Experience Our Expertise Annual Report 2014-15

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Yes Bank Branch

YES BANK provides you an all-inclusive banking experience through an extensive network of 1000+ Branches Pan India. Always located at a convenient distance from your home or office, our state-of-the-art branches are designed to ensure a superior and consistent banking experience through aesthetics, high-quality service, and cutting-edge technology at all touch points. Click here to find your nearest ATM. Click here to find your nearest Retail Loans operation branch. Check the table below to find your nearest branch: Branch City Branch Address Pincode Code Ground & 1st Floor, Moti Mahal, Next to 1 Greater Mumbai City Bakery, Dr. Annie Beasant Road, 400018 Mumbai - 400 018 Fortune Global Arcade, Sikandarabad, 2 Gurgaon Mehrauli Gurgaon Road, Gurgaon, Haryana 122002 – 122 002 (New Address) : Plot No. 11/48, Shopping 3 New Delhi Centre, Diplomatic Enclave, Malcha Market, 110021 Chanakya Puri, New Delhi, PIN 110021 Premises No 1A, Ground Floor, Mittal Chambers, Plot no. 228 of Block no. III of 4 Greater Mumbai 400021 Backbay Reclamation, Nariman Point, Mumbai - 400 021 Ground Floor,143/1, Uthamar Gandhi Salai, 5 Chennai Nungambakkam High Road, Chennai - 600034 600034 Ground Floor, "Mayank Towers", Survey no. 6 Hyderabad 31 (Old). 31/2(New), Raj Bhavan Road, 500082 Somajiguda, Hyderabad - 500082 Unit No.G/3,102-103, "C.G.Centre”, 7 Ahmedabad 380009 C.G.Road, Ahmedabad - 380 009 Shop No. 1, 'Ivory Tower' , C.T.S. No. 8 Pune 39/6+39/7 out of final plot No. 36, Plot No. 6 411004 & 7, Prabhat road, Eradawane, Pune, Maharashtra 411 004 Gr+ Mezz, Corner Square, Race Course 9 Vadodara 390007 Circle, Baroda 390007 G1, Ground Floor, Valecha Chambers, Plot 10 Greater Mumbai B-6, New Link Road, Andheri (W), Mumbai 400053 400053 Gr. -

Changes in Jurisdictional Limits of Towns in Haryana: Legal and Administrative Aspects

RESEARCH PAPER Geography Volume : 5 | Issue : 9 | September 2015 | ISSN - 2249-555X Changes in Jurisdictional Limits of Towns in Haryana: Legal and Administrative Aspects Municipal towns, abolition, alteration of municipal limits, legal hassles, haphazard, urban KEYWORDS growth, stakeholders. Dr. Randhir Singh Sangwan Parul Rana Professor & Chairperson, Department of Geography Assistant Professor, Department of Geography Indira Gandhi University, Meerpur, Rewari (Haryana) Govt. College for Women, Faridabad (Haryana), India ABSTRACT Statutory towns governed through the municipal acts of respective state governments in India are known as municipal towns. Haryana Municipal Act, 1973 has laid down a broad framework with regard to clas- sification, constitution, functions and powers of municipal bodies. A close investigation of the Act reveals the over- riding powers of the state government with regard to constitution and abolition of a municipal body. With regard to alteration in the municipal limits too, the government tends to ignore the objections raised by the inhabitants of the affected area leading to legal hassles and inordinate delay in the expansion of municipal limits to contain haphazard urban growth on the periphery of towns in many instances. This paper is an attempt to analyse the legal and adminis- trative aspects of changes in jurisdictional limits of towns in Haryana and conflict of interests of various stakeholders in the process of alteration of municipal limits. Introduction tional Amendment Act (CAA) is a milestone in the history In India, all those settlements which are towns by virtue of urban governance. The aim of the 74th CAA is to ensure of a statutory notification are known as municipal towns. -

