Hsbc Bank Egypt S.A.E

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pdf (895.63 K)

Egyptian Journal of Aquatic Biology & Fisheries Zoology Department, Faculty of Science, Ain Shams University, Cairo, Egypt. ISSN 1110 -6131 Vol. 21(1): 11-23 (2017) www.ejabf.js.iknito.com Assessment of shoreline stability and solidity for future investment plans at Ras El-Bar Resort (E GYPT ). Walaa A.Ali 1; Mona F.Kaiser 1; Suzan Kholief 2 and Maysara El-Tahan 3 1- Geology Department, Faculty of Science, Suez Canal University, Ismailia, Egypt. 2- National Institute of Oceanography and Fisheries (NIOF), Alexandria, Egypt. 3- Faculty of Engineering, Alexandria University, Egypt. ARTICLE INFO ABSTRACT Article History: Ras El-Bar resort located in the northeastern Egyptian Nile Delta Received: Nov.2016 coast includes a very active sandy beach coastline, which extends roughly Accepted: Jan. 2017 12 km west of Damietta Nile branch. Erosion along the coast of Ras El- Available online: May 2017 Bar resort has been mitigated by constructing a series of coastal _______________ engineering structures that include jetties, groins, seawalls and detached breakwaters. The Project of protecting Ras El-bar resort started early in Keywords : 1941 and ended in 2010 and aimed to decrease the continuous erosion Ras El-Bar and protecting the investments at the Ras El-bar resort. Studying shore Landsat 8 line change at this region is important in making the development plan of Egyptsat Erdas Imagine protection works along the Egyptian northeastern coast by evaluating the DSAS effect of constructed detached breakwaters on shoreline. The purpose of GIS this paper is to calculate the change detection rate of Ras El-bar shoreline Shoreline at the last 15 years (2000-2015) and to evaluate the effect of basaltic stones and dollos blocks that constructed to re-protect the western jetty and fanar area by mitigating beach erosion. -

I'm Here Implementation—El Obour, Greater Cairo, Egypt

I’m Here Implementation—El Obour, Greater Cairo, Egypt Process. Results. Response planning. Drafted by: Omar J. Robles | Sr. Program Officer | Women’s Refugee Commission With key inputs from: Rachael Corbishley | Emergency Program Officer | Save the Children Egypt Summary | Key Steps and Outputs In January 2015, Save the Children Egypt (SC Egypt), with support from the Women’s Refugee Commission (WRC), implemented the I’m Here Approach in El Obour, Egypt. The approach and complementary field tools are designed to help humanitarian actors identify, protect, serve and engage adolescent girls from the start of emergency operations or of program design for girls. SC Egypt is committed to ensuring that its soon-to-open child centered space (CCS) program in El Obour is responsive to adolescent girls. SC Egypt aims to make its child-centered services “accessible for girls and for excluded children …, tailoring activities to meet their specific needs and capacities.”1 Specifically in El Obour, SC Egypt has chosen to adopt a mobile CCS model, which extends programming from a “CCS hub into existing community spaces” such as schools, gardens and community centers.2 I’m Here implementation in El Obour was the first in an urban refugee setting. The process, results and response planning outlined in this report are designed to inform how SC Egypt can fulfill its expressed commitment to not overlook adolescent girls – to account for their context-specific profile, vulnerabilities and capacities. Key steps and outputs. With UNHCR-approved access to registration information for Syrian refugees who live in Greater Cairo, the WRC and SC Egypt modified the I’m Here Approach and tools to safely translate this unique access into actionable info for programmatic decision-making. -

