Industry & Trade Summary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LIBATIONS Beer Wines

oct LIBATIONS CHICAGO, IL beer WINEs classic COCKTAILS draught SPARKLING APEROL SPRITZ 14 ROSE CIDER, Cider 8 FRANCOIS MONTAND 13 / 59 Aperol, Proscecco, Soda Virtue • Fenville, MI Brut Rose• Jura, France TULLIA 13 / 59 BLOODY MARY 14 PULASKI PILS, Pilsner 8 Prosecco Brut • Veneto, Italy Vodka, House Mix Off Color Brewing • Chicago, IL + Today’s Skewer 3 CASTELL D’AGE 14 / 63 + High Life Pony 3 MATILDA, Belgian Style Ale 8 Brut Cava • Spain Goose Island • Chicago, IL OLD FASHIONED 14 Bourbon, Demerara, Bitters GUMBALL HEAD , Wheat Beer 8 Three Floyds • Munster, IN WHISKEY SMASH 14 WHITE Whiskey, Mint, Lemon, Demerara APEX PREDATOR, Farmhouse Ale 8 Maplewood Brewery • Darien, IL NORTICO 15 / 68 HURRICANE 14 Alvarinho • Minho, Portugal Light & Dark Rum, Passion Fruit, SOULMAN, Salted Carmel Brown Ale 8 SCARPETTA 13 / 59 Orange Juice, Lime, Grenadine Aleman Brewing. • Chicago, IL Pinot Grigio • Friuli, Italy NEGRONI 14 TAPROOM IPA IPA 8 OTTO’S CONSTANT DREAM 15 / 68 Gin, Carpano Antica, Campari Penrose Brewing • Geneva, IL Sauvignon Blanc • Marlborough, New Zealand EL DIABLO 14 CHOCOLATE CHURRO, Baltic Porter 8 FOLEY JOHNSON 16 / 72 Blanco Tequila, Mezcal, Creme de Cassis Moody Tongue Brewing • Chicago, IL Chardonnay • Carneros, California Ancho Reyes Verde, Lime, Ginger Beer SCOFFLAW 14 Bourbon, Dry Vermouth, Pomegraaite ROSE Grenadine, Lime packaged LA BAMBINA 14 / 63 Nero d’Alvola • Menfi, Sicily MILLER HIGH LIFE martinis 3/7oz • 5/12oz • 12/40oz The Champagne of Beers CRAFTER’S UNION SPARKLING ROSE BEE’S KNEES 14 20/Can MILLER LITE, Pilsner 7 Gin, Blanc Vermouth, Miller Brewing • Milwaukee, WI Lemon, Honey, Sage AMSTEL LIGHT, Lager 7 RED FRENCH 75 14 Heineken N.V. -

Beverages Menu

WWW.JAKEMELNICKS.COM 41. East Superior street, chicago, illinois 60611 312.266.0400 on tap Special Release 3 Floyds: Blot Out the Sun Imperial Stout - 10.4% ABV – 9.00 / 10oz Full-bodied offering with a heavy handed hop addition for a bitter finish. Notes of chocolate, caramel, nuts & coffee. Avery: Tangerine Quad Barrel-Aged Belgian Style Quad - 10.1% ABV – 7.00 / 10oz Patiently aged in the finest of Bourbon barrels. Notes of dark fruit, vanilla & caramel with a burst of tangerine peel. Brooklyn: Capataz Barleywine - 11.3% ABV – 9.00 / 10oz Aged in Pedro Ximenez & amontillado sherry barrels producing notes of deep fruit, nuts, chocolate & rich coffee. The Bruery: The Archetype Strong Ale - 14.6% ABV – 10.00 / 10oz A blend of the best of the best of The Bruery. Their “Bruers” hand selected a number of barrels from their 2400 barrel stock and blended them to produce a barrel-aged ale that boldly represents their ambitious portfolio. Seipps: Extra Pale Pilsner 4.5% ABV – 7.00 / Pint Pilsner – One of Chicago’s original beers. Brewed in collaboration with Metropolitan Brewing. Clean & crisp Bohemian hop character. Coming Soon! Revolution: 2019 Café Deth BA Imperial Oatmeal Stout - 14.8% ABV 14.00 / 10oz Brewed with freshly roasted whole bean coffee from Dark Matter for assertive coffee aromatics without overshadowing the base beer on the palate. Solemn Oath: My Favorite Aunt Tiramisu Stout - 9.0% ABV 13.00 / 10oz Blend of chocolate Poter & coffee Stout aged in bourbon barrels & blended together with fresh coffee, chocolate & vanilla. * Happy hour Drafts Local Offerings on tap Goes Down Easy On the Darker Side * Allagash: Crosspath * Krombacher: Dark 5.5% ABV – 7.00 / Pint Dark Lager - 4.7% ABV Golden Ale – A celebration of the versatility of 7.00 / Krombacher Glass Maine’s grain. -

