PE & VC Key to Strong Pension Fund Returns

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2012 Annual Report on Form 10-K

first florida integrity bank UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K (Mark One) ⌧ Annual Report Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 For the fiscal year ended December 31, 2012 Transition Report Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 For the transition period from to Commission File No. 333-182414 TGR FINANCIAL, INC. (Exact name of registrant as specified in its charter) Florida 45-4250359 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 3560 Kraft Road Naples, Florida 34105 (Address of principal executive offices) (Zip Code) (239) 348-8000 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: None Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ⌧ NO Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ⌧ NO Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ⌧ YES NO Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). -

Q1 09 Fundraising Update

www.preqin.com Preqin Ltd. Q1 2009 Private Equity Fundraising Update Special Report 23rd April 2009 © 2009 Preqin Ltd. / www.preqin.com 2 ◄ Q1 2009 Fundraising Update Q1 Overview The Coming Turn in Fundraising As everyone is painfully aware, Fig. 1: fundraising conditions in Q1 2009 were dire. Looking across all private Final Close vs. Original Target equity fund types (venture, buyout, mezzanine, distressed, fund of funds etc.), a total of only 78 funds worldwide achieved fi nal closes, raising $49 billion between them. This represents a return to the kind of levels we were experiencing in 2004 following the trough of the previous fundraising depression. As bad as these headline statistics are, they actually disguise just how bad fundraising conditions had become. Faced with a very diffi cult market, many managers who were on the road decided to cut their losses and declare fi nal closes for funds that may have two-thirds of all funds closed were equity fundraising is set to rebound actually raised most of their funding achieving between 80% and 120% strongly: in interim closes six or twelve months of their targeted amount. Around previously – hence much of the money 15% of funds fell short by more than • LP Intentions: Preqin regularly in the ‘fi nal closes’ total was actually 20%, while 20-25% of funds exceeded surveys LP intentions, and even raised in previous quarters. Very little their targets by 20% or more. The in the depths of the credit crisis new money was committed in Q1 situation deteriorated markedly in Q4 in December 2008 these LPs 2009. -

As Filed with the Office of the Comptroller of the Currency On

FIRST NATIONAL BANK OF THE GULF COAST 5,412,523 Shares of Common Stock, $5.00 per share First National Bank of the Gulf Coast, a national banking association (the “Company”), is offering up to 5,412,523 shares of our common stock, par value $5.00 per share (the “Common Stock”), at a price of $5.00 per share, to certain of our existing shareholders, in a limited rights offering (the “Rights Offering”, and each right to purchase Common Stock a “Right”). These shares will be offered to certain of our shareholders of record as of 5:00 p.m., Eastern Time, on July 12, 2011 (the “Record Date,” and each eligible holder of our Common Stock as of the Record Date, an “Eligible Shareholder”). Eligible Shareholders have the right to purchase one share of Common Stock for each share of Common Stock owned (the “Basic Subscription Rights”). See “The Offering”, beginning on page 20 of this prospectus. This offering of rights to subscribe is not made pursuant to any mandatory provisions for same in the Company’s Articles of Association. Shareholders do not have preemptive rights. See “Description of Securities.” Such rights to subscribe shall be irrevocable, fully transferable and shall be evidenced by transferable subscription warrants (the “Subscription Warrants”). The rights offering will be made on an “any and all” basis, no minimum required. Eligible Shareholders are entitled to subscribe for all, or any portion, of the shares of Common Stock underlying their Basic Subscription Rights. Eligible Shareholders may also transfer their Rights to any other Eligible Shareholders or non-shareholders at their discretion. -

Attendee Bios

ATTENDEE BIOS Ejim Peter Achi, Shareholder, Greenberg Traurig Ejim Achi represents private equity sponsors in connection with buyouts, mergers, acquisitions, divestitures, joint ventures, restructurings and other investments spanning a wide range of industries and sectors, with particular emphasis on technology, healthcare, industrials, consumer packaged goods, hospitality and infrastructure. Rukaiyah Adams, Chief Investment Officer, Meyer Memorial Trust Rukaiyah Adams is the chief investment officer at Meyer Memorial Trust, one of the largest charitable foundations in the Pacific Northwest. She is responsible for leading all investment activities to ensure the long-term financial strength of the organization. Throughout her tenure as chief investment officer, Adams has delivered top quartile performance; and beginning in 2017, her team hit its stride delivering an 18.6% annual return, which placed her in the top 5% of foundation and endowment CIOs. Under the leadership of Adams, Meyer increased assets managed by diverse managers by more than threefold, to 40% of all assets under management, and women managers by tenfold, to 25% of AUM, proving that hiring diverse managers is not a concessionary practice. Before joining Meyer, Adams ran the $6.5 billion capital markets fund at The Standard, a publicly traded company. At The Standard, she oversaw six trading desks that included several bond strategies, preferred equities, derivatives and other risk mitigation strategies. Adams is the chair of the prestigious Oregon Investment Council, the board that manages approximately $100 billion of public pension and other assets for the state of Oregon. During her tenure as chair, the Oregon state pension fund has been the top-performing public pension fund in the U.S. -