Alphabetical List of Towns and Their Population

ALPHABETICAL LIST OF TOWNS AND THEIR POPULATION HARYANA 1. Ambala (M Cl ) [HAR, Population: 139279, Class - I] 2. Ambala UA [HAR, Population: 168316, Class - I] 3. Asankhurd (CT) [HAR, Population: 8066, Class - V] 4. Assandh (MC) [HAR, Population: 22707, Class - III] 5. Ateli (MC) [HAR, Population: 5673, Class - V] 6. Babiyal (CT) [HAR, Population: 21644, Class - III] 7. Bahadurgarh UA [HAR, Population: 131925, Class - I] 8. Barwala (MC) [HAR, Population: 33132, Class - III] 9. Bawal (MC) [HAR, Population: 12144, Class - IV] 10. Bawani Khera (MC) [HAR, Population: 17424, Class - IV] 11. Beri (MC) [HAR, Population: 16162, Class - IV] 12. Bhiwani (M Cl ) [HAR, Population: 169531, Class - I] 13. Bilaspur (CT) [HAR, Population: 9621, Class - V] 14. Buria (MC) [HAR, Population: 9830, Class - V] 15. Charkhi Dadri (MC) [HAR, Population: 44895, Class - III] 16. Cheeka (MC) [HAR, Population: 32128, Class - III] 17. Chhachhrauli (MC) [HAR, Population: 9710, Class - V] 18. Dharuhera (CT) [HAR, Population: 18892, Class - IV] 19. Dundahera (CT) [HAR, Population: 10626, Class - IV] 20. Ellenabad (MC) [HAR, Population: 32795, Class - III] 21. Farakhpur (CT) [HAR, Population: 8740, Class - V] 22. Faridabad (M Corp.) [HAR, Population: 1055938, Class - I] 23. Farrukhnagar (MC) [HAR, Population: 9521, Class - V] 24. Fatehabad (MC) [HAR, Population: 59917, Class - II] 25. Ferozepur Jhirka (MC) [HAR, Population: 17755, Class - IV] 26. Ganaur (MC) [HAR, Population: 29006, Class - III] 27. Gharaunda (MC) [HAR, Population: 30172, Class - III] 28. Gohana (MC) [HAR, Population: 48532, Class - III] 29. Gurgaon UA [HAR, Population: 228820, Class - I] List of towns: Census of India 2001 Haryana – Page 1 of 4 HARYANA (Continued): 30. -

International Journal of Research in Informative Science Application & Techniques (IJRISAT) 1 Global Traffic: Discourses

International Journal of Research in Informative ISSN-2581-5814 Science Application & Techniques (IJRISAT) 1 Global Traffic: Discourses and Practices of Trade in English Literature and Culture from 1550 to 1700 (review) DR. ASHOK KUMAR, ASSTT. PROFESSOR, DEPT. OF ENGLISH, G. C. SATNALI DR. SANEH LATA, ENGLISH TEACHER, G. M. S. REWASA MONIKA, RESEARCH SCHOLAR, Singhania University, Pacheri Bari (Raj.) Abstract In the century and a half after 1550, England experienced a variety of economic and cultural changes in the wake of its expanding international trade. This period saw developments as diverse as joint stock companies, advanced map-making techniques, and the creation of maritime insurance to protect investors. But, as this volume makes clear, the changes in the period were more broadly cultural than technological. Building on recent work exploring the place of England within developing systems of global exchange, Global Traffic illuminates the myriad ways that trade became increasingly central not just to the economy but to the changing self-imagination of the English nation. In its varied explorations of travel, exploration, emergent nationalism, imperialism, and incipient colonialism in the early modern period, this collection clarifies the epistemological and discursive shifts through which the abstract world of trade became increasingly central to the wider English culture. In the first section on the new epistemologies of trade, Daniel Vitkus sets the scene by exploring how the overseas maritime trade, underwritten by investors in London, spread over the globe, and how this new global role of the English nation was remained on the London stage. 2 Indian Roads, Traffic Problems and The Common Man Rekha Bai, Rersearch Scholar Singhania University, Pacheri Bari (Raj) SUNITA KUMARI, EXTENSION LECTURER, BAIJNATH COLLEGE, NANGAL CHAUDHARY Abstract India is a country with the second largest road network in the world. -

