Spanish Broadcasting System, Inc. (Exact Name of Registrant As Specified in Its Charter)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

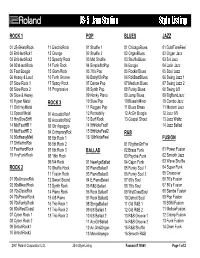

PTSVNWU JS-5 Jam Station Style Listing

PTSVNWU JS-5 Jam Station Style Listing ROCK 1 POP BLUES JAZZ 01 JS-5HardRock 11 ElectricRock 01 Shuffle 1 01 ChicagoBlues 01 DublTimeFeel 02 BritHardRck1 12 Grunge 02 Shuffle 2 02 OrganBlues 02 Organ Jazz 03 BritHardRck2 13 Speedy Rock 03 Mid Shuffle 03 ShuffleBlues 03 5/4 Jazz 04 80'sHardRock 14 Funk Rock 04 Simple8btPop 04 Boogie 04 Latin Jazz 05 Fast Boogie 15 Glam Rock 05 70's Pop 05 Rockin'Blues 05 Soul Jazz 06 Heavy & Loud 16 Funk Groove 06 Early80'sPop 06 RckBeatBlues 06 Swing Jazz 1 07 Slow Rock 1 17 Spacy Rock 07 Dance Pop 07 Medium Blues 07 Swing Jazz 2 08 Slow Rock 2 18 Progressive 08 Synth Pop 08 Funky Blues 08 Swing 6/8 09 Slow & Heavy 09 Honky Piano 09 Jump Blues 09 BigBandJazz 10 Hyper Metal ROCK 3 10 Slow Pop 10 BluesInMinor 10 Combo Jazz 11 Old HvyMetal 11 Reggae Pop 11 Blues Brass 11 Modern Jazz 12 Speed Metal 01 AcousticRck1 12 Rockabilly 12 AcGtr Boogie 12 Jazz 6/8 13 HvySlowShffl 02 AcousticRck2 13 Surf Rock 13 Gospel Shout 13 Jazz Waltz 14 MidFastHR 1 03 Gtr Arpeggio 14 8thNoteFeel1 14 Jazz Ballad 15 MidFastHR 2 04 CntmpraryRck 15 8thNoteFeel2 R&B 16 80sHeavyMetl 05 8bt Rock 1 16 16thNoteFeel FUSION 17 ShffleHrdRck 06 8bt Rock 2 01 RhythmGtrFnk 18 FastHardRock 07 8bt Rock 3 BALLAD 02 Brass Funk 01 Power Fusion 19 HvyFunkRock 08 16bt Rock 03 Psyche-Funk 02 Smooth Jazz 09 5/4 Rock 01 NewAgeBallad 04 Cajun Funk 03 Wave Shuffle ROCK 2 10 Shuffle Rock 02 PianoBallad1 05 Funky Soul 1 04 Super Funk 11 Fusion Rock 03 PianoBallad2 06 Funky Soul 2 05 Crossover 01 90sGrooveRck 12 Sweet Sound 04 E.PianoBalad 07 60's Soul 06 -

Background Music

BACKGROUND MUSIC GET THE BEST MUSIC ALL DAY LONG TouchTunes’ music programmers are passionate about music. They create a variety of fully licensed background music channels for TouchTunes locations to choose from. From Classic Rock and The Hits to Decades Variety and Holiday Mix, TouchTunes jukeboxes are designed to keep the party going all night long while still allowing patrons to make their own song selections. HIGHLIGHTS • Fully licensed for commercial establishments • Over 20 themed music channels to choose from • Each channel features over 30 hours of music • Refreshed monthly with new music • Channels can be changed instantly using the jukebox remote • Can be scheduled for a specific time of the day or all day long LITCMP V.032016 BACKGROUND MUSIC ADULT CONTEMPORARY REGGAE Easy light favorites from the ‘90s to today. Classic jams from Reggae legends. ALTERNATIVE ROCK THE HITS A diverse selection of alternative rock songs. A mix of current and mainstream hits across all genres. BLUES URBAN & HIP HOP A contemporary collection of blues artists. A contemporary mix of urban and hip-hop songs. CLASSIC R&B & SOUL ROCK MIX Sounds from the pioneers of R&B and Soul. The ultimate rock selection featuring timeless rock songs from CLASSIC ROCK the past 30 years. Rock’s biggest bands and timeless hits. DECADES VARIETY COUNTRY MIX Great songs by great artists from the 70’s to today. Mid-tempo mix of country music from the last 30 years. LATIN MIX EASY LISTENING A mix of Latin styles including Regional Mexican, Pop Rock, Lite pop and rock hits from the ‘80s, ‘90s and today. -

