Innovent Biologics (1801

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Current and Future Natural Gas Demand in China and India

Global Gas/LNG Research Current and Future Natural Gas Demand in China and India By Miranda Wainberg Senior Energy Advisor Michelle Michot Foss, Ph.D. Chief Energy Economist and Program Manager Gürcan Gülen, Ph.D. Senior Energy Economist and Research Scientist Daniel Quijano Economist and Research Associate April 2017 April 2017, BEG/CEE China/India Gas Demand, Page 1 TABLE OF CONTENTS ESSENTIAL ACRONYMNS, UNITS AND CONVERSIONS ................................................................................................... 5 ACKNOWLEDGMENTS .................................................................................................................................................... 6 PREFACE ......................................................................................................................................................................... 7 INTRODUCTION ............................................................................................................................................................. 8 MACROECONOMIC CONTEXT FOR NATURAL GAS IN CHINA AND INDIA ...................................................................... 9 Composition of GDP and Employment Structure ...................................................................................................... 9 GDP Growth and Industrial Structures in China and India ...................................................................................... 11 Industrial overcapacity and debt in China ......................................................................................................... -

Occupational Characteristics and Management Measures of Sporadic

Occupational characteristics and management measures of sporadic COVID-19 outbreaks from June 2020 to January 2021 in China: the importance of tracking down “patient zero” Maohui Feng 1,a, Qiong Ling 2,a, Jun Xiong 3, Anne Manyande 4, Weiguo Xu 5, Boqi Xiang 6,* 1 Department of Gastrointestinal Surgery, Wuhan Peritoneal Cancer Clinical Medical Research Center, Zhongnan Hospital of Wuhan University, Hubei Key Laboratory of Tumor Biological Behaviors and Hubei Cancer Clinical Study Center, Wuhan 430071, Hubei, PR China; 2 Department of Anesthesiology, The Second Affiliated Hospital of Guangzhou University of Chinese Medicine, Guangzhou 510120, Guangdong, PR China; 3 Hepatobiliary Surgery Center, Union Hospital of Tongji Medical College, Huazhong University of Science and Technology, Wuhan, 430022, PR China; 4 School of Human and Social Sciences, University of West London, London, United Kingdom; 5 Department of Orthopedics, Tongji Hospital of Tongji Medical College, Huazhong University of Science and Technology, Wuhan 430030, PR China; 6 School of Public Health, University of Rutgers, New Brunswick, NJ 08854, USA. a These authors have contributed equally to this work. *Correspondence: Boqi Xiang, E-mail: [email protected] Abstract There are occupational disparities in the risk of contracting COVID-19. Occupational characteristics and work addresses play key roles in tracking down “patient zero”. The present descriptive analysis for occupational characteristics and management measures of sporadic COVID-19 outbreaks from June to December 2020 in China offers important new information to the international community at this stage of the pandemic. These data suggest that Chinese measures including tracking down “patient zero”, launching mass COVID-19 testing in the SARS-CoV-2-positive areas, designating a new high or medium-risk area, locking down the corresponding community or neighborhood in response to new COVID-19 cases and basing individual methods of protection on science, are effective in reducing transmission of the highly contagious SARS-CoV-2 across China. -

LAG-3: from Molecular Functions to Clinical Applications

Open access Review J Immunother Cancer: first published as 10.1136/jitc-2020-001014 on 13 September 2020. Downloaded from LAG-3: from molecular functions to clinical applications Takumi Maruhashi , Daisuke Sugiura , Il- mi Okazaki , Taku Okazaki To cite: Maruhashi T, Sugiura D, ABSTRACT (PD-1) and cytotoxic T lymphocyte antigen Okazaki I, et al. LAG-3: from To prevent the destruction of tissues owing to excessive 4 (CTLA-4) significantly improved the molecular functions to clinical and/or inappropriate immune responses, immune outcomes of patients with diverse cancer applications. Journal for cells are under strict check by various regulatory ImmunoTherapy of Cancer types, revolutionizing cancer treatment. The mechanisms at multiple points. Inhibitory coreceptors, 2020;8:e001014. doi:10.1136/ success of these therapies verified that inhib- including programmed cell death 1 (PD-1) and cytotoxic jitc-2020-001014 itory coreceptors serve as critical checkpoints T lymphocyte antigen 4 (CTLA-4), serve as critical checkpoints in restricting immune responses against for immune cells to not attack the tumor Accepted 29 July 2020 self- tissues and tumor cells. Immune checkpoint inhibitors cells as well as self-tissues. However, response that block PD-1 and CTLA-4 pathways significantly rates are typically lower and immune-related improved the outcomes of patients with diverse cancer adverse events (irAEs) are also observed in types and have revolutionized cancer treatment. However, patients administered with immune check- response rates to such therapies are rather limited, and point inhibitors. This is indicative of the immune-rela ted adverse events are also observed in a continued need to decipher the complex substantial patient population, leading to the urgent need biology of inhibitory coreceptors to increase for novel therapeutics with higher efficacy and lower response rates and prevent such unwanted toxicity. -

