Mechanical CAD/CAM/CAE Worldwide, 1995

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Networking Nirvana: AUGI at Autodesk University

Diamond Sponsors AUGIWorldThe Official Publication of Autodesk User Group International December 2014 Networking Nirvana: AUGI at Autodesk University Also in this issue: • How to Develop and Maintain Your Professional Network • Navisworks for Detailers • MEP Constuction Content: Build or Buy? HP recommends Windows. Make your AutoCAD® performance more awesome It’s time to move up to an AutoCAD 2015 certified, affordably priced Z with Workstation from HP.1 Featuring next-gen processors and professional graphics technologies, Z Workstations are specifically designed to handle today’s most complex modeling and rendering projects. Add in our three-year warranty and experience HP’s ultimate combination of performance and value. Find out what http://hp.com/go/autodeskmakes HP Z Workstations the world’s #1 workstation brand.2 Z Learn more at hp.com/go/autocad HP can deliver up to: 59% faster modeling 40% faster rendering 95% better overall performance3 © 2014 Hewlett-Packard Company, L.P. The information contained herein is subject to change without notice. 1The HP Z230 SFF Workstation is certified for AutoCAD 2015. 2Units shipped based on IDC Quarterly Worldwide Workstation Tracker Q2 CY2014. 3Based on the white paper, AutoCAD 2015 Performance: HP Z230 Workstation vs. HP PC. Autodesk was not involved in testing; this does not constitute an endorsement of these claims by Autodesk. NVIDIA, the NVIDIA logo and Quadro are registered trademarks and/or trademarks of NVIDIA Corporation in the United States and other countries. Autodesk and AutoCAD are registered trademarks or trademarks of Autodesk, Inc.,and/or its subsidiaries and/or affiliates in the USA and other countries. -

CAD/CAM/CAE/GIS Worldwide, 1993

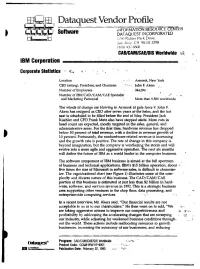

Dataquest Vendor Profile Gnfttaioro INFORMATION RESOURCE CENTER > donware DATAQUEST [NCORPORATED 1290 Rsdder Park Drive San Jose, CA 95131-2398 (408) 437-8600 CAD/CAM/CAE/GIS Worldwide 14 IBM Corporation Corporate Statistics 'IT, Location , •- Armonk, New York CEO (acting). President, and Oiairman John F. Akers Number of Employees 344,396 • Number of IBM CAD/CAM/CAE Specialist and Marketing Personnel More than 9,500 worldwide The winds of change are blowing in Armonk at gale force 9. John F. Akers has resigned as CEO after seven years at tiie helm, and the hot seat is scheduled to be filled before ttie end of May. President Jack Kuehler and GFO Frank Metz also have stepped aside. More cuts in head count are expected, mostly targeted in the sales, general, and administrative areas. For the first time, hardware revenue has dropped below 50 percent of total revenue, with a decline in revenue growth of » 10 percent. Fortvmately, the nonhardware-related revenue is increasing and the growth rate is positive. The rate of change in this company is beyond imagination, but the company is weathering the storm and will evolve into a more agile and aggressive operation. The next six months will define the future of 3M as a world leader in the computer business. The software component of IBM business is aimed at the full spectrum of business and technical applications. IBM's $15 billion operation, about five times the size of Microsoft in software sales, is difficult to character ize. The organizational chart (see Figure 1) illtistrates some of the com plexity and diverse nature of this business. -

BIM Tools and Parametric Modeling

CHAPTER2 BIM Tools and Parametric Modeling 2.0 EXECUTIVE SUMMARY This chapter provides an overview of the primary technology that distinguishes BIM design applications from other CAD systems. Object - based parametric modeling was originally developed in the 1980s. It does not represent objects with fi xed geometry and properties. Rather, it represents objects by parame- ters and rules that determine the geometry as well as some non - geometric properties and features. The parameters and rules allow the objects to auto- matically update according to user control or changing contexts. In other industries, companies use parametric modeling to develop their own object representations and to refl ect corporate knowledge and best practices. In architecture, BIM software companies have pre- defi ned a set of base building object families for users, which may be extended, modifi ed, or added to. An object family allows for the creation of any number of object instances, with forms that are dependent on parameters and relationships with other objects. Companies should have the capability of developing user - defi ned parametric objects and corporate object libraries for customized quality control and to establish their own best practices. Custom parametric objects allow for the modeling of complex geometries, which were previously not possible or simply impractical. Object attributes are needed to interface with analyses, cost estimations, and other applications, but these attributes must fi rst be defi ned by the fi rm or user. Current BIM tools vary in many ways: in the sophistication of their prede- fi ned base objects; in the ease with which users can defi ne new object families; BIM Handbook: A Guide to Building InformationModeling for Owners, Managers,Designers, Engineers, and Contractors. -

