April 2015 M&A and Investment Summary 245245 232232 184184

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chris Pereira Chief Risk Officer and Vice President, Strategy, GE

Chris Pereira Chief Risk Officer and Vice President, Strategy, GE Appointed September 2020. Chris serves as General Electric Company's Chief Risk Officer and Vice President, Strategy. In this role, Chris is responsible for evaluating risk and opportunities across the enterprise and establishing company- level governance frameworks and operational initiatives for strategy and risk. Chris joined GE in 2007 as Senior Corporate, Securities & Finance Counsel. He went on to become Vice President, Deputy General Counsel & Corporate Secretary, GE Capital, where he oversaw Board Risk Committee governance for GE Capital during Federal Reserve oversight; Vice President, General Counsel, Business Innovations, in which role he oversaw the Global Law & Policy teams for GE Current, GE Lighting, GE Ventures and GE Shared Services; Vice President, Chief Corporate, Securities & Finance Counsel, General Electric Company, responsible for global securities law, board governance, corporate finance, corporate law and antitrust; and Vice President, Chief Risk Officer and Chief Corporate Counsel, General Electric Company, in which role he assumed additional responsibility for GE’s overall risk governance and operationalizing the company-level risk oversight and governance framework. Chris joined GE from Exelixis, a California biotech company, where he served as Vice President of Legal Affairs and Corporate Secretary. Prior to that he practiced law at Sullivan & Cromwell in New York and Palo Alto. Chris is a CFA charter holder and holds law degrees from the University of Chicago and the University of Vienna, Austria. He is also an Adjunct Professor at Columbia Law School. . -

2018 FINTECH100 Leading Global Fintech Innovators 2017 FINTECH100 ������� ������ ������� ��������

2018 FINTECH100 Leading Global Fintech Innovators 2017 FINTECH100 Leadin loba Fintec nnovators 1 1 2016 2017 Fintech100 Report FINTECH100 Leadin loba Fintec nnovators Company #00 1 | Fintech Innovators 2016 1 2015 Fintech100 Report FINTECH 100 Leading Global “ Fintech Innovators Report 2015 Company Description At a Glance Tag Line Located Year Founded Key People Website Specialisation Staff Enabler or Disruptor Key Investors Ownership Size User Engagement $ $ $ $ $ The 100 Leading Fintech Innovators Report 2016 Fintech100 Report The 50 Best Fintech Innovators Report 2014 Fintech100 Report 2 About the List The Fintech100 is a collaborative effort between H2 Ventures and KPMG. In its fifth year, the Fintech100 uncovers and evaluates the most innovative Fintech companies globally. The Fintech100 comprises a ‘Top 50’ and an ‘Emerging 50’ and highlights those companies globally that are taking advantage of technology and driving disruption within the financial services industry. A judging panel comprised of senior partners from H2 Ventures and KPMG has decided the final composition of the Fintech100 list. H2 Ventures H2 Ventures is a global thought leader in fintech venture capital investment. Founded by brothers Ben and Toby Heap, and based in Sydney, Australia, it invests alongside entrepreneurs and other investors in early stage fintech ventures. H2 Ventures is the manager of the H2 Accelerator – Australia’s only dedicated fintech accelerator – and operates out of Sydney’s dynamic Startup Hub. Twitter @H2_Ventures LinkedIn H2 Ventures Facebook H2 Ventures KPMG Global Fintech The financial services industry is transforming with the emergence of innovative, new products, channels and business models. This wave of disruption is primarily driven by evolving customer expectations, digitalisation, as well as continued regulatory and cost pressures. -

