GEELY SWEDEN HOLDINGS AB ANNUAL REPORT 2019 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Malaysia Autobook 2019 Previewc

AUTOMOTIVE INTELLIGENCE FOR PROFESSIONALS Malaysia AutoBook 2019 PREVIEWc Malaysia AutoBook 2019 WELCOME! Malaysia is one of the Automotive Top Player Focus on contacts of ASEAN – a market comprising some 625 Million people and significant potential for This update introduces new quick links to access web sites, Google growth. Maps locations and social media sites of the featured companies and their representatives. Simply click on the following icons to connect: Outsourcing, localization and business development The information was compiled from personal I am sure this book will give you lots of information and inspire you to research, the internet and with support of friends do business in Malaysia. at automotive companies, automotive organizations, industrial estates and business associates and is designed to support: To your success! 1) Outsourcing – local and international commodity managers, buyers who are looking to source automotive components from Malaysia Ulrich Kaiser 2) Localization – international managers desiring to expand their market and set up a footprint in China – either for distribution or local production. 3) Business Development - managers who seek to identify potential customers and sales opportunities in China’s automotive industry ii Chapter 1 Introduction Section 1 Introduction AT A GLANCE Automotive History Malaysia 1. Ford was the first automotive firm present The first automotive firm in Malaysia was Gadelius & Company that represented Ford in Malaysia, represented by Gadelius & Motor Company sales in Malaysia in 1909. The company was relater replaced with an company. Australian representative called Wearne & Co., that signed a contract for 60 vehicles per year. In 1941, Ford Malaysia set up its first assembly plant in Bukit Timah, Singapore to 2. -

Volvo Cars and Geely Auto to Deepen Collaboration

Volvo Cars and Geely Auto to Deepen Collaboration VOLVO CAR AB STOCK EXCHANGE RELEASE 24 FEBRUARY 2021 AT 14:30 CET Volvo Cars and Geely Auto have agreed on a wide-ranging collaboration that will maximise the strengths of the Swedish and Chinese automotive groups, delivering synergies in powertrains, sharing of electric vehicle architecture, joint procurement, autonomous drive technologies and aftersales. • Powertrain operations to be combined in new company focused on next-generation hybrid systems and internal combustion engines • Expanded use of shared modular architectures for electric vehicles (EVs) • Enhanced collaboration in autonomous and electric drive technologies • Joint procurement to cut purchasing costs • Lynk & Co to expand globally by utilising Volvo distribution and service network • Companies to retain independent corporate structures Following a detailed review of combination options, Volvo Cars and Geely Auto have concluded they can secure new growth opportunities in their respective markets and meet evolving industry challenges through deeper cooperation, while preserving their existing separate corporate structures. The deeper collaboration will enable existing stakeholders and potential new investors in Volvo Cars and Geely Auto to value their respective standalone strategies, performance, financial exposure and returns. We will also have the opportunity to explore capital market options. The collaboration will be overseen by a new governance model, supported by Geely Holding, the lead shareholder in both companies. Volvo Cars and Geely Auto confirmed the combination of their existing powertrain operations into a new standalone company. The company, expected to become operational this year, will provide internal combustion engines, transmissions, and next-generation dual-motor hybrid systems for use by both companies as well as other automobile manufacturers. -

Lee, Woo Cheol (2015) the Political Economy of Vietnam : the Evolution of State- Business Relationships

