Macedonian Outsourcing Industry Report (2019)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Contract Number: 4400016179

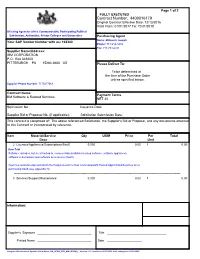

Page 1 of 2 FULLY EXECUTED Contract Number: 4400016179 Original Contract Effective Date: 12/13/2016 Valid From: 01/01/2017 To: 12/31/2018 All using Agencies of the Commonwealth, Participating Political Subdivision, Authorities, Private Colleges and Universities Purchasing Agent Name: Millovich Joseph Your SAP Vendor Number with us: 102380 Phone: 717-214-3434 Fax: 717-783-6241 Supplier Name/Address: IBM CORPORATION P.O. Box 643600 PITTSBURGH PA 15264-3600 US Please Deliver To: To be determined at the time of the Purchase Order unless specified below. Supplier Phone Number: 7175477069 Contract Name: Payment Terms IBM Software & Related Services NET 30 Solicitation No.: Issuance Date: Supplier Bid or Proposal No. (if applicable): Solicitation Submission Date: This contract is comprised of: The above referenced Solicitation, the Supplier's Bid or Proposal, and any documents attached to this Contract or incorporated by reference. Item Material/Service Qty UOM Price Per Total Desc Unit 2 Licenses/Appliances/Subscriptions/SaaS 0.000 0.00 1 0.00 Item Text Software: includes, but is not limited to, commercially available licensed software, software appliances, software subscriptions and software as a service (SaaS). Agencies must develop and attach the Requirements for Non-Commonwealth Hosted Applications/Services when purchasing SaaS (see Appendix H). -------------------------------------------------------------------------------------------------------------------------------------------------------- 3 Services/Support/Maintenance 0.000 0.00 -

Smart Networks and Services Version 30 June 2020

Draft proposal for a European Partnership under Horizon Europe Smart Networks and Services Version 30 June 2020 Summary The European communication networking and services sector is proposing the Smart Networks and Services Partnership to secure European leadership in the development and deployment of next generation network technologies and services, while accelerating European industry digitization. It will position Europe as a lead market and positively impact the citizens’ quality of life, while boosting the European data economy and contributing to ensure European sovereignty in critical supply chains. This document is supported by ACKNOWLEDGEMENTS 5G-IA and the Networld2020 European Technology Platform launched a Smart Networks and Services Task Force to prepare this Partnership proposal in Horizon Europe. AIOTI joined the Task Force. Additional contributors are from Cispe.cloud and the NESSI European Technology Platform. All these organizations appreciate the work of the Task Force and approved this report. DISCLAIMER AND COPYRIGHT STATEMENT This document contains material which is prepared by 5G-IA, the Networld2020 European Technology Platform, AIOTI, Cispe.cloud and the NESSI European Technology Platform and is based on referenced material and documents from public institutions and industry associations. 1 About this draft In autumn 2019 the Commission services asked potential partners to further elaborate proposals for the candidate European Partnerships identified during the strategic planning of Horizon Europe. These proposals have been developed by potential partners based on common guidance and template, taking into account the initial concepts developed by the Commission and feedback received from Member States during early consultation1. The Commission Services have guided revisions during drafting to facilitate alignment with the overall EU political ambition and compliance with the criteria for Partnerships. -

Digitally Empowered Generation Equality EUROPE Women, Girls and ICT in the Context of COVID-19 in Selected Western Balkan and Eastern Partnership Countries

ITUPublications International Telecommunication Union Europe 2021 Digitally empowered Generation Equality EUROPE Women, girls and ICT in the context of COVID-19 in selected Western Balkan and Eastern Partnership countries In partnership with: Digitally empowered Generation Equality Generation Digitally empowered Digitally empowered Generation Equality: Women, girls and ICT in the context of COVID-19 in selected Western Balkan and Eastern Partnership countries DISCLAIMER The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of ITU concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontiers or boundaries. Dotted and dashed lines on maps represent approximate border lines for which there may not yet be full agreement. The mention of specific companies or of certain manufacturers’ products does not imply that they are endorsed or recommended by ITU in preference to others of a similar nature that are not mentioned. Errors and omissions excepted, the names of proprietary products are distinguished by initial capital letters. All reasonable precautions have been taken by ITU to verify the information contained in this publication. However, the published material is being distributed without warranty of any kind, either expressed or implied. The responsibility for the interpretation and use of the material lies with the reader. The opinions, findings and conclusions expressed in this publication do not necessarily reflect the views of ITU or its membership. Please consider the environment before printing this report. © ITU 2021 Some rights reserved. This work is licensed to the public through a Creative Commons Attribution-Non- Commercial-Share Alike 3.0 IGO license (CC BY-NC-SA 3.0 IGO). -