Design of a Single Family House Using BIM Software

Sandip Rai Design of a Single Family House Using BIM Software Modelling on ArchiCAD & Tekla Structures Helsinki Metropolia University of Applied Sciences Bachelor of Engineering Civil Engineering Bachelor`s Thesis November 2016 Degree Programme Thesis Date Abstract Author(s) Sandip Rai Title Design of a Single Family House Using BIM Software Number of Pages 40 pages + 19 appendices Date 24 November 2016 Degree Bachelor of Engineering Degree Programme Civil Engineering Specialisation option Sustainable Building Engineering Tomi Karppinen, (Senior Lecturer at HAMK UAS) Instructor(s) Jorma Säteri, (Head of Degree Program) The main objective of this Bachelor`s thesis was to create a model of a single family house using different Building Information Modelling (BIM) software. This thesis also aimed to provide the user with a manual for designing concrete structures using ArchiCAD and Tekla Structures. Each and every process of using the software has been clearly explained in this thesis. The theoretical part of the thesis was collected from various articles and websites. It in- cludes information and history about ArchiCAD and Tekla Structures. In addition to this, the advantages of using BIM software for Architects and Structural Engineers have also been presented in this thesis. The practical part of the thesis involves the use of BIM software. The example of BIM soft- ware that was used throughout the thesis is Graphisoft ArchiCAD and Tekla Structures. The thesis explains the methodologies of creating 3D architectural design from 2D draw- ings in ArchiCAD, as well as 3D structural design in Tekla Structures from ArchiCAD IFC model. The solution for linking ArchiCAD model to Tekla software is also explained in the thesis. -

ENGINEERING SOFTWARE Products

ENGINEERING SOFTWARE products Company Products Offered Product Description Acronym Software, Inc. SODA 4: Structural Software for the analysis and design of steel frameworks. Analyzes and designs steel frame- www.acronym.ca Optimization Design & works subject to AISC and CISC standards. The latest release has new toolbars, a faster 519.885.2454 Analysis analysis engine, an enhanced output viewer, and an editor for steel cross-sections. A 3D static and dynamic, frame and finite element analysis and design system. Pre- and ATIR Engineering Software STRAP Version 12.5 post-analysis options quicken and simplify data input and results interpretation. Postproces- www.ATIR.com sors include steel, concrete, and light gauge steel design. 847.677.1945 A postprocessor for bridge design, the program creates 3D influence lines for any point on STRAP BRIDGE the bridge and calculates the critical effect of the vehicle loads. Autodesk Building information modeling (BIM) software for structural engineering, design, and draft- www.autodesk.com Autodesk Revit Structure ing. It offers concurrent multi-material structural modeling for layout, coordination, and 415.507.5000 documentation—and bidirectional linking to analysis and design applications. Specifically developed for building designers, this fully integrated suite of building analysis, design, and drafting software automates the most time-consuming design tasks, such as RAM Structural System gravity and lateral load generation and fully integrated design of deep and shallow founda- tions. CAD files for floor framing plans, foundation plans, frame elevations, and beam and column schedules are automatically produced, all from a single model. Providing the “missing link” between the analytical model and construction drawings, the program works inside AutoCAD to help create and manage all construction documents. -

BIM Handbook: a Guide to Building Information Modeling for Owners, Managers, Designers, Engineers, and Contractors

www.EngineeringBooksPdf.com www.EngineeringBooksPdf.com BIM Handbook A Guide to Building Information Modeling for Owners, Managers, Designers, Engineers, and Contractors Second Edition Chuck Eastman Paul Teicholz Rafael Sacks Kathleen Liston John Wiley & Sons, Inc. ffirs.indd i 3/8/11 10:53:45 PM www.EngineeringBooksPdf.com This book is printed on acid-free paper. ϱ Copyright © 2011 by John Wiley & Sons, Inc.. All rights reserved Published by John Wiley & Sons, Inc., Hoboken, New Jersey Published simultaneously in Canada No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except as permitted under Section 107 or 108 of the 1976 United States Copyright Act, without either the prior written permission of the Publisher, or authorization through payment of the appropriate per-copy fee to the Copyright Clearance Center, 222 Rosewood Drive, Danvers, MA 01923, (978) 750-8400, fax (978) 646-8600, or on the web at www.copyright.com. Requests to the Publisher for permission should be addressed to the Permissions Department, John Wiley & Sons, Inc., 111 River Street, Hoboken, NJ 07030, (201) 748-6011, fax (201) 748-6008, or online at www.wiley.com/go/permissions. Limit of Liability/Disclaimer of Warranty: While the publisher and the author have used their best efforts in preparing this book, they make no representations or warranties with respect to the accuracy or completeness of the contents of this book and specifi cally disclaim any implied warranties of merchantability or fi tness for a particular purpose. -