Lee, Woo Cheol (2015) The political economy of Vietnam : the evolution of state- business relationships. PhD Thesis. SOAS, University of London http://eprints.soas.ac.uk/23662 Copyright © and Moral Rights for this thesis are retained by the author and/or other copyright owners. A copy can be downloaded for personal non‐commercial research or study, without prior permission or charge. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the copyright holder/s. The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the copyright holders. When referring to this thesis, full bibliographic details including the author, title, awarding institution and date of the thesis must be given e.g. AUTHOR (year of submission) "Full thesis title", name of the School or Department, PhD Thesis, pagination. The Political Economy of Vietnam: The Evolution of State-Business Relationships Woo Cheol Lee Thesis submitted for the degree of PhD in Economics 2015 Department of Economics School of Oriental and African Studies University of London 1 Declaration for SOAS PhD thesis I have read and understood regulation 17.9 of the Regulations for students of the School of Oriental and African Studies concerning plagiarism. I undertake that all the material presented for examination is my own work and has not been written for me, in whole or in part, by any other person. I also undertake that any quotation or paraphrase from the published or unpublished work of another person has been duly acknowledged in the work which I present for examination. -

DRB-HICOM, GEELY, REACH ACCORD Heads of Agreement Signed; Definitive Agreement by Mid- July

MEDIA RELEASE IMMEDIATE RELEASE DRB-HICOM, GEELY, REACH ACCORD Heads of agreement signed; Definitive Agreement by mid- July PUTRAJAYA, 24 May 2017: DRB-HICOM Berhad (DRB-HICOM) has reached an agreement with China-based Zhejiang Geely Holding Group Co., Ltd (Geely Holding) for the Chinese car group to acquire 49.9% equity in PROTON Holdings Berhad. DRB-HICOM currently owns 100% of the manufacturer of the first national car. The two parties signed the agreement in Putrajaya today, witnessed by YB Datuk Seri Johari Abdul Ghani, the Minister of Finance II. The deal will enable PROTON to tap into Geely Holding’s vast range of platforms and powertrains, and will also enable PROTON to have access to existing markets of the Chinese carmaker, as well as right-hand drive markets in south-east Asia. DRB-HICOM Group Managing Director, Dato’ Sri Syed Faisal Albar says the PROTON brand will remain present and will grow significantly with the new foreign strategic partner on board. “Our intention was always to ensure the revitalization of the PROTON nameplate. It was Malaysia’s first national car brand and has more than 30 years of history. This deal will be the catalyst to elevate a brand that Malaysians resonate with,” said Syed Faisal. Geely Holding Group Executive Vice President and CFO Mr. Daniel Donghui Li commented, “With PROTON and Lotus joining the Geely Group portfolio of brands we strengthen our global foot print and develop a beachhead in South East Asia. Geely Holding is full of confidence for the future of PROTON, we will fully respect the brands history and culture to restore PROTON to its former glory with the support of Geely’s innovative technology and management resources. -

Freedom to Move in a Personal, Sustainable and Safe Way

VOLVO CAR GROUP ANNUAL REPORT 2020 Freedom to move in a personal, sustainable and safe way TABLE OF CONTENTS OVERVIEW 4 2020 Highlights 6 CEO Comment 8 Our Strenghts 10 The Volvo Car Group 12 Our Strategic Affiliates THE WORLD AROUND US 16 Consumer Trends 18 Technology Shift OUR STRATEGIC FRAMEWORK 22 Our Purpose 24 Strategic Framework HOW WE CREATE VALUE 28 Our Stakeholders 30 Our People and Culture 32 Product Creation 38 Industrial Operations 42 Commercial Operations MANAGEMENT REPORT 47 Board of Directors Report 52 Enterprise Risk Management 55 Corporate Governance Report FINANCIAL STATEMENTS 60 Contents Financial Report 61 Consolidated Financial Statements 67 Notes to the Consolidated Financial Statements 110 Parent Company Financial Statements 112 Notes to the Parent Company Financial Statements 118 Auditor’s Report 120 Board of Directors 122 Executive Management Team Freedom to move SUSTAINABILITY INFORMATION 124 Sustainability Management and Governance 129 Performance 2020 PERSONAL SUSTAINABLE SAFE 139 Sustainability Scorecard 144 GRI Index Cars used to be the symbol for personal freedom. Owning a car meant that you had the We commit to developing We commit to the highest We commit to pioneering 146 TCFD Index means to be independently mobile – that you owned not just a vehicle, but choice as and building the most per- standard of sustainability the safest, most intelligent 147 Auditor's Limited Assurance Report on sonal solutions in mobility: in mobility to protect technology solutions in Sustainability well. Nothing of that has changed, but the world we live in has. The earth, our cities and to make life less compli- the world we share. -

