Proton Holdings Berhad

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Malaysia Autobook 2019 Previewc

AUTOMOTIVE INTELLIGENCE FOR PROFESSIONALS Malaysia AutoBook 2019 PREVIEWc Malaysia AutoBook 2019 WELCOME! Malaysia is one of the Automotive Top Player Focus on contacts of ASEAN – a market comprising some 625 Million people and significant potential for This update introduces new quick links to access web sites, Google growth. Maps locations and social media sites of the featured companies and their representatives. Simply click on the following icons to connect: Outsourcing, localization and business development The information was compiled from personal I am sure this book will give you lots of information and inspire you to research, the internet and with support of friends do business in Malaysia. at automotive companies, automotive organizations, industrial estates and business associates and is designed to support: To your success! 1) Outsourcing – local and international commodity managers, buyers who are looking to source automotive components from Malaysia Ulrich Kaiser 2) Localization – international managers desiring to expand their market and set up a footprint in China – either for distribution or local production. 3) Business Development - managers who seek to identify potential customers and sales opportunities in China’s automotive industry ii Chapter 1 Introduction Section 1 Introduction AT A GLANCE Automotive History Malaysia 1. Ford was the first automotive firm present The first automotive firm in Malaysia was Gadelius & Company that represented Ford in Malaysia, represented by Gadelius & Motor Company sales in Malaysia in 1909. The company was relater replaced with an company. Australian representative called Wearne & Co., that signed a contract for 60 vehicles per year. In 1941, Ford Malaysia set up its first assembly plant in Bukit Timah, Singapore to 2. -

Lee, Woo Cheol (2015) the Political Economy of Vietnam : the Evolution of State- Business Relationships

Lee, Woo Cheol (2015) The political economy of Vietnam : the evolution of state- business relationships. PhD Thesis. SOAS, University of London http://eprints.soas.ac.uk/23662 Copyright © and Moral Rights for this thesis are retained by the author and/or other copyright owners. A copy can be downloaded for personal non‐commercial research or study, without prior permission or charge. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the copyright holder/s. The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the copyright holders. When referring to this thesis, full bibliographic details including the author, title, awarding institution and date of the thesis must be given e.g. AUTHOR (year of submission) "Full thesis title", name of the School or Department, PhD Thesis, pagination. The Political Economy of Vietnam: The Evolution of State-Business Relationships Woo Cheol Lee Thesis submitted for the degree of PhD in Economics 2015 Department of Economics School of Oriental and African Studies University of London 1 Declaration for SOAS PhD thesis I have read and understood regulation 17.9 of the Regulations for students of the School of Oriental and African Studies concerning plagiarism. I undertake that all the material presented for examination is my own work and has not been written for me, in whole or in part, by any other person. I also undertake that any quotation or paraphrase from the published or unpublished work of another person has been duly acknowledged in the work which I present for examination. -

DRB-HICOM, GEELY, REACH ACCORD Heads of Agreement Signed; Definitive Agreement by Mid- July

MEDIA RELEASE IMMEDIATE RELEASE DRB-HICOM, GEELY, REACH ACCORD Heads of agreement signed; Definitive Agreement by mid- July PUTRAJAYA, 24 May 2017: DRB-HICOM Berhad (DRB-HICOM) has reached an agreement with China-based Zhejiang Geely Holding Group Co., Ltd (Geely Holding) for the Chinese car group to acquire 49.9% equity in PROTON Holdings Berhad. DRB-HICOM currently owns 100% of the manufacturer of the first national car. The two parties signed the agreement in Putrajaya today, witnessed by YB Datuk Seri Johari Abdul Ghani, the Minister of Finance II. The deal will enable PROTON to tap into Geely Holding’s vast range of platforms and powertrains, and will also enable PROTON to have access to existing markets of the Chinese carmaker, as well as right-hand drive markets in south-east Asia. DRB-HICOM Group Managing Director, Dato’ Sri Syed Faisal Albar says the PROTON brand will remain present and will grow significantly with the new foreign strategic partner on board. “Our intention was always to ensure the revitalization of the PROTON nameplate. It was Malaysia’s first national car brand and has more than 30 years of history. This deal will be the catalyst to elevate a brand that Malaysians resonate with,” said Syed Faisal. Geely Holding Group Executive Vice President and CFO Mr. Daniel Donghui Li commented, “With PROTON and Lotus joining the Geely Group portfolio of brands we strengthen our global foot print and develop a beachhead in South East Asia. Geely Holding is full of confidence for the future of PROTON, we will fully respect the brands history and culture to restore PROTON to its former glory with the support of Geely’s innovative technology and management resources. -

