Q1 09 Fundraising Update

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2012 Annual Report on Form 10-K

first florida integrity bank UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K (Mark One) ⌧ Annual Report Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 For the fiscal year ended December 31, 2012 Transition Report Pursuant to Section 13 or 15(d) of The Securities Exchange Act of 1934 For the transition period from to Commission File No. 333-182414 TGR FINANCIAL, INC. (Exact name of registrant as specified in its charter) Florida 45-4250359 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) 3560 Kraft Road Naples, Florida 34105 (Address of principal executive offices) (Zip Code) (239) 348-8000 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: None Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ⌧ NO Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ⌧ NO Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ⌧ YES NO Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). -

As Filed with the Office of the Comptroller of the Currency On

FIRST NATIONAL BANK OF THE GULF COAST 5,412,523 Shares of Common Stock, $5.00 per share First National Bank of the Gulf Coast, a national banking association (the “Company”), is offering up to 5,412,523 shares of our common stock, par value $5.00 per share (the “Common Stock”), at a price of $5.00 per share, to certain of our existing shareholders, in a limited rights offering (the “Rights Offering”, and each right to purchase Common Stock a “Right”). These shares will be offered to certain of our shareholders of record as of 5:00 p.m., Eastern Time, on July 12, 2011 (the “Record Date,” and each eligible holder of our Common Stock as of the Record Date, an “Eligible Shareholder”). Eligible Shareholders have the right to purchase one share of Common Stock for each share of Common Stock owned (the “Basic Subscription Rights”). See “The Offering”, beginning on page 20 of this prospectus. This offering of rights to subscribe is not made pursuant to any mandatory provisions for same in the Company’s Articles of Association. Shareholders do not have preemptive rights. See “Description of Securities.” Such rights to subscribe shall be irrevocable, fully transferable and shall be evidenced by transferable subscription warrants (the “Subscription Warrants”). The rights offering will be made on an “any and all” basis, no minimum required. Eligible Shareholders are entitled to subscribe for all, or any portion, of the shares of Common Stock underlying their Basic Subscription Rights. Eligible Shareholders may also transfer their Rights to any other Eligible Shareholders or non-shareholders at their discretion. -

The Art of Exiteering

THE ART OF EXITEERING In conversation with European tech founders NOTION INSIGHTS Start. Grow. Succeed 1 Notion Insights is published by Notion Capital, 91 Wimpole Street, London W1G 0EF. Registered address: Third Floor, 1 New Fetter Lane, London EC4A 1AN Contact Notion Capital is a trading name of The Fund Incubator +44 (0)845 498 9393 Limited – registered in Scotland Co No SC218683. [email protected] MBM COMMERCIAL, 5th Floor 125 Princes Street, Edinburgh, Scotland, EH2 4AD. Content Authorised and Regulated by the Financial For opportunities to contribute to future editions Conduct Authority. of Notion Insights please contact Kate Hyslop. Reproduction in whole or in part without written Design permission is strictly prohibited. [email protected] © 2017 Notion Capital. All rights reserved. The Art of Exiteering is brought to you by Supported by 2 3 Contents The Art of Exiteering: In conversation with European tech founders 6 / Introduction 44 / Professional Perspectives 82 / The Qlik Story Stephen Chandler Daniel Glazer, Steven Bernard Måns Hultman and Bradley Finkelstein 8 / The Advisor’s View – from the EY Fast Growth Team Wilson Sonsini Goodrich & Rosati 86 / Professional Perspectives Kevin McGovern, Advisor 10/ Executive Summary 49 / The Hybris Story The Art of Exiteering: In conversation Stefan Schmidt 91 / The Thunderhead Story with European tech founders Glen Manchester 54 / The MessgeLabs Story 16 / The Astonishing Tribe Story Ben White, Jos White, Stephen Chandler 96 / The Scansafe Story Hampus Jakobsson and Chris -

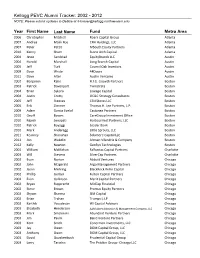

Kellogg PEVC Alumni Tracker: 2002 - 2012 NOTE: Please Submit Updates to Debbie at [email protected]

