Shaping Commercial Radio's Future

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Main Ridge Township Protection Plan Inmerncy E Ge Dial 000 (Tty 106)

Making Victoria FireReady Main Ridge Township Protection Plan In EMERGENCY dial 000 (TTY 106) . Do not call Triple Zero for information or advice. Calling Triple Zero unnecessarily may put others who are in a genuine emergency situation at risk. PROTECTYOUR PROTECTYOUR FAMILY LIFE Victorian Bushfire Information Line (VBIL): 1800 240 667 Emergency Contact Information Tuning into your emergency broadcaster and CFA website on days of high fire danger ratings is the most reliable way of staying informed. Mains power may be unavailable, or fail, during fire and emergencies – keep a battery powered radio available. Emergency Broadcasters: Sky News TV, ABC 774 AM, FOX FM, Triple M, Gold 104.3 FM, Classic Rock 91.5, Nova 100.3, 3AW, Magic 1278, MTR 1377, FOX FM, 1116 SEN, Mix 101.1 FM - Melbourne Road closures: 13 11 70 www.vicroads.vic.gov.au Park closures – Parks Victoria hotline: 13 19 63 State Forest closures (DSE): 13 61 86 School closures (DEECD): 1800 809 834 24 Hour Wildlife Emergency: 13 000 WILDLIFE or 1300 094 535 24 Hour NURSE-ON-CALL: 1300 60 60 24 Bushfire Information: CFA website: www.cfa.vic.gov.au Why Main Ridge is at risk of bushfire Follow CFA on Twitter: www.twitter.com/cfa_updates Join the CFA Facebook page: www.facebook.com/cfavic Fire Authorities have assessed Main Ridge as having a VERY HIGH to EXTREME bushfire risk. Local DSE Website (Planned burning): www.dse.vic.gov.au residents and visitors should be prepared for fire and have a plan for when the Fire Danger Rating is Further Information SEVERE, EXTREME or CODE RED. -

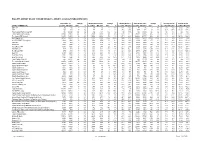

RAJAR Comparative Report Q3 2003

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2003/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share LOCAL COMMERCIAL Last Pub W3 2003 000's % Last Pub W3 2003 000's % Last Pub W3 2003 Last Pub W3 2003 000's % Last Pub W3 2003 Last Pub W3 2003 Bath FM 82 82 0 0% 16 15 -1 -6% 19% 19% 88 95 7 8% 5.6 6.3 5.5% 5.8% 2BR 203 203 0 0% 77 78 1 1% 38% 38% 799 826 27 3% 10.3 10.6 18.3% 18.8% Total Capital Radio Group UK n/p 48384 n/a n/a n/p 7756 n/a n/a n/p 16% n/p 71888 n/a n/a n/p 9.3 n/p 6.8% Total Capital Radio Group 28097 28081 -16 0% 7600 7630 30 0% 27% 27% 70870 71265 395 1% 9.3 9.3 11.8% 11.9% The Capital FM Network 18951 18951 0 0% 5090 5016 -74 -1% 27% 26% 42282 41373 -909 -2% 8.3 8.2 10.3% 10.2% 95.8 Capital FM 10344 10343 -1 0% 2624 2269 -355 -14% 25% 22% 18991 15613 -3378 -18% 7.2 6.9 8.9% 7.0% 96.4 FM BRMB Birmingham 2004 2004 0 0% 588 555 -33 -6% 29% 28% 4339 4456 117 3% 7.4 8.0 9.8% 10.2% FOX FM 558 559 1 0% 208 214 6 3% 37% 38% 2289 2354 65 3% 11.0 11.0 19.2% 19.5% Invicta FM 1075 1075 0 0% 425 438 13 3% 39% 41% 4634 4984 350 8% 10.9 11.4 17.0% 18.3% 103.2 Power FM 1066 1066 0 0% 299 277 -22 -7% 28% 26% 2624 2326 -298 -11% 8.8 8.4 10.2% 9.7% Southern FM 949 949 0 0% 356 332 -24 -7% 38% 35% 4218 3679 -539 -13% 11.9 11.1 17.4% 16.3% Red Dragon FM 889 889 0 0% 301 311 10 3% 34% 35% 2789 2570 -219 -8% 9.3 8.3 13.3% 12.8% Beat 106 2599 2599 0 0% 415 447 32 8% 16% 17% 2976 3490 514 17% 7.2 7.8 5.8% 7.0% Beat 106 (East) 1101 1101 0 0% 199 198 -1 -1% 18% -

Replacing Digital Terrestrial Television with Internet Protocol?

