Market Segment Report: European Insurers' Focus on Profitability

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

American Post-Conflict Educational Reform This Page Intentionally Left Blank American Post-Conflict Educational Reform from the Spanish-American War to Iraq

American Post-Conflict Educational Reform This page intentionally left blank American Post-Conflict Educational Reform From the Spanish-American War to Iraq Edited by Noah W. Sobe AMERICAN POST-CONFLICT EDUCATIONAL REFORM Copyright © Noah W. Sobe, 2009. Softcover reprint of the hardcover 1st edition 2009 978-0-230-61592-2 All rights reserved. First published in 2009 by PALGRAVE MACMILLAN® in the United States—a division of St. Martin’s Press LLC, 175 Fifth Avenue, New York, NY 10010. Where this book is distributed in the UK, Europe and the rest of the world, this is by Palgrave Macmillan, a division of Macmillan Publishers Limited, registered in England, company number 785998, of Houndmills, Basingstoke, Hampshire RG21 6XS. Palgrave Macmillan is the global academic imprint of the above companies and has companies and representatives throughout the world. Palgrave® and Macmillan® are registered trademarks in the United States, the United Kingdom, Europe and other countries. ISBN 978-1-349-37951-4 ISBN 978-0-230-10145-6 (eBook) DOI. 10.1057/9780230101456 Library of Congress Cataloging-in-Publication Data American post-conflict educational reform : from the Spanish- American War to Iraq / edited by Noah W. Sobe. p. cm. Includes bibliographical references and index. 1. Educational assistance, American. 2. Educational change. 3. Conflict management. I. Sobe, Noah W., 1971– LB2283.A47 2009 379.1Ј290973—dc22 2009014130 A catalogue record of the book is available from the British Library. Design by Newgen Imaging Systems (P) Ltd., Chennai, India. First edition: December 2009 10 9 8 7 6 5 4 3 2 1 CONTENTS Part I Introduction One American Imperatives, Educational Reconstruction and the Post-Conflict Promise 3 Noah W. -

GLOBAL CLIMATE BULLETIN N°222 – December 2017

RCC RA VI Climate Bulletin n°222 December - January - February 2017 - 2018 GLOBAL CLIMATE BULLETIN n°222 – December 2017 Table of Contents I. DESCRIPTION OF THE CLIMATE SYSTEM I.1. Oceanic analysis I.1.a Global analysis I.1.b Sea surface temperature Near Europe I.2. Atmosphere I.2.a General Circulation I.2.b Precipitation I.2.c Temperature I.2.d Sea ice II. SEASONAL FORECAST FROM DYNAMICAL MODELS II.1. OCEANIC FORECASTS II.1.a Sea surface temperature (SST, figure II.1.1 to II.1.4) II.1.b ENSO forecast II.1.c Atlantic ocean forecasts II.1.d Indian ocean forecasts II.2. GENERAL CIRCULATION FORECAST II.2.a Global forecast II.2.b Norther n hemisphere and E urope forecast II.2.c Modes of variability II.2.d Weather regimes II.3. IMPACT: TEMPERATURE FORECASTS (figure II.3.1 to II.3.4) II.3.a Météo-FranceECMWF II.3.b ECMWF II.3.c Japan Meteorological Agency (JMA) II.3.d EUROSIP II.4. IMPACT : PRECIPITATION FORECAST © Météo-France DCSC December 2017 1 sur 31 RCC RA VI Climate Bulletin n°222 December - January - February 2017 - 2018 II.4.a Météo-France II.4.b ECMWF II.4.c Japan Meteorological Agency (JMA) II.4.d EUROSIP II.5. REGIONAL TEMPERATURES and PRECIPITATIONS II.6. "EXTREME" SCENARIOS II.7. DISCUSSION AND SUMMARY II.7.a Forecast over Europe II.7.b Tropical cyclone activity III. ANNEX III.1. Seasonal Forecasts III.2. « NINO », SOI indices and Oceanic boxes III.3. -