View Whitepaper

INFRAREPORT Top M&A Trends in Infrastructure Software EXECUTIVE SUMMARY 4 1 EVOLUTION OF CLOUD INFRASTRUCTURE 7 1.1 Size of the Prize 7 1.2 The Evolution of the Infrastructure (Public) Cloud Market and Technology 7 1.2.1 Original 2006 Public Cloud - Hardware as a Service 8 1.2.2 2016 - 2010 - Platform as a Service 9 1.2.3 2016 - 2019 - Containers as a Service 10 1.2.4 Container Orchestration 11 1.2.5 Standardization of Container Orchestration 11 1.2.6 Hybrid Cloud & Multi-Cloud 12 1.2.7 Edge Computing and 5G 12 1.2.8 APIs, Cloud Components and AI 13 1.2.9 Service Mesh 14 1.2.10 Serverless 15 1.2.11 Zero Code 15 1.2.12 Cloud as a Service 16 2 STATE OF THE MARKET 18 2.1 Investment Trend Summary -Summary of Funding Activity in Cloud Infrastructure 18 3 MARKET FOCUS – TRENDS & COMPANIES 20 3.1 Cloud Providers Provide Enhanced Security, Including AI/ML and Zero Trust Security 20 3.2 Cloud Management and Cost Containment Becomes a Challenge for Customers 21 3.3 The Container Market is Just Starting to Heat Up 23 3.4 Kubernetes 24 3.5 APIs Have Become the Dominant Information Sharing Paradigm 27 3.6 DevOps is the Answer to Increasing Competition From Emerging Digital Disruptors. 30 3.7 Serverless 32 3.8 Zero Code 38 3.9 Hybrid, Multi and Edge Clouds 43 4 LARGE PUBLIC/PRIVATE ACQUIRERS 57 4.1 Amazon Web Services | Private Company Profile 57 4.2 Cloudera (NYS: CLDR) | Public Company Profile 59 4.3 Hortonworks | Private Company Profile 61 Infrastructure Software Report l Woodside Capital Partners l Confidential l October 2020 Page | 2 INFRAREPORT -

Innovalue #Payments

Innovalue #payments INSIGHT | OPINION Vol 7 • Q2 2014 Apple Pay: Taking a bite out of payments Christina Cordes, the start (usually merchants who already Associate accepted NFC). Furthermore, Apple announced significant bank partnerships Kalle Dunkel, with Bank of America, Capital One Bank, Associate Chase, Citi,Wells Fargo and others which together represent about 83% of the US credit Mirko Krauel, card purchase volume. Principal For now, Apple Pay is a solution for the US market only. In Europe, Apple will face more Following months and weeks of extensive speculation and leaked rumours, the new "Apple Pay is not revolutionary. It is evolutionary." iPhone 6 with its feature Apple Pay has finally been presented on 9th of September. button. That’s it. The innovation and lifestyle complex challenges. First of all, Europe is more To be frank, Apple Pay is not revolutionary. oriented Apple user base will push “their” solu- fragmented and has several markets with It is evolutionary as Apple uses the existing tion, especially in the US market where the only a low penetration rate of NFC enabled payment ecosystem and partners with estab- company has a market share of around 40%. POS terminals - at least for now. Furthermore, lished players. Also, none of the ingredients of However, a good mobile payment solu- Apple has a lower market share in a lot of Apple Pay are new but this seems to be the tion on the customer side is basically worthless European countries compared to the US. first recipe that people like and want. Obvi- if there are no POS acceptance points on the Finally, the banking landscape consists of ously, this is due to a multitude of reasons, merchant side. -

General Electric Co Company Update on June 26, 2018 / 12:30PM

Client Id: 77 THOMSON REUTERS STREETEVENTS EDITED TRANSCRIPT GE - General Electric Co Company Update EVENT DATE/TIME: JUNE 26, 2018 / 12:30PM GMT OVERVIEW: Co. provided an update on its fundamental changes. THOMSON REUTERS STREETEVENTS | www.streetevents.com | Contact Us ©2018 Thomson Reuters. All rights reserved. Republication or redistribution of Thomson Reuters content, including by framing or similar means, is prohibited without the prior written consent of Thomson Reuters. 'Thomson Reuters' and the Thomson Reuters logo are registered trademarks of Thomson Reuters and its affiliated companies. Client Id: 77 JUNE 26, 2018 / 12:30PM, GE - General Electric Co Company Update CORPORATE PARTICIPANTS Jamie S. Miller General Electric Company - Senior VP & CFO John L. Flannery General Electric Company - Chairman & CEO Kieran P. Murphy GE Healthcare Limited - Former President & CEO of Life Sciences Matthew G. Cribbins General Electric Company - VP of Investor Communications CONFERENCE CALL PARTICIPANTS Andrew Alec Kaplowitz Citigroup Inc, Research Division - MD and U.S. Industrial Sector Head Andrew Burris Obin BofA Merrill Lynch, Research Division - MD Charles Stephen Tusa JP Morgan Chase & Co, Research Division - MD Christopher D. Glynn Oppenheimer & Co. Inc., Research Division - MD and Senior Analyst Jeffrey Todd Sprague Vertical Research Partners, LLC - Founder and Managing Partner Julian C.H. Mitchell Barclays Bank PLC, Research Division - Research Analyst Nigel Edward Coe Wolfe Research, LLC - MD & Senior Research Analyst Scott Reed Davis Melius Research LLC - Founding Partner, Chairman, CEO & Research Analyst of Multi-Industry Research Steven Eric Winoker UBS Investment Bank, Research Division - MD & Industrials Analyst PRESENTATION Operator Good day, ladies and gentlemen, and welcome to the General Electric Company Update. -