Immutep Limited (ASX: IMM; NASDAQ: IMMP) (“Immutep” Or “The Company”) Is Pleased to Announce the Grant of Canadian Patent No

ASX/Media Release (Code: ASX: IMM; NASDAQ: IMMP) 7 August 2018 IMMUTEP SECURES CANADIAN PATENT GRANT FOR IMP731 ANTIBODY SYDNEY, AUSTRALIA - Immutep Limited (ASX: IMM; NASDAQ: IMMP) (“Immutep” or “the Company”) is pleased to announce the grant of Canadian patent no. 2,685,584 entitled “Cytotoxic anti-LAG-3 monoclonal antibody and its use in the treatment or prevention of organ transplant rejection and autoimmune disease.” The patent is directed to Immutep’s IMP731 antibody that was originally developed by Immutep S.A.S., Immutep’s French subsidiary. The granted claims provide broad protection for the antibody and use of the antibody for treating or preventing organ transplant rejection or treating a T-cell mediated autoimmune disease. The patent has an expiry date of 30 April 2028, and joins corresponding patents from the same family previously granted in the United States, Europe and Japan, as announced to the market. Rights for the development of the IMP731 antibody were granted to GSK in December 2010. GSK has developed a proprietary humanized antibody derived from IMP731, known as GSK2831781. About IMP731 and GSK2831781 IMP731 and GSK2831781 are designed to specifically deplete potentially pathogenic, recently activated, LAG-3 expressing T cells that are enriched at the disease site in T-cell driven immuno‐inflammatory disorders. Depletion of these LAG-3 expressing T cells should spare other T-cells which may be necessary for disease control. About Immutep Immutep is a globally active biotechnology company that is a leader in the development of immunotherapeutic products for the treatment of cancer and autoimmune disease. Immutep is dedicated to leveraging its technology and expertise to bring innovative treatment options to market for patients and to maximise value to shareholders. -

Asx: Prr, Nasdaq: Pbmd

ASX: PRR, NASDAQ: PBMD August 2017 CORPORATE PRESENTATION Notice: Forward Looking Statements The purpose of the presentation is to provide an update of the business of Prima BioMed Ltd ACN 009 237 889 (ASX:PRR; NASDAQ:PBMD). These slides have been prepared as a presentation aid only and the information they contain may require further explanation and/or clarification. Accordingly, these slides and the information they contain should be read in conjunction with past and future announcements made by Prima BioMed and should not be relied upon as an independent source of information. Please refer to the Company's website and/or the Company’s filings to the ASX and SEC for further information. The views expressed in this presentation contain information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking statements in this presentation have been prepared on the basis of a number of assumptions which may prove incorrect and the current intentions, plans, expectations and beliefs about future events are subject to risks, uncertainties and other factors, many of which are outside Prima BioMed’s control. Important factors that could cause actual results to differ materially from assumptions or expectations expressed or implied in this presentation include known and unknown risks. Because actual results could differ materially to assumptions made and Prima BioMed’s current intentions, plans, expectations and beliefs about the future, you are urged to view all forward looking statements contained in this presentation with caution. -

World Energy Investment 2021 INTERNATIONAL ENERGY AGENCY

World Energy Investment 2021 INTERNATIONAL ENERGY AGENCY The IEA examines the IEA member IEA association full spectrum countries: countries: of energy issues including oil, gas and Australia Brazil coal supply and Austria China demand, renewable Belgium India energy technologies, electricity markets, Canada Indonesia energy efficiency, Czech Republic Morocco access to energy, Denmark Singapore demand side Estonia South Africa management and Finland Thailand much more. Through France its work, the IEA Germany advocates policies that Greece will enhance the Hungary reliability, affordability Ireland and sustainability of Italy energy in its 30 member countries, Japan 8 association countries Korea and beyond. Luxembourg Mexico Netherlands New Zealand Norway Poland Portugal Please note that this Slovak Republic publication is subject to Spain specific restrictions that limit its use and distribution. The Sweden terms and conditions are Switzerland available online at Turkey www.iea.org/t&c/ United Kingdom United States This publication and any map included herein are The European without prejudice to the Commission also status of or sovereignty over participates in the any territory, to the delimitation of international work of the IEA frontiers and boundaries and to the name of any territory, city or area. Source: IEA. All rights reserved. International Energy Agency Website: www.iea.org World Energy Investment 2021 Abstract Abstract This year’s edition of the World Energy Investment report presents the latest data and analysis of how energy investment flows are recovering from the shock of the Covid-19 pandemic, including full-year estimates of the outlook for 2021. It examines how investors are assessing risks and opportunities across all areas of fuel and electricity supply, efficiency and research and development, against a backdrop of a recovery in global energy demand as well as strengthened pledges from governments and the private sector to address climate change. -