Joint Media Statement by Drb-Hicom and Zhejiang Geely Holding Group

MEDIA RELEASE IMMEDIATE ISSUANCE JOINT MEDIA STATEMENT BY DRB-HICOM AND ZHEJIANG GEELY HOLDING GROUP DRB-HICOM, Geely Holding names nominees to PROTON Group boards Dr. Li Chunrong, appointed CEO of PONSB, leads executive team of global experts Full revitalisation of PROTON Group underway 29 September, 2017, Shah Alam: Exactly one hundred days after the signing of the Definitive Agreement between DRB-HICOM Berhad (DRB-HICOM) and Zhejiang Geely Holding Group (Geely Holding) on 23 June, the two companies have confirmed the new board structures and part of the executive team for PROTON Holdings Berhad and its related companies (PROTON Group). Company Structure At the PROTON Holdings Berhad (PHB) level, Dato’ Sri Syed Faisal Albar remains as the Chairman, and he is joined on the board by Shaharul Farez Hassan and Amalanathan Thomas as nominees from DRB-HICOM. Farez and Nathan are both part of the senior management team at DRB-HICOM. Geely Holding has nominated Daniel Donghui Li and Feng Qing Feng as their nominees to the PHB board. Daniel Donghui Li is the current Executive Vice President and CFO of Geely Holding, while Feng is the Group Vice President and CTO of Hong Kong-listed Geely Auto. All five nominees also sit on the Perusahaan Otomobil Nasional Sdn Bhd (PONSB) board, along with Dr. Nathan Yu Ning, who is the Vice President of International Business at Geely Holding. Winfried Vahland, who was formerly the Chairman and Chief Executive Officer of Skoda Auto, is also on the board of PONSB. Syed Faisal, Farez, Nathan, Daniel Donghui Li and Dr. -

Proton Success Story

MSC.Software: User Case Study - Proton USER CASE STUDY PROTON Customer Profile: Noor Hisham Bin Ismail Mr Noor Hisham Bin Ismail is head of CAE at PROTON based in Kuala Lumpur, Malaysia. Mr Ismail and other members of the computer-aided engineering team are responsible for improving the virtual development of mechanical and structural components, sub systems and complete vehicle system at PROTON. Through Mr Ismail’s innovative process of probabilistic analysis, PROTON has been able to effectively identify areas of high-risk failure and fine-tuning engineering design alternatives. Challenge Mr Ismail’s foundation of probabilistic design methodology uses design In developing complex mechanical and structural automotive criteria based on reliability targets instead of deterministic criteria. components, going through multiple build-and-test hardware prototype First, design parameters such as applied loads, material strength, and cycles to verify performance, stress and fatigue life is just too time- operational parameters are researched and/or measured and then consuming and expensive. This issue can be addressed by evaluating statistically defined. A probabilistic analysis model is then developed for and refining designs with analysis tools up front in development, reducing the entire system and solutions performed to yield failure probabilities. test cycles later in the development process. PROTON’s pioneering spirit With MSC’s FEA, applied stress is obtained from finite element models. naturally has led Mr ismail to not just stop at traditional methodologies in The general concept is to integrate the joint probability of applied stress computer-aided engineering for design analysis. As the risk of failure in and material strength over the region where stress exceeds strength. -

Comparative Political Economic Analysis of Automotive Industrial Policies in Malaysia and Thailand

60 State and Industrial Policy State and Industrial Policy: Comparative Political Economic Analysis of Automotive Industrial Policies in Malaysia and Thailand Wan-Ping Tai Cheng Shiu University, Taiwan Samuel C. Y. Ku National Sun Yat-Sen University, Taiwan Abstract Numerous differences exist between the neoclassical and national development schools of economics on how an economy should develop. For example, should the state interfere in the market using state resources, and cultivate certain industries to achieve specific developmental goals? Although the automotive industries in both Thailand and Malaysia developed in the 1970s with considerable government involvement, they have evolved along very different lines. Can these differences be traced to different interactions between the state and industry in these two countries? This paper examines this issue and finds that although industries in developing countries need government assistance, the specific political and economic contexts of each country affect the policies adopted and their effectiveness. The choice between “autonomous development” (Malaysia) and “dependent development” (Thailand) is the first issue. The second issue is that politics in Malaysia has deterred the automotive industry from adopting a “market following” position. This paper finds that the choice of strategy and political interference are the two main reasons the automotive industry in Malaysia is less competitive than that in Thailand. Keywords: Automotive Industry, Developmental State, Malaysia Automotive Industry, Thai Automotive Industry, PROTON, Political Economic Analysis Introduction sectors and industries as diverse as iron, oil, manufacturing, sales, the stock market, In the wake of the 2008 economic crash, credit, and insurance. Because of the huge whether the U.S. -