Joint Media Statement by Drb-Hicom and Zhejiang Geely Holding Group

MEDIA RELEASE IMMEDIATE ISSUANCE JOINT MEDIA STATEMENT BY DRB-HICOM AND ZHEJIANG GEELY HOLDING GROUP DRB-HICOM, Geely Holding names nominees to PROTON Group boards Dr. Li Chunrong, appointed CEO of PONSB, leads executive team of global experts Full revitalisation of PROTON Group underway 29 September, 2017, Shah Alam: Exactly one hundred days after the signing of the Definitive Agreement between DRB-HICOM Berhad (DRB-HICOM) and Zhejiang Geely Holding Group (Geely Holding) on 23 June, the two companies have confirmed the new board structures and part of the executive team for PROTON Holdings Berhad and its related companies (PROTON Group). Company Structure At the PROTON Holdings Berhad (PHB) level, Dato’ Sri Syed Faisal Albar remains as the Chairman, and he is joined on the board by Shaharul Farez Hassan and Amalanathan Thomas as nominees from DRB-HICOM. Farez and Nathan are both part of the senior management team at DRB-HICOM. Geely Holding has nominated Daniel Donghui Li and Feng Qing Feng as their nominees to the PHB board. Daniel Donghui Li is the current Executive Vice President and CFO of Geely Holding, while Feng is the Group Vice President and CTO of Hong Kong-listed Geely Auto. All five nominees also sit on the Perusahaan Otomobil Nasional Sdn Bhd (PONSB) board, along with Dr. Nathan Yu Ning, who is the Vice President of International Business at Geely Holding. Winfried Vahland, who was formerly the Chairman and Chief Executive Officer of Skoda Auto, is also on the board of PONSB. Syed Faisal, Farez, Nathan, Daniel Donghui Li and Dr. -

Proton Success Story

MSC.Software: User Case Study - Proton USER CASE STUDY PROTON Customer Profile: Noor Hisham Bin Ismail Mr Noor Hisham Bin Ismail is head of CAE at PROTON based in Kuala Lumpur, Malaysia. Mr Ismail and other members of the computer-aided engineering team are responsible for improving the virtual development of mechanical and structural components, sub systems and complete vehicle system at PROTON. Through Mr Ismail’s innovative process of probabilistic analysis, PROTON has been able to effectively identify areas of high-risk failure and fine-tuning engineering design alternatives. Challenge Mr Ismail’s foundation of probabilistic design methodology uses design In developing complex mechanical and structural automotive criteria based on reliability targets instead of deterministic criteria. components, going through multiple build-and-test hardware prototype First, design parameters such as applied loads, material strength, and cycles to verify performance, stress and fatigue life is just too time- operational parameters are researched and/or measured and then consuming and expensive. This issue can be addressed by evaluating statistically defined. A probabilistic analysis model is then developed for and refining designs with analysis tools up front in development, reducing the entire system and solutions performed to yield failure probabilities. test cycles later in the development process. PROTON’s pioneering spirit With MSC’s FEA, applied stress is obtained from finite element models. naturally has led Mr ismail to not just stop at traditional methodologies in The general concept is to integrate the joint probability of applied stress computer-aided engineering for design analysis. As the risk of failure in and material strength over the region where stress exceeds strength. -

Comparative Political Economic Analysis of Automotive Industrial Policies in Malaysia and Thailand