Volume 6: Environment Assessment Reports – Sub-Projects

Technical Assistance Consultant’s Report Project Number: 41598 April 2010 India: National Capital Region Planning Board Project (Financed by the Japan Special Fund) Volume 6: Environment Assessment Reports – Sub-Projects Prepared by Sheladia Associates, Inc. USA For National Capital Region Planning Board This consultant’s report does not necessarily reflect the views of ADB or the Government concerned, and ADB and the Government cannot be held liable for its contents. (For project preparatory technical assistance: All the views expressed herein may not be incorporated into the proposed project’s design. TA 7114-IND NATIONAL CAPITAL REGION PLANNING BOARD PROJECT Medium Term Strategic Evolution and Borrowers Assessment ENVIRONMENT ASSESSMENT REPORTS ON SUB PROJECTS April 2010 Asian Development Bank Submitted To : National Capital Re ion Plannin Board Prepared By : Sheladia Associates Inc, USA Final Report : VOLUME - VI TA 7114-IND National Capital Region Planning Board Final Report Project cts Sub Proje – TABLE OF CO TE TS A – PATAUDI WATER SUPPLY PROJECT B - PATAUDI SEWERA(E PROJECT C - DEVELOPME T OF MULTI-MODEL TRA SIT CE TRE AT A A D VIHAR, CTD Environmental Assessment Report D. BADLI BYPASS – E.CO STRUCTIO OF VARIOUS ROADS I SO EPAT DISTRICT Volume 6 F. REHABILITATIO OF 1. ROADS I JHAJJAR DISTRICT (. DEVELOPME T OF MULTI-MODEL TRA SIT CE TRE AT SARAI /ALE /HA Sheladia Associates, Inc. USA TA 7114-IND National Capital Region Planning Board Final Report Project Environmental Assessment Document Sub Projects Sub – A. PATAUDI ATER SUPPLY PRO$ECT Environmental Assessment Report – Volume 6 The Environmental A e ment i a document of the borrower. -

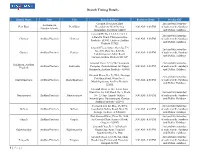

Branch Timing Details

Branch Timing Details Branch Name State City Branch Address Business Hours Weekly Off Ground Floor And First 2nd and 4th Saturday Andaman & Port Blair Port Blair Floor,Survey No 104/1/2, 9:30 AM - 3:30 PM of each month, Sundays Nicobar Islands Junglighat, Port Blair 744103 and Public Holidays Ground Flr No 8-8-1,8-8-2 & 8-8- 2nd and 4th Saturday 3,Gandhi Road, Chittoorandhra Chittoor Andhra Pradesh Chittoor 9:30 AM - 4:30 PM of each month, Sundays Pradesh - 517001 Chittoor Andhra and Public Holidays Pradesh 517325 Ground Floor, Satya Akarsha, T S 2nd and 4th Saturday No. 2/5, Door No. 5-87-32, Guntur Andhra Pradesh Guntur 9:30 AM - 4:30 PM of each month, Sundays Lakshmipuram Main Road, and Public Holidays Guntur,Andhra Pradesh 522 007 Ground Floor, 2/27/14-2 Koppana 2nd and 4th Saturday Kakinada, Andhra Andhra Pradesh Kakinada Complex, Gokula Street, Sri Nagar, 9:30 AM - 4:30 PM of each month, Sundays Pradesh Kakinada, Andhra Pradesh - 533003. and Public Holidays Ground Floor, No. 7/473-1, Godugu 2nd and 4th Saturday Pet Main Road, Ward No.7, Machilipatnam Andhra Pradesh Machilipatnam 9:30 AM - 4:30 PM of each month, Sundays Machilipatnam, Andhra Pradesh and Public Holidays 521001 Ground Floor, H. No. 9-9-2, New Ward No. 16, Old Ward No. 4, Block 2nd and 4th Saturday Narsaraopet Andhra Pradesh Narasaoropet No. 2, Opp. Angele Talkies, 9:30 AM - 3:30 PM of each month, Sundays Arundalpeta, Narasaraopet, Guntur, and Public Holidays Andhra Pradesh – 522601. -

