Retailing Within the E.C

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Developing Employees As Organisational Assets

Developing Employees as Organisational Assets INTRODUCTION The Kingfisher Recruitment • The Person Specification How KMDS is evolving commercial and afterwards in key functions The Group requires from prospec- Kingfisher plc is one of Europe’s leading retailers based Management Development Scheme Investing in a trainee over ten years tive KMDS trainees: The KMDS was launched in 1995 and • a post-graduate certificate in man- around three main sectors - DIY, electrical and general involves significant cost as well as today has 172 individuals on the scheme agement studies from Templeton • excellent interpersonal skills merchandise. The company employs over 130,000 people in invest- risk. The risk includes choosing the working across the Group. All individu- College, Oxford The KMDS represents a key • enthusiasm and drive to become ment by the organisation in its human wrong type of person and equally als following the KMDS route joined in • a ‘skills tool-box’ consisting of 2,900 stores across 15 countries and has some of the best senior managers within 7-10 years assets. The scheme takes high-poten- importantly losing the person to anoth- their early 20s. Recently Kingfisher has day-release training to develop per- known retail brands in Europe, including B&Q, Castorama, • innovative approach to challenges tial graduates who want to make a er organisation during the training recognised that there are benefits in sonal skills Comet, Darty, BUT, Woolworths and Superdrug among opening up the process to existing high- career in retail, and provides them with process. For this reason, Kingfisher • the ability to analyse and make • a ‘buddy’ who is already on the others. -

Swale Borough Council

SWALE BOROUGH COUNCIL Project: RETAIL STUDY 2010: Bulky and DIY Goods Addendum Latest Revision: 20/05/2011 - DRAFT Study area population by zone Zone 2010 2015 2020 2025 1 39,501 40,410 41,418 42,595 2 12,888 13,185 13,514 13,897 3 46,052 47,112 48,287 49,659 4 11,242 11,501 11,788 12,123 5 19,162 19,603 20,092 20,663 6 5,340 5,463 5,599 5,758 TOTAL 134,185 137,274 140,698 144,695 Sources/notes for frontispiece 1. 2010 population for each zone from Pitney Bowes Business Insight Area Profile Report (6 July 2010) 2. Growth in population based on growth rates implied by scenarioKent County 3 of Council 6 scenarios population prepared forecasts by Research for Swale & Intelligence, Borough - South Kent CouEastntyPlan Council Strategy (16- Septemberbased Forecasts 2010). (September The KCC projections 2009) Total are Population based on SwaleForecasts. Borough Available: Counciil's 'Option 1' for newhttps://shareweb.kent.gov.uk/Documents/facts homes which assumes an additional 13,503-and dwellings-figures/sep between-forecasts 2006-sep-2031-09 -usingweb.pdf a phasing Access provideddate: 12 byOctober SBC 2010 OTHER COMPARISON GOODS Table 3.1 Expenditure per capita (£) Zone 2007 2010 2015 2020 2025 1 2,062 2,162 2,592 3,124 3,764 2 2,356 2,470 2,962 3,569 4,301 3 2,164 2,269 2,721 3,278 3,950 4 2,336 2,449 2,937 3,539 4,264 5 2,194 2,300 2,758 3,324 4,005 6 2,347 2,460 2,951 3,555 4,284 Sources/notes for Table 3.1 1. -

Finance Project

MASTER OF SCIENCE IN FINANCE MASTERS FINAL WORK PROJECT EQUITY RESEARCH: HORNBACH BAUMARKT AG JOÃO MARIA GONÇALVES PAIVA DÓRDIO RODRIGUES SUPERVISOR: ANA ISABEL ORTEGA VENÂNCIO OCTOBER 2020 Acknowledgements This paper represents the end of a journey started in 2018 and I would like to express my sincerest gratitude to all persons involved in these 2 years of the Masters. Firstly, to Professor Ana Venâncio for the guidance, time and patience, not only during this project, but also during classes. Secondly, to my family, parents, sister and grandmother, for supporting and believing in me. And last but not least, to my friends, new and old, for the moments shared in these past 2 years. i Abstract The following project is a valuation of the company Hornbach Baumarkt AG, based on publicly available information until the 6th November 2020. It follows the format recommended by the CFA Institute. Hornbach Baumarkt AG was chosen due to the interest in wanting to explore and learn about the DIY sector and by it being the only publicly traded German company. Hornbach Baumarkt AG is a Top 10 player in the DIY Home Improvement sector in Europe. It was created in 1993 after an IPO that saw Hornbach AG being subdivided in Hornbach Holding AG (Parent Company) and Hornbach Baumarkt AG, having the original company being founded in 1877, in Landau, Germany, but only making their first IPO in 1987. Today, Hornbach Baumarkt AG is a Child company of Hornbach Holding AG. The valuation was derived from an intrinsic valuation, based on a Discounted Cash Flow (DFC) method, more specifically, through a Free Cash Flow to the Firm (FCFF) perspective. -