Encouraging Peaceful Co-Existence Through a Multi-Faceted Approach

Encouraging Peaceful Co-Existence Through a Multi-Faceted Approach Implementing Agency: Plan International Egypt Partners: Syria Al Gad Relief Foundation in Greater Cairo and Islamic Charity Complex Association in Damietta Donor: European Commission- Humanitarian Aid and Civil Protection Location: Damietta and Qalubia (Greater Cairo) Target Population: Syrian and Egyptian students ages 0 – 18 years Implementation Period: June 1, 2016 - May 31, 2018 Number of Beneficiaries: 3600 children and 60 adults 1200 children, 0 – 5 years 1900 children, 6 – 12 years 500 children, 13 – 18 years 60 teachers and school management Background The violence in Syria has seen over 2.2 million child refugees fleeing to other countries, and 6 million children in need of assistance, including 2.8 million displaced, inside Syria. UNHCR reports that circa 51,000 Syrian child refugees registered, 1,600 of them are separated, all in need of assistance. The initial findings of an on-going UNHCR-led survey show that between 20 and 30 percent of Syrian refugee children in Egypt are out of school, compared to 12 percent in 2014. Damietta and Qalubia are two of the governorates with high numbers of Syrian refugees and limited humanitarian support. In response, Plan International (Plan) set up an office in Damietta to help Syrian children to fulfill their right to education and integrate in host communities. Plan’s Qalubia sub-office has been supporting public schools to accept and cater for the needs of refugee children. In this action, Plan is working with the Ministry of Education to integrate 7,590 Syrian refugee children aged 0-18 years in six communities of the Damietta and Qalubia governorates, promoting a safe and socially inclusive environment and supporting their smooth integration in host communities. -

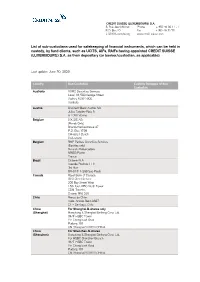

List of Sub-Custodians Used for Safekeeping of Financial Instruments

CREDIT SUISSE (LUXEMBOURG) S.A. 5, Rue Jean Monnet Phone + 352 46 00 11 - 1 P.O. Box 40 Fax + 352 46 32 70 L-2010 Luxembourg www.credit-suisse.com List of sub-custodians used for safekeeping of financial instruments, which can be held in custody, by fund clients, such as UCITS, AIFs, RAIFs having appointed CREDIT SUISSE (LUXEMBOURG) S.A. as their depositary (or banker/custodian, as applicable) Last update: June 30, 2020 Country Sub-Custodian Custody Delegate of Sub- Custodian Australia HSBC Securities Services Level 13, 580 George Street Sydney NSW 2000 Australia Austria UniCredit Bank Austria AG Julius Tandler-Platz 3 A-1090 Vienna Belgium SIX SIS AG (Bonds Only) Brandschenkestrasse 47 P.O. Box 1758 CH-8021 Zurich Switzerland Belgium BNP Paribas Securities Services (Equities only) 9 rue du Débarcadère 93500 Pantin France Brazil Citibank N.A. Avenida Paulista 1111 3rd floor BR-01311-290 Sao Paulo Canada Royal Bank of Canada GSS Client Service 200 Bay Street West 15th floor, RBC North Tower CDN-Toronto, Ontario M5J 2J5 Chile Banco de Chile Avda. Andrés Bello 2687 CL – Santiago, Chile China For Shanghai-B-shares only (Shanghai) Hongkong & Shanghai Banking Corp. Ltd. 34/F HSBC Tower Yin Cheng East Road Pudong 101 CN-Shanghai 200120 CHINA China For Shenzhen-B-shares (Shenzhen) Hongkong & Shanghai Banking Corp. Ltd. For HSBC Shenzhen Branch 34/F HSBC Tower Yin Cheng East Road Pudong 101 CN-Shanghai 200120 CHINA Colombia Cititrust Colombia S.A. Sociedad Fiduciaria Carrera 9A No. 99-02 First Floor Santa Fé de Bogotá D.C. -

Importers Address Telephone Fax Make(S)

