Downtown Los Angeles Demographic Study 2011

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Jacket Required NEW YORK — After Fall’S Broody Palette, Giorgio Armani Lightened up Collezioni’S Line for Resort

The Inside: Retail’s Top WomenPg. 12 TOMMY’S DONE DEAL/3 BUSH RULES ON CHINA/3 WWD WWDWomen’s Wear Daily • The Retailers’THURSDAY Daily Newspaper • May 11, 2006 • $2.00 List Sportswear Jacket Required NEW YORK — After fall’s broody palette, Giorgio Armani lightened up Collezioni’s line for resort. The designer played up jackets in every which way, with an emphasis on shorter shapes and clean lines. Here, for example, Armani Collezioni’s cotton and elastin jacket and cotton and elastin denim pants. For more, see page 8. Beginning a New Era: Federated Posts Loss On May Merger Costs By Vicki M. Young NEW YORK — Federated Department Stores Inc.’s bottom line for the first quarter of its “transition year” was heavily weighed down by the costs of merging with May Department Stores. The retailer on Wednesday posted a $52 million first-quarter loss, but managed to beat its own guidance and said its integration of The May Department Stores Co. remains “solidly on track” as sales soared. Meanwhile, the books are out for both Lord & Taylor and the Bridal Group businesses. Federated is said to be seeking $1.2 billion for Lord & Taylor. See Federated’s, Page 13 PHOTO BY JOHN AQUINO PHOTO BY WWD.COM WWDTHURSDAY Sportswear FASHION ™ Fall’s frilled looks feature ruffl ed cuffs and collars on fi tted blazers and 6 denim that goes dark in shades of black, gray and burgundy. A weekly update on consumer attitudes and behavior based on ongoing research from Cotton Incorporated GENERAL Federated Department Stores’ bottom line in the fi rst quarter of its “tran- 1 sition year” was weighed down by costs from merging with May Co. -

Malls & Outlets

WESTFIELD FASHION SQUARE WESTFIELD.COM/FASHIONSQUARE 14006 RIVERSIDE DRIVE @ WOODMAN AVE, SHERMAN OAKS, CA 91423 1-818-783-0550 MON-FRI 10:00am-9:00pm SATURDAY 10am-9pm* SUNDAY 11am-7pm The closest mall to the Sheraton Universal, featuring over 120 stores such as Macy’s, Bloomingdales, Apple & Banana Republic. * Please note: Bloomingdales closes at 8:00pm on Saturdays. DIRECTIONS: TURN LEFT OUT OF OUR DRIVEWAY AND PROCEED TO THE BOTTOM OF THE HILL. GO STRAIGHT THROUGH THE TRAFFIC LIGHT ACROSS LANKERSHIM BLVD AND UP THE CAMPO DE CAHUENGA BRIDGE. STAY TO THE RIGHT AND ENTER THE 101 FREEWAY NORTH. FOLLOW THE 101 APPROXIMATELY 4.5 MILES TO THE WOODMAN AVE EXIT. TURN RIGHT OFF THE EXIT ONTO WOODMAN AVE AND IMMEDIATELY GET INTO THE FAR LEFT LANE. TURN LEFT AT THE FIRST TRAFFIC LIGHT ONTO RIVERSIDE DRIVE. THE MALL IS ON YOUR LEFT SIDE. (Approximately 10 minutes.) GLENDALE GALLERIA / THE AMERICANA @ BRAND 2148 GLENDALE GALLERIA, GLENDALE, CA 91210 GALLERIA: GLENDALEGALLERIA.COM AMERICANA: AMERICANAATBRAND.COM 1-818-240-9481 1-818-637 8900 MON-SAT 10am-9pm MON-THURS 10am-9pm SUN 11am-7pm FR-SAT 10am-10pm SUN 11am-8pm The Glendale Galleria is a large indoor mall with over 270 stores including Macy’s, Nordstrom, JC Penny, Apple, Hollister & Target. Directly adjacent to the Galleria is The Americana, a large upscale, outdoor mall featuring over 75 shops such as A/X Armani Exchange, Kitson , Guess and restaurants such as The Cheesecake Factory, Granville Café featuring farm fresh, organic ingredients and Katsuya, one of L.A.’s top Japanese restaurants. -

··Y of Los ANGEL. Office of the City Clerk CITY CLERK Council and Public Services FRANK T