60 State and Industrial Policy State and Industrial Policy: Comparative Political Economic Analysis of Automotive Industrial Policies in Malaysia and Thailand Wan-Ping Tai Cheng Shiu University, Taiwan Samuel C. Y. Ku National Sun Yat-Sen University, Taiwan Abstract Numerous differences exist between the neoclassical and national development schools of economics on how an economy should develop. For example, should the state interfere in the market using state resources, and cultivate certain industries to achieve specific developmental goals? Although the automotive industries in both Thailand and Malaysia developed in the 1970s with considerable government involvement, they have evolved along very different lines. Can these differences be traced to different interactions between the state and industry in these two countries? This paper examines this issue and finds that although industries in developing countries need government assistance, the specific political and economic contexts of each country affect the policies adopted and their effectiveness. The choice between “autonomous development” (Malaysia) and “dependent development” (Thailand) is the first issue. The second issue is that politics in Malaysia has deterred the automotive industry from adopting a “market following” position. This paper finds that the choice of strategy and political interference are the two main reasons the automotive industry in Malaysia is less competitive than that in Thailand. Keywords: Automotive Industry, Developmental State, Malaysia Automotive Industry, Thai Automotive Industry, PROTON, Political Economic Analysis Introduction sectors and industries as diverse as iron, oil, manufacturing, sales, the stock market, In the wake of the 2008 economic crash, credit, and insurance. Because of the huge whether the U.S. -

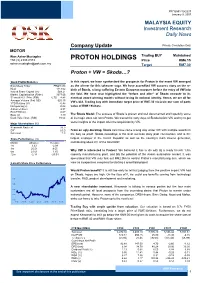

PROTON HOLDINGS Price RM6.15 [email protected] Target RM7.30

PP/10551/10/2007 January 9, 2007 MALAYSIA EQUITY Investment Research Daily News Private Circulation Only Company Update MOTOR Wan Azhar Mustapha Trading BUY Maintained +60 (3) 2333 8373 PROTON HOLDINGS Price RM6.15 [email protected] Target RM7.30 Proton + VW = Skoda…? Stock Profile/Statistics In this report, we have synthesized the prospects for Proton in the event VW emerged Bloomberg Ticker PROH MK as the winner for this takeover saga. We have accredited VW success story on the re- KLCI 1113.02 birth of Škoda, a long suffering Eastern European marques before the entry of VW into Issued Share Capital (m) 549.21 Market Capitalisation (RMm) 3377.66 the fold. We have also highlighted the “before and after” of Škoda en-route to its 52 week H | L Price (RM) 6.75 4.48 eventual award winning models without losing its national identity. Hence, we are all for Average Volume (3m) ‘000 625.15 VW’s bid. Trading buy with immediate target price of RM7.30 vis-à-vis our sum of parts YTD Returns (%) -0.45 Net gearing (x) -0.02 value of RM9.19/share. Altman Z-Score 2.97 ROCE/WACC -0.07 Beta (x) 1.49 The Škoda Model. The success of Škoda is proven and well documented and hopefully some Book Value/share (RM) 10.64 of its magic does rub onto Proton. We traced the early days of Škoda before VW and try to get some insights of the impact after the acquisition by VW. Major Shareholders (%) Khazanah Nasional 38.3 EPF 10.5 From an ugly duckling. -

China Autos Driving the EV Revolution

Building on principles One-Asia Research | August 21, 2020 China Autos Driving the EV revolution Hyunwoo Jin [email protected] This publication was prepared by Mirae Asset Daewoo Co., Ltd. and/or its non-U.S. affiliates (“Mirae Asset Daewoo”). Information and opinions contained herein have been compiled in good faith from sources deemed to be reliable. However, the information has not been independently verified. Mirae Asset Daewoo makes no guarantee, representation, or warranty, express or implied, as to the fairness, accuracy, or completeness of the information and opinions contained in this document. Mirae Asset Daewoo accepts no responsibility or liability whatsoever for any loss arising from the use of this document or its contents or otherwise arising in connection therewith. Information and opin- ions contained herein are subject to change without notice. This document is for informational purposes only. It is not and should not be construed as an offer or solicitation of an offer to purchase or sell any securities or other financial instruments. This document may not be reproduced, further distributed, or published in whole or in part for any purpose. Please see important disclosures & disclaimers in Appendix 1 at the end of this report. August 21, 2020 China Autos CONTENTS Executive summary 3 I. Investment points 5 1. Geely: Strong in-house brands and rising competitiveness in EVs 5 2. BYD and NIO: EV focus 14 3. GAC: Strategic market positioning (mass EVs + premium imported cars) 26 Other industry issues 30 Global company analysis 31 Geely Automobile (175 HK/Buy) 32 BYD (1211 HK/Buy) 51 NIO (NIO US/Buy) 64 Guangzhou Automobile Group (2238 HK/Trading Buy) 76 Mirae Asset Daewoo Research 2 August 21, 2020 China Autos Executive summary The next decade will bring radical changes to the global automotive market. -

