Food Processing Ingredients Sector Report Czech Republic

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Schreiber Foods, Inc

+44 20 8123 2220 [email protected] Schreiber Foods, Inc. - Strategy, SWOT and Corporate Finance Report https://marketpublishers.com/r/SD126B7CC8AEN.html Date: December 2020 Pages: 33 Price: US$ 175.00 (Single User License) ID: SD126B7CC8AEN Abstracts Schreiber Foods, Inc. - Strategy, SWOT and Corporate Finance Report Summary Schreiber Foods, Inc. - Strategy, SWOT and Corporate Finance Report, is a source of comprehensive company data and information. The report covers the company's structure, operation, SWOT analysis, product and service offerings and corporate actions, providing a 360? view of the company. Key Highlights Schreiber Foods, Inc. (Schreiber or 'the company') is an employee-owned dairy company. Its dairy foods include yogurt, cheese, shelf stable juice and milk, ghee, dairy desserts, sour cream, ice cream, custard desserts, reduced-fat cheese curd and powders including skim-milk powder, organic whey-protein powder and whole-milk powder. The company caters its products to retailers, distributors, restaurants, and food manufacturers. It also provides insights to customer trends, risk management, help customers create marketing tools and dairy foods export across the world. It has production and distribution facilities in Austria, Bulgaria, Brazil, Czech Republic, Germany, India, Mexico, Spain, Portugal, France and the US. The company is headquartered in Green Bay, Wisconsin, the US. Scope Detailed information on Schreiber Foods, Inc. required for business and competitor intelligence needs Schreiber Foods, Inc. - Strategy, SWOT and Corporate Finance Report +44 20 8123 2220 [email protected] A study of the major internal and external factors affecting Schreiber Foods, Inc. in the form of a SWOT analysis An in-depth view of the business model of Schreiber Foods, Inc. -

USA OIL ASSOCIATION (NAOOA) Building C NEPTUNE NJ 07753

11.12.2017 LISTE DES EXPORTATEURS ET IMPORTATEURS D’HUILES D’OLIVE, D’HUILES DE GRIGNONS D’OLIVE ET D’OLIVES DE TABLE LIST OF EXPORTERS AND IMPORTERS OF OLIVE OILS, OLIVE-POMACE OILS AND TABLE OLIVES UNITED STATES OF AMERICA/ÉTATS-UNIS D’AMÉRIQUE ENTITÉ/BODY ADRESSE/ADDRESS PAYS/ WEBSITE COUNTRY NORTH AMERICAN OLIVE 3301 Route 66 – Suite 205, USA www.naooa.org OIL ASSOCIATION (NAOOA) Building C NEPTUNE NJ 07753 ACEITES BORGES PONT, S.A. Avda. J. Trepat s/n SPAIN 25300 TARREGA (Lleida) ACEITES DEL SUR, S.A. Ctra. Sevilla-Cádiz, Km. SPAIN www.acesur.com 550,6 41700 DOS HERMANAS (Sevilla) ACEITES TOLEDO S.A. Paseo Pintor Rosales, 4 y 6 SPAIN www.aceitestoledo.com 28008 MADRID ACEITUNAS DE MESA S.L. Antiguo Camino de Sevilla SPAIN s/n 41840 PILAS (Sevilla) ACEITUNAS GUADALQUIVIR Camino Alcoba, s/n SPAIN www.agolives.com S.L. 41530 MORON DE LA FRONTERA (Sevilla) ACEITUNAS MONTEGIL, S.L. Eduardo Dato, 9 SPAIN www.aceitunasmontegil.es 41530 MORON DE LA FRONTERA (Sevilla) ACEITUNAS RUMARIN S.A. Calle Pedro Crespo, 79 SPAIN 41510 MAIRENA DEL ALCOR (Sevilla) ACEITUNAS SEVILLANAS Calle Párroco Vicente Moya, SPAIN S.A. 14 41840 PILAS (Sevilla) ACTIVIDADES OLEICOLAS, Autovia Sevilla-Cádiz, Ctra. SPAIN www.acolsa.es S.A. IV Km. 550-600 41703 DOS HERMANAS (Sevilla) AEGEAN STAR FOOD Kral Incir Isletmesi TURKEY www.aegeanstar.com.tr INDUSTRY TRADE LTD. Dallica Mevkii 09800 NAZ AGRICOLA I CAIXA Calle Sindicat, 2 SPAIN www.coopcambrils.com AGRARIA SC CAMBRILS 43850 CAMBRILS SCCL (Tarragona) 2 ENTITÉ/BODY ADRESSE/ADDRESS PAYS/ WEBSITE COUNTRY AGRITALIA S.R.L. -

