword” leaves countless victims of oppressive contracts unable to assert the doctrine as an affirmative claim. This crippling interpretation betrays unconscionability’s equitable roots and absolves merchants who have already obtained their ill-gotten gains. But this need not be so. Using California consumer credit law as a backdrop, this Note argues that the doctrine of unconscionability must be recrafted into an offensive sword that provides affirmative relief to victims of unconscionable contracts. While some consumers may already assert unconscionability under California’s Consumers Legal Remedies Act, courts have narrowly construed the Act to exempt many forms of consumer credit. As a result, thousands of debtors have remained powerless to challenge their credit terms as unconscionable unless first sued by a creditor. However, this Note explains how a recent landmark ruling by the California Supreme Court has confirmed a novel legal theory that broadly empowers consumers—including debtors—to assert unconscionability under the State’s Unfair Competition Law. Finally, this Note argues that unconscionability’s historical roots in courts of equity—as well as its treatment by the DOI: https://doi.org/10.15779/Z382B8VC3W Copyright © 2019 California Law Review, Inc. California Law Review, Inc. -

Equity's Doctrine of Unclean Hands Still Has Serious Teeth, at Least in the World of Trusts (Part 2)

Title Equity’s doctrine of unclean hands still has serious teeth, at least in the world of trusts (Part 2) Text. In an action for breach of trust, the unclean hands of the plaintiff-beneficiary, assuming they are in fact unclean, could well be an effective equitable defense. The Restatement of Restitution (1937), specifically § 140, provides that “a person may be prevented from obtaining restitution for a benefit because of his criminal or other wrongful conduct in connection with the transaction on which his claim is based.” Equity’s maxims as they apply to the trust relationship, of which the doctrine of unclean hands is one, are catalogued in §8.12 of Loring and Rounds: A Trustee’s Handbook (2021), which section is reproduced in relevant parts in the appendix below. The maxims’ relevance to the trust relationship is addressed in the footnoting to the excerpt. "The doctrine of unclean hands is unique to equity and has no analog at law. Unlike most legal doctrines, its aim is not to aid the search for truth, or even promote justice for the litigants. Its purpose is protection of the reputation of equity itself, and of those courts that exist to provide equity. The awesome power of equity, as opposed to the limited civil power of the law courts, would be intolerable unless stringently cabined by a doctrine under which Chancery withholds this power where invoked by wrongdoers whose bad acts are a part of the cause of action itself.” In re Niki & Darren Irrev. Tr., 2020 WL 8421676 (Del. Ch. Feb. -

Unconscionability and the Code-The Emperor's New Clause

University of Pennsylvania Law Review FOUNDED 1852 Formerly American Law Register VOL. 115 FEBRUARY 1967 No. 4 1UNCONSCIONABILITY AND THE CODE- THE EMPEROR'S NEW CLAUSE ABTEiuEt AIX N LF f INTRODUCTION This paper is devoted wholly to section 2-302 of the Uniform Commercial Code, the so-called unconscionability clause.' It is, how- ever, not primarily an essay on commercial law. Rather it is intended to be a study in statutory pathology, an examination in some depth of the misdrafting of one section of a massive, codifying statute and the misinterpretations which came to surround it. The paper therefore is not intended as a commentary upon the content or drafting technique t Assistant Professor of Law, Washington University Law School. B.A. 1956, Amherst College. LL.B. 1959, Harvard University. 1 UNIFORM COMMERCIAL CODE § 2-302 (1962). This is the current version of the Code, which will be cited hereinafter as UCC. In the course of this paper various other versions of the Code and its predecessor statutes will be cited: 1) NATIONAL CONFERENCE OF ComMIsSIoNERs ON UNIFORM STATE LAWS, PROPOSED REPORT ON AND DRAFT OF A REvISED UNIFORM SALES AcT (1941) [hereinafter cited as MIMEo 1941 D AFr]. There are two versions of the 1941 draft, one mimeographed and the other printed. Only the former contains the text of the then predecessor to § 2-302. See note 12 infra for further details. The printed version will be cited hereinafter as PRINTED 1941 DRAFT. 2) NATIONAL CONFERENCE OF COMMISSIONERS ON UNIFORM STATE LAWS, UNIFORM REvisED SALES ACT (Third Draft, 1943) [hereinafter cited as 1943 DRAFT]. -

Specific Performance and the Thirteenth Amendment

College of William & Mary Law School William & Mary Law School Scholarship Repository Faculty Publications Faculty and Deans 2009 Specific eP rformance and the Thirteenth Amendment Nathan B. Oman William & Mary Law School, [email protected] Repository Citation Oman, Nathan B., "Specific eP rformance and the Thirteenth Amendment" (2009). Faculty Publications. 82. https://scholarship.law.wm.edu/facpubs/82 Copyright c 2009 by the authors. This article is brought to you by the William & Mary Law School Scholarship Repository. https://scholarship.law.wm.edu/facpubs Article Specific Performance and the Thirteenth Amendment Nathan B. Oman† I. Introduction ................................................................ 2021 II. Situating the Argument ............................................. 2026 A. Specific Performance, the Common Law, and the Constitution as a Conversation-Stopper ..... 2026 B. Arguing over the Thirteenth Amendment ......... 2030 C. A Note on Methodology ....................................... 2034 III. The Meaning of “Involuntary Servitude” Before the Thirteenth Amendment .............................................. 2038 A. The Northwest Ordinance .................................. 2038 B. The Boundary Between Slavery and Contract in the Law of the Old Northwest ........................ 2040 C. Other State Constitutional Conventions ........... 2049 D. Popular Usage of the Term “Involuntary Servitude” ............................................................ 2055 IV. Legislative History of the Thirteenth Amendment .. -