Importers Address Telephone Fax Make(s) Alpha Auto trading Josef tito st. Cairo +20 02-2940330 +20 02-2940600 Citroën cars Amal Foreign Trade Heliopolis, Cairo 11Fakhry Pasha St +20 02-2581847 +20 02-2580573 Lada Artoc Auto - Skoda 2, Aisha Al Taimouria st. Garden city Cairo +20 02-7944172 +20 02-7951622 Skoda Asia Motors Egypt 69, El Nasr Road, New Maadi, Cairo +20 02-5168223 +20 02-5168225 Asia Motors Atic/Arab Trading & 21 Talaat Harb St. Cairo +20 02-3907897 +20 02-3907897 Renault CV Insurance Center of 4, Wadi Al nil st. Mohandessin Cairo +20 02-3034775 +20 02-3468300 Peugeot Development & commerce - CDC - Wagih Abaza Chrysler Egypt 154 Orouba St. Heliopolis Cairo +20 02-4151872 +20 02-4151841 Chrysler Daewoo Corp Dokki, Giza- 18 El-Sawra St. Cairo +20 02-3370015 +20 02-3486381 Daewoo Daimler Chrysler Sofitel Tower, 28 th floor Conish el Nil, +20 02-5263800 +20 02-5263600 Mercedes, Egypt Maadi, Cairo Chrysler Egypt Engineering Shubra, Cairo-11 Terral el-ismailia +20 02-4266484 +20 02-4266485 Piaggio Industries Egyptan Automotive 15, Mourad St. Giza +20 02-5728774 +20 02-5733134 VW, Audi Egyptian Int'l Heliopolice Cairo Ismailia Desert Rd: Airport +20 02-2986582 +20 02-2986593 Jaguar Trading & Tourism / Rolls Royce Jaguar Egypt Ferrari El-Alamia ( Hashim Km 22 First of Cairo - Ismailia road +20 02-2817000 +20 02-5168225 Brouda Kancil bus ) Engineering Daher, Cairo 11 Orman +20 02-5890414 +20 02-5890412 Seat Automotive / SMG Porsche Engineering 89, Tereat Al Zomor Ard Al Lewa +20 02-3255363 +20 02-3255377 Musso, Seat , Automotive Co / Mohandessin Giza Porsche SMG Engineering for Cairo 21/24 Emad El-Din St. -

Obour Land OBOUR LAND for Food Industries Mosque Ofsultanhassan -Cairo W BP802AR 350P

Food Sector Obour City - Cairo, Egypt Shrinkwrapper BP802AR 350P hen speaking about Egypt we immediately think of an ancient Wcivilization filled with art, culture, magic and majesty closely related to one of the most enigmatic and recognized cities in the world, the capital of the state and one of the principal centers of development in the old world. Being the most populous city in the entire African continent, Cairo is For Food Industries among the most important industrial and commercial points in the Middle East, and a big development center for the cotton, silk, glass and food products industries which, thanks to the commitment of its people, is constantly growing. The food industry is largely responsible for this development, having the objective of positioning quality products on the market that meet the needs of end customers, improving production processes and giving priority to investments in cutting-edge technologies that allow to achieve this end. A clear example of this commitment is represented by the Obour Land Company which, among its numerous investments, has recently acquired 7 Smipack machines model BP802AR 350P. Mosque of Sultan Hassan - Cairo OBOUR LAND 2 | Obour Land Obour Land | 3 Egyptian Museum - Cairo eing the capital of one of the most important countries in Africa, with a population growth of around 2% per year(1), Cairo has one of the fastest growing markets for food Band agricultural products in the world. The growth city in constant growth of the agri-food and manufacturing sector in Egypt is CAIRO associated -

Egyptian Natural Gas Industry Development

Egyptian Natural Gas Industry Development By Dr. Hamed Korkor Chairman Assistant Egyptian Natural Gas Holding Company EGAS United Nations – Economic Commission for Europe Working Party on Gas 17th annual Meeting Geneva, Switzerland January 23-24, 2007 Egyptian Natural Gas Industry History EarlyEarly GasGas Discoveries:Discoveries: 19671967 FirstFirst GasGas Production:Production:19751975 NaturalNatural GasGas ShareShare ofof HydrocarbonsHydrocarbons EnergyEnergy ProductionProduction (2005/2006)(2005/2006) Natural Gas Oil 54% 46 % Total = 71 Million Tons 26°00E 28°00E30°00E 32°00E 34°00E MEDITERRANEAN N.E. MED DEEPWATER SEA SHELL W. MEDITERRANEAN WDDM EDDM . BG IEOC 32°00N bp BALTIM N BALTIM NE BALTIM E MED GAS N.ALEX SETHDENISE SET -PLIOI ROSETTA RAS ELBARR TUNA N BARDAWIL . bp IEOC bp BALTIM E BG MED GAS P. FOUAD N.ABU QIR N.IDKU NW HA'PY KAROUS MATRUH GEOGE BALTIM S DEMIATTA PETROBEL RAS EL HEKMA A /QIR/A QIR W MED GAS SHELL TEMSAH ON/OFFSHORE SHELL MANZALAPETROTTEMSAH APACHE EGPC EL WASTANI TAO ABU MADI W CENTURION NIDOCO RESTRICTED SHELL RASKANAYES KAMOSE AREA APACHE Restricted EL QARAA UMBARKA OBAIYED WEST MEDITERRANEAN Area NIDOCO KHALDA BAPETCO APACHE ALEXANDRIA N.ALEX ABU MADI MATRUH EL bp EGPC APACHE bp QANTARA KHEPRI/SETHOS TAREK HAMRA SIDI IEOC KHALDA KRIER ELQANTARA KHALDA KHALDA W.MED ELQANTARA KHALDA APACHE EL MANSOURA N. ALAMEINAKIK MERLON MELIHA NALPETCO KHALDA OFFSET AGIBA APACHE KALABSHA KHALDA/ KHALDA WEST / SALLAM CAIRO KHALDA KHALDA GIZA 0 100 km Up Stream Activities (Agreements) APACHE / KHALDA CENTURION IEOC / PETROBEL -