Annual Report 2017

Annual Report 2017 www.ecmwf.int Foreword 2 2017 At a glance 4 Advancing weather science 10 Delivering global predictions 16 Sustaining high-performance computing 22 Supporting ECMWF 26 Serving Member and Co-operating States 30 How we work 36 Member States as of January 2018 Austria Belgium Croatia Denmark Finland France Germany Greece Iceland Ireland Italy Luxembourg The Netherlands Norway Portugal Serbia Slovenia Spain Sweden Switzerland Turkey United Kingdom ecmwf.int ECMWF Annual Report 2017 1 AR-2018-ARTWORK.indd 1 08/06/2018 16:01 A year among years Florence Rabier Director-General There is a lot to say about 2017, and the following pages allow us to remember or discover some of the key moments. Possibly the most striking aspect that comes to mind is the way our past, present and future collided in that speci c year. 2017 was a rework of anniversaries. Trust is earned, and 2017 has allowed It marked 20 years of 4D-Var at ECMWF, us to pay our dues and serve our Member and of seasonal forecasts, and 25 years of States and other users with some noticeable ensemble prediction and wave forecasting. progress towards our Strategy to 2025. It was also the year when ECMWF’s Council Some good examples include the work approved the development of our future undertaken to assess the best ensemble data centre in Bologna, Italy, and voted con gurations to make a 5 km ensemble a budget allowing a substantial increase affordable; the more ef cient radiation in our computing capability. The end of the scheme, completely recoded to be more year saw the Government of the UK, our exible and delivering ef ciency gains up host nation, formally offering to relocate to 30-35%; the release of the new seasonal ECMWF’s headquarters to accommodate system, SEAS5, notably improving our requirements. -

Czech Republic

Riskline / Country Report / 29 August 2021 CZECH REPUBLIC Overall risk level Medium Exercise caution Not completely safe, but typically presents predictable security risks Travel is possible, but there is a potential for disruptions Overview Emergency Numbers Medical 155 Upcoming Events There are no upcoming events scheduled Riskline / Country Report / 29 August 2021 / Czech Republic 2 Travel Advisories Riskline / Country Report / 29 August 2021 / Czech Republic 3 Summary The Czech Republic is a Medium Risk destination: exercise caution. Medium Risk locations are not completely safe, but typically present predictable security risks. Travel is possible, but there is a potential for disruptions. Covid-19 Medium Risk Health authorities confirmed the country's first cases of the novel coronavirus (COVID- 19) on 1 March 2020. Despite the spread of the delta virus variant, infection rates in the country remain low. Most measures have been relaxed or lifted. Political Instability Low Risk The Czech Republic is a largely conservative nation with a stable multi-party democracy, a robust welfare system and a healthy economy. President Miloš Zeman is from the far-right, but state institutions are relatively strong and independent, with respect for civil rights. While the Czech parliament consists of two chambers, most of the legislative powers are concentrated in the lower house, the Chamber of Deputies. The country is a member of both the North Atlantic Treaty Organisation (NATO) and the European Union (EU). Conflict Low Risk The country is not party to any conflict with other states or non-state actors. It is a member of the European Union (EU) and NATO. -

Meteorological Description of the Winter Storms SEBASTIAN, XAVIER, HERWART, ZUBIN, BURGLIND, FRIEDERIKE

DWD background report Winter storm season 2017/18 (01.09.2017–28.02.2018) – meteorological description of the winter storms SEBASTIAN, XAVIER, HERWART, ZUBIN, BURGLIND, FRIEDERIKE Due to the large temperature and thus energy differences between the polar regions and the warm-temperate climate zone during the northern hemisphere’s winter half-year, unstable wave formations typically arise on the frontal zone, with the potential to evolve into storm cyclones. According to the long-term climatological average, the high-pressure weather situations, usually dominant through to the last ten days of October, are succeeded by a cyclonic circulation regime. This then marks the start of autumn or winter storm season in central Europe. In 2017/18, the winter storm season began very early on 12 September when a polar air outburst originating in Greenland strengthened a short-wave trough to such an extent that a rapid drop in pressure (‘explosive cyclogenesis’, i.e. a fall in air pressure in a low’s centre of at least 1 hPa/h over a period of at least 24 hours1) in the corresponding surface pressure field transformed an initially unremarkable secondary low into the storm cyclone SEBASTIAN. SEBASTIAN brought hurricane-force gusts (≥ 12 Bft) mainly to the coastal areas and mountain tops in the low mountain ranges on 13 September, as well as daily precipitation totals of several tens of litres per square metre in places in southern Germany. A vigorous west wind drift again dominated over the European continent three weeks later. The secondary cyclogenesis (Shapiro-Keyser type, i.e. a special form of polar front cyclones in maritime areas2) of a central low, which had in the meantime arrived over Fennoscandia, brought the second autumn storm of the season. -

