Liberty Global / Ziggo Merger Procedure Regulation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

What Women Want RTL Nederland’S New Special-Interest Channel

24 September 2009 week 39 What women want RTL Nederland’s new special-interest channel Luxembourg United States The value of TV advertising Kevin Skinner wins America’s Got Talent Germany Russia Online commercial breaks Ren TV presents accepted new season COVER: Montage with different formats of RTL Lounge hat women want derland’s new special-interest channel 2 week 39 the RTL Group intranet Drama and Lifestyle A new digital special-interest channel is going on air just in time for RTL Nederland’s 20th anniversary on 2 October: RTL Lounge. Backstage spoke with Nicolas Eglau who spearheaded the project. The Netherlands - 24 September 2009 The Netherlands has traditionally been a very cable-dominated country. However, due to the low penetration of digital homes in the past, it has been relatively unattractive so far for commercial TV groups to launch their own special-interest channels. The significant increase in digital households over the past two years has changed the situation, so RTL Nederland has now come to an agreement with the two biggest cable operators in the country – UPC and Ziggo – to run RTL Lounge. The new channel goes on air on 2 October as part of the “Royaal” package for UPC subscribers and in Ziggo’s Film & Entertainment package for its customers. In this way, RTL Lounge will reach 15 to 20 per cent of Dutch households in future. At the RTL Nederland programme presentation on 24 August, RTL Nederland CEO Bert Habets said: “RTL is tracking viewers on all platforms. Digital television is becoming increasingly more Nicolas Eglau important. -

Televisieaanbod En Gebruik 2017

televisieaanbod en gebruik onderzoek naar de diversiteit van televisiepakketten en de tevredenheid en het kijkgedrag van de consument © december 2017 Commissariaat voor de Media Colofon Televisieaanbod en gebruik is een uitgave van het Commissariaat voor de Media Redactie Simon van Dooremalen Edmund Lauf Vormgeving Studio FC Klap Commissariaat voor de Media Hoge Naarderweg 78 lllll 1217 AH Hilversum Postbus 1426 lllll 1200 BK Hilversum T 035 773 77 00 lllll 035 773 77 99 lllll [email protected] www.cvdm.nl lllll www.mediamonitor.nl ISSN 2211-2995 2 televisieaanbod en gebruik Onderzoek naar de diversiteit van televisiepakketten en de tevredenheid en het kijkgedrag van de consument Een divers televisiepakket met uitgebreide keuze uit publieke en commerciële zenders blijft zeer relevant voor Nederlanders De trend lijkt duidelijk: binnen enkele jaren kijkt iedereen online – en vooral on demand. Dan hebben alleen Nederlanders van boven de 65 nog een televisiepakket met lineaire tv-zenders. Zo lijkt het misschien nu. De vraag is of het ooit zo ver zal komen. Tot 2013 waren het de programmaraden die de pakketaanbieders adviseerden over de pluriforme samenstelling van hun televisiepakketten. Het was destijds een grote stap om die samenstelling over te laten aan de pakketaanbieders zelf en hen alleen te verplichten minimaal 30 zenders door te geven, waaronder een aantal verplichte, de ‘must carry’ zenders. Er waren aanzienlijke zorgen over een mogelijke neergang van de diversiteit van de pakketten en de gevolgen daarvan voor de tevredenheid van de gebruikers. Die zorgen blijken vooralsnog niet nodig. Het Commissariaat heeft hier voor het vierde jaar op rij onderzoek naar gedaan en constateert dat de diversiteit van de pakketten onverminderd hoog is en dat de tevredenheid van de gebruiker in 2017 opnieuw niet is afgenomen. -

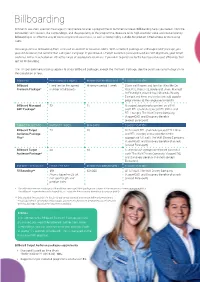

Billboarding Billboards Are Short Sponsor Messages (5 Sec) Before Or After a Programme Or Commercial Break