Kellogg PEVC Alumni Tracker: 2002 - 2012 NOTE: Please submit updates to Debbie at [email protected] Year First Name Last Name Fund Metro Area 2006 Christopher Mitchell Roark Capital Group Atlanta 2007 Andrea Malik Roe CRH Holdings, LLC Atlanta 2007 Peter Pettit MSouth Equity Partners Atlanta 2010 Kenny Shum Stone Arch Capital Atlanta 2004 Jesse Sandstad EquityBrands LLC Austin 2004 Harold Marshall Long Branch Capital Austin 2005 Jeff Turk Council Oak Investors Austin 2009 Dave Wride 44Doors Austin 2011 Dave Alter Austin Ventures Austin 2002 Benjamin Kahn H.I.G. Growth Partners Boston 2003 Patrick Davenport Twinstrata Boston 2004 Brian Sykora Lineage Capital Boston 2004 Justin Crotty OC&C Strategy Consultants Boston 2005 Jeff Steeves CSN Stores LLC Boston 2005 Erik Zimmer Thomas H. Lee Partners, L.P. Boston 2009 Adam Garcia Evelof Castanea Partners Boston 2010 Geoff Bowes CareGroup Investment Office Boston 2010 Rajesh Senapati HarbourVest Partners, LLC Boston 2010 Patrick Boyaggi Leader Bank Boston 2010 Mark Anderegg Little Sprouts, LLC Boston 2011 Kearney Shanahan Solamere Capital LLC Boston 2012 Jon Wakelin Altman Vilandrie & Company Boston 2012 Kelly Newton GenSyn Technologies Boston 2003 William McMahan Falfurrias Capital Partners Charlotte 2003 Will Stevens SilverCap Partners Charlotte 2002 Evan Norton Abbott Ventures Chicago 2002 John Fitzgerald Argo Management Partners Chicago 2002 Jason Mehring BlackRock Kelso Capital Chicago 2002 Phillip Gerber Fulton Capital Partners Chicago 2002 Evan Gallinson Merit Capital Partners -

Angeleno Group 2020 ESG Report

ANGELENO GROUP RESPONSIBLE AND SUSTAINABLE INVESTING 2020 ESG REPORT 10TH EDITION 2020 ESG REPORT 0 ANGELENO GROUP TABLE OF CONTENTS …………………………………………………………………………………… Letter from Our Leadership 1 Firm Profile 2 Creating Value 4 Investing for the Future 7 Impact in Action 9 Renewable Energy 10 Energy and Resource Efficiency 12 Water 15 Smart Cities 16 Sustainable Forestry 18 Diversity, Equity and Inclusion 20 ESG at Angeleno Group 22 Our Culture 23 Stakeholder Engagement 26 Portfolio Management 30 Vision for the Next Decade 32 Invitation to Dialogue 33 Appendices I Team and Advisors II III Values and Expectations for Portfolio Companies VI 2020 Impact Metrics and Engagement Outcomes 2020 ESG REPORT 0 ANGELENO GROUP LETTER FROM OUR LEADERSHIP …………………………………………………………………………………… This ESG Report – our tenth – is a special one for Angeleno Group. The report provides us with the opportunity to reflect on how our Responsible and Sustainable Investing Program has evolved over the past decade, and also to look forward to the future and, in particular, to the decade ahead. 2020 was a momentous year in numerous ways. Being faced with the COVID-19 pandemic showed us how interconnected we are, and how adaptive and resilient we can be. The social justice movement brought to the forefront systemic discrimination issues that businesses and society must address. The public and private markets exhibited remarkable growth in the clean energy sector. An inflection point was also reached among investors, corporations and governments that the need to transition to a low carbon economy cannot be delayed – and that a commitment to ESG principles will be integral to achieving long-term returns and creating shared value for all. -

Pharma Asset Insights POWERED by SCRIP and in VIVO

Pharma intelligence Pharma Asset Insights POWERED BY SCRIP AND IN VIVO Bringing science innovation and partnering news to the biopharmaceutical business community Pharma intelligence Innovation in the pharmaceutical industry has never been more exciting, and complicated. Disruptive technologies, such as artificial intelligence and digital health tools, and advanced therapeutic modalities including cell and gene therapies and antisense oligonucleotides demand that all health care stakeholders make efforts to move into the next generation of patient care and centricity. Funding for start-ups has reached an inflection point, with venture capital money flowing into companies at a rapid speed and at record-high amounts, particularly for those located in Europe. In 2013 only three life science venture capital rounds surpassed $100 million; by the first quarter of 2018, those financings have become more of the rule than the exception, as 10 venture rounds worth over $100 million were completed, led by a massive $500 million late-stage funding from Moderna Therapeutics. Many of these firms have progressed to the IPO stage, where markets have been very favorable over the past couple years. Indeed, 11 biopharma IPOs netted an aggregate $1 billion in Q1 2018, and included a $56 million offering from BioXcel Therapeutics, which is using artificial intelligence to identify the most promising neurological and immune-oncology drug candidates to advance. Overall, companies involved in mining and applying predictive analytics to big datasets have been well funded recently, including BenevolentAI, which closed on a $115 million financing, and Pear Therapeutics, a digital health company that has raised $50 million and signed on Novartis to market its reSET digital therapeutics product for substance abuse. -