Study of Proposed Amendments to Canada's Beer Standard of Identity

Study of Proposed Amendments to Canada’s Beer Standard of Identity Report prepared by Beer Canada’s Product Quality Committee October 2013 Authors Bill Andrews Ludwig Batista Manager, Brewing Quality National Technical Director Molson Coors Canada Sleeman Breweries Ltd. [email protected] [email protected] Ian Douglas (Committee Chair) Dr. Terry Dowhanick Global Director, Quality and Food Safety Quality Assurance and Product Integrity Manager Molson Coors Canada Labatt Breweries of Canada [email protected] [email protected] Anita Fuller Brad Hagan Quality Services Manager Director of Brewing Operations Great Western Brewing Company Labatt Breweries of Canada [email protected] [email protected] Peter Henneberry Dave Klaassen Adviser Vice President, Operations Moosehead Breweries Ltd. Sleeman Breweries Ltd. [email protected] [email protected] Russell Tabata Luke Harford Chief Operating Officer President Brick Brewing Co. Limited Beer Canada [email protected] [email protected] Luke Chapman Manager, Economic and Technical Affairs Beer Canada [email protected] 2 Table of Contents 1.0 Executive Summary ................................................................................................................................. 4 2.0 The Canadian Brewing Industry .............................................................................................................. 5 3.0 Historical Context of the Standard ......................................................................................................... -

Quick Report

Quick Report Average Quiz Score Total Responses Average Score Max Points Attainable Average Percentage Who was the first Prime Minister of Canada? 82 0.98 1 97.56% What is the most popular sport in Canada? 81 0.95 1 95.06% What two animals are featured on the Canadian Coat of Arms? 81 0.48 1 48.15% What is the largest City in Canada? 81 0.95 1 95.06% What is the national animal of Canada? 81 0.98 1 97.53% True or false- the origin of the name Canada is derived from the Huron-Iroquois word, Kanata, meaning a village or settlement? 81 0.96 1 96.30% What are french fries, gravy and cheese curds called? 81 0.99 1 98.77% Wood Buffalo National Park has the world's longest 81 0.79 1 79.01% What percentage of all the alcohol consumed in Canada is Beer? 80 0.50 1 50.00% How many countries are larger geographically than Canada? 80 0.65 1 65.00% What is the best selling beer in Canada? 77 0.21 1 20.78% What percentage of the world's fresh water is in Canada? 78 0.42 1 42.31% Who is the Head of State of Canada? 78 0.63 1 62.82% What was launched in 1936 to unify our sprawling Country? 77 0.38 1 37.66% True or False - Laura Secord warned the British of an impending attack on Canada by the Americans during the war of 1812 and because of this won t… 77 0.86 1 85.71% What is an Inukshuk? 77 0.95 1 94.81% 50% of the world's population of this animal live in Canada? 76 0.49 1 48.68% What is the most popular coffee chain in Canada? 76 0.97 1 97.37% What animal is on the Quarter? 76 0.64 1 64.47% What was the name of the system of safe passages and safe houses that allowed American slaves to escape to freedom in Canada? 76 0.87 1 86.84% Canada produces 80% of the world's supply of what? 75 0.77 1 77.33% What is slang for Canadian? 75 0.77 1 77.33% What is the most recent territory in Canada called? 75 0.92 1 92.00% Please enter in your contact information to be entered to win the Canada 150 prize packFirst name and phone # or email 68 0.00 0 0% Total: 82 16.38 23 71.21% Who was the first Prime Minister of Canada? Paul Martin John Diefenbaker John A. -