J. MICHAEL CAREY -··y OF Los ANGEL. Office of the City Clerk CITY CLERK Council and Public Services FRANK T. MARTINEZ Room 395, City Hall Executive Officer Los Angeles, CA 90012 Council File Information - (213) 978-1043 General Information - (213) 978-1133 When making inquiries Fax: (213) 978-1040 relative to this matter refer to File No. HELEN GINSBURG Chier, Council and Public Services Division 01-0317 JAMES K. HAHN MAYOR PLACE IN FILES CDs 1 & 14 JUL 1 8 2002 ~ DEPUTY ; I July 15, 2002 1 Councilmember Reyes Councilmember Bernson Councilmember Pacheco Chief Legislative Analyst City Attorney Housing Department Planning Department, Cultural Affairs Department Planning Commission Bureau of Engineering, Director of Planning Land Development Group Office of Zoning Administration Department of Building & Safety Community Planning Section c/o Zoning Coordinator Geographic Information Section Department of Transportation, Attn: Fae Tsukamoto Traffic/Planning Sections RE: ESTABLISHING THE AVENUE 57 TRANSIT ORIENTED DISTRICT SPECIFIC PLAN IN THE HIGHLAND PARK COMMUNITY OF NORTHEAST LOS ANGELES COMMUNITY PLAN At the meeting of the Council held June 11, 2002, the following action was taken: Attached report adopted, as amended ......................... ···----=X=--- Amending motion (Reyes - Bernson) adopted ..................... ·----=X=--~ Ordinance adopted ............................................. ·-~6_-~1=-:8;.....-_0:;..:2=--- Ma yo r a pp roved . _....;::6;_-....;::2'-'7;_-_0:..:2=--- 0rdi nanc e Number .............................................. ·-~1~7....;4:..:6:..:6:..:3=--- Po sting date ................................................... _ _.c7_-_.c9;_-_0~2- E ff e ct i ve date ................................................. _....;::8_-....;::1:....:8;.....-....;0:..:2=--- F i ndi ng s adopted ............................................... ___X=----- Environmental Impact Report certified ......................... ·--~X=----- (}~~~ ~ity Cl~e~- \I~ o-v' Jr . -

North American Airports Shine Under Massive Redevelopment

Special Issue TFWA World Exhibition/ FDFA October/November 2013 North American airports shine under INSIDE INSIDER News North America massive redevelopment FDFA updates; Peace Arch invests for success There is no doubt that this LAX, JFK unveiled is the year for North America’s DFS – ups the ante on luxury airports to move into the limelight International Shoppes remodels/ as more and more of the country’s expands at BOS, PHL outdated aviation infrastructure DFA ushers in digital era in MIA benefit from massive infusions of investment and rebuilding. Latin America Following the recent Monalisa, Mannah, Grupo Wisa, Shopping China, Bernabel, completion of billions of dollars London Supply, Las Delicias, of international terminal projects Dufry, Brazil, Rivera Overview in Miami and Atlanta, JFK International Airport Terminal Caribbean 4, operated by JFKIAT, ushered San Juan airport privatization; in a new era in its history in Havana upgrades May with the opening of its $1.4 billion redevelopment expansion that added 346,000-square-feet of space on Concourse D to accommodate Delta Airlines. The centerpiece of the new Tom Bradley International Terminal at Los Angeles In September, Los Angeles International Airport is the 150,000-square-foot Antonio Villaraigosa Pavilion that International Airport began will feature more than 60 premier dining, luxury retail and duty free shops. operations from its $1.9 billion new Tom Bradley International American airport operations, world-class gateway (exclusive On the Kentucky Bourbon Trail Record American whiskey sales Terminal, considered the crown details of which are covered inside interview begins on page 51). lead to booming bourbon tourism jewel of LAX’s $4.1-billion the pages of this issue. -

Freed Fliers Go 3 Separate Ways by the Associated Press Charles, 27, Captive Nine Months

