Sigma No 6/2019 1 Key Takeaways

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Current and Future Natural Gas Demand in China and India

Global Gas/LNG Research Current and Future Natural Gas Demand in China and India By Miranda Wainberg Senior Energy Advisor Michelle Michot Foss, Ph.D. Chief Energy Economist and Program Manager Gürcan Gülen, Ph.D. Senior Energy Economist and Research Scientist Daniel Quijano Economist and Research Associate April 2017 April 2017, BEG/CEE China/India Gas Demand, Page 1 TABLE OF CONTENTS ESSENTIAL ACRONYMNS, UNITS AND CONVERSIONS ................................................................................................... 5 ACKNOWLEDGMENTS .................................................................................................................................................... 6 PREFACE ......................................................................................................................................................................... 7 INTRODUCTION ............................................................................................................................................................. 8 MACROECONOMIC CONTEXT FOR NATURAL GAS IN CHINA AND INDIA ...................................................................... 9 Composition of GDP and Employment Structure ...................................................................................................... 9 GDP Growth and Industrial Structures in China and India ...................................................................................... 11 Industrial overcapacity and debt in China ......................................................................................................... -

Occupational Characteristics and Management Measures of Sporadic

Occupational characteristics and management measures of sporadic COVID-19 outbreaks from June 2020 to January 2021 in China: the importance of tracking down “patient zero” Maohui Feng 1,a, Qiong Ling 2,a, Jun Xiong 3, Anne Manyande 4, Weiguo Xu 5, Boqi Xiang 6,* 1 Department of Gastrointestinal Surgery, Wuhan Peritoneal Cancer Clinical Medical Research Center, Zhongnan Hospital of Wuhan University, Hubei Key Laboratory of Tumor Biological Behaviors and Hubei Cancer Clinical Study Center, Wuhan 430071, Hubei, PR China; 2 Department of Anesthesiology, The Second Affiliated Hospital of Guangzhou University of Chinese Medicine, Guangzhou 510120, Guangdong, PR China; 3 Hepatobiliary Surgery Center, Union Hospital of Tongji Medical College, Huazhong University of Science and Technology, Wuhan, 430022, PR China; 4 School of Human and Social Sciences, University of West London, London, United Kingdom; 5 Department of Orthopedics, Tongji Hospital of Tongji Medical College, Huazhong University of Science and Technology, Wuhan 430030, PR China; 6 School of Public Health, University of Rutgers, New Brunswick, NJ 08854, USA. a These authors have contributed equally to this work. *Correspondence: Boqi Xiang, E-mail: [email protected] Abstract There are occupational disparities in the risk of contracting COVID-19. Occupational characteristics and work addresses play key roles in tracking down “patient zero”. The present descriptive analysis for occupational characteristics and management measures of sporadic COVID-19 outbreaks from June to December 2020 in China offers important new information to the international community at this stage of the pandemic. These data suggest that Chinese measures including tracking down “patient zero”, launching mass COVID-19 testing in the SARS-CoV-2-positive areas, designating a new high or medium-risk area, locking down the corresponding community or neighborhood in response to new COVID-19 cases and basing individual methods of protection on science, are effective in reducing transmission of the highly contagious SARS-CoV-2 across China. -

Innovent Biologics (1801

22 Jul 2021 CMB International Securities | Equity Research | Company Initiation Innovent Biologics (1801 HK) BUY (Initiation) Growing into a global biopharma company Target Price HK$120.91 Up/Downside +43.00% Current Price HK$84.55 Rich innovative drug pipelines. Innovent is a leading integrated biopharma company with comprehensive innovative pipelines including monoclonal antibodies (mAbs), bispecific antibodies (bsAbs), small molecules and CAR- China Healthcare Sector T therapies, covering oncology, autoimmune and metabolic diseases. Besides five marketed products (sintilimab, three biosimilars and pemigatinib), Jill Wu, CFA Innovent has six innovative drugs in pivotal clinical stage, including IBI306 (852) 3900 0842 (PCSK9 antibody), IBI310 (CTLA-4 antibody), IBI376 (PI3Kδ inhibitor), IBI326 [email protected] (BCMA-CART), taletrectinib (ROS1/NTRK inhibitor) and HQP1351 (olverembatinib, third-generation BCR-ABL TKI). In addition, Innovent has Sam Hu, PhD established a comprehensive innovative portfolio covering next-generation (852) 3900 0882 immuno-oncology (I/O) targets, including CD47/SIRPα, TIGT, LAG3, 4-1BB, [email protected] etc. It’s worth noting that Innovent is an early mover in CD47-SIRPα pathway with three assets under development, including clinical-stage IBI188 (a CD47 Jonathan Zhao antibody) and IBI322 (a PD-L1/CD47 bispecific antibody), and preclinical (852) 6359 1614 stage IBI397 (AL008, a SIRPα antibody). [email protected] Tyvyt being an early mover in large indications. After the approval for r/r- cHL in Dec 2018, Tyvyt has been approved by the NMPA for 1L ns-NSCLC, Mkt. Cap. (HK$ mn) 123,312 1L s-NSCLC and 1L HCC in 2021. These three large indications may be Avg. -