Who's Behind ICE: Tech and Data Companies Fueling Deportations

Who’s Behind ICE? The Tech Companies Fueling Deportations Tech is transforming immigration enforcement. As advocates have known for some time, the immigration and criminal justice systems have powerful allies in Silicon Valley and Congress, with technology companies playing an increasingly central role in facilitating the expansion and acceleration of arrests, detentions, and deportations. What is less known outside of Silicon Valley is the long history of the technology industry’s “revolving door” relationship with federal agencies, how the technology industry and its products and services are now actually circumventing city- and state-level protections for vulnerable communities, and what we can do to expose and hold these actors accountable. Mijente, the National Immigration Project, and the Immigrant Defense Project — immigration and Latinx-focused organizations working at the intersection of new technology, policing, and immigration — commissioned Empower LLC to undertake critical research about the multi-layered technology infrastructure behind the accelerated and expansive immigration enforcement we’re seeing today, and the companies that are behind it. The report opens a window into the Department of Homeland Security’s (DHS) plans for immigration policing through a scheme of tech and database policing, the mass scale and scope of the tech-based systems, the contracts that support it, and the connections between Washington, D.C., and Silicon Valley. It surveys and investigates the key contracts that technology companies have with DHS, particularly within Immigration and Customs Enforcement (ICE), and their success in signing new contracts through intensive and expensive lobbying. Targeting Immigrants is Big Business Immigrant communities and overpoliced communities now face unprecedented levels of surveillance, detention and deportation under President Trump, Attorney General Jeff Sessions, DHS, and its sub-agency ICE. -

The Silicon Valley Mafia

The Silicon Valley Mafia From Computer Chips to Gun Clips. From the Whore House To The White House. How Tech Billionaire Oligarchs Make Al Capone Look Tame. By Alex Lund, Audrey Finis and Connie Britley with acknowledgement to International Consortium of Investigative Journalists VOLUME ONE OF A TEN VOLUME SET Madicore Press First Edition Revision 4.2– Updates to follow A Public Wiki Report To The U.S. Congress and the FBI 1 Table of Contents INTRODUCTION.....................................................................................................................................7 So A Blogger Walks Into A Bar… | TechCrunch........................................................................8 TECH BOSS CONFESSES: “I PUT DONALD TRUMP IN THE WHITE HOUSE IN ORDER TO WIPE OUT SILICON VALLEY’S HORRIFIC CORRUPTION!”.........................................................11 What Is A Cartel?: A Definition...............................................................................................................13 Origin.......................................................................................................................................................13 How Does A Crony Political Payola Kickback Scam Work?..................................................................14 In practice.................................................................................................................................................14 John Doerr................................................................................................................................................16 -