Cat Hit Makes 2018 a Crucial Year for Lloyd's

MARKET NEWS, DATA AND INSIGHT ALL DAY, EVERY DAY TUESDAY 12 DECEMBER 2017 ISSUE 4,997 In depth: Cat hit makes 2018 a crucial year for Lloyd’s p4-7 Raging Thomas fire threatens to IAG deal add to $10bn California wildfire bill lays ground for ‘10% premium boost’ for top three reinsurers p2 p3 Get the complete picture Award-winning scoops, trusted analysis and insight for the specialty and reinsurance sectors ID-Complete Picture-260x70.indd 1 08/09/2017 14:23 2 www.insuranceday.com | Tuesday 12 December 2017 NEWS Raging Thomas fire Market news, data and insight all day, every day Insurance Day is the world’s only daily newspaper for the international insurance and reinsurance and risk industries. Its primary focus is on the London market and what affects it, threatens to add to $10bn concentrating on the key areas of catastrophe, property and marine, aviation and transportation. It is available in print, PDF, mobile and online versions and is read by more than 10,000 people in more than 70 countries worldwide. California wildfire bill First published in 1995, Insurance Day has become the favourite publication for the London market, which relies on its mix of news, analysis and data to keep in touch with this fast-moving and vitally important sector. Its experienced and highly skilled insurance writers are well known and respected in the market Fire in southern California is among state’s 10 most destructive and their insight is both compelling and valuable. Insurance Day also produces a number of must-attend annual Scott Vincent Firefighters events to complement its daily output, including the Insurance Editor, news services monitor the Day London Market Awards, which recognise and celebrate the Thomas fire as very best in the industry. -

Pdf, 647.9 KB

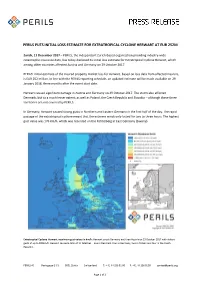

PERILS PUTS INITIAL LOSS ESTIMATE FOR EXTRATROPICAL CYCLONE HERWART AT EUR 252M Zurich, 11 December 2017 – PERILS, the independent Zurich-based organisation providing industry-wide catastrophe insurance data, has today disclosed its initial loss estimate for Extratropical Cyclone Herwart, which among other countries affected Austria and Germany on 29 October 2017. PERILS’ initial estimate of the insured property market loss for Herwart, based on loss data from affected insurers, is EUR 252 million. In line with the PERILS reporting schedule, an updated estimate will be made available on 29 January 2018, three months after the event start date. Herwart caused significant damage in Austria and Germany on 29 October 2017. The storm also affected Denmark, but to a much lesser extent; as well as Poland, the Czech Republic and Slovakia – although these three territories are not covered by PERILS. In Germany, Herwart caused strong gusts in Northern and Eastern Germany in the first half of the day. The rapid passage of the extratropical cyclone meant that the extreme winds only lasted for two to three hours. The highest gust value was 176 km/h, which was recorded on the Fichtelberg in East Germany (Saxony). Extratropical Cyclone Herwart, maximum gust values in km/h: Herwart struck Germany and then Austria on 29 October 2017 with violent gusts of up to 180km/h. Herwart caused a total of 11 fatalities – one in Denmark, four in Germany, two in Poland and four in the Czech Republic. PERILS AG Marktgasse 3 / 5 8001 Zurich Switzerland T: + 41 44 256 81 00 F: +41 44 256 8109 [email protected] Page 1 of 2 PERILS PUTS INITIAL LOSS ESTIMATE FOR EXTRATROPICAL CYCLONE HERWART AT EUR 252M Austria was hit by Herwart during the late morning and early afternoon. -