3Rd FCF Life Science Venture Capital Report

FCF Life Science Research 3rd Life Science Venture Capital Report – Financing Trends in Europe and the US Fungi Penicillium Part of FCF Life Science Research Series Executive Summary FCF Overview Funding Development in 2018 Life Sciences: A closer Look C r o s s - border Investment Activity Investor Analysis Life Science Exits 2 Executive Summary The FCF Life Science Venture Capital FCF Life Science Venture Capital Report Recipients Report is a is a comprehensive, standardized analysis for biotechnology, The FCF Life Science Venture Capital Report targets the following standardized report pharmaceutical and medical technology companies, examining recipients: focusing on venture recent venture capital deal trends in the European life science ▪ Corporates / Executives ▪ Venture capital investors capital deal industry ▪ Institutional investors ▪ Family Offices / High- characteristics in the ▪ Private equity investors net-worth individuals biotechnology, ▪ Advisors Selection of Companies pharmaceutical and medical technology The selection of companies is based on the following criteria: Availability segments, and can be used as a quick ▪ Companies operating in the biotechnology, pharmaceutical, The FCF Life Science Venture Capital Report is available on FCF’s reference for medical technology, services or other life science related sectors website at “https://www.fcf.de/de/research/life-science-research“ investors, corporates ▪ Sole focus on transactions involving European life science and professionals companies Data ▪ The therapeutics sector is further divided into the following All input data is provided by Pitchbook, S&P Capital IQ or More advanced, indications: Oncology, Central Nervous System, Infectious GlobalData and is not independently verified by FCF. Ratio and detailed and / or Diseases, Immunology, Ophthalmology, Rare Diseases, multiple calculations are driven based on the input data available. -

2007 Annual Report

CONNECT 2007 ANNUAL REPORT Recycled 100% Supporting responsible use of forest resources www.fsc.org Cert no. SW-COC-002680 © 1996 Forest Stewardship Council Founding Chair’s Letter FOUNDING CHAIRMAN’S LETTER: CARL D. THOMA It seems like only yesterday that we celebrated the debut of the Before the IVCA, our city and state lacked the informal network Illinois Venture Capital Association at a gala party, distributing the that fuses venture capitalists, emerging enterprises, academics poster “Dawn of America” that the late Chicago artist Ed Paschke and government offi cials. These networks are essential to create made especially for IVCA as well as chocolate gold coins bearing work and wealth – work for many new employees in our state the IVCA logo. It was the start of a new century. We sought to stir and wealth for those innovators and investors that forge and some excitement into the state’s private equity and venture capital launch successful start-ups. industry and the entrepreneurial community and, in the process, foster a great deal more networking. The IVCA has become that nurturing network as well as an organization regarded in the state legislature and in the That was seven years ago – and what a difference those ensuing media for getting things done. Just glance at our calendar years have made. We have grown from an organization with 28 of events. members to 129 members. We have become an active – some might say activist – trade association, lobbying arm and meeting Through this initial report of the IVCA, I think you will quickly place. We have widened our net, too, embracing academic members recognize that our voice is the voice of our members – and this and service providers essential to our industry and association, united voice grows stronger and more powerful every year. -

2010 ANNUAL REPORT :: a DECADE of INFLUENCE Introduction

20 10 2010 ANNUAL REPORT :: A DECADE OF INFLUENCE INTRODUCTION IT BEGAN DURING THE FIRST INTERNET BOOM AS THE GERM OF AN IDEA BY A LEGISLATIVE AIDE1 TO AN ILLINOIS STATE LAWMAKER: Why not launch an organization to serve as the voice of private equity and venture capital in Illinois and Chicago, America’s crossroads? Championed by a private- equity legend in Chicago,2 the group originally focused on legislative issues critical to venture capital and private equity investing and on building its membership during an increasingly troubled tech economy. Now, on its 10th anniversary, the organization – the Illinois Venture Capital Association – prevails as the most influential advocate for Illinois’ venture and private equity investing. It delivers superbly on the three elements of its mission: Invest in Illinois; Advocate for venture capital and private equity; Serve its member- ship. In the process, it has become a determined activist for advancing Illinois as an Innovation Economy. Indeed, except for the National Venture Capital Association on the countrywide stage, the IVCA has forged the most distinctive and influential voice for venture capital and private equity investors of any state or regional organization. The IVCA’s executive director, its board members and others active in the association increasingly are sought after by legislators, entrepreneurs, business development officials and the media for their counsel on issues important to the industry. Today, the IVCA’s mission and activities are more high profile and intensified than at any time during the last decade because of venture and private equity investing’s huge and positive impact on the state’s economy. -