Wine & Cheese January 2020 Beer Club

Wine & Cheese January 2020 Beer Club From blustery conditions on Halloween night to unseasonably warm temperatures Christmas week, we can’t wait to see what January’s weather will hold. Needless to say, we anticipate much colder temps and with that we have two extraordinary “winter beers” for you to enjoy. The first selection is Winter Solstice Seasonal Ale from Anderson Valley Brewing Co in Boonville, California. What makes this place incredibly unique is that the original 10 barrel brewery was founded in 1987. At the time, they were one of only 20 craft breweries in the entire country and have long been considered one of the pioneers of the craft beer industry. By 1996, their 26-acre property housed a 100-barrel brewhouse, tasting room, beer garden, and is now home to the first 18-hole disc golf course. Their large solar panel array provides over 40% of their electrical needs, while 100% of the waste water is treated and used for the irrigation of their goat pastures and estate hop fields. In addition, the spent grain is given to local cows and spent hops are used as a natural fertilizer. In 2011, they established an exclusive partnership with Wild Turkey Bourbon, which brought about their Barrel Series of bourbon barrel-aged beers which have opened up unique opportunities in beer making. The second selection is Generator Doppelbock from Metropolitan Brewing in Chicago, Illinois. This type of beer is not only rich in flavor but rich in history as well. This is a sub-category of the bock style~ Doppelbocks are extra strong, rich, and weighty lagers characterized by an intense malty sweetness with a note of hop bitterness to balance the sweetness. -

Consumer Trends Wine, Beer and Spirits in Canada

MARKET INDICATOR REPORT | SEPTEMBER 2013 Consumer Trends Wine, Beer and Spirits in Canada Source: Planet Retail, 2012. Consumer Trends Wine, Beer and Spirits in Canada EXECUTIVE SUMMARY INSIDE THIS ISSUE Canada’s population, estimated at nearly 34.9 million in 2012, Executive Summary 2 has been gradually increasing and is expected to continue doing so in the near-term. Statistics Canada’s medium-growth estimate for Canada’s population in 2016 is nearly 36.5 million, Market Trends 3 with a medium-growth estimate for 2031 of almost 42.1 million. The number of households is also forecast to grow, while the Wine 4 unemployment rate will decrease. These factors are expected to boost the Canadian economy and benefit the C$36.8 billion alcoholic drink market. From 2011 to 2016, Canada’s economy Beer 8 is expected to continue growing with a compound annual growth rate (CAGR) between 2% and 3% (Euromonitor, 2012). Spirits 11 Canada’s provinces and territories vary significantly in geographic size and population, with Ontario being the largest 15 alcoholic beverages market in Canada. Provincial governments Distribution Channels determine the legal drinking age, which varies from 18 to 19 years of age, depending on the province or territory. Alcoholic New Product Launch 16 beverages must be distributed and sold through provincial liquor Analysis control boards, with some exceptions, such as in British Columbia (B.C.), Alberta and Quebec (AAFC, 2012). New Product Examples 17 Nationally, value sales of alcoholic drinks did well in 2011, with by Trend 4% growth, due to price increases and premium products such as wine, craft beer and certain types of spirits. -

L & F to Purchase Desert Eagle Dist

Modern Brewery Age Weekly E-Newsletter •Volume 58, Number 51• December 17, 2007 Miller Brewing Co. to test “lite” craft beers Miller Brewing Co. has announced that it will test the ‘‘Miller Lite Brewers Collection,’’ a portfolio of craft-style beers that are lower in calories and carbohydrates. Miller will test the collection in four markets— Minneapolis, Charlotte, San Diego and Baltimore, beginning in February 2008. The Brewers Collection will feature three beers—Blonde Ale, an Amber and a Wheat—each with fewer calories and carbs than a typical craft beer for that style. Miller Chief Marketing Officer Randy Ransom said “Miller is seeking to again establish a whole new category for the beer industry—craft-style-light. “The brewer who can provide a more refreshing and drinkable craft style can stake out a whole new niche in the market. (Continued on Page 10) L & F to purchase Desert Eagle Dist. Desert Eagle Distributing, which controls 76 percent of El Paso's beer market is sell- ing the company to L&F Distributors, a larger McAllen, TX-based, family-owned distributor, the El Paso Times reports. "The future of the business will be large, Jim Sloan, vice president, Star Brand Imports, pours the first draft beer from a rare keg of Affligem mega wholesalers. We either had to grow Noel tapped at the Ginger Man in New York City this past week. Star Brands is importing 61 20-liter the business or sell out. In our case we had kegs of the celebrated Belgian seasonal, to be sold on draft in select accounts in the New York, no acquisition possibilities," J. -