Sigma 1/2018

No 1 /2018 Natural catastrophes and 01 Executive summary 02 Catastrophes in 2017: man-made disasters in 2017: global overview a year of record-breaking 06 Regional overview 18 HIM: an unprecedented losses hurricane cluster event? 27 Tables for reporting year 2017 50 Terms and selection criteria Foreword This year we celebrate the 50th anniversary of sigma, the flagship publication of the Swiss Re Institute´s research portfolio. Over the last half century, sigma has provided thought leadership spanning the ever-evolving risk landscape facing society, the macro and regulatory environments and their impact on insurance markets, and industry-specific topics such as underwriting cycles and distribution channels. As the industry's leading research publication, sigma has been and remains a central pillar of Swiss Re's vision to make the world more resilient. As the first edition of sigma in 2018, we are pleased to bring you our annual report providing data on and in-depth analysis of recent major natural and man-made disasters. Our first-ever sigma report on natural catastrophes (nat cat) was published in 1969, and nat cat has been a mainstay of the series ever since. In “sigma No. 12/1969: Insurance against power of nature damage and its problems˝, our objective was to “point out the nature and extent of power of nature damage˝ … by which “we mean events caused by the forces of nature.˝ Fifty years on, the “forces of nature“ continue to inflict devastation on communities all around the world. By far the largest nat cat events in 2017 were a series of hurricanes that hit the Caribbean and the US. -

Informe Geobrasilgeobrasil (

VVINFORMEINFORME GEOBRASILGEOBRASIL (www.geobrasil.net) Fotos tiradas do site da Nasa キ1 CONCURSOS キ2 BOLSAS Inpe seleciona bolsistas de pós-doutorado キ3 CONGRESSOS E SIMPÓSIOS キ4 ARTIGO DA SEMANA A mais distante das galáxias Paleontólogos encontram fóssil de dinossauro com apenas uma garra キ5 ÍNDICE DE NOTÍCIAS キ6 AMBIENTE BRASIL キ7 JORNAL DA CIÊNCIA Edição 4187 - Notícias de C&T - Serviço da SBPC Edição 4186 - Notícias de C&T - Serviço da SBPC Edição 4185 - Notícias de C&T - Serviço da SBPC Edição 4184 - Notícias de C&T - Serviço da SBPC キ8 MUNDOGEO キ9 IAPC キ10 EARTH PAGES ***As pessoas interessadas em receber nossa newsletter via mail, podem escrever para [email protected] ou [email protected] pedindo sua adesão. Newsletter Geobrasil キ11 CONCURSOS O Portal MundoGEO publica, toda semana, as mais recentes oportunidades de trabalho na área de geoinformação. São empregos com carteira assinada, trabalhos temporários, processos seletivos, concursos públicos, licitações, estágios e programas de trainee. Empregos Cargos: 1) Assistente comercial. Experiência em vendas na área de geotecnologia, conhecimento do pacote Office, atendimento ao cliente. 2) Assistente comercial. Vaga para profissionais do sexo feminino de nível médio. Necessário conhecimento em informática e microsoft office, experiência em proposta comercial preferenciamente na área de engenharia e serviços técnicos e atendimento a clientes. Empresa: Senografia Sensoriamento Remoto Ltda. Local: Curitiba (PR) Contato: Enviar currículo com pretensão salarial para [email protected], informando no assunto do email o cargo. Cargo: Topógrafo II. Experiência comprovada na função; Experiência em obras de Vias de Comunicação (Terraplenagem e Pavimentação); •Domínio do Office; Domínio de GPS e Estação Total; Facilidade de adaptação a contextos multiculturais; Disponibilidade Imediata. -