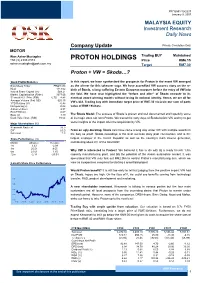

PROTON HOLDINGS Price RM6.15 [email protected] Target RM7.30

PP/10551/10/2007 January 9, 2007 MALAYSIA EQUITY Investment Research Daily News Private Circulation Only Company Update MOTOR Wan Azhar Mustapha Trading BUY Maintained +60 (3) 2333 8373 PROTON HOLDINGS Price RM6.15 [email protected] Target RM7.30 Proton + VW = Skoda…? Stock Profile/Statistics In this report, we have synthesized the prospects for Proton in the event VW emerged Bloomberg Ticker PROH MK as the winner for this takeover saga. We have accredited VW success story on the re- KLCI 1113.02 birth of Škoda, a long suffering Eastern European marques before the entry of VW into Issued Share Capital (m) 549.21 Market Capitalisation (RMm) 3377.66 the fold. We have also highlighted the “before and after” of Škoda en-route to its 52 week H | L Price (RM) 6.75 4.48 eventual award winning models without losing its national identity. Hence, we are all for Average Volume (3m) ‘000 625.15 VW’s bid. Trading buy with immediate target price of RM7.30 vis-à-vis our sum of parts YTD Returns (%) -0.45 Net gearing (x) -0.02 value of RM9.19/share. Altman Z-Score 2.97 ROCE/WACC -0.07 Beta (x) 1.49 The Škoda Model. The success of Škoda is proven and well documented and hopefully some Book Value/share (RM) 10.64 of its magic does rub onto Proton. We traced the early days of Škoda before VW and try to get some insights of the impact after the acquisition by VW. Major Shareholders (%) Khazanah Nasional 38.3 EPF 10.5 From an ugly duckling. -

Welfare Effects of Trade Barriers on Malaysian Car Industry: an Alternative Approach

WELFARE EFFECTS OF TRADE BARRIERS ON MALAYSIAN CAR INDUSTRY: AN ALTERNATIVE APPROACH Wai Kun C Lau (1718460) A Dissertation Submitted In Fulfilment Of The Requirements For The Degree of DOCTOR OF PHILOSOPHY FACULTY OF BUSINESS & LAW SWINBURNE UNIVERSITY OF TECHNOLOGY April 2020 i Abstract Malaysian car industry has been heavily protected by tariff and non-tariff tools since it was founded in 1983. Despite excessive tariffs imposed on foreign cars, the demand for foreign cars increases after the Asian financial crisis 1997 while the demand for domestic cars declines. Partial equilibrium framework is applied in this research because the car industry’s contribution to GDP is very small and the focus of this research is specifically on the car industry. Since cars are durable and differentiated, changes due to technological advancement may influence car demand. This research applies Discrete Choice model to account for car characteristics in addition to socio-economic factors for analysis of car demand in Malaysia. Logistic regression analysis results show factors that influence car demand are: horsepower, fuel consumption, and car size that is measured by number of passengers. Results suggest that non-tariff barriers and government incentives given to the civil servants have significant influence on Proton cars’ demand, and foreign car makers that have been operating in Malaysia before the founding of Proton enjoy their reputation from their historical experience and performance. While it is often believed that European cars have ostentatious value in Malaysia, the results show otherwise. Price elasticity of demand for major car makes is estimated based on the average horsepower, car size and fuel consumption. -