Schreiber Foods Overview

SCHREIBER FOODS OVERVIEW More Than Great Cheese. Much More. More Than Great Cheese. Much More. Schreiber History More Than Great Cheese. Much More. 3 Schreiber Foods In business for almost 70 years with ability and desire to grow Created in 1945 with Head office in Green Bay, Wisconsin One of the largest worldwide milk producer Schreiber’s Home Office in Green Bay, Wisconsin • Plants in 2017: 15 U.S. plants and 10 distribution centers (Wisconsin, Missouri, Pennsylvania, Georgia, Texas, Arizona, California) 15 International plants (India (3), Germany, France (2), Belgium, Mexico, Brazil, Bulgaria, Czech Republic, Portugal, Spain (2) , Tenerife; Over 8,000 partners worldwide More Than Great Cheese. Much More. Our Products More Than Great Cheese. Much More. Our Customers More Than Great Cheese. Much More. Schreiber Foods Bulgaria More Than Great Cheese. Much More. Schreiber Foods Bulgaria Information History: • The Plant is built 1964 & located in Sofia, close to the city center, in an industrial zone . • On 30.01.2014 Schreiber Foods bought the Plant; Land: 31 105m2; Capacity: current Plant capacity of 55 kt/ y; end game – 72kt/y More Than Great Cheese. Much More. Schreiber Foods Bulgaria Products: 5 different Yoghurt technologies capable in our plant: currently, production of 32 white masses and 100 SKU’s : Set yoghurt according to BDS ( Bulgarian Government Standard) Set yoghurt Stirred yoghurt – plain, with fruits and with flavors Drinkable yoghurt Milk with Extended shelf life (sterile process) – plain & choco milk 1 Non Dairy aseptic technologies capable in our plant: currently, production of 5 white masses and 5 SKU’s : More Than Great Cheese. -

Responsibilities

2017-2018 responsibilities WELCOME OUR COMPANY OUR PEOPLE OUR FOOD OUR EARTH OUR COMMUNITIES our company what does it take to be the best customer-brand dairy company in the world? First and foremost, it means ensuring the food we make is always safe for people That’s why we’ve joined others to support the United Nations Sustainable everywhere to enjoy. It also means doing business in a way that’s good for our Development Goals. Look for these icons throughout our fourth Responsibility people, our earth and our communities. Serving the common good is part of who Report to see how our activities will help build a better world by 2030. We’re we are, as a company and as individuals. proud to play a role in addressing the world’s greatest challenges. LEARN MORE about the United Nations Sustainable Development Goals Together, we can make the world a better place. 2 WELCOME OUR COMPANY OUR PEOPLE OUR FOOD OUR EARTH OUR COMMUNITIES our company 1945 1962 TODAY Our company L.D. Schreiber was founded in agreed to sell 49 Green Bay, Wisconsin, percent of the where our global company to 13 headquarters employees who remains today. were responsible for the growing success of the company and wanted a stake in the business. our VISION Our vision is to be the best customer-brand dairy company in the world. We’ll achieve this by creating sustainable value for our customers as a modern, global partner delivering exceptional quality, service, innovation and insight – all while enriching lives around the globe. -

Our Responsibilities 2015-16

OUR RESPONSIBILITIES 2015-16 Our COMPANY Our PEOPL E Our FOOD COMPANY Our EARTH Our Our COMMUNITIES 1 GREETINGS “As we continue on our path I am honored to share our third Responsibility Report with you and I’m also pleased to be the best to report that we continue to make meaningful progress toward achieving our near and long-term responsibility goals. customer-brand dairy company As we continue on our journey to be the best customer-brand dairy company in the world, you have my word that we remain deeply committed to ensuring that the in the world, we food we make is always safe for people around the world to enjoy. And since our last remain steadfast report was published, we have only amplified our efforts to operating our company in in our resolve to a way that is good for our people, our communities and our earth. ensure the food Over the last few years, it has been a joy for me to see how our partners around we provide is the globe have wholly embraced our efforts to be a more sustainable company. I hope you will see our partners’ passion for improvement and desire to do good for always safe for humanity reflected in the stories and results shared in this report. people to enjoy everywhere.” Mike Haddad, VIDEO: President and CEO A MESSAGE FROM MIKE HADDAD Mike Haddad President and CEO Schreiber Foods E H RT OOD F EA PEOPL Our Our COMPANY Our Our COMMUNITIES Our 2 OUR COMPANY 1945 1962 TODAY Our company was L.D. -