This is a repository copy of The short future of public broadcasting: Replacing digital terrestrial television with internet protocol?. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/94851/ Version: Accepted Version Article: Ala-Fossi, M and Lax, S orcid.org/0000-0003-3469-1594 (2016) The short future of public broadcasting: Replacing digital terrestrial television with internet protocol? International Communication Gazette, 78 (4). pp. 365-382. ISSN 1748-0485 https://doi.org/10.1177/1748048516632171 Reuse Unless indicated otherwise, fulltext items are protected by copyright with all rights reserved. The copyright exception in section 29 of the Copyright, Designs and Patents Act 1988 allows the making of a single copy solely for the purpose of non-commercial research or private study within the limits of fair dealing. The publisher or other rights-holder may allow further reproduction and re-use of this version - refer to the White Rose Research Online record for this item. Where records identify the publisher as the copyright holder, users can verify any specific terms of use on the publisher’s website. Takedown If you consider content in White Rose Research Online to be in breach of UK law, please notify us by emailing [email protected] including the URL of the record and the reason for the withdrawal request. [email protected] https://eprints.whiterose.ac.uk/ The Short Future of Public Broadcasting: Replacing DTT with IP? Marko Ala-Fossi & Stephen Lax School of Communication, School of Media and Communication Media and Theatre (CMT) University of Leeds 33014 University of Tampere Leeds LS2 9JT Finland UK [email protected] [email protected] Keywords: Public broadcasting, terrestrial television, switch-off, internet protocol, convergence, universal service, data traffic, spectrum scarcity, capacity crunch. -

AM / FM / DAB / XM Tuner

ENGLISH FRANÇAIS Owner’s Manual Owner’s ESPAÑOL ® ITALIANO AM / FM / DAB / XM Tuner /XM /DAB /FM AM M4 DEUTSCH NEDERLANDS SVENSKA РУССКИЙ IMPORTANT SAFETY INSTRUCTIONS ENGLISH 1. Read instructions - All the safety and operating instructions should be NOTE TO CATV SYSTEM INSTALLER read before the product is operated. This reminder is provided to call the CATV system installer’s attention to Section 820-40 of 2. Retain instructions - The safety and operating instructions should be the NEC which provides guidelines for proper grounding and, in particular, specifies that retained for future reference. the cable ground shall be connected to the grounding system of the building, as close 3. Heed Warnings - All warnings on the product and in the operating to the point of cable entry as practical. instructions should be adhered to. 4. Follow Instructions - All operating and use instructions should be FRANÇAIS followed. 5. Cleaning - Unplug this product from the wall outlet before cleaning. Do not use liquid cleaners or aerosol cleaners. Use a damp cloth for cleaning. 6. Attachments - Do not use attachments not recommended by the product manufacturer as they may cause hazards. 7. Water and Moisture - Do not use this product near water-for example, near a bath tub, wash bowl, kitchen sink, or laundry tub; in a wet basement; or near a swimming pool; and the like. ESPAÑOL 8. Accessories - Do not place this product on an unstable cart, stand, tripod, bracket, or table. The product may fall, causing serious injury to a child or adult and serious damage to the product. Use only with a cart, stand, tripod, bracket, or table recommended by the manufacturer, or sold with the product. -