Billboarding Billboards are short sponsor messages (5 sec) before or after a programme or commercial break. Billboarding helps you benefit from the connection with viewers, the surroundings, and the popularity of the programme. Because of its high attention value and cost-efficiency, billboarding is an effective way of increasing brand awareness, as well as being highly suitable for product introductions or increasing sales. You can purchase billboarding from us based on content or based on GRPs. With a Content package or a Managed GRP package, you yourself decide on the content that suits your campaign. If you choose a Target Audience package based on GRP objectives, your target audience will be reached on an attractive range of appropriate channels. If you wish to purchase to the best-possible cost-efficiency, then opt for Fill boarding. The TV spot commercial policy applies to all our Billboard packages, except the Premium Package. See the purchase system diagram for the calculation of fees. CONTENT FEE/PRODUCT INDEX MINIMUM PERIOD/GRPS CLASSIFICATION Billboard Fixed fee for the agreed Minimum period 1 week Claim well-known and familiar titles like De Premium Package* number of billboards Klok, RTL Weer, RTL Boulevard, Jinek, Married At First Sight, Weet Ik Veel, Chantals Beauty Camper and films and series (we add popular programmes to the range every month) Billboard Managed 83 15 Managed according to content on all full GRP Package* audit RTL channels (except RTL Crime and RTL Lounge), The Walt Disney Company, ViacomCBS, and Discovery Benelux (except Eurosport). TARGET AUDIENCE PRODUCT INDEX MIN GRPS CLASSIFICATION Billboard Target 78 10 All full audit RTL channels (except RTL Crime Audience Package and RTL Lounge) and a selection of the Plus* appropriate full audit The Walt Disney Company, ViacomCBS, and Discovery Benelux channels (except Eurosport). -

2030 Galt General Plan Existing Conditions Report

2030 Galt General Plan Existing Conditions Report Final November 2005 With 2008 updates to the Traffic, Fire Protection, and Historic Resources sections Prepared by: ----------------------------------------------- Mintier & Associates RACESTUDIO Environmental Science Associates Applied Development Economics Omni-Means, Inc. Please visit the City’s website for more information on the General Plan Update: www.ci.galt.ca.us City of Galt General Plan EXISTING CONDITIONS REPORT CREDITS CITY COUNCIL GENERAL PLAN CONSULTANTS Randy D. Shelton, Mayor Mintier Harnish Barbara Payne, Vice Mayor Larry Mintier, FAICP, Principal Andrew Meredith, Councilmember Jim Harnish, JD, Principal Don Haines, Councilmember Dan Amsden, AICP, Project Manager Darryl Clare, Councilmember Tim Raboy, Councilmember (1999-2008) RACESTUDIO Tom Malson, Councilmember (2002-2006) Bruce Race, FAIA, AICP, Principal Environmental Science Associates PLANNING COMMISSION Laurie Warner, Director Ray Weiss, Director Lori Heuer, Chairperson Jessica Mitchell, Associate Mark Yates, Vice Chairperson Lee Ann McFaddin, Commissioner Applied Development Economics Marylou Powers, Commissioner Doug Svensson, Managing Principal Sherry Daley, Commissioner Tony Daysog, Associate Eugene Davenport, Alternate Commissioner Randy Evans, Associate CITY STAFF Omni-Means Marty Inouye, Principal Ted C. Anderson, City Manager Paul Miller, Associate Jason Behrmann, Assistant City Manager Andrew Lee, Traffic Engineer Curt Campion, Community Development Director Gregg Halladay, Director of Public Works Inez -

