DOE Solar Energy Technologies Program FY 2007 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2015-SVTC-Solar-Scorecard.Pdf

A PROJECT OF THE SILICON VALLEY TOXICS COALITION 2015 SOLAR SCORECARD ‘‘ www.solarscorecard.com ‘‘ SVTC’s Vision The Silicon Valley Toxics Coalition (SVTC) believes that we still have time to ensure that the PV sector is safe The PV industry’s rapid growth makes for the environment, workers, and communities. SVTC it critical that all solar companies envisions a safe and sustainable solar PV industry that: maintain the highest sustainability standards. 1) Takes responsibility for the environmental and health impacts of its products throughout their life- cycles, including adherence to a mandatory policy for ‘‘The Purpose responsible recycling. The Scorecard is a resource for consumers, institutional purchasers, investors, installers, and anyone who wants 2) Implements and monitors equitable environmental to purchase PV modules from responsible product and labor standards throughout product supply chains. stewards. The Scorecard reveals how companies perform on SVTC’s sustainability and social justice benchmarks 3) Pursues innovative approaches to reducing and to ensure that the PV manufacturers protect workers, work towards eliminating toxic chemicals in PV mod- communities, and the environment. The PV industry’s ule manufacturing. continued growth makes it critical to take action now to reduce the use of toxic chemicals, develop responsible For over three decades, SVTC has been a leader in recycling systems, and protect workers throughout glob- encouraging electronics manufacturers to take lifecycle al PV supply chains. Many PV companies want to pro- responsibility for their products. This includes protecting duce truly clean and green energy systems and are taking workers from toxic exposure and preventing hazardous steps to implement more sustainable practices. -

DOE Solar Energy Technologies Program FY 2005 Annual

DOE Solar Energy Technologies Program Cover Photos (clockwise from lower right): On August 8, 2005, President George W. Bush visited the National Solar Thermal Test Facility at Sandia National Laboratories as part of his signing of the Energy Bill. R.J. Montoya Photo National Renewable Energy Laboratory researchers use a computer-controlled data acquisition system at the laboratory’s Outdoor Test Facility to characterize the performance and reliability of PV cells and modules. Jim Yost, PIX14094 A Cornell University student cleans the solar-powered rooftop of his team’s entry in preparation for the 2005 Solar Decathlon competition in Washington, D.C. Stefano Paltera/Solar Decathlon Global Solar Energy, a member of the Thin Film PV Partnership, produces PV material by depositing CIGS (copper indium gallium diselenide) on a lightweight, flexible polymide substrate in roll form. Global Solar Energy, PIX13419 The DOE Solar Energy Technologies Program Raymond A. Sutula, Manager, DOE Solar Energy Technologies Program The Solar Energy Technologies Program, within the U.S. Department of Energy's Office of Energy Efficiency and Renewable Energy (EERE), is responsible for developing solar energy technologies that can convert sunlight to useful energy and make that energy available to satisfy a significant portion of our nation's energy needs in a cost-effective way. The Solar Program supports research and development that addresses a wide range of applications, including on- site electricity generation, thermal energy for space heating and hot water, and large-scale power production. This is a great time to be involved with solar energy. Photovoltaic (PV) systems are being installed in the United States and around the world in unprecedented quantities. -

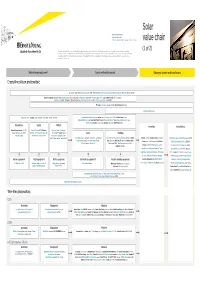

Lsoar Value Chain Value Chain

Solar Private companies in black Public companies in blue Followed by the founding date of companies less than 15 years old value chain (1 of 2) This value chain publication contains information gathered and summarized mainly from Lux Research and a variety of other public sources that we believe to be accurate at the time of ppggyublication. The information is for general guidance only and not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization nor Lux Research can accept responsibility for loss to any person relying on this publication. Materials and equipment Components and products Balance of system and installations Crystalline silicon photovoltaic GCL Silicon, China (2006); LDK Solar, China (2005); MEMC, US; Renewable Energy Corporation ASA, Norway; SolarWorld AG, Germany (1998) Bosch Solar Energy, Germany (2000); Canadian Solar, Canada/China (2001); Jinko Solar, China (2006); Kyocera, Japan; Sanyo, Japan; SCHOTT Solar, Germany (2002); Solarfun, China (2004); Tianwei New Energy Holdings Co., China; Trina Solar, China (1997); Yingli Green Energy, China (1998); BP Solar, US; Conergy, Germany (1998); Eging Photovoltaic, China SOLON, Germany (1997) Daqo Group, China; M. Setek, Japan; ReneSola, China (2003); Wacker, Germany Hyundai Heavy Industries,,; Korea; Isofoton,,p Spain ; JA Solar, China (();2005); LG Solar Power,,; Korea; Mitsubishi Electric, Japan; Moser Baer Photo Voltaic, India (2005); Motech, Taiwan; Samsung -