Global Offering

蘇州貝康醫療股份有限公司 SUZHOU BASECARE MEDICAL CORPORATION LIMITED (A joint stock company incorporated in the People's Republic of China with limited liability) Stock Code: 2170 GLOBAL OFFERING Sole Sponsor, Joint Global Coordinator, Joint Bookrunner and Joint Lead Manager Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers Joint Bookrunners and Joint Lead Managers Joint Lead Manager IMPORTANT IMPORTANT: If you are in any doubt about any of the contents of this prospectus, you should seek independent professional advice. Suzhou Basecare Medical Corporation Limited 蘇州貝康醫療股份有限公司 (A joint stock company incorporated in the People’s Republic of China with limited liability) GLOBAL OFFERING Number of Offer Shares under : 66,667,000 H Shares (subject to the the Global Offering Over-allotment Option) Number of Hong Kong Offer Shares : 6,667,000 H Shares (subject to adjustment) Number of International Offer Shares : 60,000,000 H Shares (subject to adjustment and the Over-allotment Option) Maximum Offer Price : HK$27.36 per H Share, plus brokerage of 1.0%, SFC transaction levy of 0.0027% and Stock Exchange trading fee of 0.005% (payable in full on application in Hong Kong Dollars and subject to refund) Nominal Value : RMB1.00 per H Share Stock Code : 2170 Sole Sponsor, Joint Global Coordinator, Joint Bookrunner and Joint Lead Manager Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers Joint Bookrunners and Joint Lead Managers Joint Lead Manager Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness, and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. -

AHEC Market Report

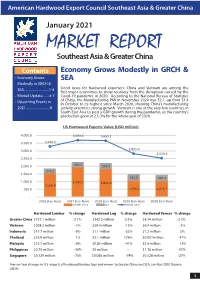

American Hardwood Export Council Southeast Asia & Greater China January 2021 MARKET REPORT Southeast Asia & Greater China Contents Economy Grows Modestly in GRCH & • Economy Grows SEA Modestly in GRCH & SEA..............................1-4 Good news for hardwood exporters: China and Vietnam are among the first major economies to show recovery from the disruption caused by the • Market Update........4-7 Covid-19 pandemic in 2020. According to the National Bureau of Statistics • Upcoming Events in of China, the Manufacturing PMI in November 2020 was 52.1, up from 51.4 in October to its highest since March 2020, showing China’s manufacturing 2021.............................8 activity extend its strong growth. Vietnam is one of the very few countries in South East Asia to post a GDP growth during the pandemic, as the country’s production grew at 2.5-3% for the whole year of 2020. US Hardwood Exports Value (USD million) 4,000.0 3,693.6 3,665.1 3,500.0 3,290.3 2,825.0 3,000.0 2,528.6 2,500.0 2,000.0 304.5 341.4 272.2 1,500.0 361.6 342.3 1,000.0 1,949.2 1,841.6 1,556.8 500.0 1,096.4 1,076.7 - 2016 (Jan-Nov) 2017 (Jan-Nov) 2018 (Jan-Nov) 2019 (Jan-Nov) 2020 (Jan-Nov) Greater China SEA World Total Hardwood Lumber % change Hardwood Log % change Hardwood Veneer % change Greater China $727.1 million -2.7% $342.2 million 0.3% $4.74 million -2.7% Vietnam $208.3 million -1% $59.4 million -15% $6.4 million -3% Indonesia $17.7 million -9% $1.1 million -53% $7.2 million 5% Thailand $15.9 million 1% $2.1 million 179% $0.057million 47% Malaysia $13.7 million -6% $0.83 million -41% $5.6 million 12% Philippines $0.75 million -36% $0 million -- $1.16 million -33% Singapore $0.129 million -75% $0.065 million -74% $0.328 million -27% Year-on-Year changes in U.S. -