The BBC's Use of Spectrum

The BBC’s Efficient and Effective use of Spectrum Review by Deloitte & Touche LLP commissioned by the BBC Trust’s Finance and Strategy Committee BBC’s Trust Response to the Deloitte & Touche LLPValue for Money study It is the responsibility of the BBC Trust,under the As the report acknowledges the BBC’s focus since Royal Charter,to ensure that Value for Money is the launch of Freeview on maximising the reach achieved by the BBC through its spending of the of the service, the robustness of the signal and licence fee. the picture quality has supported the development In order to fulfil this responsibility,the Trust and success of the digital terrestrial television commissions and publishes a series of independent (DTT) platform. Freeview is now established as the Value for Money reviews each year after discussing most popular digital TV platform. its programme with the Comptroller and Auditor This has led to increased demand for capacity General – the head of the National Audit Office as the BBC and other broadcasters develop (NAO).The reviews are undertaken by the NAO aspirations for new services such as high definition or other external agencies. television. Since capacity on the platform is finite, This study,commissioned by the Trust’s Finance the opportunity costs of spectrum use are high. and Strategy Committee on behalf of the Trust and The BBC must now change its focus from building undertaken by Deloitte & Touche LLP (“Deloitte”), the DTT platform to ensuring that it uses its looks at how efficiently and effectively the BBC spectrum capacity as efficiently as possible and uses the spectrum available to it, and provides provides maximum Value for Money to licence insight into the future challenges and opportunities payers.The BBC Executive affirms this position facing the BBC in the use of the spectrum. -

Anti-Stress Garden Coming to RHS Chelsea Flower Show

Spring 2019 News from the University of Surrey for Guildford residents SURREY.AC.UK UNIVERSITYOFSURREY @ UNIOFSURREYCPE Page 4 - Surrey graduate Page 7 - Could your car Page 10 - Iain Sinclair, Page 11 - Shrek workshop meets Michelle Obama park itself? Writer-in-Residence supports local group Guildford Residents’ Survey 2019 The University is calling on residents of Guildford to take part in our fifth annual residents’ survey. Since its launch in 2015, the Guildford Residents’ Survey has provided the Right: an artist’s impression of the garden design University with Main image: the garden will feature irises, flowers celebrated valuable insight, for their wellbeing properties. Credit: Getty Images feedback and ideas to build greater links with our home town. Last year, more than Anti-stress garden coming to 1,300 local residents took part, with many entering the annual RHS Chelsea Flower Show prize draw to win The University has partnered with Silent Pool Gin to present an anti-stress garden at the one of five £100 RHS Chelsea Flower Show, transporting visitors to the Surrey Hills using scents and sounds. cash prizes. We want to hear The exciting collaboration with Albury-based He will be using sensors to detect and from you – to gin brand Silent Pool, acclaimed Surrey-based capture changing electrical signals directly complete the survey garden designer David Neale and Dutch from the plants, enabling the garden to visit: surrey.ac.uk/ horticultural pioneers Plant-e will explore govern and interact with the soundscape. guildfordsurvey plant technologies that encourage wellbeing. Professor Murphy said: “This truly exciting The survey closes Through their combined expertise, the team collaboration brings to life the hidden power on 1 July 2019. -

We've Come a Long Way!

Spotlight The halow project’s magazine Issue 1 in June 2008 with the appointment of Project Director, We’ve come a Yvonne Hignell - by November of that year, Yvonne had produced a business plan, halow had moved into an office in Quarry Street, Guildford and held an official launch party. long way! In January of 2009, a dedicated social activities group was established for halow young people. By March of the same Over seven years since halow was formed, we bring year halow had secured its first tranche of much needed supporters new and old a sense of just where halow has come funding from Surrey Short Breaks and by June, funding was from, where it is now, and where the Guildford-based charity obtained from the LDD Fund (Learning Disability Development) is heading... to set up the Building Futures Programme and the charity’s first The inspiration for halow came from Harriet, Amber, Laura, website was launched. That summer also saw the first major Oliver and William. Their parents, all friends, came together at activity, with 36 young people and volunteers attending the the beginning of 2006 concerned with the prospect for their WOMAD festival in Malmesbury, Wiltshire. children’s future and others like them. Passionate that these In September 2009, the Building Futures Programme young people should lead positive and happy lives, near their commenced, shortly followed in October with the registration own friends and families in Surrey, the parents established the of halow care, a social enterprise, which runs alongside the halow project. halow project. Through this, our Buddy service was launched The first major turning point in the charity’s growth story was for our young people. -