P10 Holdings, Inc. Delaware 74-2961657 (State of Incorporation) (IRS Employer Identification No.)

Audited Annual Report to Shareholders for The Year Ended December 31, 2019 P10 Holdings, Inc. Delaware 74-2961657 (State of Incorporation) (IRS Employer Identification No.) 8214 Westchester Drive Suite 950 Dallas, TX 75225 (Address of principal executive office) (214) 999-0149 (Company’s telephone number) Common Stock $0.001 Par Value Trading Symbol: PIOE Trading Market: OTC Pink Open Market 110,000,000 Common Shares Authorized 89,411,175 Shares Issued and 89,234,816 Shares Outstanding As of March 27, 2020 Special Note Regarding Forward-Looking Statements The following stockholder letter contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements other than statements about historical or current facts, including, without limitation, statements about our business strategy, plans, and objectives of management and our future prospects, are forward-looking statements. You can identify forward-looking statements by words such as “may,” “will,” “expect,” “intend,” “anticipate,” “believe,” “estimate,” “seek,” “continue,” and other similar words. You should read statements that contain these words carefully because they discuss our future expectations, make projections of our future results of operations or financial condition, or state other “forward-looking” information. We claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 for all forward-looking statements. We have based these forward-looking statements on our current expectations and projections about future events. These forward-looking statements are subject to risks, uncertainties and assumptions about our business that could affect our future results and could cause those results or other outcomes to differ materially from those expressed or implied in the forward-looking statements. -

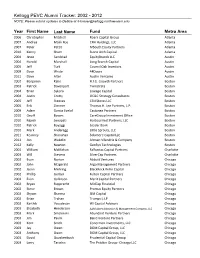

Kellogg PEVC Alumni Tracker: 2002 - 2012 NOTE: Please Submit Updates to Debbie at [email protected]

Kellogg PEVC Alumni Tracker: 2002 - 2012 NOTE: Please submit updates to Debbie at [email protected] Year First Name Last Name Fund Metro Area 2006 Christopher Mitchell Roark Capital Group Atlanta 2007 Andrea Malik Roe CRH Holdings, LLC Atlanta 2007 Peter Pettit MSouth Equity Partners Atlanta 2010 Kenny Shum Stone Arch Capital Atlanta 2004 Jesse Sandstad EquityBrands LLC Austin 2004 Harold Marshall Long Branch Capital Austin 2005 Jeff Turk Council Oak Investors Austin 2009 Dave Wride 44Doors Austin 2011 Dave Alter Austin Ventures Austin 2002 Benjamin Kahn H.I.G. Growth Partners Boston 2003 Patrick Davenport Twinstrata Boston 2004 Brian Sykora Lineage Capital Boston 2004 Justin Crotty OC&C Strategy Consultants Boston 2005 Jeff Steeves CSN Stores LLC Boston 2005 Erik Zimmer Thomas H. Lee Partners, L.P. Boston 2009 Adam Garcia Evelof Castanea Partners Boston 2010 Geoff Bowes CareGroup Investment Office Boston 2010 Rajesh Senapati HarbourVest Partners, LLC Boston 2010 Patrick Boyaggi Leader Bank Boston 2010 Mark Anderegg Little Sprouts, LLC Boston 2011 Kearney Shanahan Solamere Capital LLC Boston 2012 Jon Wakelin Altman Vilandrie & Company Boston 2012 Kelly Newton GenSyn Technologies Boston 2003 William McMahan Falfurrias Capital Partners Charlotte 2003 Will Stevens SilverCap Partners Charlotte 2002 Evan Norton Abbott Ventures Chicago 2002 John Fitzgerald Argo Management Partners Chicago 2002 Jason Mehring BlackRock Kelso Capital Chicago 2002 Phillip Gerber Fulton Capital Partners Chicago 2002 Evan Gallinson Merit Capital Partners -