Spanglish Code-Switching in Latin Pop Music: Functions of English and Audience Reception

Spanglish code-switching in Latin pop music: functions of English and audience reception A corpus and questionnaire study Magdalena Jade Monteagudo Master’s thesis in English Language - ENG4191 Department of Literature, Area Studies and European Languages UNIVERSITY OF OSLO Spring 2020 II Spanglish code-switching in Latin pop music: functions of English and audience reception A corpus and questionnaire study Magdalena Jade Monteagudo Master’s thesis in English Language - ENG4191 Department of Literature, Area Studies and European Languages UNIVERSITY OF OSLO Spring 2020 © Magdalena Jade Monteagudo 2020 Spanglish code-switching in Latin pop music: functions of English and audience reception Magdalena Jade Monteagudo http://www.duo.uio.no/ Trykk: Reprosentralen, Universitetet i Oslo IV Abstract The concept of code-switching (the use of two languages in the same unit of discourse) has been studied in the context of music for a variety of language pairings. The majority of these studies have focused on the interaction between a local language and a non-local language. In this project, I propose an analysis of the mixture of two world languages (Spanish and English), which can be categorised as both local and non-local. I do this through the analysis of the enormously successful reggaeton genre, which is characterised by its use of Spanglish. I used two data types to inform my research: a corpus of code-switching instances in top 20 reggaeton songs, and a questionnaire on attitudes towards Spanglish in general and in music. I collected 200 answers to the questionnaire – half from American English-speakers, and the other half from Spanish-speaking Hispanics of various nationalities. -

Download Internet Service Channel Lineup

INTERNET CHANNEL GUIDE DJ AND INTERRUPTION-FREE CHANNELS Exclusive to SiriusXM Music for Business Customers 02 Top 40 Hits Top 40 Hits 28 Adult Alternative Adult Alternative 66 Smooth Jazz Smooth & Contemporary Jazz 06 ’60s Pop Hits ’60s Pop Hits 30 Eclectic Rock Eclectic Rock 67 Classic Jazz Classic Jazz 07 ’70s Pop Hits Classic ’70s Hits/Oldies 32 Mellow Rock Mellow Rock 68 New Age New Age 08 ’80s Pop Hits Pop Hits of the ’80s 34 ’90s Alternative Grunge and ’90s Alternative Rock 70 Love Songs Favorite Adult Love Songs 09 ’90s Pop Hits ’90s Pop Hits 36 Alt Rock Alt Rock 703 Oldies Party Party Songs from the ’50s & ’60s 10 Pop 2000 Hits Pop 2000 Hits 48 R&B Hits R&B Hits from the ’80s, ’90s & Today 704 ’70s/’80s Pop ’70s & ’80s Super Party Hits 14 Acoustic Rock Acoustic Rock 49 Classic Soul & Motown Classic Soul & Motown 705 ’80s/’90s Pop ’80s & ’90s Party Hits 15 Pop Mix Modern Pop Mix Modern 51 Modern Dance Hits Current Dance Seasonal/Holiday 16 Pop Mix Bright Pop Mix Bright 53 Smooth Electronic Smooth Electronic 709 Seasonal/Holiday Music Channel 25 Rock Hits ’70s & ’80s ’70s & ’80s Classic Rock 56 New Country Today’s New Country 763 Latin Pop Hits Contemporary Latin Pop and Ballads 26 Classic Rock Hits ’60s & ’70s Classic Rock 58 Country Hits ’80s & ’90s ’80s & ’90s Country Hits 789 A Taste of Italy Italian Blend POP HIP-HOP 750 Cinemagic Movie Soundtracks & More 751 Krishna Das Yoga Radio Chant/Sacred/Spiritual Music 03 Venus Pop Music You Can Move to 43 Backspin Classic Hip-Hop XL 782 Holiday Traditions Traditional Holiday Music -

“Standardization of Cultural Products in Latin Pop-Music”