Securities and Exchange Commission Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the fiscal year ended December 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. Commission File No. 001-35210 HC2 HOLDINGS, INC. (Exact name of registrant as specified in its charter) Delaware 54-1708481 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 450 Park Avenue, 29th Floor, New York, NY 10022 (Address of principal executive offices) (Zip Code) (212) 235-2690 (Registrant’s telephone number, including area code) _____________________________________________________________________________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol Name of each exchange on which registered Common Stock, par value $0.001 per share HCHC New York Stock Exchange Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No x Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Demand for Storage and Import of Natural Gas in China Until 2060: Simulation with a Dynamic Model

sustainability Article Demand for Storage and Import of Natural Gas in China until 2060: Simulation with a Dynamic Model Zhihua Chen * , Hui Wang, Tongxia Li and Ieongcheng Si The Belt and Road School, Beijing Normal University, Beijing 100875, China; [email protected] (H.W.); [email protected] (T.L.); [email protected] (I.S.) * Correspondence: [email protected] Abstract: China has been reforming its domestic natural gas market in recent years, while construc- tion of storage systems is lagging behind. As natural gas accounts for an increasing proportion due to the goal of carbon neutrality, large-scale gas storage appears to be necessary to satisfy the needs for gas peak shaving and national strategic security. Additionally, the domestic gas production in China cannot meet consumption demands, and imports will play a significant role on the supply side. This paper developed a system dynamics (SD) model and applied it to simulate gas market behaviors and estimated China’s gas storage capabilities and import demands over the next 40 years. To achieve carbon neutrality, it is necessary for China to make great progress in its energy intensity and improve its energy structure, which have a great impact on natural gas consumption. Thus, alternative scenarios were defined to discuss the changes in the gas market with different gas storage goals and environmental constraints. The results show that under low and medium carbon price scenarios, natural gas demand will continue to grow in the next 40 years, but it will be difficult to achieve the goal of carbon neutrality. -

GLAXOSMITHKLINE INNOVATIVE PIPELINE Tuesday, 3 November 2015

GLAXOSMITHKLINE INNOVATIVE PIPELINE Tuesday, 3 November 2015 GLAXOSMITHKLINE INNOVATIVE PIPELINE Tuesday, 3 November 2015 Sir Andrew Witty (CEO): Welcome everybody to this R&D Investor Update from GSK here in New York. I would like to also say welcome to everybody who is watching this on the live webcast investors media around the world. I would particularly like to say a warm welcome to all of the GSK employees, particularly those in R&D and especially those who are working on the projects, which we are going to describe to you during the rest of the morning. I hope they take the great chance just to sit back and reflect on the work that they have done so diligently over the last five, 10, 15 years to get the company to where we are on this portfolio. What we plan to do during the morning or so is to take you through a reasonably large number of projects in the six focused areas of research at GSK. You will hear really from just two presenters after me, Moncef and Patrick, but, as you may have noticed, we do have a number of GSK personnel in the front row or two here. These are all of the Discovery and Development leaders of all the various programmes which you are going to hear about today. While they are not going to present to you, they are certainly here for you to interact with, certainly in the coffee session, of course, but also if there are questions which Moncef or Patrick feel are better answered by the various individual leaders, you will be hearing from them in that context as well. -

The Flip-Side of Immunotherapy

REPRINT FROM AUGUST 10, 2017 THINKSTOCK STRATEGY THE FLIP-SIDE OF IMMUNOTHERAPY By Lauren Martz, Senior Writer In the smaller print of last week’s deal between IFM Therapeutics NLRP3 is expressed primarily in macrophages, dendritic cells Inc. and Bristol-Myers Squibb Co. was the latest example of a and other immune cells. Agonizing the target activates the growing trend of companies aiming to draw extra value out of a inflammasome, triggering T cells to secrete cytokines and cancer target by using its opposite activity to treat autoimmunity. ramping up the immune response to kill tumors. The deal was noted mostly for its dollar value; BMS acquired However, in autoimmune diseases where the goal is to dampen two preclinical programs from IFM that stimulate the innate excess activity of immune cells, antagonizing NLRP3 prevents T immune system targets NLRP3 and STING for cancer, for cell activation and inflammation. an upfront payment of $300 million and up to $1 billion in “Activating the innate immune system produces the first milestones per program. inflammatory spark that makes the whole system hot. By But the biotech also spun out IFM Therapeutics LLC to develop blocking NLRP3, we’re preventing the spark rather than putting the remaining assets, which include a preclinical antagonist of out the fire,” said Glick. NLRP3 for inflammatory disease and fibrosis. That could lead Such duality is found among scores of proteins, and positions the company not only into autoimmunity, but to non-alcoholic the autoimmune field to benefit from the explosion of interest in steatohepatitis (NASH) as well. immuno-oncology, which has been busy uncovering new targets NLR proteins detect cellular threats by recognizing pathogen- and validating them as immune mediators.