VIANNEY MULLIEZ : C’Est Un Beau Cadeau D’Anniversaire, Pour Les 50 Ans De Notre Entreprise, Que De Constater Combien L’Histoire Nous a Donné Raison

VIANNEY MULLIEZ : C’est un beau cadeau d’anniversaire, pour les 50 ans de notre entreprise, que de constater combien l’Histoire nous a donné raison. Chez Auchan, nous n’en tirons aucune vanité, mais comment ne pas nous réjouir du choix judicieux qu’a fait, en 1961, notre fondateur Gérard Mulliez. D’emblée, il nous a doté d’une vision et d’une identité forte en misant résolument sur les valeurs humaines et en décidant que, chez Auchan, jamais on ne transigerait avec celles-ci. ARNAUD MULLIEZ : Des valeurs si ancrées dans notre culture d’entreprise qu’elles font notre réputation et notre fierté. Pour nous, et dans tous nos métiers, il importe que le « process » soit au service de l’Homme et cela ne doit jamais être l’inverse. Cette approche prend tout son L’EÉDITO DE VIANNEY MULLIEZ ET D’ARNAUD MULLIEZ ème Edito sens, au début de ce XXI siècle, dans un monde économique globalisé que la récente crise a ébranlé dans ses certitudes. Les experts, les observateurs expliquent cette crise, qui est d’abord une crise de confiance, par le fait que nombre de managers auraient trop misé sur le profit et le court terme. VIANNEY MULLIEZ : « Il faut absolument remettre l’homme au cœur de l’entreprise » insiste-t-on aujourd’hui. 19612011 Mais, chez Auchan, l’Homme est depuis toujours « la » priorité pour les dirigeants, dans tous nos différents métiers basés sur notre expertise de la consommation et fédérés au sein de notre groupe. Qu’il s’agisse de la grande distribution, de la banque, de l’immobilier commercial ou d’Internet. -

1997-Paribas Annual Report

A N N U A L R E P O R T - C O M P A G N I E F I N A N C I È R E D E P A R I B A S TABLE OF CONTENTS Group organization (cover flap) P A R I B A S Profile 1 Interview with the chairmen 2 Consolidated financial highlights 6 Shareholder’s handbook 9 Supervisory Board 14 Executive Committee 17 INVESTMENT BANKING 18 Equity 20 Fixed Income 22 Corporate Banking 24 Advisory Services 26 Securities Services 28 Paribas Principal Investments (Paribas Affaires Industrielles) 30 ASSET MANAGEMENT 38 Institutional and Private Asset Management 40 Cardif 42 Cortal 43 RETAIL FINANCIAL SERVICES 44 UFB Locabail 46 Arval 46 Cetelem 47 Cofica 47 UCB 48 Banque Directe 48 OTHER ACTIVITIES 49 Rental property management 49 Real estate holdings 50 Equity holdings 51 Compagnie Financière de Paribas MANAGEMENT REPORT 53 5, rue d’Antin - 75078 Paris Cedex 02 - France CONSOLIDATED STATEMENTS 68 Tel.: 33 (0)1 42 98 12 34 - Telex: PARB 210041 Report of the Statutory Auditors 121 http://www.paribas.com General information 124 A N N U A L R E P O R T - C O M P A G N I E F I N A N C I È R E D E P A R I B A S TABLE OF CONTENTS Group organization (cover flap) P A R I B A S Profile 1 Interview with the chairmen 2 Consolidated financial highlights 6 Shareholder’s handbook 9 Supervisory Board 14 Executive Committee 17 INVESTMENT BANKING 18 Equity 20 Fixed Income 22 Corporate Banking 24 Advisory Services 26 Securities Services 28 Paribas Principal Investments (Paribas Affaires Industrielles) 30 ASSET MANAGEMENT 38 Institutional and Private Asset Management 40 Cardif 42 Cortal -