“STANDARDIZATION OF CULTURAL PRODUCTS IN LATIN POP-MUSIC” RESEARCH PAPER PREPARED FOR THE 28TH ANNUAL ILASSA CONFERENCE ON LATIN AMERICA TO BE HELD AT THE UNIVERSITY OF TEXAS AT AUSTIN FROM FEBRUARY 7TH THROUGH FEBRUARY 9TH ISRAEL ALONSO CHAVEZ LATIN AMERICAN AND CARIBBEAN CENTER FLORIDA INTERNATIONAL UNIVERSITY MIAMI, FLORIDA [email protected] 2008 Introduction 2 This work represents the initial stage of a project whose seed germinated thanks in part to what seems to be an ongoing debate between two different approaches to music in the sociological field. The first approach puts much of its emphasis on the functional dimension of music. That is, on the social functions it performs, enables and enhances; but also on its economic functionality. The subservience of music to economic ends does not imply a loss in terms of creativity for the representatives of this perspective. The second perspective does not deny that music fulfills certain economic and social functions. Yet, unlike the former, the latter warns against the atrophy of creativity that can be brought about by the models implented by “the culture industries”, to use Theodor W. Adorno’s concept. My concern here lies with the question of whether the claims made by this important member of the Frankfurt school about the products of “the culture industries” can be substantiated with empirical evidence. I want to investigate whether popular music (Latin pop music in this case) is indeed, as Adorno says, just another standardized product fashioned after the formulas of “the culture industries”. This work, however, forms part of a broader preoccupation with the issue of musical style, what causes it and what makes it change. -

Bringing Mexican Regional Music to Market Amanda Maria Morrison University of Texas at Austin, [email protected]

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by SJSU ScholarWorks San Jose State University SJSU ScholarWorks National Association for Chicana and Chicano 2008: 35th Annual: Poesia, Baile, y Cancion - Studies Annual Conference Austin, TX Apr 1st, 5:00 AM Too Mex for the Masses: Bringing Mexican Regional Music to Market Amanda Maria Morrison University of Texas at Austin, [email protected] Follow this and additional works at: http://scholarworks.sjsu.edu/naccs Part of the Chicano Studies Commons, Ethnic Studies Commons, Music Commons, and the Race and Ethnicity Commons Amanda Maria Morrison, "Too Mex for the Masses: Bringing Mexican Regional Music to Market" (April 1, 2008). National Association for Chicana and Chicano Studies Annual Conference. Paper 12. http://scholarworks.sjsu.edu/naccs/2008/Proceedings/12 This Event is brought to you for free and open access by the Conferences at SJSU ScholarWorks. It has been accepted for inclusion in National Association for Chicana and Chicano Studies Annual Conference by an authorized administrator of SJSU ScholarWorks. For more information, please contact [email protected]. Amanda Maria Morrison Department of Anthropology University of Texas at Austin 2008 NACCS Conference Presentation Too Mex for the Masses: Bringing Mexican Regional Music to Market The notion of a “Latin boom” in the music industry typically conjures the swiveling hips and buoyant salsa-infused rhythms of pop performers like Ricky Martin and Shakira or, more recently, the driving island beats of reggaeton. Few imagine a Stetson-sporting vaquero as a representative figure of the contemporary Latin music scene. -

Playnetwork Business Mixes

PlayNetwork Business Mixes 50s to Early 60s Marketing Strategy: Period themes, burgers and brews and pizza, bars, happy hour Era: Classic Compatible Music Styles: Fun-Time Oldies, Classic Description: All tempos and styles that had hits Rock, 70s Mix during the heyday of the 50s and into the early 60s, including some country as well Representative Artists: Elvis, Fats Domino, Steve 70s Mix Lawrence, Brenda Lee, Dinah Washington, Frankie Era: 70s Valli and the Four Seasons, Chubby Checker, The Impressions Description: An 8-track flashback of great music Appeal: People who can remember and appreciate from the 70s designed to inspire memories for the major musical moments from this era everyone. Featuring hits and historically significant album cuts from the “Far Out!,” Bob Newhart, Sanford Feel: All tempos and Son era Marketing Strategy: Hamburger/soda fountain– Representative Artists: The Eagles, Elton John, themed cafes, period-themed establishments, bars, Stevie Wonder, Jackson Brown, Gerry Rafferty, pizza establishments and clothing stores Chicago, Doobie Brothers, Brothers Johnson, Alan Parsons Project, Jim Croce, Joni Mitchell, Sugarloaf, Compatible Music Styles: Jukebox classics, Donut Steely Dan, Earth Wind & Fire, Paul Simon, Crosby, House Jukebox, Fun-Time Oldies, Innocent 40s, 50s, Stills, and Nash, Creedence Clearwater Revival, 60s Average White Band, Bachman-Turner Overdrive, Electric Light Orchestra, Fleetwood Mac, Guess Who, 60s to Early 70s Billy Joel, Jefferson Starship, Steve Miller Band, Carly Simon, KC & the Sunshine Band, Van Morrison Era: Classic Feel: A warm blanket of familiar music that helped Description: Good-time pop and rock legends from define the analog sound of the 70s—including the the mid-60s through the early-to-mid-70s that marked one-hit wonders and the best known singer- the end of an era. -