Hybrid Solutions

Hybrid Solutions gepower.com/hybrid There’s a way to do it better... “fnd it. THOMAS EDISON Inventor, businessman and founder of the General Electric Company trends solutions enablers 08 Hybrid Solutions: Defned 20 GE's Hybrid Portfolio 40 GE Store hy·brid/’hī brid/ Noun 12 Hybrid Solutions: Value 22 Building Blocks 42 GE Energy Financial 1. BIOLOGY: the ofspring of two plants or • Battery Energy Storage Services animals of diferent species or varieties, 14 Energy Storage 101 Solutions (BESS) such as a mule. 44 GE Energy Consulting 2. a thing made by combining two diferent 16 Battery Storage 101 • Industrial Internet elements; a mixture. Control System 45 GE Ventures Adjective 26 Hybrid Systems 1. of mixed character; composed of 46 Ecomagination mixed parts. • Wind Integrated Solar Energy (WiSE*) 48 GE Beliefs Hybrids have been commonplace in • Pumped Storage (PSP) 49 GE’s Commitment the plant and animal kingdoms for • Simple Cycle millennia. Diferent species or varieties of Gas Turbine + Battery organisms have been crossbred because • Combined Cycle they have desirable characteristics not Gas Turbine (CCGT) + found or inconsistently present in the Battery parent individuals or populations. • Gas Engine + Renewables + Battery • Containerized Packages *Trademark of the General Electric Company trends tan·ge·lo /'tanj lō/ Noun A bright red-orange hybrid of a tangerine and grapefruit with an unmistakable sweetness countered by a tart aftertaste (courtesy of its grapefruit ancestor). Tangelos are seedless, easy to peel and have a thick skin similar to that of oranges. 6 / HYBRID SOLUTIONS / www.gepower.com/hybrid www.gepower.com/hybrid / HYBRID SOLUTIONS / 7 trends trends Hybrid solutions: defned Each form of power generation has its pros and cons. -

GE 2015 INTEGRATED SUMMARY REPORT About the Integrated Summary Report “The Integrated Summary Report Shows Investors GE Through the Lens of Management.”

GE 2015 INTEGRATED GE 2015 INTEGRATED SUMMARY REPORT GE 2015 Integrated Report About the Integrated Summary Report “The integrated summary report shows investors GE through the lens of management.” “Public company reporting has become so complicated that what matters to investors can get lost. Our priority is to provide meaningful information that all investors can readily access. For investors to make investment and voting decisions, we don’t believe that more information is necessarily better. Instead, we’ve challenged ourselves to provide better information. Over the past several years, we have already been enhancing our reporting in response to feedback from investors, and they have told us how much they like it. This year, we are taking it even further with our new Integrated Summary Report.” JEFFREY R. IMMELT Chairman of the Board & Chief Executive Officer, GE March 14, 2016 Contents Chairman’s Letter 3 Strategy & Results 29 Our Businesses 35 WHERE YOU CAN FIND MORE Portfolio & Capital Allocation 38 INFORMATION • Annual Report Margins 40 www.ge.com/annualreport • Proxy Statement Financials 42 www.ge.com/proxy • Sustainability Report Risk 51 www.ge.com/sustainability Governance 52 FORWARD-LOOKING STATEMENTS Compensation 57 Some of the information we provide in this document is forward-looking and therefore could change over time to reflect changes in Audit 60 the environment in which GE competes. See Forward-Looking Statements on page 65 for Shareowner Proposals 61 more information. 62 Sustainability NON-GAAP FINANCIAL MEASURES Some of the financial measures we provide Annual Meeting 64 in this document, including measures that exclude Alstom, may be considered to be non-GAAP financial measures. -