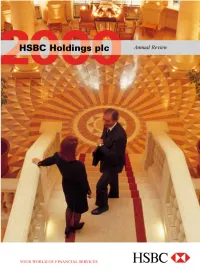

Annual Review Show Major International Network Comprises Some 6,500 Offices in Developments in the HSBC Group Last Year

The HSBC Group Headquartered in London, HSBC Holdings plc is one Illustrative Theme of the largest banking and financial services Managing for Value organisations in the world. The HSBC Group’s The photographs in this Annual Review show major international network comprises some 6,500 offices in developments in the HSBC Group last year. They illustrate 79 countries and territories in Europe, the Asia- the progress we have made in implementing our five-year strategic plan, ‘Managing for Value’, launched in 1998. Pacific region, the Americas, the Middle East and Africa. The picture spreads are grouped around these initiatives. They reflect the breadth and scope of our operations, and With listings on the London, Hong Kong, New our international character. York and Paris stock exchanges, shares in HSBC Building our ‘wealth management’ (personal financial Holdings plc are held by around 190,000 shareholders services) business is a cornerstone of our plan. It was seen in in some 100 countries and territories. The shares are our acquisitions during 2000, notably CCF, and in the launch traded on the New York Stock Exchange in the form of our first truly global service for personal customers, HSBC Premier. To provide essential back office support, we of American Depositary Receipts. invested more resources in the global processing of banking operations. We focused on e-business to bring customers a Through a global network linked by advanced range of new services via new delivery channels, such as technology, including a rapidly growing e-commerce internet and mobile phone banking. We joined forces with capability, HSBC provides a comprehensive range of Merrill Lynch in a joint venture offering online investment and banking services. -

Assessment Impact of the Damietta Harbour (Egypt) and Its Deep Navigation Channel on Adjacent Shorelines

Journal of Integrated Coastal Zone Management (2020) 20(4): 265-281 © 2020 APRH ISSN 1646-8872 DOI 10.5894/rgci-n338 url: https://www.aprh.pt/rgci/rgci-n338.html ASSESSMENT IMPACT OF THE DAMIETTA HARBOUR (EGYPT) AND ITS DEEP NAVIGATION CHANNEL ON ADJACENT SHORELINES Mohsen M. Ezzeldin1, Osami S. Rageh2, Mahmoud E. Saad3 @ ABSTRACT: Deep navigation channels have a great impact on adjacent beaches and crucial economic effects because of periodic dredging operations. The navigation channel of the Damietta harbour is considered a clear example of the sedimentation problem and deeply affects the Northeastern shoreline of the Nile Delta in Egypt. The aim of the present study is to monitor shoreline using remote sensing techniques to evaluate the effect of Damietta harbour and its navigation channel on the shoreline for the last 45 years. Also, the selected period was divided into two periods to illustrate the effect of man-made interventions on the shoreline. Shorelines were extracted from satellite images and then the Digital Shoreline Analysis System (DSAS) was used to estimate accurate rates of shoreline changes and predict future shorelines evolution of 2030, 2040, 2050 and 2060. The Damietta harbour created an accretion area in the western side with an average rate of 2.13 m year-1. On the contrary, the shoreline in the eastern side of the harbour retreated by 92 m on average over the last 45 years. So, it is considered one of the main hazard areas along the Northeastern shoreline of the Nile Delta that needs a sustainable solution. Moreover, a detached breakwaters system is predicted to provide shore stabilization at the eastern side as the implemented one at Ras El-Bar beach. -