Form 9 Pataudi

8/8/2019 Form9 Print ANNEXURE 5.8 (CHAPTER V, PARA 25) FORM 9 List of Applications for inclusion received in Form 6 Designated location identity (where Constituency (Assembly/£Parliamentary): PATAUDI(SC) Revision identity applications have been received) From date To date @ 2. Period of applications (covered in this list) 1. List number 01/08/2019 01/08/2019 3. Place of hearing* Serial Name of Father / Mother / $ Date of Name of Date of Time of number Husband and Place of residence of receipt claimant hearing* hearing* (Relationship)# application 1 01/08/2019 Shivam Abhey singh (F) 376, near airtel tower, Nanu kalan, , GURGAON MAMTA 01, WARD NO 8 JAIDEV COLONY, HAILY 2 01/08/2019 JOGINDER SINGH (H) YADAV MANDI, , GURGAON PRASHANT SATYA SWAROOP 127, MEHCHANA, FARRUKH 3 01/08/2019 CHAUHAN CHAUHAN (F) NAGAR, , GURGAON PRIYA 127, MEHCHANA, FARUKH NAGAR 4 01/08/2019 SATYA SWAROOP (F) CHAUHAN , , GURGAON BHANU SATYA 127, MEHCHANA, FARRUKH NAGAR 5 01/08/2019 PRATAP SWAROOP CHAUHAN (F) , , GURGAON CHAUHAN Mohinder Singh 6 01/08/2019 Jagdish Chander (F) 101, Ward No 7 , Tajnagar , , GURGAON 7 01/08/2019 ASHA MOHINDER SINGH (H) 101, TAJNAGAR, TAJNAGAR, , GURGAON 8 01/08/2019 Priyanka yadav rahul yadav (H) 41, jamalpur, jamalpur, , GURGAON 9 01/08/2019 BIMLA DEVI JAGMAL SINGH (H) 243, jamalpur, jamalpur, , GURGAON 10 01/08/2019 RAHUL JAGAT SINGH (M) 243, jamalpur, jamalpur, , GURGAON 11 01/08/2019 PUSHPA DEVI MADAN (H) 302, jamalpur, jamalpur, , GURGAON 12 01/08/2019 REETU RANI MANJEET KUMAR (H) 44/3, JAMALPUR, JAMALPUR, , GURGAON SANTOSH 13 01/08/2019 -