Perusahaan Otomobil Nasional Berhad

PERUSAHAAN OTOMOBIL NASIONAL BERHAD Annual Report 2004 Laporan Tahunan Performance Review penilaian prestasi Chairman’s Statement 146 Perutusan Pengerusi 146 Group CEO’s Review of Business Operations 156 Tinjauan Operasi Ketua Pegawai Eksekutif Kumpulan 156 Five Years Financial Highlights 180 Ringkasan Kewangan untuk Lima Tahun 180 Key Financial Indicators 186 Petunjuk Kewangan Utama 186 Financial Calendar 187 Takwim Kewangan 187 Share Price and Volume Traded 188 Harga Saham dan Saham Diniagakan 188 Awards and Recognition 189 Anugerah dan Pengiktirafan 189 CHAIRMAN’S Y.Bhg. Datuk Abu Hassan bin Kendut Chairman / Pengerusi 147 TATEMENT S PERUTUSAN PENGERUSI INTRODUCTION On behalf of the Board of Directors, I am pleased to present the annual report of Perusahaan Otomobil Nasional Berhad for the year ended 31 March 2004, prepared in accordance with the applicable approved accounting standards in Malaysia and the provisions of the Companies Act 1965. CORPORATE REORGANISATION On 27 May 2003, the Board announced a proposed Corporate Reorganisation, which was subsequently approved by the shareholders and regulatory authorities. On 5 April 2004, all shareholders of Perusahaan Otomobil Nasional Berhad exchanged their ordinary shares of RM1.00 each in the Company for new ordinary shares of RM1.00 each in PROTON Holdings Berhad. With the exchange of shares, PROTON Holdings Berhad became the shareholder of Perusahaan Otomobil Nasional Berhad and the ultimate holding company of the PROTON Group. On 16 April 2004, the shares of Perusahaan Otomobil Nasional Berhad were delisted and PROTON Holdings Berhad assumed the listing status on the Bursa Malaysia Securities Berhad. PROTON Holdings Berhad was incorporated on 28 July 2003 and remained dormant until the exchange of shares on 5 April 2004. -

Operations Review

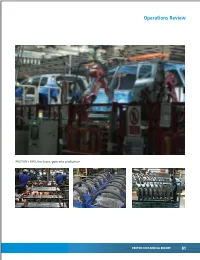

Operations Review PROTON’s MPV, the Exora, goes into production. PROTON 2009 ANNUAL REPORT 81 Operations Review The Group also anticipates strong local demand for the Persona and Saga, while export volume is expected to increase especially for the Exora with plans already in place to introduce this vehicle to the ASEAN market in the second half of 2009. Furthermore, with the expansion of the Overseas Manufacturing Plants in China and Iran, the export business on completely–knocked–down (CKD) vehicles is expected to increase as well. New robots and more sophisticated handling equipment were installed successfully with minimal line disruptions. Previous PROTON production systems and Total Productive Maintenance (TPM) activities have already resulted in the main plant having one of the lowest downtimes in history and similar activities were implemented successfully in the Casting and Engine Transmission Department. Much effort was taken to maintain this. An increasing number of model lines or equipment was established through ‘yokoten’, a Japanese term which essentially means duplicating. The next stage in these intensive improvement activities will be the implementation of ‘Kobetsu Kaizen’ (which means ‘Focus Improvement’) and the usage of Overall Equipment Efficiency (OEE) as the de facto parameter to measure equipment efficiency. In view of PROTON’s commitment to improvement, the Manufacturing Division has started implementing the world-renowned practice of ‘Genba Kanri’, another Japanese term this time referring to ‘Shopfloor Control’. This is to reflect how the division is continuously improving itself by benchmarking PROTON against world-class industry players. We shall aim to reach level 4 (which means sustainable world-class level in shop control) in ‘Genba Kanri’ by the year 2011. -

Activities by Region Asia, ASEAN and Other Regions

Activities by Region Asia, ASEAN and Other Regions Principal Operational Facilities in Southeast Asia Philippines Thailand Vietnam VSM Vina Star Motors Corporation Malaysia Activities: Manufacturing and sales of automobiles and parts ■ ATC Shareholders: MMC 25.0% Asian Transmission Corp. Location: Calamba Laguna, Philippines Capitalization: PHP 770.0 million Activities: Manufacturing of automobile transmissions MMC Voting Rights: 94.7% A c t i v i t i e ■ MMPC s b Mitsubishi Motors Philippines Corp. y R Indonesia Location:Rizal, Philippines e g i o Capitalization: PHP 1,640.0 million n / Activities: Importing, assembly and sales of automobiles A s i MMC Voting Rights:51.0% a , A S E A N a n d O MMM t h e r Mitsubishi Motors Malaysia Sdn. Bhd. R e Activities: Vehicle sales g i o Shareholders: MMC 0.0%, MC 52.0% n s ■ MEC KTB MMTh Engine Co., Ltd. P.T. Krama Yudha Tiga Berlian Motors Location: Cholburi, Thailand Activities: Distributor Capitalization: THB 20.0 million Shareholders: MMC 2.0%, MC 40.0% Activities: Manufacturing of automobile engine and pressed parts MKM MMC Voting Rights: 100.0% P.T. Mitsubishi Krama Yudha Motors and Manufacturing Activities: Activities: Manufacture of automotive parts Shareholders: MMC 0.0%, MC 32.3% ■ MMTh Mitsubishi Motors (Thailand) Co.,Ltd. Location: Phathumthani, Thailand Capitalization: THB 7,000.0 million Activities: Importing, assembly and sales of automobiles and parts MMC Voting Rights: 100.0% (As of March 31, 2013) MC: Mitsubishi Corporation ■ MMC and Consolidated Subsidiaries 17 Asia, ASEAN Production Volume by Model (Unit: Vehicles) Production Facility / Assembler 2008 2009 2010 2011 2012 ■ MMTh (Thailand) .............................................................................................................. -