Compilation of the PPE

Compilation of Inputs to the WMO Open Consultative Platform White Paper #1 Future of Weather and Climate Forecasting (Annex to WMO No. 1263) Unedited original inputs from contributors Contents A message from the Lead Author .......................................................................................................... 1 About this White Paper .......................................................................................................................... 2 Goal 1: Customised impact-based forecasts and warnings .............................................................. 2 Goal 2: Reliable and trusted forecasts ............................................................................................... 3 Goal 3: An Earth system prediction capability .................................................................................. 3 Goal 4: Seamless weather and climate insights ................................................................................ 3 Inputs of White Paper Contributors ...................................................................................................... 4 Peter Bauer ......................................................................................................................................... 4 Natacha Bernier .................................................................................................................................. 9 Veronique Bouchet ......................................................................................................................... -

Analysis of the Degree of Threat to Railway Infrastructure by Falling Tree Vegetation

International Journal of Geo-Information Article Analysis of the Degree of Threat to Railway Infrastructure by Falling Tree Vegetation Michal Kuˇcera 1,2 and Zdena Dobesova 1,* 1 Department of Geoinformatics, Palacký University Olomouc, 771 46 Olomouc, Czech Republic; [email protected] 2 Railway Administration, Jeremenkova 103/23, 779 00 Olomouc, Czech Republic * Correspondence: [email protected] Abstract: The article presents a method for determining and evaluating the threat to railway infras- tructure from falling trees. The main objective was to identify the degree of threat according to three parameters: the height of tree stands, species composition, and vegetation health. Identification of the threat to individual railway sections would allow the creation of measures that could increase operational safety. Evaluation should be carried out at regular intervals to assess vegetation health during certain seasons. We, therefore, recommend the use of satellite images to provide a data source and regular data updates. The potential benefit is a reduction in railway infrastructure damage and an increase in traffic flow, especially during periods of exceptional weather conditions involving high wind, ice or heavy snow. The new method presented in the paper, based on data for railway infrastructure, law and other data sources in the Czech Republic, determines a Vegetation Threat Index for Railways (VTIR). We selected the Liberec Region as an example case study because of its large spread of wooded areas around railway lines and high incidence of railway traffic accidents. Citation: Kuˇcera,M.; Dobesova, Z. Analysis of the Degree of Threat to Keywords: raster analysis; railway; tree; damage; satellite data; remote sensing; GIS; NDVI Railway Infrastructure by Falling Tree Vegetation. -

Pdf, 356.62 KB

PERILS DISCLOSES FINAL LOSS ESTIMATE FOR EXTRATROPICAL CYCLONE HERWART OF EUR 264M Zurich, 29 October 2018 – PERILS, the independent Zurich-based organisation providing industry-wide catastrophe insurance data, has today disclosed its final loss estimate for Extratropical Cyclone Herwart, which primarily affected Austria and Germany on 29 October 2017. PERILS’ estimate of the insured property market loss for Herwart, based on loss data collected from affected insurers, is EUR 264 million. This compares to the third loss estimate of EUR 255 million which was issued by PERILS on 27 April 2018, six months after the event. This final loss number has been issued twelve months after the event, in line with the PERILS reporting schedule. Herwart was a rapidly moving system bringing extreme wind conditions that lasted for only a few hours. The storm impacted the northern and eastern regions of Germany during the early hours of the day, before hitting the eastern half of Austria in the late morning and early afternoon. The highest gust values recorded were 176 km/h in Germany (Fichtelberg, Saxony), and 180 km/h in Austria (Feuerkogel Mountain, Upper Austria). Extratropical Cyclone Herwart, market loss footprint: PERILS final loss estimate for the property market loss of Herwart amounts to EUR 264m. As for every final loss report, the market loss data for Herwart are available by CRESTA zone and property line of business. This loss footprint information is complemented by gust speed values and loss ratios which show the incurred loss from Herwart as a percentage of the sums insured. PERILS AG Marktgasse 3 / 5 8001 Zurich Switzerland T: + 41 44 256 81 00 F: +41 44 256 8109 [email protected] Page 1 of 2 PERILS DISCLOSES FINAL LOSS ESTIMATE FOR EXTRATROPICAL CYCLONE HERWART OF EUR 264M About PERILS PERILS is an independent Zurich-based organisation providing industry-wide natural catastrophe exposure and event loss data.