Tracker Master 9.25.18 TM

IT Services & BPO Implied Implied Implied Announce Target Target Description Buyer Enterprise EV/ EV/ Transaction Comments Date Value ($M) Revenue EBITDA Calligo (UK) Ltd acquired Network Integrity Services Ltd for an undisclosed amount. The acquisition Network Integrity {match score: 00} Network Integrity Services provides an array of services, including IT consulting, web would allow Calligo (UK) Ltd to expand its local presence throughout the United Kingdom. Network 12/3/2020 Calligo (UK) Ltd. NA NA NA Services Ltd. design, and systems integration. Integrity Services Ltd is located in Salford, Greater Manchester, United Kingdom and provides information technology services. It has around 160 employees. {match score: 00} BigBear, Inc. provides cost effective and cutting edge information technology NuWave Solutions LLC acquired Big Open Inc, trading as BigBear Inc for an undisclosed amount. The NuWave 12/3/2020 BigBear, Inc. solutions. It offers software design, engineering, and platform development services to its customers. NA NA NA transaction would enhance NuWave Solutions LLC’s existing capabilities. Founded in 2008, Big Open Solutions LLC The company was founded in 2008 and is headquartered in San Diego, CA. Inc is located in San Diego, California, United States and provides software services. {match score: 00} In 2002, four friends saw the need for true customer service in the Ottawa IT and computer industry, so they took action. Mathew Lafrance, Christian Ste-Marie, Allan Ghosn and Mathieu Bouchard joined forces to bring their idea to life and excellent IT services to market. There Convergence Networks acquired Grade A for an undisclosed amount. The acquisition is in line with the was no shortage of companies selling hardware and software, but after-sales IT support was (and still Convergence growth strategy of both the companies and enhances their service offerings. -

Insight MFR By

Manufacturers, Publishers and Suppliers by Product Category 7/18/2019 10/100 Hubs & Switch COMPREHENSIVE CABLE IOGEAR TECHNOLOGY QUANTUM VCE COMPANY LLC 3COM COMTROL IXIA QVS INC. VERBATIM 4XEM CORP. CONNECTPRO JUNIPER NETWORKS RADWARE VERTIV ACCELL CP TECHNOLOGIES KANEX RAM MOUNTS VISIONTEK ADTRAN CRESTRON ELECTRONICS KANGURU RAPID TECHNOLOGIES LLC. VIVOTEK ADVANTECH CO LTD CYBERDATA SYSTEMS KENSINGTON RARITAN VMWARE AEROHIVE NETWORKS CYBERPOWER SYSTEMS KRAMER ELECTRONICS, LTD. RED LION CONTROLS WASP BARCODE ALCATEL LUCENT DATTO, INC. LANTRONIX RIVERBED TECHNOLOGIES WIFI‐TEXAS.COM INC ALLIED TELESIS DELL LENOVO ROSE ELECTRONIC W‐LINX TECHNOLOGY ALTRONIX DELL EMC LG ELECTRONICS ROSEWILL XIRRUS (SEE NOTES) ALURATEK, INC. DIGI INTERNATIONAL LINKSYS RUCKUS WIRELESS ZYXEL AMER NETWORKS DIGIUM MANHATTAN WIRE PRODUCTS SABRENT Adapter IDE/ATA/SATA AMX D‐LINK SYSTEMS MCAFEE SANHO ADAPTEC ANKER EATON MELLANOX SAVVIUS INC ADDONICS TECHNOLOGY INC. APC EDGECORE MICRON CONSUMER PRODUCTS GROUP SDA ALERATECH ARISTA NETWORKS EDGEWATER NETWORKS INC MICROSEMI CORP SENNHEISER ALURATEK, INC. ARRIS GROUP INC ENGENIUS MILESTONE SYSTEMS INC SHARP APRICORN ASUS ENTERASYS NETWORKS MITEL SHORETEL ARECA US ATEN TECHNOLOGY ETHERWAN MONOPRICE SIGNAMAX ATTO TECHNOLOGY ATLONA EVGA.COM MOTOROLA ISG SIIG AVAGOTECH TECHNOLOGIES AUDIOCODES, INC. EXABLAZE MOXA TECHNOLOGIES, INC. SISOFTWARE AXIOM MEMORY AUTOMATION INTEGRATED LLC EXACQ TECHNOLOGIES INC NETAPP SMARTAVI INC BYTECC AVAYA EXTREME NETWORKS NETEON TECHNOLOGIES INC. SMC NETWORKS CABLES TO GO AXIS COMMUNICATIONS EXTRON NETGEAR, INC. STAMPEDE TECHNOLOGIES INC CHENBRO B & B ELECTRONICS FORTINET NETRIA STARTECH.COM CISCO SYSTEMS BELKIN COMPONENTS FUJITSU SCANNERS NETSCOUT SYSTEMS, INC SUPERMICRO COMPUTER CORSAIR MEMORY BLACK BOX FUJITSU SERVER STORAGE NOVATEL WIRELESS SYBA TECH LTD CRU ‐ CONNECTOR RESOURCES BLACKMAGIC DESIGN USA GARRETTCOM OMNITRON TARGUS DELL BLONDER TONGUE LABORATORIES GEAR HEAD ORACLE TEK‐REPUBLIC DELL EMC BOSCH SECURITY GEFEN OVERLAND STORAGE TELEADAPT, INC. -