MFDS Draft List of Grandfathered Livestock Facility Plants (Dairy)

MFDS Draft List of Grandfathered Livestock Facility Plants (Dairy) - United States (Plants with a history of export of livestock products from June 1998 - February 3, 2016) WHETHER A FOOD SAFETY MA N A G E ME N T L I NE NAME OF ESTABLI SHMENT C ODE ADDRE S S REMARKS SYSTEM APPLI ES( HACCP, I SO22000. et c) 1 ABBOTT LABORATORIES A0370 625 CLEVELAND AVENUE, COLUMBUS U.S.A. 2 ABBOTT LABORATORIES A0681 1015 DISTRIBUTORS ROW, HARAHAN, LA 3 ABBY`S QUALITY FOODS A1835 75-178 GERALD FORDDRIVE STE 1-A PALM DESERT, CA 92211 4 ADVANCED FOODS R0725 1211 EAST NOBLE AVENUE, VISALLA, CA PRODUCTS LLC 93292 5 AGRI-MARK INC. A1495 39 MCCADAM LANE, CHATEAUGAY, NY GFSI SQF Level 3 12920 (PLANT #36-8620) 6 AGRI-MARK INC. A5008 950 RIVERDALE ST, WEST SPRINGFIELD, GFSI SQF Level 3 MA 01089 (PLANT #25-18) 7 AGRI-MARK, INC.(PLANT 50- A1507 869 EXCHANGE STREET, MIDDLEBURY, GFSI SQF Level 3 40) VT 05753 8 AGROPUR INC T1569 2701 FREEDOM ROAD, APPLETON, WI HACCP 54913 (PLANT NO. #55-1539) 9 AGROPUR INC. A1897 200 MAIN STREET SE, PRESTON, MN HACCP 55965, U.S.A. 10 AGROPUR INC. T1336 105 E 3RD AVE., HACCP WEYAUWEGA,WISCONSIN 54983 (55- 1410) 11 AGROPUR M1006 2340. ENTERPRISE AVE LA CROSSE HACCP INGREDIENTS(#55-8822) WISCONSIN U.S.A(구.MAIN STREET INGREDIENT) 12 AGROPUR, INC A1731 332 DIVISION STREET HULL, IOWA 51239 HACCP 13 ALAMANCE FOODS INC A0765 BURLINGTON NC 27216-2690 U.S.A.PLT NO.3746 14 ALCAM CREAMERY CO., INC A1841 142 EAST HASELTINE ST., HACCP, SQF Level 2 RICHLANDCENTER, WI 53581 (PLANT 55- 358) 15 ALL AMERICAN DAIRY A1707 100 DEERFIELD LANE SUITE 250 PRODUCTS, INC MALVERN, PA 19355 Page 1 of 23 WHETHER A FOOD SAFETY MA N A G E ME N T L I NE NAME OF ESTABLI SHMENT C ODE ADDRE S S REMARKS SYSTEM APPLI ES( HACCP, I SO22000. -

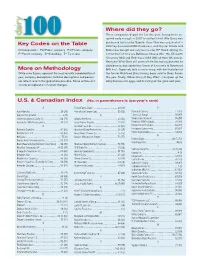

Key Codes on the Table More on Methodology Where Did They

Where did they go? Three companies depart the list this year, having been ac- quired early enough in 2007 to not be listed. Alto Dairy was Key Codes on the Table purchased last year by Saputo, Cass Clay was acquired at in 2007 by Associated Milk Producers, and Crystal Cream and C=Cooperative Pu=Public company Pr=Private company Butter was bought out early last year by HP Hood. Joining the P=Parent company S=Subsidiary T= Tie in rank list for the first time are BelGioso Cheese (No. 75), Ellsworth Creamery (84) and Roth Kase USA (96) all from Wisconsin. Next year Winn-Dixie will come off the list, having divested its dairy processing capabilities (some of it recently to Southeast More on Methodology Milk Inc.). Supervalu tells a similar story, with the final plant of While sales figures represent the most recently completed fiscal the former Richfood Dairy having been sold to Dean Foods year, company descriptions, facilities descriptions and person- this year. Finally, Wilcox Dairy of Roy, Wash., has given up the nel reflect recent changed where possible. Some entries will dairy business for eggs, and its listing will be gone next year. include an explanation of recent changes. U.S. & Canadian Index (No. in parentheses is last year’s rank) A Foster Farms Dairy ....................................... 50 (48) P Agri-Mark Inc. .............................................. 29 (29) Friendly Ice Cream Corp. ...............................55 (56) Parmalat Canada .........................................12 (13) Agropur Cooperative .........................................6 (9) G Perry’s Ice Cream ........................................ 97 (97) Anderson Erickson Dairy Co. ......................... 66 (71) Glanbia Foods Inc. ........................................ 23 (32) Plains Dairy Products ....................................95 (99) Associated Milk Producers Inc. -