Today: Our Weekend Enjoyment Section SEE TABLOID INSERT the Weather THEDAILY FINAL Cloudy with periods of rain Red Bank, Freehold likely today, tonight and to- tang Branch 7 EDITION morrow. 26 PAGES Momnouth County's Outstanding Home Newspaper TEN CENTS VOL.95 NO. 68 RED BANK, N.J. FRIDAY, SEPTEMBER 29,1972 iiiiiiiiiiiiiiumiimiiiiiuiftiHiimiiniiiim iiiiniiiiiiiimiiiiiiiimiaiiiiiuiiiiiiiiitiiiiiiiiiiiiiiiiiiiiiiiiiiiiii i m HiiiiiiiiiiiiiiiiiiiiiiiiiiiniuiuniiiminiiiiiiiinniiiiiiiiiiiHiiiniiiinuBniinmmiainHniiiDniiBmiiiiiiiiiiii iiinuniiiiiiiiiiiiiiiiiiiii Delegates Press for Park Ferry Service gested urban area. Twenty By SHERRY FIGDOUE p-N.J., responded with nearly aide to Mr. Howard, who au- were barred by the House Jack Vandenberg, aide to Jacob K. Javits, R-N.Y., cos- "There's always the possi- thored the deleted amend- parliamentarian. U.S. Sen Clifford P. Case, R- ponsor of the 1971 Senate bill, bility the (House) bill will million people live within two. identical statements yes- hours of the 26,000 acre park, WASHINGTON — Mon- terday in the wake of House ments, said yesterday that The Senate adopted its Ga- N.J., said he was "Virtually Mr. Vandenberg said "The pass with the amendments. If "essentially, very little can be teway bill last year and in-'certain a bill will be enacted New York people are as inter- it doesn't, there is a possi- many of them subsisting on tnouth County's congressional deletion of a $30 million provi- poverty level incomes, and delegation here is united in sion for development of water done now, since conferees cluded in it the f 30 million de- this session." ested in the ferry as we are." bility that a separate bill transit to the park. -

Kitson Opens Beverly Hills Shop

Exterior of Kitson in Beverly Hills. Photo courtesy Kitson RETAIL Kitson Opens Beverly Hills Shop By Andrew Asch | Wednesday, July 8, 2020 Fraser Ross once ran a fleet of more than 15 Kitson stores, which spanned from the original flagship on Los Angeles’ Robertson Boulevard to Las Vegas. The fleet was shuttered more than five years ago, and Ross reopened the Kitson flagship in 2016. Since then, he’s reopened a handful of stores on Robertson. It looks like Kitson is ready to move beyond its neighborhood. On July 3, Ross opened what he described as a "mini-Kitson," at 321 N. Beverly Dr. in Beverly Hills, Calif. The shop has a 1,600-square-foot selling space, much smaller than the 5,000-square-foot Kitson flagship at 115 S. Robertson Dr. Ross said that the new location would offer many of the gifts, and styles for women, men and children that have been popular a few minutes drive away on Robertson. “It’s the best of the best,” he said of the new shop. He decided to open the new space because he felt that Kitson enjoyed good business when it ran a pop- up shop at a Lucky Brand store at 420 N. Beverly Dr. The Lucky Shop has been closed since the beginning of the COVID-19 pandemic. “I always wanted to run a store in Beverly Hills, but I could never afford the rent,” Ross said of the new space. “It was a great deal.” He signed a two-year lease. Jay Luchs of Newmark Knight Frank brokered the deal. -

Oil & Hazardous Substance Release

OIL & HAZARDOUS SUBSTANCE RELEASE PREVENTION & RESPONSE FUND Fiscal Year 2007 - 2008 BIENNIAL REPORT July 1, 2006 through June 30, 2008 Alaska Department of Environmental Conservation Prepared by the Division of Spill Prevention and Response Presented to the First Session of the 26th Alaska Legislature January 20, 2009 Sarah Palin, Governor Larry Hartig, Commissioner DEPARTMENT OF ENVIRONMENTAL CONSERVATION OIL AND HAZARDOUS SUBSTANCE RELEASE PREVENTION AND RESPONSE FUND FISCAL YEAR 2007 – 2008 Biennial Report to the Legislature JULY 1, 2006 THROUGH JUNE 30, 2008 January 2009 This page intentionally left blank OIL AND HAZARDOUS SUBSTANCE RELEASE PREVENTION AND RESPONSE FUND BIENNIAL REPORT FISCAL YEAR 2007 & 2008 TABLE OF CONTENTS Page Introduction …………………………………………………………………………………… 1 Oil & Hazardous Substance Release Prevention & Response Fund Diagram …………………. 3 Reports: Table A: Summary of Fiscal Year 2007 & 2008 Expenditures and Obligations ……….. 4 Table B: Prevention Mitigation and Response Mitigation Revenues ………………….... 6 . Table C: Revenue Sources .............................................................................................. 17 Table D: Summary of Response Contracts & Purchases in Excess of $10,000.00 ….…… 18 Table E: Summary of Fiscal Year 2008 & 2009 Appropriations ….…………………….. 20 Table F: Fiscal Year 2007 & 2008 Projects .................................................................... 22 Table G: Fiscal Year 2007 & 2008 Personal Services Costs for Projects ......................... 36 Table H: DEC Inventory -