Goldman Sachs New York September 12-13Th 2018 Agenda

Goldman Sachs New York September 12-13th 2018 Agenda 1 2 3 2018 Group Operational Strategy & highlights highlights Outlook 2018 2 Highlights The pan-European leader in Total Video BROADCAST REVENUE Leading free-to-air In € million 3,046 +2.3% channels and growing TV HY 2018: First time over €3 billion VOD services CONTENT Global entertainment brands Record-high in TV and growing catalogue of high-end drama challenging market environments DIGITAL Proprietary tech with HY 2013 HY 2018 TV leading ad-tech stack & global MPNs EBITDA of €638 million 3 Highlights Our long-term track record LOCAL CONTENT AS KEY SUCCESS FACTOR … Consistent revenue since 2014 growth +3% CAGR High EBITDA margins 20.9% in HY 2018 Ever more diversified Non-TV ad revenue revenue mix 52.3% Organic growth 1 … PROVIDING FIREPOWER TO from content & digital +10.3% Digital: +16.3% EXPAND “TOTAL VIDEO” POSITION revenue YoY revenue YoY Notes: 1.Refers to total digital revenue of MGRTL, M6, and RTL NL. 4 Highlights Strong second quarter drives half-year results Q2 revenue +3.6% Q2 EBITDA +4.7% Half-year revenue +2.3% Half-year EBITDA +1.9% 5 Highlights Continued organic growth through a broad and diversified revenue mix RTL GROUP HY 2018 REVENUE SPLIT PLATFORM AND DIGITAL REVENUE In % In € million Groupe M6: Renewal of distribution agreements Platform1 591 Content 167 #1 MPN 1.7x Revenue +20% YoY3 18.7 213 3.8x 424 100 5.5 113 TV advertising 47.7 € 3.0 bn RTL Group: 13.9 HY 2014 HY 2018 Video views +28% YoY 10.0 4.2 3.7% 5.5% % of total RTL Radio advertising Group revenue 4.2% 13.9% Goal: Other Grow direct-to-consumer 2 Digital Platform Digital revenue significantly Notes: 1. -

Annual Report 2009

Annual Report 2009 Digitization INNOVATION CultureFREEDOM CommitmentChange Bertelsmann Annual Report 2009 CreativityEntertainment High-quality journalism Performance Services Independence ResponsibilityFlexibility BESTSELLERS ENTREPRENEURSHIP InternationalityValues Inspiration Sales expertise Continuity Media PartnershipQUALITY PublishingCitizenship companies Tradition Future Strong roots are essential for a company to prosper and grow. Bertelsmann’s roots go back to 1835, when Carl Bertelsmann, a printer and bookbinder, founded C. Bertelsmann Verlag. Over the past 175 years, what began as a small Protestant Christian publishing house has grown into a leading global media and services group. As media and communication channels, technology and customer needs have changed over the years, Bertelsmann has modifi ed its products, brands and services, without losing its corporate identity. In 2010, Bertelsmann is celebrating its 175-year history of entrepreneurship, creativity, corporate responsibility and partnership, values that shape our identity and equip us well to meet the challenges of the future. This anniver- sary, accordingly, is being celebrated under the heading “175 Years of Bertelsmann – The Legacy for Our Future.” Bertelsmann at a Glance Key Figures (IFRS) in € millions 2009 2008 2007 2006 2005 Business Development Consolidated revenues 15,364 16,249 16,191 19,297 17,890 Operating EBIT 1,424 1,575 1,717 1,867 1,610 Operating EBITDA 2,003 2,138 2,292 2,548 2,274 Return on sales in percent1) 9.3 9.7 10.6 9.7 9.0 Bertelsmann Value -

Global Pay TV Operator Forecasts

Global Pay TV Operator Forecasts Table of Contents Published in October 2016, this 190-page electronically-delivered report comes in two parts: A 190-page PDF giving a global executive summary and forecasts. An excel workbook giving comparison tables and country-by-country forecasts in detail for 400 operators with 585 platforms [125 digital cable, 112 analog cable, 208 satellite, 109 IPTV and 31 DTT] across 100 territories for every year from 2010 to 2021. Forecasts (2010-2021) contain the following detail for each country: By country: TV households Digital cable subs Analog cable subs Pay IPTV subscribers Pay digital satellite TV subs Pay DTT homes Total pay TV subscribers Pay TV revenues By operator (and by platform by operator): Pay TV subscribers Share of pay TV subscribers by operator Subscription & VOD revenues Share of pay TV revenues by operator ARPU Countries and operators covered: Country No of ops Operators Algeria 4 beIN, OSN, ART, Algerie Telecom Angola 5 ZAP TV, DStv, Canal Plus, Angola Telecom, TV Cabo Argentina 3 Cablevision; Supercanal; DirecTV Australia 1 Foxtel Austria 3 Telekom Austria; UPC; Sky Bahrain 4 beIN, OSN, ART, Batelco Belarus 2 MTIS, Zala Belgium 5 Belgacom; Numericable; Telenet; VOO; Telesat/TV Vlaanderen Bolivia 3 DirecTV, Tigo, Entel Bosnia 3 Telemach, M:Tel; Total TV Brazil 5 Claro; GVT; Vivo; Sky; Oi Bulgaria 5 Blizoo, Bulsatcom, Vivacom, M:Tel, Mobitel Canada 9 Rogers Cable; Videotron; Cogeco; Shaw Communications; Shaw Direct; Bell TV; Telus TV; MTS; Max TV Chile 6 VTR; Telefonica; Claro; DirecTV; -