January 2021 List of U.S. Dairy Product Manufactures/Processors Eligible to Export to Chile

January 2021 List of U.S. Dairy Product Manufactures/Processors Eligible to Export to Chile Establishment Name Factory Number Products Address Contact Phone Fax Email Nasonville Dairy 55-1499 Dairy 10898 Hwy 10 West, Marshfield, WI, 54449 Sars Griesbach 001 715 6762177 [email protected] Great Lakes Cheese of New York 1311323 Dairy 23 Phelps St, Adams, NY, 13605 Nathalie Seiler 001 440 8343509 001 440 8341002 [email protected] Michigan Milk Producers Association 1810166 Dairy 125 Depot St, Constantine, MI, 49042 Dave Davis 001 269 4352835 Ext: 322 [email protected] Glanbia Performance Nutrition (Manufacturing), Inc 3002591065 Dairy 600 N Commerce St, Aurora, IL, 60504 Elizabeth Balsavich 001 630 2567400 Ext: 7508 001 331 2146037 [email protected] Continental Dairy Facilities Southwest, LLC 3014391005 Dairy 1926 Fm 54, Littlefield, TX, 79339 Jose Villegas 001 855 3781835 Ext: 0613 [email protected] Leprino Foods Company 3009096698 Dairy 1302 1st Ave, Greeley, CO, 80631 Larry Rasmussen 001 303 6002514 [email protected] High Desert Milk 16-45 Dairy 1033 Idaho St, Burley, ID, 83318 Karla Robinson 001 208 8786455 [email protected] Agropur, inc. 2116532 Dairy 719 North Main Street, Le Sueur, MN, 56058 Wyatt Reyerson 001 952 9140400 001 952 9140887 [email protected] Maple Island, Inc. 2123454 Dairy 335 Wisconsin Ave, Medford, WI, 54451 Michelle Swigart 001 651 7732668 [email protected] Foremost Farms USA 2127681 Dairy 220 Saint Paul St SW, Preston, MN, 55965 Amy Rogers 001 608 3558659 [email protected] Wiskerchen Cheese, Inc 2118351 Dairy 5710 County Road H, Auburndale, WI, 54412 John Wiskerchen 001 715 6522333 [email protected] Agropur, inc. -

Ron Dunford Was Named President and CEO of Schreiber Foods in Should Articulate What Those Values Adapt to Evolving Consumers but Do So 2019

CHEESE MARKET NEWS® — March 6, 2020 Ron Dunford was named president and CEO of Schreiber Foods in should articulate what those values adapt to evolving consumers but do so 2019. He is Schreiber’s eighth president and CEO. are. Hoever, it’s more than words on in a well-coordinated fashion so we’re Dunford has more than 35 years of experience in the dairy industry with a plaque or statements on a wall; our not just chasing fads. Additionally, roles in operations, sales/marketing and general management. He joined “core values” are represented and never believe in “good enough,” and Schreiber Foods in 1996 at the Green Bay, Wisconsin, home offi ce. He was communicated by our actions. Oth- always be looking to solve the custom- named a vice president in 2000, senior vice president in 2002, president ers will calibrate the appropriateness er’s problem, not yours. and chief operating offi cer of Schreiber chain sales in 2003, president and of their own behavior based on the chief operating offi cer, operations, in 2006, and president Schreiber US in actions of the leader. 2014. Additionally, he was elected to the Schreiber Foods board of direc- tors in 2003. What would you cite as an During his tenure, Dunford has helped set the vision and execute the They say “you learn from example of a time where your mistakes” …. please Q your company showed strategy that has resulted in company records for revenue, volume, profi t, product quality and safety. He also led the implementation of process ex- Q share an example where innovation and leadership in the cellence, lean manufacturing, the utilization of risk management tools and this was relevant for you? dairy marketplace? the integration of new product categories into the company. -