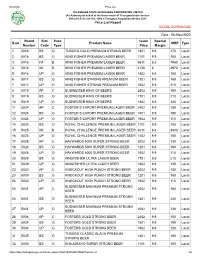

Price List Report EXCEL DOWNLOAD Date : 06-May-2020 S.No Brand

5/6/2020 Price List TELANGANA STATE BEVERAGES CORPORATION LIMITED (An Authority on behalf of the Government of Telangana Under Section 68A of A.P. Excise Act, 1968 )( Telangana Adaptation) Orders 2015 Price List Report EXCEL DOWNLOAD Date : 06-May-2020 Brand Size Pack Issue Special S.no Product Name MRP Type Number Code Type Price Margin 1 5006 BS G TUBORG GOLD PREMIUM STRONG BEER 1301 9.9 170 Local 2 5016 BS G KING FISHER PREMIUM LAGER BEER 1101 9.9 150 Local 3 5016 FK B KING FISHER PREMIUM LAGER BEER 6611 6.8 7960 Local 4 5016 KK B KING FISHER PREMIUM LAGER BEER 4120 6 4970 Local 5 5016 UP G KING FISHER PREMIUM LAGER BEER 1402 9.9 100 Local 6 5017 BS G KING FISHER STRONG PREMIUM BEER 1201 9.9 160 Local 7 5017 UP G KING FISHER STRONG PREMIUM BEER 1602 9.9 110 Local 8 5019 AP C BUDWEISER KING OF BEERS 2602 9.9 160 Local 9 5019 BS G BUDWEISER KING OF BEERS 1701 9.9 210 Local 10 5019 UP G BUDWEISER KING OF BEERS 1802 9.9 120 Local 11 5024 AP C FOSTER S EXPORT PREMIUM LAGER BEER 2402 9.9 150 Local 12 5024 BS G FOSTER S EXPORT PREMIUM LAGER BEER 1501 9.9 190 Local 13 5024 UP G FOSTER S EXPORT PREMIUM LAGER BEER 1602 9.9 110 Local 14 5025 BS G ROYAL CHALLENGE PREMIUM LAGER BEER 1101 9.9 150 Local 15 5025 KK B ROYAL CHALLENGE PREMIUM LAGER BEER 4011 6.8 4840 Local 16 5025 UP G ROYAL CHALLENGE PREMIUM LAGER BEER 1402 9.9 100 Local 17 5028 AP C HAYWARDS 5000 SUPER STRONG BEER 2002 9.9 130 Local 18 5028 BS G HAYWARDS 5000 SUPER STRONG BEER 1201 9.9 160 Local 19 5028 UP G HAYWARDS 5000 SUPER STRONG BEER 1602 9.9 110 Local 20 5029 BS G KINGFISHER -

Official Tasting Guide Saturday, March 5, 2016 EAA Airventure Museum

Official Tasting Guide Saturday, March 5, 2016 EAA AirVenture Museum Presented by Hosted by Arena Americas Ad 2 | 2016 Hops & Props Welcome Thank you for joining us at Hops & Props 2016! We hope you enjoy your evening of beer sampling in our world-class aviation museum. Thanks to Avery Brewing Company and Becket’s for hosting our VIP Dining Experience. We proudly welcome The Machine Shed as our general event caterer. Food stations are available near the Spirit of St. Louis exhibit, SpaceShipOne exhibit, and in the Eagle Hangar. Enjoy the music of the talented bands who join us tonight: > Brandon Beebe: Pioneer Airport Exhibit > Kyle Megna & the Monsoons: Eagle Hangar > Paddygrass: SpaceShipOne Exhibit Funds raised at this event support EAA’s efforts to supply free community programming throughout the year. Strawberry shortcake will be available in the Founders’ Wing at 8:45 p.m. Sponsored by Festival Foods. Please enjoy responsibly. Last call is at 9:45 p.m. A special thank you to the many wonderful volunteers and EAA staff members who help make this event happen. We couldn’t do it without you. Thank you to our sponsors SCEEN EAA AirVenture Museum, Oshkosh | 3 Breweries and Beverages 28 | 14 Hands Winery 7 | Bell’s Brewery Inc. 14 Hands Merlot Bell’s Two Hearted Ale 14 Hands Cabernet Sauvignon Bell’s Smitten Golden Rye Ale 14 Hands Chardonnay Bell’s Double Cream Stout 14 Hands Hot to Trot White Blend Bell’s Expedition Stout 1 | Alaskan Brewing Co. 8 | Bent Kettle Brewing LLC Alaskan Amber Insolence Double IPA Alaskan Icy Bay IPA Go Fasters Amber Rye Alaskan Hop Turn Alaskan Kicker 9 | Blue Moon Brewing Co. -