Schachtscheine Der Versorgungsunternehmen

Anschriften der wichtigsten Eigentümer von Ver- und Entsorgungsleitungen für Leitungsauskünfte 12.06.2018 Energieversorgung Gera GmbH- Frau Bohrisch 0365 / 8561790 Neue Str.5 Fax 0365 / 8561509 07545 Gera Bereiche Strom, Gas, Wärme, Steuerkabel [email protected] oder [email protected] OTWA Ostthüringer Wasser- und Abwasser GmbH Abt. Stadtbeleuchtung De-Smit-Str. 18, 07545 Gera (Postanschrift ) Sitz Kantstraße 3 [email protected] Straßenbeleuchtung Herr Schneider 0365 / 77309503 Fax 0365 / 77309519 Zweckverband Wasser/Abwasser „Mittleres Elstertal“ De-Smit-Str. 6, 07545 Gera [email protected] Trinkwasser / Abwasser Herr Billhardt 0365 / 4870 840 Fax 0365 / 4870 875 Onlineportal des Zweckverbandes nutzen Deutsche Telekom Technik GmbH PTI 22 PPB 6, Planauskunft Mühlweg 16, Haus A Fax 0361 / 651 77 88 99091 Erfurt Mail: [email protected] Vodafone Kabel Deutschland GmbH Südwestpark 15 90449 Nürnberg Fax 089 / 923342-1321 https://partner.kabeldeutschland.de/webauskunft-neu/datashop/ Breitbandkabel- AG Handwerk Kabel TV über TECOSI ATF GmbH Frau Meiser 036605 / 888-0 Gleinaer Weg 1, 07586 Bad Köstritz Fax 036605 / 888-22 [email protected] 1&1 Versatel Deutschland GmbH Dokumentation Sammel-Nr. 030 81 88 12 05 Aroser Allee 78 Frau Teichmann 030 81 88 99 13407 Berlin Fax 030 81 88 911 11 [email protected] oder https://vt-leitungsauskunft.versatel.de/Datashop 1 PrimaCom Berlin GmbH (gehört zu DTK Deutsche Telekabel GmbH) Messe-Allee 2 Frau Kirmse 0341 / 60 95 24 69 04356 Leipzig [email protected] Tele Columbus AG An der Flutrinne 12° 0351 / 20282-49/47 01139 Dresden Fax 0531 / 20282-70 [email protected] Thüringer Netkom GmbH Schwanseestraße 13 Frau Beyer 03643 21 3037 99423 Weimar Fax 03643 21 3089 [email protected] Engel & Co. -