Missouri Advantages for the Food Processing Industry

Missouri advantages for the food processing industry Located in the heart of the nation’s agricultural production—and with a transportation network that can get product to market quickly—Missouri has the right ingredients for success in the food processing industry. While several major food-related businesses have already made Missouri their home, the state has the resources to support many more. 5 reasons to Locate a food processing coMpany in Missouri ▪ 2 5 reasons to locate a food processing company in Missouri: “The State of Missouri and the local communities in which we operate have been very supportive of Gilster-Mary Lee for over 40 years. Our sites there have access to a capable workforce, close proximity to many of our key raw materials, many of which are grown in Missouri including rice, popcorn and corn- meal, and good transportation access to serve our customers throughout the U.S. and other parts of the world. The State has also helped us identify and explore new international markets for our products. We appreciate the support that Missouri gives its existing agribusiness partners.” toM WeLge, Vice president, technicaL saLes, giLster-Mary Lee 1. Thriving industry: Missouri has a robust food manufacturing sector. (page 3) already home to over 130 food processing companies, Missouri has the resources to support many more. 2. Central location: Missouri’s proximity to markets and agricultural output ensures quick access to customers and suppliers. (page 13) Located in the heart of america’s agricultural region, Missouri has the 2nd highest number of farms in the country (USDA). -

View Our 2019-2020 Responsibility Report

™ OUR PEOPLE Partners Helping Partners James in Carthage, Missouri, lost his family's vehicles after a tornado ripped through his property. Mandi in Shippensburg, Pennsylvania, was left homeless after losing her family's house to an electrical fire. Miguel in Silao, Mexico, passed away due to COVID-19. Nancy in Green Bay, Wisconsin, was facing mounting medical expenses after being diagnosed with breast cancer. In each of these devastating situations - and hundreds more just like them - partners stepped up to take care of each other by raising funds through our Partners Helping Partners program. What makes our program unique is there's no limit to the amount Schreiber will match. In 2019 and 2020, partners raised more than $176,000 for other partners, and all of that was matched - dollar for dollar, peso for peso, euro for euro, rupee for rupee - by Schreiber. We want Schreiber to be a safe and inclusive place for all partners. That's why we created Business Resource Groups that enable partners to connect with others who share similar interests and backgrounds, or simply show their support as an ally. THESE GROUPS ARE JUST ONE PIECE OF OUR GOAL TO CREATE AN INCLUSIVE CULTURE WHERE DIVERSITY IS EMBRACED AND VALUED . C.,f.a1�� •·'";"· MOSAIC .. scHREIBER RECRUIT, ENRICH, AND DEVELOP ENHANCING ABILITIES LEVERAGING DIFFERENCES EMBRACE THE WORLD. CREATE THE FUTURE. Strives to make Schreiber the Our mission is to make Schreiber Our mission is to make Schreiber Foods Inspire an environment of cultural employer of choice for top Foods a workplace that fosters, learns, a workplace that to encourages fluency at Schreiber Foods through African American talent by and celebrates the uniqueness that conversations and collaboration across globally diverse backgrounds, providing educational opportunities each generational group conveys, and generations and to break generational experiences, and perspectives. -

The History of Schreiber Foods

SIXTEEN OUNCES TO THE POUND ------ The History of Schreiber Foods This book is dedicated to the past, present andfuture partners ofSchreiber Foods. Copyright© 2003 by Schreiber Foods Inc. All rights reserved. No part ofthis book may be reproduced, stored in a retrieval system or transmitted in any farm or by any means, electronic, mechanical photocopying, recording or otherwise, without the prior permission in writingfrom the publisher, except by a reviewer who may quote a briefpassage in review. First Edition ISBN 1-882771-07-9 Library of Congress Catalog Card Number 2003112442 Produced by The History Factory 14140 Parke Long Court Chantilly, Va. 20151 www.historyfactory.com Published by Schreiber Foods Inc. 425 Pine Street P. 0. Box 19010 Green Bay, Wis. 54307-9010 www.schreiberfoods.com CONTENTS Preface XI Part One: Origins 1 A Slice of History- The Story of" 16 Ounces to the Pound" 2 Wisconsin- T he Cheese Capital of America 3 Early Industry Leaders 4 Founding Schreiber Foods 11 Part Two: For the Record- An Overview of the Schreiber Experience 13 Building a Business Based on Values 14 Tests of W ill 23 The Challenge of Growth 33 Taking Schreiber to the Next Level 39 Finding New Ways to Grow 48 Schreiber in the New Millennium 57 Part Three: Recipe for Success 67 T he Journey Continues 68 Epilogue 77 Part Four: Timeline 79 Part Five: People and Places 87 "We wanted quality that would permit us to keep our self- respect, and we wanted to guarantee to every customer that he need never keep one pound of Schreiber cheese that he didn't want.