Changing Stations

1 CHANGING STATIONS FULL INDEX 100 Top Tunes 190 2GZ Junior Country Service Club 128 1029 Hot Tomato 170, 432 2HD 30, 81, 120–1, 162, 178, 182, 190, 192, 106.9 Hill FM 92, 428 247, 258, 295, 352, 364, 370, 378, 423 2HD Radio Players 213 2AD 163, 259, 425, 568 2KM 251, 323, 426, 431 2AY 127, 205, 423 2KO 30, 81, 90, 120, 132, 176, 227, 255, 264, 2BE 9, 169, 423 266, 342, 366, 424 2BH 92, 146, 177, 201, 425 2KY 18, 37, 54, 133, 135, 140, 154, 168, 189, 2BL 6, 203, 323, 345, 385 198–9, 216, 221, 224, 232, 238, 247, 250–1, 2BS 6, 302–3, 364, 426 267, 274, 291, 295, 297–8, 302, 311, 316, 345, 2CA 25, 29, 60, 87, 89, 129, 146, 197, 245, 277, 354–7, 359–65, 370, 378, 385, 390, 399, 401– 295, 358, 370, 377, 424 2, 406, 412, 423 2CA Night Owls’ Club 2KY Swing Club 250 2CBA FM 197, 198 2LM 257, 423 2CC 74, 87, 98, 197, 205, 237, 403, 427 2LT 302, 427 2CH 16, 19, 21, 24, 29, 59, 110, 122, 124, 130, 2MBS-FM 75 136, 141, 144, 150, 156–7, 163, 168, 176–7, 2MG 268, 317, 403, 426 182, 184–7, 189, 192, 195–8, 200, 236, 238, 2MO 259, 318, 424 247, 253, 260, 263–4, 270, 274, 277, 286, 288, 2MW 121, 239, 426 319, 327, 358, 389, 411, 424 2NM 170, 426 2CHY 96 2NZ 68, 425 2Day-FM 84, 85, 89, 94, 113, 193, 240–1, 243– 2NZ Dramatic Club 217 4, 278, 281, 403, 412–13, 428, 433–6 2OO 74, 428 2DU 136, 179, 403, 425 2PK 403, 426 2FC 291–2, 355, 385 2QN 76–7, 256, 425 2GB 9–10, 14, 18, 29, 30–2, 49–50, 55–7, 59, 2RE 259, 427 61, 68–9, 84, 87, 95, 102–3, 107–8, 110–12, 2RG 142, 158, 262, 425 114–15, 120–2, 124–7, 129, 133, 136, 139–41, 2SM 54, 79, 84–5, 103, 119, 124, -

Pocketbook for You, in Any Print Style: Including Updated and Filtered Data, However You Want It

Hello Since 1994, Media UK - www.mediauk.com - has contained a full media directory. We now contain media news from over 50 sources, RAJAR and playlist information, the industry's widest selection of radio jobs, and much more - and it's all free. From our directory, we're proud to be able to produce a new edition of the Radio Pocket Book. We've based this on the Radio Authority version that was available when we launched 17 years ago. We hope you find it useful. Enjoy this return of an old favourite: and set mediauk.com on your browser favourites list. James Cridland Managing Director Media UK First published in Great Britain in September 2011 Copyright © 1994-2011 Not At All Bad Ltd. All Rights Reserved. mediauk.com/terms This edition produced October 18, 2011 Set in Book Antiqua Printed on dead trees Published by Not At All Bad Ltd (t/a Media UK) Registered in England, No 6312072 Registered Office (not for correspondence): 96a Curtain Road, London EC2A 3AA 020 7100 1811 [email protected] @mediauk www.mediauk.com Foreword In 1975, when I was 13, I wrote to the IBA to ask for a copy of their latest publication grandly titled Transmitting stations: a Pocket Guide. The year before I had listened with excitement to the launch of our local commercial station, Liverpool's Radio City, and wanted to find out what other stations I might be able to pick up. In those days the Guide covered TV as well as radio, which could only manage to fill two pages – but then there were only 19 “ILR” stations. -