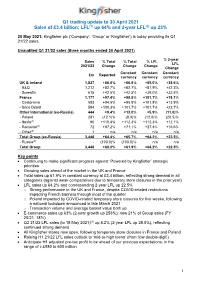

Q1 Trading Update to 30 April 2021 Sales of £3.4 Billion; LFL(1) up 64% and 2-Year LFL(2) up 23%

Q1 trading update to 30 April 2021 Sales of £3.4 billion; LFL(1) up 64% and 2-year LFL(2) up 23% 20 May 2021: Kingfisher plc (‘Company’, ‘Group’ or ‘Kingfisher’) is today providing its Q1 21/22 sales. Unaudited Q1 21/22 sales (three months ended 30 April 2021) % 2-year Sales % Total % Total % LFL LFL 2021/22 Change Change Change Change Constant Constant Constant £m Reported currency currency currency UK & Ireland 1,827 +66.8% +66.8% +65.0% +38.6% - B&Q 1,212 +82.7% +82.7% +81.9% +42.3% - Screwfix 615 +42.5% +42.5% +39.0% +32.5% France 1,177 +97.4% +98.8% +101.7% +18.1% - Castorama 583 +94.5% +95.8% +101.8% +13.9% - Brico Dépôt 594 +100.3% +101.7% +101.7% +22.7% Other International (ex-Russia) 444 +9.4% +13.0% +5.9% (11.0)% - Poland 281 (12.1)% (8.9)% (12.0)% (20.5)% - Iberia(3) 90 +110.8% +112.3% +112.3% +12.1% - Romania(4) 72 +67.2% +71.1% +27.4% +16.6% - Other(5) 1 n/a n/a n/a n/a Total Group (ex-Russia) 3,448 +64.4% +65.7% +64.2% +22.5% - Russia(6) - (100.0)% (100.0)% n/a n/a Total Group 3,448 +60.0% +61.9% +64.2% +22.5% Key points • Continuing to make significant progress against ‘Powered by Kingfisher’ strategic priorities • Growing sales ahead of the market in the UK and France • Total sales up 61.9% in constant currency at £3.4 billion, reflecting strong demand in all categories (against weak comparatives due to temporary store closures in the prior year) • LFL sales up 64.2% and corresponding 2-year LFL up 22.5% o Strong performance in the UK and France, despite COVID-related restrictions impacting French banners through most -

Screwfix Builds Bricks and Mortar Presence with 300Th Store

SCREWFIX BUILDS BRICKS AND MORTAR PRESENCE WITH 300TH STORE Trade and DIY retailer Screwfix is now even more accessible for busy tradesmen on the move across the UK, with the launch of its 300th trade counter in Birstall, West Yorkshire. Screwfix started life as a mail order catalogue-based business, but in response to customers needing to get their tools quickly and conveniently, a rapid store expansion has followed, with 60 stores being opened in 2013 alone. The national store network now gives the nation’s tradesmen, which includes builders, plumbers and electricians, as well as serious DIY-ers, greater access to tools and supplies when on the move in-between jobs. Meeting this 300th store milestone is equally significant given that Screwfix opened its very first store just eight years ago in Yeovil, Somerset. This need for a fast and easy shopping experience has been boosted by an early adoption of a multi-channel model as Screwfix chief executive Andrew Livingston explains: “It really is a case of time is money for our customers because they are busy out and about on the road, from job to job. So we’re doing all we can to help them buy the tools and accessories they need as quickly and easily as possible. As we open the doors to more and more stores across the country, we become even more convenient for our customers. This, topped with our Click & Collect technology, mobile website and smartphone apps means that customers can shop when they want and how they want. “Tradesmen rely on us for the ease and speed of online and over-the-phone ordering, but they also enjoy the store experience thanks to regular – often daily - interaction with staff, many of whom have a background in the trade.” The 300th Screwfix store will open its doors in Birstall, West Yorkshire, joining 8 other stores across West Yorkshire. -