Solar Is Driving a Global Shift in Electricity Markets

SOLAR IS DRIVING A GLOBAL SHIFT IN ELECTRICITY MARKETS Rapid Cost Deflation and Broad Gains in Scale May 2018 Tim Buckley, Director of Energy Finance Studies, Australasia ([email protected]) and Kashish Shah, Research Associate ([email protected]) Table of Contents Executive Summary ......................................................................................................... 2 1. World’s Largest Operational Utility-Scale Solar Projects ........................................... 4 1.1 World’s Largest Utility-Scale Solar Projects Under Construction ............................ 8 1.2 India’s Largest Utility-Scale Solar Projects Under Development .......................... 13 2. World’s Largest Concentrated Solar Power Projects ............................................... 18 3. Floating Solar Projects ................................................................................................ 23 4. Rooftop Solar Projects ................................................................................................ 27 5. Solar PV With Storage ................................................................................................. 31 6. Corporate PPAs .......................................................................................................... 39 7. Top Renewable Energy Utilities ................................................................................. 44 8. Top Solar Module Manufacturers .............................................................................. 49 Conclusion ..................................................................................................................... -

Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support

U.S. Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support Michaela D. Platzer Specialist in Industrial Organization and Business January 27, 2015 Congressional Research Service 7-5700 www.crs.gov R42509 U.S. Solar PV Manufacturing: Industry Trends, Global Competition, Federal Support Summary Every President since Richard Nixon has sought to increase U.S. energy supply diversity. Job creation and the development of a domestic renewable energy manufacturing base have joined national security and environmental concerns as reasons for promoting the manufacturing of solar power equipment in the United States. The federal government maintains a variety of tax credits and targeted research and development programs to encourage the solar manufacturing sector, and state-level mandates that utilities obtain specified percentages of their electricity from renewable sources have bolstered demand for large solar projects. The most widely used solar technology involves photovoltaic (PV) solar modules, which draw on semiconducting materials to convert sunlight into electricity. By year-end 2013, the total number of grid-connected PV systems nationwide reached more than 445,000. Domestic demand is met both by imports and by about 75 U.S. manufacturing facilities employing upwards of 30,000 U.S. workers in 2014. Production is clustered in a few states including California, Ohio, Oregon, Texas, and Washington. Domestic PV manufacturers operate in a dynamic, volatile, and highly competitive global market now dominated by Chinese and Taiwanese companies. China alone accounted for nearly 70% of total solar module production in 2013. Some PV manufacturers have expanded their operations beyond China to places like Malaysia, the Philippines, and Mexico. -

Expanding the Photovoltaic Supply Chain in the United States: Opportunities and Challenges

Expanding the Photovoltaic Supply Chain in the United States: Opportunities and Challenges Brittany L. Smith and Robert Margolis NREL is a national laboratory of the U.S. Department of Energy Technical Report Office of Energy Efficiency & Renewable Energy NREL/TP-6A20-73363 Operated by the Alliance for Sustainable Energy, LLC July 2019 This report is available at no cost from the National Renewable Energy Laboratory (NREL) at www.nrel.gov/publications. Contract No. DE-AC36-08GO28308 Expanding the Photovoltaic Supply Chain in the United States: Opportunities and Challenges Brittany L. Smith and Robert Margolis Suggested Citation Smith, Brittany L., and Robert Margolis. (2019). Expanding the Photovoltaic Supply Chain in the United States: Opportunities and Challenges. Golden, CO: National Renewable Energy Laboratory. NREL/TP-6A20-73363. https://www.nrel.gov/docs/fy19osti/73363.pdf. NREL is a national laboratory of the U.S. Department of Energy Technical Report Office of Energy Efficiency & Renewable Energy NREL/TP-6A20-73363 Operated by the Alliance for Sustainable Energy, LLC July 2019 This report is available at no cost from the National Renewable Energy National Renewable Energy Laboratory Laboratory (NREL) at www.nrel.gov/publications. 15013 Denver West Parkway Golden, CO 80401 Contract No. DE-AC36-08GO28308 303-275-3000 • www.nrel.gov NOTICE This work was authored by the National Renewable Energy Laboratory, operated by Alliance for Sustainable Energy, LLC, for the U.S. Department of Energy (DOE) under Contract No. DE-AC36- 08GO28308. Funding provided by the U.S. Department of Energy Office of Energy Efficiency and Renewable Energy Solar Energy Technologies Office. -