The Strait of Hormuz

PragueMUN2020 Security Council Prague, February 2020 Prague Model United Nations Conference Model United Nations Prague z.s. Jaurisova 515/4 140 00 Prague 4 The Czech Republic Web: www.praguemun.cz Authors: Mohammed Babiker and Lennert Houbrechts Graphic Design: Anna Grybova PragueMUN2020 Security Council Contents Welcome Letter 1 Introduction to the Security Council 2 Topic A: Amidst rising tensions - Strait of Hormuz 3 Introduction to the topic 3 Background 3 Key actors 5 Involvement of the UNSC and the international community 6 The Strait of Hormuz 7 Global importance: economics and geopolitics 7 Status in UNCLOS 7 Questions to consider 8 Further reading 8 Bibliography 9 Topic B: Reforming the Security Council 11 Introduction to the topic 11 Historical background 11 Background and creation 11 Cold War 12 Post-Cold War 12 1. Question of the veto 13 2. Regional Representation 14 3. Increasing Size 15 Permanent Members 15 Annan Plan 16 4. Relations with the General Assembly 16 Questions to Consider 17 Further reading 17 Bibliography 18 PragueMUN2020 Security Council Welcome Letter Welcome to the United Nations Security Council (UNSC) at Prague Model United Nations 2020! My name is Mohammed Babiker, and I have the honor of being one of your chairs for this committee. I was born and grew up in the United Kingdom, moved to Sudan and then Saudi Arabia where I have recently graduated with bachelor diploma in Software Engineering. This will be my second time chairing. Despite appearing unrelated to my major, I believe MUN is a great experience for students of all academic backgrounds. -

Japan's Strategies for Advancing Diplomacy in the United

Japan’s Strategies for Advancing Diplomacy in the United Nations: Implications for U.S.-Japan Cooperation By Miki Honda 1 Introduction 1956 was an historic year for Japan as it was approved as the 80th member of the United Nations (UN), one of the postwar multilateral institutions led by the United States. Becoming a UN member signified Japan’s genuine return to the international community. Two years after gaining membership, Japan became a non-permanent member of the UN Security Council for the first time, and since then Japan has served as a non-permanent member on 11 occasions, the most of any member state. Japan has made efforts as a stakeholder to achieve the UN mission—maintaining international peace and security, protecting human rights, delivering humanitarian aid, promoting sustainable development, and upholding international law. In addition to Japan’s alliance with the United States, UN policy has been a major component of Japanese diplomacy in the postwar period. The UN enables Japan to contribute to the international community despite constitutional limitations in the area of security. Nonetheless, Japan has successfully expanded its security role in the international community within the framework of the UN by supporting international norms, addressing non-traditional security (NTS) issues, and strengthening relations with like-minded countries. But there have always been tensions within the UN concerning agenda-setting and achieving consensus on promoting collective security and maintaining the postwar liberal order. Since joining the UN, Japan has made great efforts to support those aims as a pacifist nation and strengthen the U.S.-Japan alliance to enhance its own security and stability in East Asia. -

G20: Shaping an Interconnected World

G20 GERMANY 2017 HAMBURG The Indo-German mag with swag ! ISSUE 2 | 2017 G20: SHAPING AN INTERCONNECTED WORLD www.whatsupgermany.de WHAT’S UP, AMBASSADOR? DR MARTIN NEY We live in an interconnected world that is responsibility to address these issues, undergoing enormous changes—changes because their concerted efforts can bring that touch the lives of virtually everyone. about change. They work together in the These changes can bring us closer G20—the Group of Twenty—a platform for together or create new rifts. Our societies dialogue and close collaboration. are transformed by new networks and an increasing exchange of ideas which, thanks Germany currently holds the presidency of to modern technologies, flow across borders. the G20. Having already organised a series People are also on the move in real terms, of ministerial meetings, we will host the looking for opportunities around the world or leaders’ summit on 7–8 July in Hamburg. Our fleeing from conflicts. presidency centres on the triad of stability, responsibility and sustainability, which we New opportunities have not only driven deem essential to secure the prosperity innovation and economic growth, but have and security of everyone. helped to lift millions of people out of dire poverty. At the same time, we have Together with India and other partners had to overcome unprecedented we strive to increase the resilience of our challenges which emanated economies and financial institutions. We from the very institutions that aim to translate the commitments to a underpin our global economic sustainable development path and to the system. We are facing protection of our climate into concrete even more challenges measures. -