Hypermarket Lessons for New Zealand a Report to the Commerce Commission of New Zealand

Hypermarket lessons for New Zealand A report to the Commerce Commission of New Zealand September 2007 Coriolis Research Ltd. is a strategic market research firm founded in 1997 and based in Auckland, New Zealand. Coriolis primarily works with clients in the food and fast moving consumer goods supply chain, from primary producers to retailers. In addition to working with clients, Coriolis regularly produces reports on current industry topics. The coriolis force, named for French physicist Gaspard Coriolis (1792-1843), may be seen on a large scale in the movement of winds and ocean currents on the rotating earth. It dominates weather patterns, producing the counterclockwise flow observed around low-pressure zones in the Northern Hemisphere and the clockwise flow around such zones in the Southern Hemisphere. It is the result of a centripetal force on a mass moving with a velocity radially outward in a rotating plane. In market research it means understanding the big picture before you get into the details. PO BOX 10 202, Mt. Eden, Auckland 1030, New Zealand Tel: +64 9 623 1848; Fax: +64 9 353 1515; email: [email protected] www.coriolisresearch.com PROJECT BACKGROUND This project has the following background − In June of 2006, Coriolis research published a company newsletter (Chart Watch Q2 2006): − see http://www.coriolisresearch.com/newsletter/coriolis_chartwatch_2006Q2.html − This discussed the planned opening of the first The Warehouse Extra hypermarket in New Zealand; a follow up Part 2 was published following the opening of the store. This newsletter was targeted at our client base (FMCG manufacturers and retailers in New Zealand). -

Retail Change: a Consideration of the UK Food Retail Industry, 1950-2010. Phd Thesis, Middlesex University

Middlesex University Research Repository An open access repository of Middlesex University research http://eprints.mdx.ac.uk Clough, Roger (2002) Retail change: a consideration of the UK food retail industry, 1950-2010. PhD thesis, Middlesex University. [Thesis] This version is available at: https://eprints.mdx.ac.uk/8105/ Copyright: Middlesex University Research Repository makes the University’s research available electronically. Copyright and moral rights to this work are retained by the author and/or other copyright owners unless otherwise stated. The work is supplied on the understanding that any use for commercial gain is strictly forbidden. A copy may be downloaded for personal, non-commercial, research or study without prior permission and without charge. Works, including theses and research projects, may not be reproduced in any format or medium, or extensive quotations taken from them, or their content changed in any way, without first obtaining permission in writing from the copyright holder(s). They may not be sold or exploited commercially in any format or medium without the prior written permission of the copyright holder(s). Full bibliographic details must be given when referring to, or quoting from full items including the author’s name, the title of the work, publication details where relevant (place, publisher, date), pag- ination, and for theses or dissertations the awarding institution, the degree type awarded, and the date of the award. If you believe that any material held in the repository infringes copyright law, please contact the Repository Team at Middlesex University via the following email address: [email protected] The item will be removed from the repository while any claim is being investigated. -

Port, Sherry, Sp~R~T5, Vermouth Ete Wines and Coolers Cakes, Buns and Pastr~Es Miscellaneous Pasta, Rice and Gra~Ns Preserves An

51241 ADULT DIETARY SURVEY BRAND CODE LIST Round 4: July 1987 Page Brands for Food Group Alcohol~c dr~nks Bl07 Beer. lager and c~der B 116 Port, sherry, sp~r~t5, vermouth ete B 113 Wines and coolers B94 Beverages B15 B~Bcuits B8 Bread and rolls B12 Breakfast cereals B29 cakes, buns and pastr~es B39 Cheese B46 Cheese d~shes B86 Confect~onery B46 Egg d~shes B47 Fat.s B61 F~sh and f~sh products B76 Fru~t B32 Meat and neat products B34 Milk and cream B126 Miscellaneous B79 Nuts Bl o.m brands B4 Pasta, rice and gra~ns B83 Preserves and sweet sauces B31 Pudd,ngs and fru~t p~es B120 Sauces. p~ckles and savoury spreads B98 Soft dr~nks. fru~t and vegetable Ju~ces B125 Soups B81 Sugars and artif~c~al sweeteners B65 vegetables B 106 Water B42 Yoghurt and ~ce cream 1 The follow~ng ~tems do not have brand names and should be coded 9999 ~n the 'brand cod~ng column' ~. Items wh~ch are sold loose, not pre-packed. Fresh pasta, sold loose unwrapped bread and rolls; unbranded bread and rolls Fresh cakes, buns and pastr~es, NOT pre-packed Fresh fru~t p1es and pudd1ngs, NOT pre-packed Cheese, NOT pre-packed Fresh egg dishes, and fresh cheese d1shes (ie not frozen), NOT pre-packed; includes fresh ~tems purchased from del~catessen counter Fresh meat and meat products, NOT pre-packed; ~ncludes fresh items purchased from del~catessen counter Fresh f1sh and f~sh products, NOT pre-packed Fish cakes, f1sh fingers and frozen fish SOLD LOOSE Nuts, sold loose, NOT pre-packed 1~. -