The Seeds of Solar Innovation: How a Nation Can Grow a Competitive Advantage by Donny Holaschutz

The Seeds of Solar Innovation: How a Nation can Grow a Competitive Advantage by Donny Holaschutz B.A. Hispanic Studies (2004), University of Texas at Austin B.S. Aerospace Engineering (2004), University of Texas at Austin M.S.E Aerospace Engineering (2007), University of Texas at Austin Submitted to the System Design and Management Program In Partial Fulfillment of the Requirements for the Degree of Master of Science in Engineering and Management ARCHIVES MASSACHUSETTS INSTITUTE at the OF TECHNOLOGY Massachusetts Institute of Technology February 2012 © 2012 Donny Holaschutz. All rights reserved The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part in any medium now known or hereqfter reated. Signed by Author: Donny Holaschutz Engineering Systems Division and Sloan School of Management January 20, 2012 Certified by: James M. Utterback, Thesis Supervisor David . McGrath jr (1959) Professor of Management and Innovation and Professor of neering SysemsIT oan School of Management Accepted by: Patrick C.Hale Director otS ystem Design and Management Program THIS PAGE INTENTIONALLY LEFT BLANK Table of Contents Fig u re List ...................................................................................................................................................... 5 T ab le List........................................................................................................................................................7 Executive -

US Solar Photovoltaic Manufacturing

U.S. Solar Photovoltaic Manufacturing: Industry Trends, Global Competition, Federal Support Michaela D. Platzer Specialist in Industrial Organization and Business May 30, 2012 Congressional Research Service 7-5700 www.crs.gov R42509 CRS Report for Congress Prepared for Members and Committees of Congress U.S. Solar PV Manufacturing: Industry Trends, Global Competition, Federal Support Summary Every President since Richard Nixon has sought to increase U.S. energy supply diversity. In recent years, job creation and the development of a domestic renewable energy manufacturing base have joined national security and environmental concerns as rationales for promoting the manufacturing of solar power equipment in the United States. The federal government maintains a variety of tax credits, loan guarantees, and targeted research and development programs to encourage the solar manufacturing sector, and state-level mandates that utilities obtain specified percentages of their electricity from renewable sources have bolstered demand for large solar projects. The most widely used solar technology involves photovoltaic (PV) solar modules, which draw on semiconducting materials to convert sunlight into electricity. By year-end 2011, the total number of grid-connected PV systems nationwide reached almost 215,000. Domestic demand is met both by imports and by about 100 U.S. manufacturing facilities employing an estimated 25,000 U.S. workers in 2011. Production is clustered in a few states, including California, Oregon, Texas, and Ohio. Domestic PV manufacturers operate in a dynamic and highly competitive global market now dominated by Chinese and Taiwanese companies. All major PV solar manufacturers maintain global sourcing strategies; the only U.S.-based manufacturer ranked among the top 10 global cell producers in 2010 sourced the majority of its panels from its factory in Malaysia. -

About to Explode

PHOTOVOLTAICS USA/MANUFACTURERS About to explode Projects in the non- Similar to other PV markets, the development in the United States is residential market segment, such as this characterized by excess capacities in manufacturing and a rapid price rooftop PV system in decline for component of solar power plants. Nevertheless, the US industry California, have been the driving force behind representatives are less pessimistic about the future than their colleagues the US solar market. Photo: Europressedienst in Europe. It shows that the markets are quite different from each other. ata by the Solar Energy Industries Association range of 31.14 % for companies found to benefit from (SEIA) suggests that the newly installed PV ca unfair subsidies and price dumping as well as Dpacity on the US market had reached 1,855 MW 249.96 % for companies that did not collaborate with in 2011, exceeding the previous record year 2010 the US customs service or failed to provide the infor (887 MW) by nearly 110 %. Generally, the solar indus mation needed. “The decision by the US Department try has therefore reason to be pleased with the devel of Commerce encourages us to believe that we can re opment in the last year. The newly installed capacities turn to fair competition,” explains Frank Asbeck, CEO had been equivalent to a market share of 7 % (2010: of SolarWorld. The path on the US market seems now 5 %) in the global new installa tions. The trend is ex open for a positive trend that could be comparable to pected to continue over the next few years – not least the last year. -