20 GREATEST Latin Grammys Moments Over 20 Years

Recuerdos: 20 GREATEST j2000 Ricky Martin, Celia Cruz and Gloria Estefan pay homage To Tito Puente (Staples Center, Los Angeles, 2000): During the inaugural Latin Grammy ceremony, Puerto Rican millennium breakout star Ricky Martin teams up with Latin GrammyS Cuban-American icon Gloria Estefan and the Queen of Salsa Celia Cruz for a rare yet memorable performance. Honoring Tito Puente, the Fania All-Star legend Moments Over and pioneer of Afro-Latin jazz who passed away in 2000, the trio of icons deliver a tropical storm of his hits like “Quimbara,” “Oriente” and “Oye Como Va.” The For two decades, the Biggest Night in Latin Music has witnessed latter hit from 1962 became immortalized by Santana’s 1971 rendition. 20 Years a myriad of unforgettable scenes that have gone down in both television and Latin music history. From norteño and rock legends g Santana and Maná’s double threat (Staples Center, Los delivering bold statements to unlikely acts making music magic, Angeles, 2000): The guitar virtuoso is joined by the Mexican here are the 20 most epic performances at the Latin Grammys. pop-rock idols for an electric performance of the 2000 Latin by ISABELA RAYGOZA Grammy Record of the Year song “Corazón Espinado.” The riveting showcase saw the then-53- year-old Woodstock icon pierce through bursting flares of guitar h Latin music all-stars fretwork that paired well with remember Celia Cruz Maná’s knack for sun-soaked (American Airlines Arena, tropical rock. The riveting 2003 Miami, 2003): A star-studded lovelorn song, which picked up performance by Gloria Estefan, another Latin Grammy win for Willie Colón, Marc Anthony, Best Rock Performance by a Duo Oscar Leon, Johnny Pacheco or Group, has become a Latin and others unite to honor the rock classic for both groups. -

Bringing Mexican Regional Music to Market

San Jose State University SJSU ScholarWorks 2008: 35th Annual: Poesia, Baile, y Cancion - NACCS Annual Conference Proceedings Austin, TX Apr 1st, 5:00 AM Too Mex for the Masses: Bringing Mexican Regional Music to Market Amanda Maria Morrison University of Texas at Austin, [email protected] Follow this and additional works at: https://scholarworks.sjsu.edu/naccs Part of the Chicana/o Studies Commons, Ethnic Studies Commons, Music Commons, and the Race and Ethnicity Commons Morrison, Amanda Maria, "Too Mex for the Masses: Bringing Mexican Regional Music to Market" (2008). NACCS Annual Conference Proceedings. 12. https://scholarworks.sjsu.edu/naccs/2008/Proceedings/12 This Conference Proceeding is brought to you for free and open access by the National Association for Chicana and Chicano Studies Archive at SJSU ScholarWorks. It has been accepted for inclusion in NACCS Annual Conference Proceedings by an authorized administrator of SJSU ScholarWorks. For more information, please contact [email protected]. Amanda Maria Morrison Department of Anthropology University of Texas at Austin 2008 NACCS Conference Presentation Too Mex for the Masses: Bringing Mexican Regional Music to Market The notion of a “Latin boom” in the music industry typically conjures the swiveling hips and buoyant salsa-infused rhythms of pop performers like Ricky Martin and Shakira or, more recently, the driving island beats of reggaeton. Few imagine a Stetson-sporting vaquero as a representative figure of the contemporary Latin music scene. Yet this is the visual style associated with what is by far the largest-selling Latin genre in the U.S.: Mexican regional music. “Regional Mexican” is the catchall phrase the industry uses to categorize a variety of musical traditions. -

Music Guide Music HISTORY There Was a Time When “Elevator Music” Was All You Heard in a Store, Hotel, Or Other Business