United States

UNITED STATES BIOPHARMACEUTICALS 2020 BIOPHARMACEUTICALS UNITED STATES UNITED STATES BIOPHARMACEUTICALS 2020 Research and Development - Contract Services - Drug Discovery Academic Research Regulations and Compliance - East Coast Hubs - Logistics and Distribution Amos i m 0 0 5 Fredericton Timmins Quebec i m 0 0 4 The East Coast Corridor: MAINE i m Bangor The Heart of 0 0 American Biopharma 3 Montreal Augusta Dear Reader, i Ottawa m 0 VERMONT CANADA 0 2 Montpelier NEW HAMPSHIRE Portland Kingston i The United States Biopharmaceutical industry is widely envied m 0 0 Concord around the world, and for good reason. From gene editing, to cell- 1 Welcomebased to therapies, the 2020 toedition profoundly of the new US Biopharmaceuticalways of manipulating Industry immune Report, a jointcells GBR-CPhI to target analysis. cancers, Thetoday’s United science States is being Biopharmaceutical translated into industryprac- is Toronto widelytical envied treatments around forthe patients world, and at breakneck for good reason.speed. FromBiopharma gene editing,com- to MICHIGAN Albany BOSTON cell-basedpanies therapies, have achieved to profoundly remarkable new progressways of manipulating in advancing immune early dis cells- to Rochester MASSACHUSETTS targetease cancers, detection today’s and science enabling is being targeted translated treatments into practical with limited treatments side for NEW YORK patientseffects. at breakneck These innovations speed. Biopharma have catalyzed companies significant have reductionsachieved remark in - Buffalo Providence -

Life Sciences Venture Equity Market Review: the Evolving Role of Crossover Investors

Life Sciences Venture Equity Market Review: The Evolving Role of Crossover Investors June 2021 Securities offered in the United States are offered through Torreya Capital LLC, Member FINRA/SIPC. In Europe such services are offered through Torreya Partners (Europe) LLP, which is authorized and regulated by the UK Financial Conduct Authority. The Market for Equity Privates in Life Sciences TORREYA | PRIVATE LIFE SCIENCES VENTURE FINANCING MARKET REVIEW – JUNE 2021 2 Total Private Venture Financing Volume: 2000-2021 H1 Given volumes in the first half of this year, there is little doubt that 2021 will shape up to be the most active year in history for private financing activity in the life sciences sector. Total Volume of Private Biopharma, Diagnostics and Tools 50000 Financing Rounds by Year Jan 2000 - June 2021 600 (deals over $25mm, excluding medical devices, worldwide) 45000 523 500 40000 35000 373 400 356 30000 334 25000 300 20000 224 226 Transaction Transaction Count 184 200 15000 145 138 121 122 111 10000 109 88 97 96 81 72 100 Aggregate Aggregate Dollar Volume of Private Financings ($mm) 55 5000 40 35 23 0 0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 H1 Transaction Count Dollar Volume ($mm) Source: Torreya analysis and records, CapitalIQ and Crunchbase TORREYA | PRIVATE LIFE SCIENCES VENTURE FINANCING MARKET REVIEW – JUNE 2021 3 Fresh Venture Capital Flowing into Life Science Sector We are on track to see record amount raised in life science venture capital in 2021. -

The View Beyond Venture Capital

BUILDING A BUSINESS The view beyond venture capital Dennis Ford & Barbara Nelsen Fundraising is an integral part of almost every young biotech’s business strategy, yet many entrepreneurs do not have a systematic approach for identifying and prioritizing potential investors—many of whom work outside of traditional venture capital. re you a researcher looking to start a Why and how did the funding landscape During the downturns, it quickly became Anew venture around a discovery made change? apparent that entrusting capital to third-party in your laboratory? Perhaps you have already The big changes in the life science investor alternative fund managers was no longer an raised some seed money from your friends landscape start with the venture capitalist effective strategy, and investors began to with- and family and are now seeking funds to sus- (VC). In the past, venture capital funds were draw capital. The main reason for the with- tain and expand your startup. In the past, the typically capitalized by large institutional drawal (especially from VCs in the early-stage next step on your road to commercialization investors that consisted of pensions, endow- life science space) was generally meager returns would doubtless have been to seek funding ments, foundations and large family offices across the asset class; despite the high risk and from angels and venture capital funds; today, with $100 million to $1 billion in capital long lockup periods that investors accepted in however, the environment for financing an under management. Traditionally, the major- return for a promise of premium performance, early-stage life science venture looks strik- ity of these institutions maintained a low-risk, VCs were often not returning any more capital ingly different from that familiar landscape low-return portfolio of stocks and bonds that than investors would have earned by making of past decades.