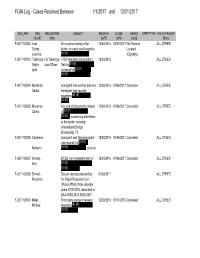

Department of State FOIA Log 2017

FOIA Log - Cases Received Between 1/1/2017 and 12/31/2017 REQ_REF REQ REQUESTER SUBJECT RECEIVE CLOSE GRANT EXEMPTIONS FEE CATEGORY NAME ORG DATE DATE CODE DESC F-2017-00002 Leal All records relating to the 12/30/2016 02/27/2017 No Records ALL OTHER Oteiza, border crossing card issued to Located Lourdes (b) (6) . (Oglesby) F-2017-00003 Tabangay-Fel Tabangay I-130 immigrant visa petition 12/30/2016 ALL OTHER Vigilla, Law Offices filed by (b) (6) April on behalf of (b) (6) (b) (6) F-2017-00004 Monarrez, Immigrant visa petition and non- 12/30/2016 01/06/2017 Cancelled ALL OTHER Carlos immigrant visa records regarding (b) (6) (b) (6) F-2017-00005 Monarrez, Any and all documents related 12/30/2016 01/06/2017 Cancelled ALL OTHER Carlos to (b) (6) (b) (6) concerning detentions at the border crossing International Bridge Brownsville, TX F-2017-00006 Cardenas Immigrant and Non-immigrant 12/30/2016 01/06/2017 Cancelled ALL OTHER , visa records for (b) (6) Norberto (b) (6) records F-2017-00007 Arocha, B1/B2 non-immigrant visa for 12/30/2016 01/06/2017 Cancelled ALL OTHER Ana (b) (6) (b) (6) F-2017-00008 Emmel, Special reports produced by 01/03/2017 ALL OTHER Benjamin the Rapid Response Unit (Public Affairs) from calendar years 2015-2016, described in DAA-0059-2013-0008-0001 F-2017-00010 Miller, Third party passport request 12/29/2016 01/17/2018 Cancelled ALL OTHER Michael regarding (b) (6) (b) (6) REQ_REF REQ REQUESTER SUBJECT RECEIVE CLOSE GRANT EXEMPTIONS FEE CATEGORY NAME ORG DATE DATE CODE DESC F-2017-00011 Cabrera, Cables, files, and documents -

5-30-68 Not Held REGULAR MEETING of the COUNCIL of the CITY of SAN DIEGO, CALIFORNIA

CITY OF SAN DIEGO. CALIFORNIA COUNCIL ~IINUTES 5-30-68 Not Held REGULAR MEETING OF THE COUNCIL OF THE CITY OF SAN DIEGO, CALIFORNIA - THURSDAY, MAY 30, 1968 IN THE CHAMBER OF THE COUNCIL - ADMINISTRATION BUILDING COMMUNITY CONCOURSE - NOT HELD - Present - None. Absent -- Councilmen Cobb, Loftin, Scheidle, Hom, Morrow, Walsh, Hitch, Schaefer and Mayor Curran. Clerk --- John Lockwood. In the absence of the members of the City Council, the City Clerk declared this Meeting adjourned until 9:00 a.m., Tuesday, June 4, 1968, in the Chamber of the City Council, 12th Floor, City Administration Building, Community Concourse. ATTEST: Adjourned tgl CITY OF SAN DIEGO. CALIFORNIA COUNCIL WNUTES 5-30-68 held 6-4-68 2 ADJOURNED REGULAR MEETING OF THE COUNCIL .OF THE.CITY OF SAN.DIEGO, .CALIFORNIA. THURSDAY, MAY 30, 1968 ~ HELD TUESDAY, JUNE 4, 1968 IN.THE CHAMBER OF THE COUNCIL.~ ADMINISTRATION BUILDING COMMUNITY.CONCOURSE Present-Councilmen Cobb, Loftin, Scheidle, Hom, Hitch and Mayor Curran. Absent--Councilmen Morrow, Walsh and Schaefer. Clerk---John Lockwood.' The Adjourned Regular Meeting was called to order by Mayor Curran at 9:00 a.m. It was reported that this meeting was adjourned from Thursday, May 30, 1968 to Tuesday, June 4, 1968 by the City Clerk. The City Clerk reported that a copy of the Notice of Adjournment covering the adjournment of this meeting from Thursday, May 30, 1968 to 9:00 a.m., Tuesday, June 4, 1968, had been posted as required by law, and the Notices of Adjournment had been mailed to the members of the City Council and any others who had given written request for such notices as required by law, and that the proper affidavits covering such posting and mailing are on file. -