Music Guide Music HisTORY There was a time when “elevator music” was all you heard in a store, hotel, or other business. Yawn. 1 1971: a group of music fanatics based out of seattle - known as Aei Music - pioneered the use of music in its original form, and from the original artists, inside of businesses. A new era was born where people could enjoy hearing the artists and songs they know and love in the places they shopped, ate, stayed, played, and worked. 1 1985: DMX Music began designing digital music channels to fit any music lover’s mood and delivered this via satellite to businesses and through cable TV systems. 1 2001: Aei and DMX Music merge to form what becomes DMX, inc. This new company is unrivaled in its music knowledge and design, licensing abilities, and service and delivery capability. 1 2005: DMX moves its home to Austin, TX, the “Live Music capital of the World.” 1 Today, our u.s. and international services reach over 100,000 businesses, 23 million+ residences, and over 200 million people every day. 1 DMX strives to inspire, motivate, intrigue, entertain and create an unforgettable experience for every person that interacts with you. Our mission is to provide you with Music rockstar service that leaves you 100% ecstatic. Music Design & Strategy To get the music right, DMX takes into account many variables including customer demographics, their general likes and dislikes, your business values, current pop culture and media trends, your overall décor and design, and more. Our Music Designers review hundreds of new releases every day to continue honing the right music experience for our clients. -

Latino/A Pop Music in the Cultural Mainstream

Seattle University School of Law Digital Commons Faculty Scholarship 1-1-2001 Will the Wolf Survive?: Latino/a Pop Music in the Cultural Mainstream Steven W. Bender Follow this and additional works at: https://digitalcommons.law.seattleu.edu/faculty Part of the Law and Society Commons Recommended Citation Steven W. Bender, Will the Wolf Survive?: Latino/a Pop Music in the Cultural Mainstream, 78 DENV. U. L. REV. 719 (2001). https://digitalcommons.law.seattleu.edu/faculty/357 This Article is brought to you for free and open access by Seattle University School of Law Digital Commons. It has been accepted for inclusion in Faculty Scholarship by an authorized administrator of Seattle University School of Law Digital Commons. For more information, please contact [email protected]. WILL THE WOLF SURVIVE?:* LATINO/A POP MUSIC IN THE CULTURAL MAINSTREAM STEVEN W. BENDER* 2 The American' news media dubbed 1999 as the year of the Latino based almost entirely on the runaway sales success3 and appeal4 of La- *. Titled after track number 11 of the same name from Los Lobos' debut album in 1984 How Will the Wolf Survive? Los LOBos, How WILL THE WOLF SURVIVE (Wea/Warner Bros. 1984). That track is an anthem of hope for cultural and spiritual survival in a challenging and changing America, as is the less hopeful Los Lobos tune One Time, One Night [In America] from 1987. Los LOBOS, One Time, One Night, on BY THE LIGHT OF THE MOON (Wea/Warner Bros. 1987). **. Associate Professor of Law, University of Oregon School of Law. Thanks to the partici- pants at LatCrit V where I presented this paper as part of the plenary Multi/Cultural Artistic Re/Presentations in Mass Media: Capitalism, Power, Privilege and Cultural Production. -

Redalyc.Pop Latinidad: Puerto Ricans in the Latin Explosion, 1999

Centro Journal ISSN: 1538-6279 [email protected] The City University of New York Estados Unidos Fiol-Matta, Licia Pop latinidad: Puerto Ricans in the latin explosion, 1999 Centro Journal, vol. XIV, núm. 1, 2002, pp. 27-51 The City University of New York New York, Estados Unidos Available in: http://www.redalyc.org/articulo.oa?id=37711290002 How to cite Complete issue Scientific Information System More information about this article Network of Scientific Journals from Latin America, the Caribbean, Spain and Portugal Journal's homepage in redalyc.org Non-profit academic project, developed under the open access initiative pgs26-51.qxd 7/22/07 3:09 PM Page 27 CENTRO Journal Volume7 xiv Number 1 spring 2002 Pop Latinidad: Puerto Ricans in the Latin Explosion, 1999 Licia Fiol-Matta Para Lynn ABSTRACT The article compares the media personas and musical performances of two Puerto Rican pop megastars, the Nuyorican Marc Anthony and the island-born Ricky Martin. I argue that both artists actively perform a Latinidad that is consumer-oriented, in which Puerto Ricanness, or better put, their performance of Puerto Ricanness, is fundamental. I relate the artists’ commercial success to the general appeal to clichéd visions of local, exotic flavor, in Martin’s case, and a weak “Puerto Rican-American” hyphen in Marc Anthony’s. I also consider the impact of marketing categories on the music itself. Drawing on previous work by scholars in Puerto Rican/Latino Studies, I attempt to make a contribution toward a critique of “consumer ethnicities” and “mapping latinidad” in the U.S.