World Energy Investment 2021 INTERNATIONAL ENERGY AGENCY

World Energy Investment 2021 INTERNATIONAL ENERGY AGENCY The IEA examines the IEA member IEA association full spectrum countries: countries: of energy issues including oil, gas and Australia Brazil coal supply and Austria China demand, renewable Belgium India energy technologies, electricity markets, Canada Indonesia energy efficiency, Czech Republic Morocco access to energy, Denmark Singapore demand side Estonia South Africa management and Finland Thailand much more. Through France its work, the IEA Germany advocates policies that Greece will enhance the Hungary reliability, affordability Ireland and sustainability of Italy energy in its 30 member countries, Japan 8 association countries Korea and beyond. Luxembourg Mexico Netherlands New Zealand Norway Poland Portugal Please note that this Slovak Republic publication is subject to Spain specific restrictions that limit its use and distribution. The Sweden terms and conditions are Switzerland available online at Turkey www.iea.org/t&c/ United Kingdom United States This publication and any map included herein are The European without prejudice to the Commission also status of or sovereignty over participates in the any territory, to the delimitation of international work of the IEA frontiers and boundaries and to the name of any territory, city or area. Source: IEA. All rights reserved. International Energy Agency Website: www.iea.org World Energy Investment 2021 Abstract Abstract This year’s edition of the World Energy Investment report presents the latest data and analysis of how energy investment flows are recovering from the shock of the Covid-19 pandemic, including full-year estimates of the outlook for 2021. It examines how investors are assessing risks and opportunities across all areas of fuel and electricity supply, efficiency and research and development, against a backdrop of a recovery in global energy demand as well as strengthened pledges from governments and the private sector to address climate change. -

Global Offering

蘇州貝康醫療股份有限公司 SUZHOU BASECARE MEDICAL CORPORATION LIMITED (A joint stock company incorporated in the People's Republic of China with limited liability) Stock Code: 2170 GLOBAL OFFERING Sole Sponsor, Joint Global Coordinator, Joint Bookrunner and Joint Lead Manager Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers Joint Bookrunners and Joint Lead Managers Joint Lead Manager IMPORTANT IMPORTANT: If you are in any doubt about any of the contents of this prospectus, you should seek independent professional advice. Suzhou Basecare Medical Corporation Limited 蘇州貝康醫療股份有限公司 (A joint stock company incorporated in the People’s Republic of China with limited liability) GLOBAL OFFERING Number of Offer Shares under : 66,667,000 H Shares (subject to the the Global Offering Over-allotment Option) Number of Hong Kong Offer Shares : 6,667,000 H Shares (subject to adjustment) Number of International Offer Shares : 60,000,000 H Shares (subject to adjustment and the Over-allotment Option) Maximum Offer Price : HK$27.36 per H Share, plus brokerage of 1.0%, SFC transaction levy of 0.0027% and Stock Exchange trading fee of 0.005% (payable in full on application in Hong Kong Dollars and subject to refund) Nominal Value : RMB1.00 per H Share Stock Code : 2170 Sole Sponsor, Joint Global Coordinator, Joint Bookrunner and Joint Lead Manager Joint Global Coordinators, Joint Bookrunners and Joint Lead Managers Joint Bookrunners and Joint Lead Managers Joint Lead Manager Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness, and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. -

AHEC Market Report

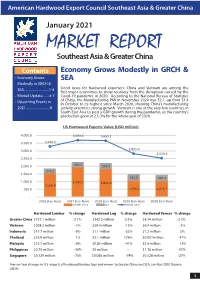

American Hardwood Export Council Southeast Asia & Greater China January 2021 MARKET REPORT Southeast Asia & Greater China Contents Economy Grows Modestly in GRCH & • Economy Grows SEA Modestly in GRCH & SEA..............................1-4 Good news for hardwood exporters: China and Vietnam are among the first major economies to show recovery from the disruption caused by the • Market Update........4-7 Covid-19 pandemic in 2020. According to the National Bureau of Statistics • Upcoming Events in of China, the Manufacturing PMI in November 2020 was 52.1, up from 51.4 in October to its highest since March 2020, showing China’s manufacturing 2021.............................8 activity extend its strong growth. Vietnam is one of the very few countries in South East Asia to post a GDP growth during the pandemic, as the country’s production grew at 2.5-3% for the whole year of 2020. US Hardwood Exports Value (USD million) 4,000.0 3,693.6 3,665.1 3,500.0 3,290.3 2,825.0 3,000.0 2,528.6 2,500.0 2,000.0 304.5 341.4 272.2 1,500.0 361.6 342.3 1,000.0 1,949.2 1,841.6 1,556.8 500.0 1,096.4 1,076.7 - 2016 (Jan-Nov) 2017 (Jan-Nov) 2018 (Jan-Nov) 2019 (Jan-Nov) 2020 (Jan-Nov) Greater China SEA World Total Hardwood Lumber % change Hardwood Log % change Hardwood Veneer % change Greater China $727.1 million -2.7% $342.2 million 0.3% $4.74 million -2.7% Vietnam $208.3 million -1% $59.4 million -15% $6.4 million -3% Indonesia $17.7 million -9% $1.1 million -53% $7.2 million 5% Thailand $15.9 million 1% $2.1 million 179% $0.057million 47% Malaysia $13.7 million -6% $0.83 million -41% $5.6 million 12% Philippines $0.75 million -36% $0 million -- $1.16 million -33% Singapore $0.129 million -75% $0.065 million -74% $0.328 million -27% Year-on-Year changes in U.S. -