September 29, 2020

Plymouth County Retirement Association September 29, 2020 Meeting Materials BOSTON CHICAGO LONDON MIAMI NEW YORK PORTLAND SAN DIEGO MEKETA.COM Plymouth County Retirement Association Agenda Agenda 1. Estimated Retirement Association Performance As of August 31, 2020 2. Performance Update As of July 31, 2020 3. Current Issues Non-Core Real Estate RFP Respondent Review Non-Core Infrastructure Finalist Presentations 4. Disclaimer, Glossary, and Notes 2 of 129 Estimated Retirement Association Performance As of August 31, 2020 3 of 129 Plymouth County Retirement Association Estimated Retirement Association Performance Estimated Aggregate Performance1 August2 QTD YTD 1 YR 3 YR 5 YR 10 YR (%) (%) (%) (%) (%) (%) (%) Total Retirement Association 2.7 6.3 0.5 7.8 5.0 6.4 7.9 Policy Benchmark 3.1 6.8 3.0 10.1 6.9 7.7 8.5 Benchmark Returns August QTD YTD 1 YR 3 YR 5 YR 10 YR (%) (%) (%) (%) (%) (%) (%) Russell 3000 7.2 13.3 9.4 21.4 14.0 13.9 14.9 MSCI EAFE 5.1 7.6 -4.6 6.4 2.3 4.7 5.9 MSCI Emerging Markets 2.2 11.3 0.5 14.5 2.8 8.7 3.8 Barclays Aggregate -0.8 0.7 6.9 6.5 5.1 4.3 3.7 Barclays TIPS 1.1 3.4 9.6 9.0 5.7 4.6 3.7 Barclays High Yield 1.0 5.7 1.7 4.7 4.9 6.5 6.9 JPM GBI-EM Global Diversified (Local Currency) -0.3 2.7 -4.4 1.7 0.7 4.6 1.3 S&P Global Natural Resources 4.0 7.6 -13.0 -1.9 -0.1 5.6 1.5 Estimated Total Assets Estimate Total Retirement Association $1,106,611,546 1 The August performance estimates are calculated using index returns as of August 31, 2020 for each asset class. -

2019 ILGIF Annual Report

2019 ANNUAL REPORT TABLE OF CONTENTS A Message from the Treasurer ���������������������������������������������������������������������3 Fund Overview ������������������������������������������������������������������������������������������������5 Why Invest in Venture Capital?..........................................................................5 Overview..............................................................................................................6 History of ILGIF...................................................................................................6 ILGIF Goals..........................................................................................................6 Vision ..................................................................................................................6 Mission ................................................................................................................6 Illinois Venture Capital Landscape ��������������������������������������������������������������7 Investment Performance ������������������������������������������������������������������������������9 Investment Activity in 2019 ������������������������������������������������������������������������������������ 10 Key Investment Updates ����������������������������������������������������������������������������������������� 10 Economic Impact ������������������������������������������������������������������������������������������12 Equity, Diversity, and Inclusion �����������������������������������������������������������������13 -

Angeleno Group 2020 ESG Report

ANGELENO GROUP RESPONSIBLE AND SUSTAINABLE INVESTING 2020 ESG REPORT 10TH EDITION 2020 ESG REPORT 0 ANGELENO GROUP TABLE OF CONTENTS …………………………………………………………………………………… Letter from Our Leadership 1 Firm Profile 2 Creating Value 4 Investing for the Future 7 Impact in Action 9 Renewable Energy 10 Energy and Resource Efficiency 12 Water 15 Smart Cities 16 Sustainable Forestry 18 Diversity, Equity and Inclusion 20 ESG at Angeleno Group 22 Our Culture 23 Stakeholder Engagement 26 Portfolio Management 30 Vision for the Next Decade 32 Invitation to Dialogue 33 Appendices I Team and Advisors II III Values and Expectations for Portfolio Companies VI 2020 Impact Metrics and Engagement Outcomes 2020 ESG REPORT 0 ANGELENO GROUP LETTER FROM OUR LEADERSHIP …………………………………………………………………………………… This ESG Report – our tenth – is a special one for Angeleno Group. The report provides us with the opportunity to reflect on how our Responsible and Sustainable Investing Program has evolved over the past decade, and also to look forward to the future and, in particular, to the decade ahead. 2020 was a momentous year in numerous ways. Being faced with the COVID-19 pandemic showed us how interconnected we are, and how adaptive and resilient we can be. The social justice movement brought to the forefront systemic discrimination issues that businesses and society must address. The public and private markets exhibited remarkable growth in the clean energy sector. An inflection point was also reached among investors, corporations and governments that the need to transition to a low carbon economy cannot be delayed – and that a commitment to ESG principles will be integral to achieving long-term returns and creating shared value for all. -