Directory of Development Organizations

EDITION 2010 VOLUME I.A / AFRICA DIRECTORY OF DEVELOPMENT ORGANIZATIONS GUIDE TO INTERNATIONAL ORGANIZATIONS, GOVERNMENTS, PRIVATE SECTOR DEVELOPMENT AGENCIES, CIVIL SOCIETY, UNIVERSITIES, GRANTMAKERS, BANKS, MICROFINANCE INSTITUTIONS AND DEVELOPMENT CONSULTING FIRMS Resource Guide to Development Organizations and the Internet Introduction Welcome to the directory of development organizations 2010, Volume I: Africa The directory of development organizations, listing 63.350 development organizations, has been prepared to facilitate international cooperation and knowledge sharing in development work, both among civil society organizations, research institutions, governments and the private sector. The directory aims to promote interaction and active partnerships among key development organisations in civil society, including NGOs, trade unions, faith-based organizations, indigenous peoples movements, foundations and research centres. In creating opportunities for dialogue with governments and private sector, civil society organizations are helping to amplify the voices of the poorest people in the decisions that affect their lives, improve development effectiveness and sustainability and hold governments and policymakers publicly accountable. In particular, the directory is intended to provide a comprehensive source of reference for development practitioners, researchers, donor employees, and policymakers who are committed to good governance, sustainable development and poverty reduction, through: the financial sector and microfinance, -

"Clouds in Egypt's Sky"

"Clouds in Egypt's Sky" Sexual Harassment: from Verbal Harassment to Rape A Sociological Study Scientific revision by Prepared by Dr. Aliyaa Shoukry Rasha Mohammad Hassan Professor of Anthropological Sociology ECWR Researcher Supervisor Nehad Abul Komsan ECWR Chair 1 CONCLUSIONS The issue of sexual harassment has become less taboo recently in the Egyptian media and within academic circles, and has even become a part of daily discourse among women in Egyptian society, regardless of social or economic status or political belief. In the past, women were afraid to talk about sexual harassment and considered discussing it culturally taboo. With the problem worsening, we have found that the way ahead is to encourage dialogue about this problem and to try to search for solutions. Sexual harassment has become an overwhelming and very real problem experienced by all women in Egyptian society, often on a daily basis, in public places such as markets, public transportation and the streets, as well as in private places such as educational institutions, sports clubs, and the workplace. The research component of the Egyptian Center for Women’s Rights’ (ECWR) work concerning the phenomenon of sexual harassment has progressed in three phases. In 2005 we received and documented over 100 complaints of women subjected to sexual harassment – women across all different age groups and socio-economic classes. These women spoke to us about the seriousness of the problem and the extent of their personal and private suffering. During the second phase of our research, in order to investigate the issue further and discover if the problem of sexual harassment was an isolated phenomenon or a pervasive problem faced by the majority of women in Egypt, we conducted an exploratory study surveying over 2,800 Egyptian women. -

Anthropogenic Enhancement of Egypt's Mediterranean Fishery

Anthropogenic enhancement of Egypt’s Mediterranean fishery Autumn J. Oczkowskia,1, Scott W. Nixona, Stephen L. Grangera, Abdel-Fattah M. El-Sayedb, and Richard A. McKinneyc aGraduate School of Oceanography, University of Rhode Island, Narragansett, RI 02882; bOceanography Department, Faculty of Science, Alexandria University, Alexandria, Egypt; and cUnited States Environmental Protection Agency, Atlantic Ecology Division, Narragansett, RI 02882 Communicated by Peter Vitousek, Stanford University, Stanford, CA, December 10, 2008 (received for review September 8, 2008) The highly productive coastal Mediterranean fishery off the Nile River delta collapsed after the completion of the Aswan High Dam in 1965. But the fishery has been recovering dramatically since the mid-1980s, coincident with large increases in fertilizer application and sewage discharge in Egypt. We use stable isotopes of nitrogen (␦15N) to demonstrate that 60%–100% of the current fishery production may be from primary production stimulated by nutri- ents from fertilizer and sewage runoff. Although the establish- ment of the dam put Egypt in an ideal position to observe the impact of rapid increases in nutrient loading on coastal productiv- ity in an extremely oligotrophic sea, the Egyptian situation is not unique. Such anthropogenically enhanced fisheries also may occur along the northern rim of the Mediterranean and offshore of some rapidly developing tropical countries, where nutrient concentra- tions in the coastal waters were previously very low. fisheries ͉ Nile delta ͉ nutrient enrichment ͉ stable isotope n contrast to many of the world’s fisheries, which are in serious Idecline (1, 2), Egypt’s Mediterranean fishery offshore of the Nile River delta has been expanding dramatically in recent decades and at rates higher than can be explained by fishing Fig.