Encapsulation Advancements Extend Life of Thin-Film PV, The

The Spectrum of innovati nClean Energy Innovation Encapsulation Advancements Fundamental Science Market-Relevant Research Extend Life of Thin-Film PV Systems Integration Thin-film photovoltaic technology is proof positive that great Testing and Validation things can come in lightweight, flexible packages. This technology, Commercialization pioneered by NREL in 1978, has changed the way the world uses energy from the sun. And now, thin-film photovoltaic (PV) devices Deployment are even better, since NREL scientists created a low-cost way to encapsulate them that provides greater resistance to heat and Through deep technical expertise moisture—and longer lifetimes. and an unmatched breadth of capabilities, NREL leads an integrated Thin-film solar cells made from semiconductors such as copper, indium, gallium, and selenium approach across the spectrum of renewable energy innovation. From (known as “CIGS”) have several advantages over traditional crystalline silicon solar cells. One scientific discovery to accelerating big advantage is that they can be made into flexible products that can be used in aerospace market deployment, NREL works in applications, integrated into buildings (for example, on rooftops and walls), and much more. partnership with private industry However, flexible CIGS thin films also have one big disadvantage. They’re susceptible to failure to drive the transformation of our under long-term exposure to heat and humidity. nation’s energy systems. This vulnerability is apparent in the breakdown of the “window” layer caused by moisture This case study illustrates NREL’s entering through the device’s flexible encapsulation and degrading its transparent conductive innovations and contributions material, typically zinc oxide. The zinc oxide serves to collect the current from the device and in Fundamental Science through deliver the current to the module’s electrical terminals. -

Photovoltaic Thin Film Cells 2009

i Photovoltaic Thin Film Cells 2009 France Innovation Scientifique & Transfert FRINNOV 83 Boulevard Exelmans 75016 PARIS, FRANCE Tel.: +33 (0)1 40 51 00 90 Fax: +33 (0)1 40 51 78 58 www.frinnov.fr Patent Mapping - A new tool to decipher market trends MULTI-CLIENT PATENT LANDSCAPE ANALYSIS IP Overview is a report that analyses all patent families filed on a given thematic Available reports in engineering sciences are Carbon nanotubes, Photovoltaic cells (3 reports), LiMPO4 batteries TAILOR-MADE PATENT LANDSCAPE ANALYSIS IP Overview On Demand is similar to IP Overview but 100% tailored to your needs Ask your questions and we will answer by a specific analysis of the patent landscape of your area of interest CUSTUMIZED STUDIES OF PATENT PORTFOLIOS Position your patent portfolio or the one of your competitors PRIOR-ART SEARCH Need more information? Free access to the interactive database Contact us at [email protected] is provided for studies published since 2010 Photovoltaic Thin Film Cells CContents METHODOLOGY 11 INTRODUCTION 12 1. BRIEF OUTLINE OF THE PHOTOVOLTAICS MARKET 14 2. GLOBAL OVERVIEW OF PHOTOVOLTAIC PATENTS 17 2.1. Technological segmentation 18 2.2. Segmentation by application 20 2.3. Zoom on companies involved in the market 22 2.4. Zoom on CANON 24 2.4.1. History of patent application filings and ambitions 24 2.4.2. Segmentation of the patent portfolio 25 2.4.3. Filing policy 26 2.4.4. Analysis of the patent portfolio 28 3. THIN FILM CELL PATENTS - WORLD ANALYSIS 31 3.1. Protection strategies 31 3.1.1. -

GLOBAL TRENDS in RENEWABLE ENERGY INVESTMENT 2013 Frankfurt School-UNEP Centre/BNEF

GLOBAL TRENDS IN RENEWABLE ENERGY INVESTMENT 2013 Frankfurt School-UNEP Centre/BNEF. 2013. Global Trends in Renewable Energy Investment 2013, http://www.fs-unep-centre.org (Frankfurt am Main) Copyright © Frankfurt School of Finance & Management gGmbH 2013. This publication may be reproduced in whole or in part in any form for educational or non-profit purposes without special permission from the copyright holder, as long as provided acknowledgement of the source is made. Frankfurt School – UNEP Collaborating Centre for Climate & Sustainable Energy Finance would appreciate receiving a copy of any publication that uses this publication as source. No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from Frankfurt School of Finance & Management gGmbH. Disclaimer Frankfurt School of Finance & Management: The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the Frankfurt School of Finance & Management concerning the legal status of any country, territory, city or area or of its authorities, or concerning delimitation of its frontiers or boundaries. Moreover, the views expressed do not necessarily represent the decision or the stated policy of the Frankfurt School of Finance & Management, nor does citing of trade names or commercial processes constitute endorsement. TABLE OF CONTENTS TABLE OF CONTENTS ACKNOWLEDGEMENTS ....................................................................................................................................