SUPERMARKET ^^^^^^^^^^•K^^^^^^^^^^^^^^^^^^^^^^^^^^^K

:A"' Some of our friends • Ca:: n the service (le$k • Win a chancrtu «in a une JUNE ISSUE 1994 \ ••'•mSik vJ SAINSBURY Savacentre HmvilElllXSIE Sft/'JSa-/4^^/S FRONTLINE Just a call away Ever wondered who the faces are behind the service desk voices? Turn to page 12 to meet some of the people who solve your computer problems, and find out what they have in store to improve their service. NOT LEAST AMONC OUR DISCERNING Have you a four-legged friend at CUSTOMERS ARE MANV OF THE COUNTRY'S MILLIONS OF CATS AND DOCS. home? Half the households in Britain FULL TAIL ON PAGES 14/15. have a dog or cat, or both. On page 15 we introduce the pets of three Group directors...Is it true that pets look like their owners? H Morton's Reading Room has proved extremely popular. Congratulations to H Cowan of Hoddesdon depot - winner of the latest Book department opens WRITELINES quarterly SSA draw for £1,000. new chapter for Savacentre BRANCH OPENINGS: A new department at Merton Savacentre is devoted to books, EAST KILBRIDE and bargain books in CHINGFORD particular. Explains Chris TAPLOW Stevens, senior buyer and KIDDERMINSTER merchandise manager, SABRE UPDATE 'Previously we only sold books near the stationery, THE DAY WE WELCOMED OUR DAUGHTERS including the top 15 novels and the JS book SERVING THE SERVERS - range. Now we have WHAT'S NEW ON THE SERVICE DESK i around ten times the space and number of titles in the WIN A CHANCE TO Reading Room with its WIN THE POOLS 1 own upmarket library EXPLAINING CATS image. -

The Revitalized Castorama Store of Ormesson Is Testing Geopositioning with Pricer Search

The revitalized Castorama store of Ormesson is testing geopositioning with Pricer Search Guyancourt, January 25th, 2017. Castorama Ormesson is piloting the Pricer geopositioning solution and is offering its customers a kiosk through which they can easily search the products they are looking for. Locate a product using Infrared trilateration Pricer, the worldwide leader of electronic shelf label (ESL) digital solutions, has developed a unique application based on Infrared (IR) trilateration. The store’s ESLs reply to Pricer’s communication platform, each using a different signal strength enabling their geopositioning and therefore automatically providing the product’s position in the store. Easily find products with the Pricer Search kiosk Relying on the IR infrastructure of the Ormesson store, Pricer has implemented a kiosk allowing customers to easily locate products in the store. The kiosk combines an intuitive « article search » function and a digital map of the store. The automated solution greatly improves the customer’s experience in a DIY world where searching for products can be difficult. Geolocalize with Pricer’s unified platform Trilateration is one the most important components of Pricer’s digital solutions. The Pricer platform associates both hardware (SmartFLASH ESLs) and software solutions composing a unique value added offer which can be easily integrated in any IT environment. Automatic product geolocation provides a better customer experience. Pricer has won the Paris Retail Awards 2016 in the Customer Experience (360) category with its automatic product positioning solution for stores. About Castorama Castorama is part of Kingfisher plc, the European leader of home improvement which operates nearly 1,200 stores in 10 countries in Europe.