Cheap Tricks Index 1990-2000

Cheap Tricks Index 1990-2000 ?, Wildcards Oct 91 4 3D CAD Shootout Apr 98 1 $, Dollar Sign, Keyboard Macro Apr 91 4 3D cars & people Nov 98 2 $ Dec 99 1 3D Cars & Trucks Feb 99 8 $$$ Marker file Feb 99 6 3D Construction Drawing Apr 95 1 *, Wildcards Oct 91 4 3D CAD Design Shootout, observations Dec 97 3 %1 to %10, DOS Replaceable Parameters Dec 91 5 3D CAD Design Shootout, playoff-caliber teams Dec 97 3 0, Alt-0 keyboard interrupt Apr 93 4 3D Cursor Dec 94 2 1.25 Million Questions May 99 7 3D Cursor Aug 95 4 10-Base-2; 10-Base-T Dec 97 4 3D Cursor Mar 95 3 16 bit processing Sep 96 2 3D Cursor, undocumented features Jun 97 4 16-bit processing May 93 3 3D Cylinder stretching Jan 98 8 3D Design & Presentation Dec 94 1 2 ½ D 3D Design Models, DC Viewer Mar 97 1 3D Designer's CADD Shootout Sep 99 2 2 1/2 D, vs. 3D for sections Jun 96 1 3D Designers CAD Shootout Dec 98 1 2 1/2D Modeling May 94 1 3D Designers CAD Shootout Nov 98 8 2 1/2 D massing model Jan 99 6 3D Drawings, As Construction Drawings Dec 91 2 2 line trim for stretching Jul 96 4 3D, Easy Method, Neal Mortenson Jan 94 3 2 1/2D vs. 3D, chart of differences Apr 00 3 3D Edit Menu May 94 3 2 1/2D vs. 3D Apr 00 2 3D Edit Plane Dec 94 4 2 1/2D, defined Apr 00 2 3D Edit, Won't work May 91 5 20/20 rule Feb 95 2 3D Editing Jan 98 8 286, 386, 486, with DOS 5.0 Aug 91 4 3D, Elevation save Mar 99 5 3D Elevation View Jun 91 2 3D Entity Menu May 94 3 2D 3D Framing macro Oct 94 8 3D, from 2D Transformations May 97 1 2D vs. -

Delivering a New Perspective

Autodesk Customer Success Story Steel Detailing Online, Inc. COMPANY Steel Detailing Online, Inc. Delivering a new perspective LOCATION Colorado, United States Advance Steel helps a steel detailer deliver SOFTWARE Autodesk® Advance Steel Autodesk® AutoCAD® more value to his clients Advance Steel helps me work out the constructability of a design, and gives me that other set of eyes when I’m rechecking complex spatial geometry. — Bart Rohal Founder and President Steel Detailing Online, Inc. Image courtesy of SDO INC. The firm In addition, as the popularity of Building Information Modeling (BIM) grows, more of Founded in 2002, the Colorado-based company Rohal’s clients are asking him to support BIM Steel Detailing Online provides structural steel workflows, thereby enabling the client to bid detailing to steel fabricators, steel erectors, on those projects. Although BIM projects are contractors, engineers, and architects. All currently a small percentage of his work, it is work is performed in-house by the company’s obvious to Rohal that BIM capabilities will become founder and president, Bart Rohal, whose steel a more common requirement, as will requests detailing career started in 1980. After progressing for the delivery of CNC files for fabrication. from Smoley’s Tables and drafting arms to 2D AutoCAD® software in the late ‘80s, Rohal made another big transition in 2010—adopting The solution Autodesk® Advance Steel software and 3D modeling for his steel detailing and checking. In 2011, Rohal began using 3D modeling in the form of Advance Steel software for detailing and checking. The software enables him to The challenges automatically generate traditional project “A lot of my projects are commercial buildings, deliverables such as shop drawings and erection which tend to be more complex due to the tight plans, as well as CNC files and material lists as constraints caused by all the building disciplines needed, directly from the Advance Steel model. -