Tracing and the Rule in Clayton's Case

LAW REFORM COMMISSION OF BRITISH COLUMBIA REPORT ON COMPETING RIGHTS TO MINGLED PROPERTY: TRACING AND THE RULE IN CLAYTON'S CASE LRC 66 September 1983 The Law Reform Commission of British Columbia was established by the Law Reform Commis- sion Act in 1969 and began functioning in 1970. The Commissioners are: The Honourable Mr. Justice John S. Aikins, Chairman Arthur L. Close, ViceChairman Bryan Williams Anthony F. Sheppard Ronald I. Cheffins, (appointed Sept. 15, 1983) Thomas G. Anderson is Counsel to the Commission. Frederick W. Hansford is Staff Lawyer to the Commission. Sharon St. Michael is Secretary to the Commission. The Commission offices are located on the 5th Floor, 700 West Georgia Street, (P.O. Box 10135, Pacific Centre) Vancouver, B.C. V7Y 1C6. Canadian Cataloguing in Publication Data Law Reform Commission of British Columbia. Report on competing rights to mingled property Includes bibliographical references. “LRC 66". ISBN 0-7718-8391-9 1. Right of property - Canada. 2. Priorities of claims and liens - Canada. I. Title. KE765.A72L38 1983 346.7104'2 C83-092306-3 TABLE OF CONTENTS I. INTRODUCTION 1 A. Revolving Credit Arrangements 1 B. The Working Paper 3 II. RIGHTS AND REMEDIES 5 A. Introduction 5 B. Law and Equity 5 C. Rights 6 1. Real Rights 6 2. Possessory Rights 7 3. Personal Rights 7 D. Remedies 7 1. Real Remedies 7 2. Personal Remedies 8 E. Title to Property at Law 8 1. Property 8 2. Money 9 F. Tracing and Following Property 10 G. Debt 12 H. What is a Bank Account? 13 I. -

The Annotated Will 2017

THE ANNOTATED WILL 2017 chairs Susannah Roth, TEP O’Sullivan Estate Lawyers Mary-Alice Thompson, C.S., TEP Cunningham, Swan, Carty, Little & Bonham LLP January 12, 2017 *CLE17-0010401-A-PUB* DISCLAIMER: This work appears as part of The Law Society of Upper Canada’s initiatives in Continuing Professional Development (CPD). It provides information and various opinions to help legal professionals maintain and enhance their competence. It does not, however, represent or embody any official position of, or statement by, the Society, except where specifically indicated; nor does it attempt to set forth definitive practice standards or to provide legal advice. Precedents and other material contained herein should be used prudently, as nothing in the work relieves readers of their responsibility to assess the material in light of their own professional experience. No warranty is made with regards to this work. The Society can accept no responsibility for any errors or omissions, and expressly disclaims any such responsibility. © 2017 All Rights Reserved This compilation of collective works is copyrighted by The Law Society of Upper Canada. The individual documents remain the property of the original authors or their assignees. The Law Society of Upper Canada 130 Queen Street West, Toronto, ON M5H 2N6 Phone: 416-947-3315 or 1-800-668-7380 Ext. 3315 Fax: 416-947-3991 E-mail: [email protected] www.lsuc.on.ca Library and Archives Canada Cataloguing in Publication The Annotated Will 2017 ISBN 978-1-77094-402-2 (Hardcopy) ISBN 978-1-77094-403-9 (PDF) THE ANNOTATED WILL 2017 Chairs: Susannah Roth, TEP O’Sullivan Estate Lawyers Mary-Alice Thompson, C.S., TEP Cunningham, Swan, Carty, Little & Bonham LLP Presenters: Darren Lund Fasken Martineau LLP Jane Martin Dickson Appell LLP January 12, 2017 9:00 a.m. -

Unconscionability Wars

Copyright 2011 by Northwestern University, School of Law Vol. 106 Northwestern University Law Review Colloquy UNCONSCIONABILITY WARS David Horton* INTRODUCTION It would be hard to exaggerate the importance of the unconscionability doctrine to federal arbitration law. In the last three decades, as the Supreme Court has expanded the scope of the Federal Arbitration Act (FAA),1 arbi- tration clauses have become a routine part of consumer, franchise, and em- ployment contracts. Some companies have sought not just to funnel cases away from courts, but to tilt the scales of justice in their favor: stripping remedies, slashing discovery, selecting biased arbitrators, eliminating the right to bring a class action, and saddling adherents with prohibitive costs and fees.2 The unconscionability doctrine has emerged as the primary check on drafter overreaching. The Court has repeatedly acknowledged that lower courts can invoke unconscionability to invalidate one-sided arbi- tration provisions,3 and dozens (perhaps hundreds) of judges have done ex- actly that.4 Recently, however, a rising chorus of voices argues that the FAA al- lows arbitrators, but not judges, to strike down arbitration clauses as un- conscionable.5 These critics make three main points. First, they argue that the FAA, which limits judicial discretion, is incompatible with unconscio- nability, which is one of the most subjective and amorphous rules in all of law.6 Second, they assert that Congress recognized that the statute might al- low powerful drafters to exploit weaker parties, but nevertheless concluded that its benefits outweighed these risks.7 Third, they seize upon a seeming discrepancy at the heart of the statute.