APPLICATION FORM and State Board Technical Education, Haryana Rs

Approved by AICTE, New Delhi and Director Technical Education, Haryana Affiliated to Maharishi Dayanand University, Rohtak APPLICATION FORM and State Board Technical Education, Haryana Rs. 500/- Please read carefully before you fill this application form. (a) Please fill the application form in CAPITAL Letters in Blue/Black ink. (b) It is your responsibility to ensure that the application with necessary certificates/testimonials is received by Photgraph BM Group of Institutions before the closing date. (c) Filling of the Form does not guarantee admission to the College. (d) Computer generated form will be accepted along with the application form fee either in cash or DD in favor of BM College of Tech. & Mgmt. / BM Group of Institutions, payable at Gurgaon. 1. COURSES / PROGRAMMES M.Tech B.Tech Diploma Mgmt. /Others Computer Science & Engineering Computer Science & Engineering Mechanical Engineering BBA Mechanical Engineering Electronics & Comm. Engineering Electrical Engineering BCA MBA Electrical & Electronics Engineering Civil Engineering HR IB IT Mechanical Engineering B.Tech/Diploma Admission Year 1st Year 2nd Year Finance Marketing Civil Engineering 2. PERSONAL DETAILS Day Month Years Gender: Male Female Da te of Birth Student's Name: Father's/Husband Name: Mother's Name: Correspondence Address: City: State: Pin Code: Mob: (Resi.)Tel: Nationality: E-mail Address: 3. ACADEMIC QUALIFICATIONS Year Qualification Subject University/Board/Institution % of Marks obtained From To X XII Graduation Post Graduation Other (Please Specify) CAMPUS : 5th KM Stone, Farukhnagar-Haileymandi Road, Distt. Gurgaon-122506(Haryana) Ph: 0124-3290534, 2015524, e-mail: [email protected] url: www.bmctm.com 4. DETAILS OF MARKS IN QUALIFYING EXAMINATION (For B.Tech course only) Subjects Max. -

4.1 Demography

Preparation of Sub Regional Plan for Haryana Sub-Region of NCR-2021: Interim Report -II Chapter 4 : DEMOGRAPHIC PROFILE AND SETTLEMENT PATTERN 4.1 Demography 4.1.1 Population distribution & density The Haryana Sub Region comprises of an area of 13428 sq. km. with a total population of 8.7 million. This amounts to 30.4% area & 41.14% Population of Haryana State. The average density of the region (647 person per sq.km.) is more than the state average of 478. The more dense areas with in the region are- Faridabad , Panipat & Gurgaon . The lowest density in the region is that of Mewat followed by Rohtak. Table 4-1 : District wise demographic details of Haryana Sub-Region befor creation of Palwal Total Population density Urbanization Districts Area (Sq KM) Household size Population (Persons/Sq Km) (%) Panipat 1268 967449 763 40.5 5.5 Sonipat 2122 1279175 603 25.1 5.7 Rohtak 1745 940128 539 35.1 5.6 Jhajjar 1834 880072 480 22.2 5.6 Rewari 1594 765351 480 17.8 5.6 Gurgaon 1254 870539 694 35.6 6.1 Faridabad 1752 1990719 1136 60.8 5.6 Mewat 1859 993617 534 7.5 7.5 Source: Census 2001, Statistical abstract haryana 2006-07 Scott Wilson India Page 4-1 Preparation of Sub Regional Plan for Haryana Sub-Region of NCR-2021: Interim Report -II Now after the division of Mewat from Gurgaon and Palwal from Faridabad we get the following demographic scenario : Table 4-2 : Demographic details of Gurgaon district Tehsil Area Population Literates (Sq.Km) Total Male Female Rural Urban Total Male Female Gurgaon 738.82 629508 342527 286981 380541 248967 433150 258969 -