Analysys Mason Report on Developments in Cable for Superfast Broadband

Final report for Ofcom Future capability of cable networks for superfast broadband 23 April 2014 Rod Parker, Alex Slinger, Malcolm Taylor, Matt Yardley Ref: 39065-174-B . Future capability of cable networks for superfast broadband | i Contents 1 Executive summary 1 2 Introduction 5 3 Cable network origins and development 6 3.1 History of cable networks and their move into broadband provision 6 3.2 The development of DOCSIS and EuroDOCSIS 8 4 Cable network elements and architecture 10 4.1 Introduction 10 4.2 Transmission elements 10 4.3 Description of key cable network elements 13 4.4 Cable access network architecture 19 5 HFC network implementation, including DOCSIS 3.0 specification 21 5.1 Introduction 21 5.2 HFC performance considerations 21 5.3 Delivery of broadband services using DOCSIS 3.0 24 5.4 Limitations of DOCSIS 3.0 specification 27 5.5 Implications for current broadband performance under DOCSIS 3.0 30 6 DOCSIS 3.1 specification 33 6.1 Introduction 33 6.2 Reference architecture 34 6.3 PHY layer frequency plan 35 6.4 PHY layer data encoding options 37 6.5 MAC and upper layer protocol interface (MULPI) features of DOCSIS 3.1 39 6.6 Development roadmap 40 6.7 Backwards compatibility 42 6.8 Implications for broadband service bandwidth of introducing DOCSIS 3.1 43 6.9 Flexibility of DOCSIS 3.1 to meet evolving service demands from customers 47 6.10 Beyond DOCSIS 3.1 47 7 Addressing future broadband growth with HFC systems – expanding DOCSIS 3.0 and migration to DOCSIS 3.1 49 7.1 Considerations of future broadband growth 49 7.2 Key levers for increasing HFC data capacity 52 7.3 DOCSIS 3.0 upgrades 53 7.4 DOCSIS 3.1 upgrades 64 7.5 Summary 69 Ref: 39065-174-B . -

Vodafone Group and Liberty Global Announce Intention to Appoint Two Senior Executives for Their Proposed Netherlands Joint Venture

Vodafone Group and Liberty Global announce intention to appoint two senior executives for their proposed Netherlands joint venture Jeroen Hoencamp to be appointed Chief Executive and Ritchy Drost to be appointed Chief Financial Officer upon completion of transaction Denver, Colorado and London, United Kingdom ‐ 19 July 2016: Vodafone Group Plc (LSE: VOD) and Liberty Global plc (NASDAQ: LBTYA, LBTYB and LBTYK) today announced their intention to appoint Jeroen Hoencamp as Chief Executive and Ritchy Drost as Chief Financial Officer of the two companies’ proposed 50‐50 joint venture business combining Vodafone Netherlands and Ziggo*. The merger is subject to approval by the relevant competition authorities. Jeroen Hoencamp is currently the Chief Executive of Vodafone UK. A Dutch citizen, he has led Vodafone’s UK business since September 2013 and was previously Chief Executive of Vodafone Ireland. Before that, he spent 12 years in a number of senior executive roles (including Sales Director and Enterprise Business Unit Director) with Vodafone Netherlands. Earlier in his career he worked in senior marketing and sales positions with Canon Southern Copy Machines, Inc. in the USA and Thorn EMI/Skala Home Electronics in The Netherlands. He is a former officer in the Royal Dutch Marine Corps. In anticipation of the joint venture closing, Vodafone Group also announced that Jeroen Hoencamp will assume the position of Chief Executive of Vodafone Netherlands, effective 1 September 2016. Ritchy Drost is currently Chief Financial Officer of Ziggo, a position he has held since September 2015. Over a 17‐year career with Liberty Global he has held a number of senior management positions including Chief Financial Officer, European Broadband Operations and Managing Director and Chief Financial Officer of UPC Netherlands, Liberty’s predecessor Dutch cable operation. -