Los Angeles Business Journal

labusinessjournal.com LOS ANGELES BUSINESS JOURNAL Volume 38, Number 45 THE COMMUNITY OF BUSINESSTM November 7 - 13, 2016 • $5.00 UpUp Front Fund Roots for Plant-Based Foods Retailers Sold INVESTMENT: Powerplant in August, is to make money while doing good and taking care of the Earth, said Rampolla. On Boulevard? aims to harvest healthy revenue. “Our mission is to make an impact on the food system but REAL ESTATE: By CAROLINE ANDERSON Staff Reporter generate excellent returns,” he Coffee store said. “We believe the best way to may stoke heat for Robertson. When L.A. vegetarian restaurant chain Veggie make money is to make a positive Grill raised $22 million in October, money it plans to impact, and we aim to prove it.” By DAINA BETH SOLOMON Staff Reporter use to double in size, it turned to some familiar faces Powerplant has invested who had formed a new venture capital fund. in Hampton Creek, a San Rampolla Blue Bottle Coffee Co. is set to sign a 10-year A video-game Powerplant Ventures, which has raised $42 Francisco producer of plant-based lease on Robertson Boulevard, and the street’s exec fights for million for its first fund, is devoted to plant-based mayonnaise, and Marina del Rey online marketplace boosters feel bullish that the gourmet roaster will job opportunities food companies. Its principals include Veggie Grill Thrive Markets, which is trying to make the type perk up the long-struggling retail strip between for veterans. co-founders Kevin Boylan and T.K. Pillan; Mark of products sold in Whole Foods available to Beverly Boulevard and Third Street. -

NYSE MAC 2008.Pdf

Macerich 2008 Annual Report Financial Highlights Corporate Information (all amounts in thousands, except per share and per square foot amounts) 2008 2007 2006 2005 2004 Principal Outside Counsel Corporate Headquarters Stock Exchange Listing O’Melveny & Myers LLP 401 Wilshire Boulevard, Suite 700 New York Stock Exchange Los Angeles, California Santa Monica, California 90401 Symbol: MAC Operating Data 310.394.6000 The common stock of the Company is listed Total revenues $ 901,490 $ 814,314 $ 749,619 $ 660,147 $ 495,175 Independent Auditor Certifi cations and traded on the New York Stock Exchange Shopping center and operating expenses $ 287,077 $ 256,730 $ 233,669 $ 203,829 $ 146,465 Deloitte & Touche LLP under the symbol “MAC.” The common Los Angeles, California The Company submitted a Section Management companies’ operating expenses $ 77,072 $ 73,761 $ 56,673 $ 52,840 $ 44,080 stock began trading on March 10, 1994, 303A.12(a) CEO Certifi cation to the at a price of $19 per share. In 2008, the REIT general and administrative expenses $ 16,520 $ 16,600 $ 13,532 $ 12,106 $ 11,077 NYSE last year. In addition, the Company Transfer Agent Company’s shares traded at a high of fi led with the Securities and Exchange Net income (loss) available to common stockholders $ 183,316 $ 73,704 $ 217,404 $ (93,614) $ 82,493 Computershare Trust Company, N.A. $76.50 and a low of $8.31. Commission the CEO/CFO certifi cation Net income (loss) per share available to common $ 2.47 $ 1.02 $ 3.05 $ (1.57) $ 1.40 P.O. Box 43010 required under Section 302 of the Sarbanes- As of February 10, 2009, there were stockholders-diluted Providence, Rhode Island 02940-3010 Oxley Act and it is included as an exhibit 941 stock holders of record. -

Extensions of Remarks

9760 EXTENSIONS OF REMARKS April 24, 1984 EXTENSIONS OF REMARKS KIM DAE JUNG office will not constitute a peaceful change which brute force abolished in spite of pop of power by democratic process. ular support. We should return not only to A genuine, peaceful change of administra the pre-Yushin constitution but also to the HON. BARNEY FRANK tions is possible only when the people freely laws governing the press and elections. OF MASSACHUSETTS and without fear exercise their rights as I want to make known to our people and IN THE HOUSE OF REPRESENTATIVES masters of the nation. Under the present the world my view that this is a most urgent circumstances, there is no guarantee of the agenda item in our struggle for democracy. Tuesday, April 24, 1984 people's sovereignty founded in such basic It is also my fervent hope that all opposi • Mr. FRANK. Mr. Speaker, Mr. Kim rights as free elections and freedom of the tion forces will come around to this view Dae Jung, the exiled Korean dissident press, and thus political change means noth and make concerted efforts to bring it into leader, recently issued a statement ing. It is a mere relay of power between dic reality. tators in which another Chun Doo Hwan C. Improvement of human rights to be which outlines his views and proposals can be imposed upon the South Korean regarding Korea. Mr. Kim was in 1971 people. preceded by structural improvements the opposition candidate for Presi The pivotal issue, therefore, is not one of Genuine improvements in human rights dent.