FROM FARM to GLASS: the Value of Beer in Canada

FROM FARM TO GLASS: The Value of Beer in Canada Glen Hodgson Chief Economist and Senior Vice President, The Conference Board of Canada November 5, 2013 conferenceboard.ca Economic Footprint of Beer. • Report investigates size and scope of beer economy. • Breweries are a large manufacturing industry, but there is more to the story. • Beer has a long supply chain and is retailed in stores and consumed in bars, and restaurants. • Therefore, beer’s contribution to Ca n adi an GDP i s m uch larger than brewers themselves. 2 Beer is the preferred alcohol choice. (volume of Canadian sales in absolute alcohol content; millions of litres) Spirits Wine Beer 140 120 100 80 60 40 20 0 Sources: Statistics Canada; The Conference Board of Canada. 3 Putting the industry into perspective. Canadian breweries industry: • Smaller than forestry and logging • About the same size as the postal service • Larger than wineries and distilleries, soft drink manufacturing, and many others. 4 Putting the industry into perspective. (2012 real GDP for selected Canadian industries; 2007 $ millions) Forestry and logging 3,729 Pharmaceutical and medicine manufacturing 3,451 Postal service 3,179 Breweries 3,166 Radio and television broadcasting 3,081 Dairy product manufacturing 2, 866 Coal mining 1,666 Soft drink and ice manufacturing 1,168 Fishing, hntinghunting, and trapping 1, 127 Wineries and distilleries 889 Sources: Statistics Canada; The Conference Board of Canada. 5 What is the “Beer Economy”? It’s more than just breweries… When you drink a bottle of beer, you support: 1. Direct Impacts: The brewing industry 2. Supply Chain Impacts: 6 What is the “Beer Economy”? It’s more than just breweries… 3. -

Crc - Liquor List

2701 W Howard Street Chicago, IL 60645-1303 PH: 773.465.3900 Fax: 773.465.6632 Rabbi Sholem Fishbane Kashruth Administrator Items listed as "Recommended" do not require a kosher symbol unless they are marked with a star (*) This list is updated regularly and should be considered accurate until December 31, 2013 cRc - Liquor List Bar Stock Items Bar Stock Items Bar equipment (strainers, shot measures, blenders, stir Other rods, shakers, etc.) used with non-kosher products Olives - Green should be properly cleaned and/or kashered prior to Require Certification use with kosher products. Onions - Pearl Canned or jarred require certification Recommended Coco Lopez OU* Beer Daily's OU* All unflavored beers with no additives are acceptable, OU* Holland House even without Kosher certification. This applies to both Jamaica John cRc* American and imported beers, light, dark and non- Jero OK* alcoholic beers. Mr & Mrs T OU or OK* Many breweries produce specialty brews that have Rose's - Grenadine OU* additives; please check the label and do not assume Rose's - Lime OU* that all varieties are acceptable. Furthermore, beers known to be produced at microbreweries, pub K* Tabasco - Hot Pepper Sauce breweries, or craft breweries require certification. Underberg - Herb Mix for Underberg OU* Natural Herb Bitters Recommended Other 800 - Ice Beer OU Bitters Anheuser-Busch - Redbridge Gluten Require Certification Free Coconut Milk Aspen Edge - Lager OU Requires Certification Blue Moon - Belgian White Ale OU* Cream of Coconut Blue Moon - Full Moon Winter Ale -

View Presentation

WORLD BREWING CONGRESS 2016 World Brewing Congress August 13-17, 2016 Prospective demand for malting barley and malt quality for the global brewing industry Sheraton Downtown Denver 159 Peter Watts1, Dr. Yueshu Li1 and Dr. Jessica Yu2 Denver, CO 80202, U.S.A. 1. Canadian Malting Barley Technical Centre, Winnipeg, Manitoba, Canada R3C 3G7 2. Tsingtao Brewery Co. Ltd, Qingdao, China 266100 Introduction China Beer Market Evolving Quality Requirements Rapid changes in the world brewing industry including the boom in craft brewing, diversification in In addition to international brewing groups such as Carlsberg and AB-InBev, China Resource Snow Brewery, Tsingtao Brewery, and Beijing Yangjing Beer are dominant Rising beer production in China and the rapid development of craft brewing in the US beer brand/style as well as changing ownership present both challenges and opportunities for the players in China accounting for 71% of beer output. Increasingly Chinese beer manufacturers are strengthening their brand positioning. In 2014 China Resources Snow are driving increased demand for malting barley and malt, and are also shifting quality malting barley industry. In this presentation, trends in global malting and brewing sectors, Breweries produced 107 million hectolitres of Snow beer making it the world’s largest beer brand at 5.4% of the global market. Its total volume is higher than the requirements. In China, brewers are demanding barley with higher grain protein and specifically in China and the United States, and changing quality requirements for malting barley combined volume of Budweiser (4.6 billion liters) and Budlight (5.0 billion liters). Together with Tsingtao Brewery and Beijing Yangjing Beer, these three Chinese brewers very high enzyme potential to compensate for large adjunct incorporation.