Ziggo Zenderoverzicht Televisie

Ziggo Zenderoverzicht. Vanaf 12 november 5 TV Gemist Horizon TV thuis Horizon TV overal Replay TV 1 NPO 1 (HD) 5 113 HBO3 (HD) 5 507 CNBC Europe 2 NPO 2 (HD) 5 120 RTL Crime 508 CCTV News 3 NPO 3 (HD) 5 121 Syfy (HD) * 509 RT 4 RTL 4 (HD) 5 122 CI 538 TV538 5 5 RTL 5 (HD) 5 123 ID 601 MTV Music 24 6 SBS6 (HD) 5 124 Comedy Central Extra 5 602 DanceTrippin 5 7 RTL 7 (HD) 5 125 Shorts TV 603 SLAM!TV 8 Veronica / Disney XD (HD) 5 126 E! (HD) * 604 MTV Brand New 9 Net5 (HD) 5 127 NPO Best 605 Stingray LiteTV 10 RTL 8 (HD) 5 128 NPO 101 606 VH1 Classic 11 FOX (HD) 5 129 OUTtv 607 Brava NL Klassiek 5 12 RTL Z (HD) 130 NPO Humor TV 608 Mezzo 13 Ziggo TV 131 AMC 5 609 DJAZZ.tv 5 14 Ziggo Sport (HD) 5 132 CBS Reality 610 TV Oranje 15 Comedy Central (HD) 5 133 Fashion TV HD 611 100% NL TV 5 16 Nickelodeon (HD) 5 134 MyZen HD 612 192TV 17 Discovery (HD) 5 136 Horse & Country TV 613 MTV Live HD 18 National Geopgraphic Channel (HD) 5 140 RTL Lounge 701 TV Noord 19 SBS9 (HD) 5 202 Discovery Science 702 Omrop Fryslân 20 Eurosport (HD) 203 Discovery World 703 TV Drenthe 21 TLC (HD) 5 204 Nat Geo Wild (HD) 704 TV Oost 5 22 13TH Street (HD) * 208 Animal Planet HD 705 TV Gelderland 23 MTV (HD) 5 210 Travel Channel (HD) 706 Omroep Flevoland 24 24Kitchen (HD) 211 ONS 707 TV NH 25 XITE 5 212 NPO Doc 708 Regio TV Utrecht 26 FOXlife (HD) 5 222 NPO Cultura 709 TV West 27 Disney Channel 5 230 Family7 710 TV Rijnmond 28 HISTORY (HD) 5 301 Disney XD 5 711 Omroep Zeeland 29 Comedy Central Family 5 302 Disney Junior 5 712 Omroep Brabant 5 30-33 Regionaal publieke 303 Nicktoons 713 L1 TV omroep van de regio 304 Nick Hits 725 AT5 34-35 Regionaal commerciële omroep 305 Pebble TV 36-50 Lokale omroep 306 Nick Jr. -

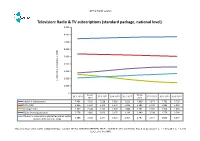

Television: Radio & TV Subscriptions (Standard Package, National Level) 9.000

OPTA Public version Television: Radio & TV subscriptions (standard package, national level) 9.000 8.000 7.000 6.000 5.000 4.000 3.000 2.000 number of subscriptionsof number x 1,000 1.000 0 31-12- 31-12- 30-9-2010 31-3-2011 30-6-2011 30-9-2011 31-3-2012 30-6-2012 30-9-2012 2010 2011 Total RTV subscriptions 7.454 7.500 7.538 7.590 7.623 7.669 7.677 7.702 7.730 Total cable 5.366 5.334 5.291 5.271 5.226 5.182 5.129 5.083 5.033 Analogue cable 2.587 2.448 2.265 2.095 1.888 1.741 1.592 1.504 1.434 Digital (+ analogue) cable 2.778 2.886 3.026 3.176 3.338 3.440 3.538 3.579 3.599 Other RTV subscriptions (digital terrestrial, digital 2.088 2.166 2.247 2.319 2.397 2.487 2.547 2.620 2.697 satellite, IPTV over DSL, FttH) Based on figures from CAIW, CANALDIGITAAL, COGAS, DELTA, KPN, REGGEFIBER, TELE2, T-MOBILE, UPC and ZIGGO. Based on questions 5_A_1_1 through 5_A_1_5 and 5_A_1_8 of the SMM. OPTA Public version Television: Churn based on radio & TV subscriptions (standard package, national level) 5% 4% 3% 2% % of number%of subscriptions 1% 0% 30-9-2010 31-12-2010 31-3-2011 30-6-2011 30-9-2011 31-12-2011 31-3-2012 30-6-2012 30-9-2012 Adds 3,1% 3,2% 3,1% 3,0% 3,3% 3,9% 3,8% 3,3% 3,2% Disconnects 2,7% 2,5% 2,8% 2,7% 2,9% 3,3% 3,4% 3,1% 3,0% Based on figures from CAIW, CANALDIGITAAL, COGAS, DELTA, KPN, REGGEFIBER, TELE2, UPC and ZIGGO.