Preqin Special Report: Northeast US Real Estate

Content Includes: Preqin Special Report: Northeast US Real Estate May 2015 Fundraising All Northeast US-focused funds closed in 2014 focus primarily on value added investments. Funds in Market Opportunistic funds account for the majority of Northeast US-focused funds in market. Fund Managers More than a third of Northeast US-based fund managers are raising their first fund. Institutional Investors Majority of Northeast US- based investors are below their target allocations to real estate. alternative assets. intelligent data. Download the data pack at: Preqin Special Report: Northeast US Real Estate www.preqin.com/USRE15 Foreword The Northeast contains some of the United States’ largest real estate markets and is home to some of the largest real estate players globally. It is also the base of many specialist real estate fund managers that have raised a combined $7.4bn over the last fi ve years. Over 550 real estate fund managers have set up shop in the Northeast US, with the majority based in the global hub of New York. Additionally, the Northeast US holds many large institutional investors that are willing to invest in real estate within their home region. In this report, we look at the state of the private real estate market in the Northeast US by examining historical fundraising, funds in market, fund managers and investors that are based in the region, drawing on the wealth of individual fi rm- and fund-level data available on Preqin’s Real Estate Online service. Key Findings Capital Raised by Private Real Estate Firms in the Last 10 Years ($bn) Total funds raised in the last 10 years $$397bn397bn by real estate fund managers based in Northeast US. -

2007 Annual Report

CONNECT 2007 ANNUAL REPORT Recycled 100% Supporting responsible use of forest resources www.fsc.org Cert no. SW-COC-002680 © 1996 Forest Stewardship Council Founding Chair’s Letter FOUNDING CHAIRMAN’S LETTER: CARL D. THOMA It seems like only yesterday that we celebrated the debut of the Before the IVCA, our city and state lacked the informal network Illinois Venture Capital Association at a gala party, distributing the that fuses venture capitalists, emerging enterprises, academics poster “Dawn of America” that the late Chicago artist Ed Paschke and government offi cials. These networks are essential to create made especially for IVCA as well as chocolate gold coins bearing work and wealth – work for many new employees in our state the IVCA logo. It was the start of a new century. We sought to stir and wealth for those innovators and investors that forge and some excitement into the state’s private equity and venture capital launch successful start-ups. industry and the entrepreneurial community and, in the process, foster a great deal more networking. The IVCA has become that nurturing network as well as an organization regarded in the state legislature and in the That was seven years ago – and what a difference those ensuing media for getting things done. Just glance at our calendar years have made. We have grown from an organization with 28 of events. members to 129 members. We have become an active – some might say activist – trade association, lobbying arm and meeting Through this initial report of the IVCA, I think you will quickly place. We have widened our net, too, embracing academic members recognize that our voice is the voice of our members – and this and service providers essential to our industry and association, united voice grows stronger and more powerful every year. -

2010 ANNUAL REPORT :: a DECADE of INFLUENCE Introduction

20 10 2010 ANNUAL REPORT :: A DECADE OF INFLUENCE INTRODUCTION IT BEGAN DURING THE FIRST INTERNET BOOM AS THE GERM OF AN IDEA BY A LEGISLATIVE AIDE1 TO AN ILLINOIS STATE LAWMAKER: Why not launch an organization to serve as the voice of private equity and venture capital in Illinois and Chicago, America’s crossroads? Championed by a private- equity legend in Chicago,2 the group originally focused on legislative issues critical to venture capital and private equity investing and on building its membership during an increasingly troubled tech economy. Now, on its 10th anniversary, the organization – the Illinois Venture Capital Association – prevails as the most influential advocate for Illinois’ venture and private equity investing. It delivers superbly on the three elements of its mission: Invest in Illinois; Advocate for venture capital and private equity; Serve its member- ship. In the process, it has become a determined activist for advancing Illinois as an Innovation Economy. Indeed, except for the National Venture Capital Association on the countrywide stage, the IVCA has forged the most distinctive and influential voice for venture capital and private equity investors of any state or regional organization. The IVCA’s executive director, its board members and others active in the association increasingly are sought after by legislators, entrepreneurs, business development officials and the media for their counsel on issues important to the industry. Today, the IVCA’s mission and activities are more high profile and intensified than at any time during the last decade because of venture and private equity investing’s huge and positive impact on the state’s economy.