Acronimos Automotriz

ACRONIMOS AUTOMOTRIZ 0LEV 1AX 1BBL 1BC 1DOF 1HP 1MR 1OHC 1SR 1STR 1TT 1WD 1ZYL 12HOS 2AT 2AV 2AX 2BBL 2BC 2CAM 2CE 2CEO 2CO 2CT 2CV 2CVC 2CW 2DFB 2DH 2DOF 2DP 2DR 2DS 2DV 2DW 2F2F 2GR 2K1 2LH 2LR 2MH 2MHEV 2NH 2OHC 2OHV 2RA 2RM 2RV 2SE 2SF 2SLB 2SO 2SPD 2SR 2SRB 2STR 2TBO 2TP 2TT 2VPC 2WB 2WD 2WLTL 2WS 2WTL 2WV 2ZYL 24HLM 24HN 24HOD 24HRS 3AV 3AX 3BL 3CC 3CE 3CV 3DCC 3DD 3DHB 3DOF 3DR 3DS 3DV 3DW 3GR 3GT 3LH 3LR 3MA 3PB 3PH 3PSB 3PT 3SK 3ST 3STR 3TBO 3VPC 3WC 3WCC 3WD 3WEV 3WH 3WP 3WS 3WT 3WV 3ZYL 4ABS 4ADT 4AT 4AV 4AX 4BBL 4CE 4CL 4CLT 4CV 4DC 4DH 4DR 4DS 4DSC 4DV 4DW 4EAT 4ECT 4ETC 4ETS 4EW 4FV 4GA 4GR 4HLC 4LF 4LH 4LLC 4LR 4LS 4MT 4RA 4RD 4RM 4RT 4SE 4SLB 4SPD 4SRB 4SS 4ST 4STR 4TB 4VPC 4WA 4WABS 4WAL 4WAS 4WB 4WC 4WD 4WDA 4WDB 4WDC 4WDO 4WDR 4WIS 4WOTY 4WS 4WV 4WW 4X2 4X4 4ZYL 5AT 5DHB 5DR 5DS 5DSB 5DV 5DW 5GA 5GR 5MAN 5MT 5SS 5ST 5STR 5VPC 5WC 5WD 5WH 5ZYL 6AT 6CE 6CL 6CM 6DOF 6DR 6GA 6HSP 6MAN 6MT 6RDS 6SS 6ST 6STR 6WD 6WH 6WV 6X6 6ZYL 7SS 7STR 8CL 8CLT 8CM 8CTF 8WD 8X8 8ZYL 9STR A&E A&F A&J A1GP A4K A4WD A5K A7C AAA AAAA AAAFTS AAAM AAAS AAB AABC AABS AAC AACA AACC AACET AACF AACN AAD AADA AADF AADT AADTT AAE AAF AAFEA AAFLS AAFRSR AAG AAGT AAHF AAI AAIA AAITF AAIW AAK AAL AALA AALM AAM AAMA AAMVA AAN AAOL AAP AAPAC AAPC AAPEC AAPEX AAPS AAPTS AAR AARA AARDA AARN AARS AAS AASA AASHTO AASP AASRV AAT AATA AATC AAV AAV8 AAW AAWDC AAWF AAWT AAZ ABA ABAG ABAN ABARS ABB ABC ABCA ABCV ABD ABDC ABE ABEIVA ABFD ABG ABH ABHP ABI ABIAUTO ABK ABL ABLS ABM ABN ABO ABOT ABP ABPV ABR ABRAVE ABRN ABRS ABS ABSA ABSBSC ABSL ABSS ABSSL ABSV ABT ABTT