Geely Group Chairman Li Shufu, Hosts Exhibition for Prime Ministers of China and Belgium

Geely owner Li Shufu showing Chinese and Belgian PMs Li Keqiang and Charles Michel the CMA architecture. Photo by VCC Eric Demunier Jun 03, 2017 09:32 CEST Geely Group Chairman Li Shufu, hosts exhibition for Prime Ministers of China and Belgium Li Shufu, the chairman and owner of Zhejiang Geely Holding Group,hosted an event showcasing the Geely global footprint and capabilities towards Li Keqiang, Prime Minister of the People’s Republic of China and Charles Michel, Prime Minister of Belgium, on June 2nd in Brussels. The two Prime Ministers were, as part of an official visit, treated to a presentation of the CMA car architecture which CEVT has been responsible to develop for the coming small and midsize cars of Geely and Volvo Cars. Furthermore the exhibition showcased the new Lynk&Co 01 as well as key innovations within autonomous driving and connectivity by Volvo. For more information, visit Geely Holding's website or the Volvo Cars online newsroom: Geely Holding Online Volvo Cars Media room For more information about CEVT, please visit the CEVT Website CEVT is an innovation and development center for future technologies of the Geely Group with the purpose of being at the forefront of new developments in mobility The whole industry is now undergoing a transformation with new ways of thinking about the car as a product. CEVT is a fast growing, fast moving and exciting company where no day is like the other – where the challenges of tomorrow are on our working table today. CEVT consists of some 2000 people with offices in Gothenburg and Trollhättan in Sweden. -

Geely Holding Group and Renault Group to Sign MOU on Joint Cooperation in China and South Korean Markets

Geely Holding Group and Renault Group to sign MOU on joint cooperation in China and South Korean Markets • Geely Holding and Renault Group have signed a MOU to accelerate ‘Renaulution Plan’ in China and South Korea. • In China, both partners will jointly introduce Renault-branded hybrid vehicles. • In South Korea, Geely Holding and Renault Group will explore localization of vehicles based on Lynk & Co energy efficient platforms. • Geely Holding and Renault Group will enhance their competitive advantages in technology and industrial systems to create leading mobility experience. 9th August 2021, Hangzhou China and Paris France. Renault Group, a global company with French roots and 120 years of history in the automotive industry, and Geely Holding Group, China’s largest privately-owned automotive group, today jointly announced an MoU framework agreement to create an innovative cooperation. The cooperation, focused on China and South Korea as initial key core markets, will allow Renault Group and Geely Holding to share resources and technologies. The focus will be on hybrid vehicles in the fast-growing Asian markets. Following the adoption by Geely Holding’s opensource strategy for its full vehicle architectures, Geely Holding will partner with Renault Group in the Chinese and Korean markets. In China, based on Geely Holding’s existing technologies and mature industrial footprint, both partners will jointly introduce Renault- branded hybrid vehicles. Renault will contribute on branding strategy, channel and service development, defining appropriate customer journey. In South Korea, where Renault Samsung Motors has over two decades of experience, the MoU allows Renault Group and Geely Holding to jointly explore localization of vehicles based on Lynk & Co’s energy-efficient vehicle platforms for local markets.