ANNEXURE 5.8 (CHAPTER V, PARA 25) FORM 9 List of Applica Ons For

ANNEXURE 5.8 (CHAPTER V, PARA 25) FORM 9 List of Applicaons for inclusion received in Form 6 Designated locaon identy (where Constuency (Assembly/£Parliamentary): PATAUDI(SC) Revision identy applicaons have been received) From date To date @ 2. Period of applicaons (covered in this list) 1. List number 01/12/2020 01/12/2020 3. Place of hearing* Serial $ Date of Name of Name of Father / Mother / Date of Time of number Place of residence of receipt claimant Husband and (Relaonship)# hearing* hearing* applicaon ASHWANI 1 01/12/2020 SHARMA MUKESH SHARMA SHARMA (F) 154, SHERPUR, SHERPUR, , GURGAON Sharma 25, WARD NO 3, HAILY 2 01/12/2020 AFREED MUNNA (F) MANDI, , GURGAON SANTRA 3 01/12/2020 JOGINDER (H) NA, NA, BAS PADAMKA, , GURGAON KUMARI Manish HN 101, Vill TajNagar ramkaran ki 4 01/12/2020 Kumar Renu singh (O) dhani, Girgaon, , GURGAON Kumar DJ 73, WARD NO 5 01/12/2020 SARITA Gautam (H) 10, pataudi, , GURGAON SEEMA 322, NA, DHANI SHANKAR 6 01/12/2020 RAN SINGH (F) YADAV WALI, , GURGAON ANGOORI 01, NA, DHANI SHANKAR 7 01/12/2020 JAGDISH (H) DEVI WALI, , GURGAON JYOTI 00, 00, DHANI CHITTER SAIN 8 01/12/2020 YADAV KHAJAN SINGH (H) , , GURGAON YADAV HIMANI House no-1, ward no -8, Haily Mandi 9 01/12/2020 PRATEEK VATS (H) SHARMA , , GURGAON 10 01/12/2020 NIKITA RAJKUMAR (H) 73b, NURPUR, NURPUR, , GURGAON 39, shiv mandir , HARINAGAR dooma 11 01/12/2020 aradhana Vijay pal (F) , , GURGAON JIVANI 118, NANU KALA, NANU 12 01/12/2020 NARESH NARESH (H) JIVANI KALA, , GURGAON 151, NEAR SHIV 13 01/12/2020 GUNJAN HEMANT (H) MANDIR, BASUNDA, , GURGAON -

“Building the Best Quality Bank of the World in India”

AnnuA l RepoR t 2013-14 “Building The BesT QualiTy Bank Of The WOrld in india” PDF processed with CutePDF evaluation edition www.CutePDF.com Contents Corporate Overview ................... 1-38 Statutory Reports ................... 90-142 About Us ...................................................................2 Management Discussion and Analysis .....................90 Highlights 2013-14 ...................................................3 Directors’ Report ................................................. 116 Message from the Non-Executive Chairman ...............4 Report on Corporate Governance ......................... 126 Managing Director and CEO’s communiqué...............6 Business excellence .................................................12 Financial Statements ............ 143-223 Enduring relationship .............................................14 Standalone Financial Statements Human capital management ..................................16 Independent Auditors’ Report .............................. 144 Processes and quality excellence ..............................18 Balance Sheet ...................................................... 146 Technology .............................................................20 Profit and Loss Account ....................................... 147 Robust risk management ........................................22 Cash Flow Statement ........................................... 148 Responsible banking ...............................................24 Schedules ........................................................... -

Haryana Sub Regional Plan

Sub-Regional Plan for Haryana Sub-Region of NCR-2021 Chapter 3 Aims, Objectives and Policy Zones Chapter 3 : AIMS, OBJECTIVES AND POLICY ZONES 3.1 Aims The State of Haryana, which is located in the heart of north India and surrounds Delhi on three sides, is one of the most progressive States in the nation. Its location with respect to the National Capital has given it an edge above any other state in India. Additionally, Haryana’s human resource has the dynamism to exploit this advantage and the state’s resources and potential to attract investments specifically in areas of comparative advantage. These specific areas consist of industrialization in the state, propagation of Leading edge technology through the private sector and to promote education in all spheres. For the nine districts of Haryana that lie in the NCR, a conducive strategy could be developed. The key elements to become the basis of this strategy are: o To promote industrialization both in the organized and small-scale sector, particularly those with backward linkages to agriculture and forest resources; hence it is imperative to strike a balance with the large pool of resources o To be in line with the state policy, leading edge technologies and sunrise industries in the State, especially Information Technology and Biotechnology o Public/private sector involvement in various sectors to be encouraged in the State o To develop Haryana as a premier education and research centre by leveraging the presence of world- class research and technical institutes. o Finally, the objective is to exploit its proximity to the National Capital Territory of Delhi, NCTD (presence of large urban and industrial clusters).