Securities and Exchange Commission Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the fiscal year ended December 31, 2020 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. Commission File No. 001-35210 HC2 HOLDINGS, INC. (Exact name of registrant as specified in its charter) Delaware 54-1708481 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 450 Park Avenue, 29th Floor, New York, NY 10022 (Address of principal executive offices) (Zip Code) (212) 235-2690 (Registrant’s telephone number, including area code) _____________________________________________________________________________________________________________________ Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol Name of each exchange on which registered Common Stock, par value $0.001 per share HCHC New York Stock Exchange Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No x Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Demand for Storage and Import of Natural Gas in China Until 2060: Simulation with a Dynamic Model

sustainability Article Demand for Storage and Import of Natural Gas in China until 2060: Simulation with a Dynamic Model Zhihua Chen * , Hui Wang, Tongxia Li and Ieongcheng Si The Belt and Road School, Beijing Normal University, Beijing 100875, China; [email protected] (H.W.); [email protected] (T.L.); [email protected] (I.S.) * Correspondence: [email protected] Abstract: China has been reforming its domestic natural gas market in recent years, while construc- tion of storage systems is lagging behind. As natural gas accounts for an increasing proportion due to the goal of carbon neutrality, large-scale gas storage appears to be necessary to satisfy the needs for gas peak shaving and national strategic security. Additionally, the domestic gas production in China cannot meet consumption demands, and imports will play a significant role on the supply side. This paper developed a system dynamics (SD) model and applied it to simulate gas market behaviors and estimated China’s gas storage capabilities and import demands over the next 40 years. To achieve carbon neutrality, it is necessary for China to make great progress in its energy intensity and improve its energy structure, which have a great impact on natural gas consumption. Thus, alternative scenarios were defined to discuss the changes in the gas market with different gas storage goals and environmental constraints. The results show that under low and medium carbon price scenarios, natural gas demand will continue to grow in the next 40 years, but it will be difficult to achieve the goal of carbon neutrality. -

Reforming Multilateralism in Post-Covid Times

ited for A NEW MULTILATERALISM EDITED BY MARIO TELÒ REFORMING MULTILATERALISM IN POST-COVID TIMES FOR A MORE REGIONALISED, BINDING AND LEGITIMATE UNITED NATIONS EDITED BY Mario Telò REFORMING MULTILATERALISM IN POST-COVID TIMES IN POST-COVID REFORMING MULTILATERALISM PUBLISHED IN DECEMBER 2020 BY Foundation for European Progressive Studies Avenue des Arts 46 B-1000 Brussels, Belgium +32 2 234 69 00 [email protected] www.feps-europe.eu @FEPS_Europe EDITOR AND PROJECT SCIENTIFIC DIRECTOR Mario Telò LEADER OF THE PROJECT Maria João Rodrigues, President, Foundation for European Progressive Studies FEPS COORDINATORS OF THE PROJECT Hedwig Giusto, Susanne Pfeil IAI COORDINATOR OF THE PROJECT Ettore Greco COPYRIGHT © 2020 Foundation for European Progressive Studies (FEPS) PROOFREADING AND COPY EDITING Nicky Robinson GRAPHIC DESIGN Triptyque.be COVER PHOTO Shutterstock PRINTED BY Oficyna Wydawnicza ASPRA-JR Published with the financial support of the European Parliament. The views expressed in this report are solely those of the authors and do not necessarily reflect the views of the European Parliament. ISBN 978-2-930769-46-2 PROJECT PARTNERS FRIEDRICH-EBERT-STIFTUNG NEW YORK OFFICE 747 Third Avenue, Suite 34D, New York, NY 10017, United States +1 (212) 687-0208 [email protected] https://www.feps-europe.eu @fesnewyork FONDATION JEAN-JAURÈS 12 Cité Malesherbes, 75009 Paris, France +33 (0)1 40 23 24 00 https://jean-jaures.org [email protected] @j_jaures CENTRO STUDI DI POLITICA INTERNAZIONALE (CeSPI) Piazza Venezia 11, 00187 Roma, Italy +39