Seavus AB Ranked Among Top 501 Global Managed Service Providers by Channel Futures

MSP501 winners 2018-07-03 11:18 CEST Seavus AB Ranked Among Top 501 Global Managed Service Providers by Channel Futures DATE July 3rd, 2018: Seavus AB ranks among the world’s 501 most strategic and innovative managed service providers (MSPs), according to Channel Futures 11th-annual MSP 501 Worldwide Company Rankings. The MSP 501 is the first, largest and most comprehensive ranking of managed service providers worldwide. This year Channel Futures received a record number of submissions. Applications poured in from Europe, Asia, South America and beyond. As it has for the last three years, Channel Futures teamed with Clarity Channel Advisors to evaluate these progressive and forward-leaning companies. MSPs were ranked according to our unique methodology, which recognizes that not all revenue streams are created equal. We weighted revenue figures according to how well the applicant's business strategy anticipates trends in the fast-evolving channel ecosystem. "The MSP 501 TOP 100 WINNERS reward is a big honor for Seavus Managed Service Provider, as it recognizes all the hard work and commitment that our engineers have given the year’s behind." said Ruzhica Kalkashliev, Managed Services Division Manager, Seavus. "We couldn’t be prouder of what we have achieved today, taking in consideration all the services we provide to our Customers so far." Channel Futures is pleased to honor Seavus AB. For the first time, Channel Futures will also name 10 special award winners, including MSP of the Year, CEO of the Year and one Lifetime Achievement Award for a career of excellence in the channel. The MSP501winners and award recipients will be recognized at a special ceremony at Channel Partners Evolution, held this year October 9-12 in Philadelphia, as well as in the Fall issue of Channel Partners Magazine. -

Contract Number: 4400016179

Page 1 of 2 FULLY EXECUTED Contract Number: 4400016179 Original Contract Effective Date: 12/13/2016 Valid From: 01/01/2017 To: 12/31/2021 All using Agencies of the Commonwealth, Participating Political Subdivision, Authorities, Private Colleges and Universities Purchasing Agent Name: Hosler Raeden Your SAP Vendor Number with us: 102380 Phone: 717-787-4103 Fax: Supplier Name/Address: IBM CORPORATION P.O. Box 643600 PITTSBURGH PA 15264-3600 US Please Deliver To: To be determined at the time of the Purchase Order unless specified below. Supplier Phone Number: 4433158492 Contract Name: Payment Terms IBM Software & Related Services NET 30 Solicitation No.: Issuance Date: Supplier Bid or Proposal No. (if applicable): Solicitation Submission Date: This contract is comprised of: The above referenced Solicitation, the Supplier's Bid or Proposal, and any documents attached to this Contract or incorporated by reference. Item Material/Service Qty UOM Price Per Total Desc Unit 2 Licenses/Appliances/Subscriptions/SaaS 0.000 0.00 1 0.00 Item Text Software: includes, but is not limited to, commercially available licensed software, software appliances, software subscriptions and software as a service (SaaS). Agencies must develop and attach the Requirements for Non-Commonwealth Hosted Applications/Services when purchasing SaaS (see Appendix H). -------------------------------------------------------------------------------------------------------------------------------------------------------- 3 Services/Support/Maintenance 0.000 0.00 1 0.00 Information: -