BBC Radio Scotland’S Delivery of the BBC’S Public Purposes

BBC Nations Radio Review BBC Nations Radio Review Quantitative audience research assessing BBC Radio Scotland’s delivery of the BBC’s Public Purposes Prepared for September 20 2011 Prepared by Kantar Media: Trevor Vagg, Sara Reid and Julia Harrison. Ref: 45110564. © Kantar Media. Contact: 020 7656 5500 All rights reserved www.kantarmedia.com www.kantarmedia.com reserved P a g e | 2 Contents 1. Introduction .................................................................................................................................... 2 1.1 Objectives.................................................................................................................................... 3 1.2 Methodology ............................................................................................................................... 3 1.3 Explanation of Public Purposes and performance gaps.............................................................. 4 2. Executive summary ......................................................................................................................... 6 3. Overall performance measures for BBC Radio Scotland............................................................... 10 3.1 Overall impression of BBC Radio Scotland ................................................................................ 10 3.2 Likelihood to miss BBC Radio Scotland ..................................................................................... 12 3.3 Perceived value for money of BBC Radio Scotland .................................................................. -

Digital One’S Response to the Ofcom Consultation “Future Pricing of Spectrum Used for Terrestrial Broadcasting”

Digital One’s Response to the Ofcom Consultation “Future pricing of spectrum used for terrestrial broadcasting” 1. Digital One operates the UK’s only national commercial DAB digital radio multiplex. Its shareholders are GCap Media (63%) and Arqiva (37%). Digital One’s transmission network (which is operated by Arqiva) is the world’s biggest DAB digital radio network with coverage well in excess of 85% of the British population. Digital One’s multiplex broadcasts: - the three INRs (Classic FM, Virgin Radio and talkSPORT); - four digital-only national stations (Capital Life, Core, Oneword and Planet Rock) with a further station being launched in the next few months; - TV channels and an Electronic Programme Guide broadcast as part of BT Movio. Digital One is a leading stakeholder in the UK’s Digital Radio Development Bureau and the WorldDAB Forum (which is responsible for the DAB digital radio standard and works to coordinate the international roll-out of Eureka 147 based technologies). 2. Digital One is licensed under the 1996 Broadcasting Act, and has licence obligations which help deliver public policy benefits. These limit Digital One’s ability to use the spectrum it has been allocated in the most efficient manner (in economic terms). For example: - the obligation to operate a transmitter network which delivers high population coverage; - the obligation (at the direction of the Secretary of State for the Department of Culture, Media and Sport) to carry the three INRs and to offer each INR an amount of capacity dictated by the regulator; -

Paisley FM Community Radio Licence Application Form

Paisley FM community radio licence application form 1. Station Name Guidance Notes What is the proposed station name? This is the name you expect to use to identify the station on air. Paisley FM ‘Radio for Renfrewshire’ 2. Community to be served Guidance Notes Define the community or communities you are It is a legislative requirement that a service is intended proposing to serve. Drawing from various sources of primarily to serve one or more communities (whether or data (e.g. from the Office of Population, Census and not it also serves other members of the public) and we Survey) and in relation to your proposed coverage need to understand who comprises that community or area, please determine the size of the population communities. The target community will also be concerned and the make-up of the population as a specified in the licence, if this application is successful. whole, along with any relevant socio-economic The legislation defines a ‘community’ as: people who live information that would support your application. or work or undergo education or training in a particular (Please tell us the sources of the information you area or locality, or people who have one or more provide.) interests or characteristics in common. Answer in fewer than 300 words: Paisley FM intends to serve the communities as published in the invitation to apply, namely: Paisley, Renfrew and Johnstone and surroundings parts of Renfrewshire. It is the intention to serve the entire population of the Renfrewshire Council local government authority area. The 2015 population for Renfrewshire is 174,560 with the main town being Paisley with a total population of 74,640.