Introducing Kauffman Fellows Class 21

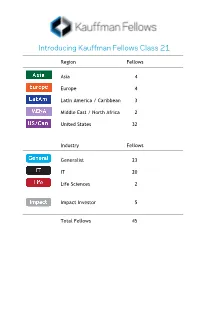

Introducing Kauffman Fellows Class 21 Region Fellows Asia 4 Europe 4 Latin America / Caribbean 3 Middle East / North Africa 2 United States 32 Industry Fellows Generalist 23 IT 20 Life Sciences 2 Impact Investor 5 Total Fellows 45 NICOLAS BERMAN Partner KaszeK Ventures [email protected] +54 (11) 4786-3426 www.kaszek.com Professional Nik is a Partner at KaszeK Ventures, a venture capital firm investing in high-impact technology-based companies whose main focus is Latin America. In addition to capital deployment, the firm actively supports its portfolio companies through value-added strategic guidance and hands-on operational help, leveraging its partners’ successful entrepreneurial backgrounds and extensive network. Before joining KaszeK Ventures, Nik worked for 13 years at MercadoLibre, where he was VP of Advertising, VP of Marketing, Marketing Manager, and covered several roles in the company’s technology and product areas. He led several key projects in search, business intelligence (BI), user experience (UX), and SEO, and created the company’s affiliate program, which is the largest in Latin America. During all these years, Nik has also been a very active advisor and angel investor in the Latin American startup scene. Prior to MercadoLibre, Nik was a Commercial Manager at LG Electronics, where he received the “LG Global Hit Idea” award for his innovative thinking. He currently sits on the boards of several technology companies, including DogHero, Contabilizei, and Pitzi. Education/Personal Nik earned a bachelor’s degree in business administration from the University of Buenos Aires (Argentina). He served as President of AMDIA (Argentina’s direct marketing association), received an Echo Award by the DMA in 2000, is currently an active mentor for Endeavor Argentina, and sits in the board of Educatina, a company focused on democratizing high-quality education across Latin America. -

General Assembly Expands Its Footprint at ABS Partners Real Estate’S 915 Broadway

October 06, 2014 General Assembly Expands its Footprint at ABS Partners Real Estate’s 915 Broadway Tech, Business and Design Educator Not Occupies 40,158 Square Feet New York-based full-service commercial real estate firm ABS Partners Real Estate, LLC announced today that tech, business and design educator General Assembly has expanded its presence at 915 Broadway. Located on the corner of 21St Street and Broadway, the 20-story, 225,000-square- footoffice and adult educational facility headquarters serves both entrepreneurs and corporate clients. General Assembly now boasts full-floor office space on floors four, three and most recently two, as well as a newly redesigned 21st Street lobby midway between Fifth Avenue and Broadway. Each floor consists of approximately 13,386 rentable square feet. Established in early 2011 as an innovative community in New York City for entrepreneurs and startup companies, General Assembly is an educational institution that transforms thinkers into creators through education in technology, business and design at nine campuses across four continents.“ We are thrilled to continue and grow our relationship with General Assembly at 915 Broadway,” said Alex Kaskel, director at ABS Partners Real Estate. “The firm is an exceptional example of the overall tenor of the neighborhood, which has become synonymous with tech and TAMI (technology, advertising, media and information) tenants, including MasterCard, Tumblr, Twitter, Facebook, Buzzfeed, Yelp, Union Square Ventures and Sony.” In fact, 915 Broadway is currently -

May 2015 M&A and Investment Summary 245245 232232 184184

BlueBlue 0 0 7979 133133 122122 141141 181181 178178 186186 213213 211211 216216 233233 234234 235235 245245 OrangeOrange 241241 184184 0 0 May 2015 M&A and Investment Summary 245245 232232 184184 GreyGrey 138138 138138 138138 203203 203203 203203 221221 221221 Expertise. Commitment. Results. 221221 Table of Contents Blue 0 79 133 122 141 181 178 186 213 1 Overview of Monthly M&A and Investment Activity 3 211 216 233 2 Monthly M&A and Investment Activity by Industry Segment 9 234 235 245 Orange 3 Additional Monthly M&A and Investment Activity Data 39 241 184 0 4 About Petsky Prunier 52 245 232 184 Grey 138 138 138 203 203 203 221 221 221 Securities offered through Petsky Prunier Securities, LLC, member of FINRA. This M&A and Investment Summary has been prepared by and is being distributed in the United States by Petsky Prunier, a broker dealer registered with the U.S. SEC and a member of FINRA. Petsky Prunier is not affiliated with Altium Capital Ltd, but has partnered with Altium to expand its international presence. Altium has not prepared or verified the information in this Summary. Persons in the United States should contact Petsky Prunier for further information or services. This M&A and Investment Summary is not being distributed by Altium Capital Ltd in the United States and Altium Capital Ltd is not offering any services to persons in the United States. 2 | M&A and Investment Summary May 2015 M&A and Investment Summary for All Segments Blue 0 79 133 122 Transaction Distribution 141 181 .