Entrepreneurship Ecosystem in North Macedonia

ENTREPRENEURSHIP ECOSYSTEM IN NORTH MACEDONIA MARKET ASSESSMENT ENTREPRENEURSHIP ECOSYSTEM IN NORTH MACEDONIA MARKET ASSESSMENT ENTREPRENEURSHIP ECOSYSTEM IN NORTH MACEDONIA MARKET ASSESSMENT Author: Makedonka Dimitrova SKOPJE, 2020 This publication was developed within the framework of the project Strengthening Social Dialogue, funded by the European Union and implemented by the International Labour Organization. This publication was produced with the financial support of the European Union. Its contents are the sole responsibility of the author and do not necessarily reflect the views of the European Union and the International Labour Organization. ENTREPRENEURSHIP ECOSYSTEM IN NORTH MACEDONIA MARKET ASSESSMENT Contents List of Abbreviations ............................................................................................................. 4 1. REPORT OUTLINE AND METHODOLOGY ........................................................................ 5 2. OVERALL ECONOMIC ENVIRONMENT ........................................................................... 7 2.1 Policies for MSME Development ................................................................................ 8 2.2 Entrepreneurial Ecosystem .....................................................................................11 2.3 BSPs Target Market ...................................................................................................15 2.4 Donor Support to Entrepreneurship and Business Services ..................................17 3.ENTREPRENEURIAL SERVICES -

Former Yugoslav Republic of Macedonia

WESTERN BALKANS REGIONAL R&D STRATEGY FOR INNOVATION COUNTRY PAPER SERIES FORMER YUGOSLAV REPUBLIC OF MACEDONIA WORLD BANK TECHNICAL ASSISTANCE PROJECT (P123211) OCTOBER 2013 Country Paper Series: FYR Macedonia ACRONYMS ADA Austrian Development Agency AI Activity Index APERM Agency for Promotion of Entrepreneurship of the Republic of Macedonia ARWU Academic Ranking of World Universities BAS Business Advisory Services BERD Business Expenditure on R&D BSCB Business Start-up Center Bitola CERN European Organization for Nuclear Research CIP Competitiveness and Innovation Program CIS Community Innovation Survey COST European Cooperation in Science and Technology EC European Commission EEN European Enterprise Network ELSR Equipping Laboratories for Scientific Research and Applicative Activities ERA European Research Area ESA Enterprise Support Agency EU European Union FDI Foreign Direct Investment FP6 Framework Program 6 FP7 Framework Program 7 FTE Full-time Equivalents FYRM Former Yugoslav Republic of Macedonia GBAORD Government Budget Appropriation or Outlays on Research and Development GDP Gross Domestic Product GEM Global Entrepreneurship Monitor GOVERD Government Expenditure on R&D GTZ Gesellschaft Technische Zusammenarbeit – German Society Technical Corporation HERD Higher Education R&D ICT Information and Communication Technology IIP International Intellectual Property IP Intellectual Property IPA Instrument for Pre-Accession Assistance IPARD IPA Rural Development Program IPR Intellectual Property Rights IRC Innovation Relay Center ISO -

Networldeurope Member Organisations Organisation Country

NetworldEurope Member organisations Organisation Country Stakeholder Group 3logic MK srl Italy SME 4GCelleX Israel SME 5GW News United States COOP Aalborg University Denmark Research Domain Aalto University Finland Research Domain Abeeway France SME Abo Akademi University Finland Research Domain Accelleran Belgium SME A-CING Spain Industry ACORDE Technologies S.A. Spain SME Acreo Swedish ICT AB Sweden Research Domain ACTA Ltd Greece SME ADVA AG Optical Networking Germany Industry ADVANTIC SISTEMAS Y SERVICIOS S.L. Spain SME Aetheric Engineering Ltd United Kingdom Industry AFUSOFT Kommunikationstechnik GmbH Germany Industry Agence Wallonne des Telecommunications Belgium COOP AGH University of Science and Technology, Department of Telecommunications Poland Research Domain AICO EDV-Beratung GmbH Austria SME AIJU - Asociación de la Industria del Juguete Spain Research Domain Airbus Defence and Space (former ASTRIUM) France Industry AITIA International, Inc. Hungary SME Albatronics Israel SME Alcatel-Lucent Germany Industry ALETI Argentina COOP Almouroltec, Lda Portugal SME Alpineon d.o.o. Slovenia SME ALTRANPORTUGAL, S.A. Portugal Industry AMBEENT WiRELESS Turkey SME Amber Flux Pvt Ltd India COOP AMETIC Spain COOP Amledo & Co Sweden SME Amphinicy Technologies Croatia SME AMVG Turkey SME Ansur Technologies Norway SME Antares S.c.ar.l. Italy SME ANTY Foundation Belgium COOP Antycip Simulation United Kingdom SME ANYBOX PTE. LTD Singapore COOP AnySolution S.L. Spain SME APFUTURA Spain SME AppArt Greece SME Applied RESearch to Technologies s.r.l. (ARES2T) Italy SME APTECH Turkey Industry Aradiom Turkey SME Aragon Technological Institute (ITA) Spain Research Domain Aratos Technologies Greece SME Arcelik A.S. Turkey Industry Arctos Labs Scandinavia AB Sweden SME ARDIC APPLIED RESEARCH DEVELOPMENT INNOVATION CENTER Turkey SME Ariadna Servicios Informáticos S.L. -

Serbia Smart Solution

SERBIA SMART SOLUTION EMBEDDED WORLD 2015 24-26 February Nürnberg, Germany Hall 2 Stand 2-524 ABOUT SERBIA 3 ADVANTAGES OF INVESTING IN SERBIA 4 IT SECTOR 5 BITGEAR 6 MIKROELEKTRONIKA 7 NOVATRONIC 8 SEAVUS 9 CHAMBER OF COMMERCE AND INDUSTRY OF SERBIA 10 SERBIA INVESTMENT AND EXPORT PROMOTION AGENCY − SIEPA 11 USEFUL ADRESSES 12 „Owing to its position on the geographic GENERAL DATA ABOUT SERBIA borderline between the East and West, Location: Serbia is often referred to as a gateway Southeastern Europe, central part of the Western Balkans of Europe and a perfect place for a company to locate its operations if it Geographic coordinates: 44 00 N and 21 00 E wants to closely and most efficiently serve its EU, SEE or Middle Eastern Territory: 88,361 square kilometers customers. The ease of travelling from Belgrade to almost every destination Population: in the world, either directly or with 7.2 million (the data for AP Kosovo and Metohia excluded)* a layover is provided by many major Borders with: international airlines“ Hungary, Romania, Bulgaria, Macedonia, Albania, Montenegro, Bosnia and Herzegovina and Croatia Capital city: Belgrade, circa 1.6 million inhabitants State organization: Parliamentary Republic Official language: Serbian National currency: RSD – dinar Time zone: GMT+1 2 *Source: Statistical Office of the Republic of Serbia 3 ADVANTAGES OF INVESTING IN SERBIA IT SECTOR • Favorable geographic position, owing to which any shipment can reach any location in Europe within 24 hours Serbia’s ICT sector has partnered with the leading technological companies across the world in order to • Highly educated and competitive labor force provide first class solutions to domestic and international clients. -

PRIVATE SECTOR DEVELOPMENT Project Insights Assessment of the National Innovation System of the Former Yugoslav Republic of Mace

PRIVATE SECTOR DEVELOPMENT Project Insights Key contact: Key contact: Assessment of the National Mr Alan Paic Mr Alan Paic Innovation System of the Former Head of Programme Head of Programme OECD Investment Compact for OECD Investment Compact for Yugoslav Republic of Macedonia South East Europe South East Europe [email protected] [email protected] Report in support of the formulation of a National Innovation Strategy www.investmentcompact.org www.investmentcompact.org www.investmentcompact.org This project is funded by the European Union RCI Covers [3].indd 4 RCI Covers [3].indd 4 23/05/2013 19:40 23/05/2013 19:40 Assessment of the National Innovation System of the Former Yugoslav Republic of Macedonia Report in support of the formulation of a National Innovation Strategy December 2013 This document has been produced with the financial assistance of the European Union. The views expressed herein can in no way be taken to reflect the official opinion of the European Union. The information included in this report, and in particular the denomination of territories used in this document, do not imply any judgement on the part of the OECD on the legal status of territories mentioned in this publication. FOREWORD Between 2000 and 2008, the Western Balkan economies experienced rapid growth, modest inflation, and increased macro-economic stability. The onset of the global economic crisis, however, saw a sharp drop in external trade and industrial production across the region. The crisis underscored the fact that buoyant growth prior to 2008 relied, to a large extent, on external financial flows – particularly FDI flows and international capital transfers that offset large and unsustainable trade and current account deficits.