Cad-Bim Requeriments for Masonry Design Process of Concrete Blocks

CIB W78 2008 International Conference on Information Technology in Construction Santiago, Chile CAD-BIM REQUERIMENTS FOR MASONRY DESIGN PROCESS OF CONCRETE BLOCKS Scheer, Sérgio Associate Professor of the Construction Engineering Department at the Federal University of Paraná – UFPR. Civil Engineering Research Centre, CEP 81.531-980, Cx. Postal 19.011, Curitiba, Paraná State, BRASIL [email protected] Ayres Filho, Cervantes1 [email protected] Azuma, Fabíola2 [email protected] Beber, Michelle3 [email protected] 1,2,3 MSc candidate of the Civil Construction Postgraduate Program at the Federal University of Paraná - UFPR. ABSTRACT The masonry constructive technique of concrete blocks is a practice that contributes for a high level of industrialization in construction in addition to achieve the rationalization in this sector. The achievement of these benefits demands some design features such as modular coordination, blocks rows details and well documented and precise specifications. One solution to meet these design features without causing agility reduction during the process is the use of CAD-BIM (Building Information Modeling), which applies modeling and visualization techniques already consolidated in other industry branches. Although the CAD- BIM brings improvements in the design process, it does not provide tools aimed directly to blocks masonry design, what can cause difficulties. The goal of this work is to identify these problems through a case study in a builder office sited in Curitiba, Parana state, Brazil, which is specialized in building design of concrete blocks masonry. Based on the results of data collected in the case study and in the literature available was possible to develop a list of CAD-BIM requirements more suitable for this kind of design. -

Formas Arquitetônicas: Possibilidades Em Ambiente Computacional

UNIVERSIDADE FEDERAL DA BAHIA FACULDADE DE ARQUITETURA PROGRAMA DE PÓS-GRADUAÇÃO EM ARQUITETURA E URBANISMO CHRISTINA ARAUJO PAIM CARDOSO FORMAS ARQUITETÔNICAS: POSSIBILIDADES EM AMBIENTE COMPUTACIONAL SALVADOR 2005 1 CHRISTINA ARAUJO PAIM CARDOSO FORMAS ARQUITETÔNICAS: POSSIBILIDADES EM AMBIENTE COMPUTACIONAL Tese apresentada ao Programa de Pós-Graduação em Arquitetura e Urbanismo da Faculdade de Arquitetura da Universidade Federal da Bahia como parte dos requisitos para obtenção do título de Doutor em Arquitetura e Urbanismo. Área de Concentração: Urbanismo. Orientador: Prof. Dr. Arivaldo Leão de Amorim SALVADOR 2005 2 UNIVERSIDADE FEDERAL DA BAHIA FACULDADE DE ARQUITETURA PROGRAMA DE PÓS-GRADUAÇÃO EM ARQUITETURA E URBANISMO CHRISTINA ARAUJO PAIM CARDOSO FORMAS ARQUITETÔNICAS: POSSIBILIDADES EM AMBIENTE COMPUTACIONAL Tese para obtenção do grau de Doutor em Arquitetura e Urbanismo Salvador, 26 de Agosto de 2005 Banca Examinadora ___________________________________________________ Prof. Doutor Arivaldo Leão de Amorim (Orientador) Universidade Federal da Bahia – Faculdade de Arquitetura ___________________________________________________ Profa. Doutora Elisabetta Romano Universidade Federal da Paraíba- Departamento de Arquitetura ___________________________________________________ Prof. Doutor Gilberto Corso Pereira Universidade Federal da Bahia – Faculdade de Arquitetura ___________________________________________________ Prof. Doutor Gilberto Sarkis Yunes Universidade Salvador ___________________________________________________ Prof. -

Smart Data Management with BIM for Architectural Heritage

POLITECNICO DI TORINO Repository ISTITUZIONALE Smart data management with BIM for Architectural Heritage Original Smart data management with BIM for Architectural Heritage / DEL GIUDICE, Matteo. - (2016). Availability: This version is available at: 11583/2652020 since: 2016-10-06T23:02:52Z Publisher: Politecnico di Torino Published DOI:10.6092/polito/porto/2652020 Terms of use: Altro tipo di accesso This article is made available under terms and conditions as specified in the corresponding bibliographic description in the repository Publisher copyright (Article begins on next page) 11 October 2021 PhD Student MATTEO DEL GIUDICE Supervisor PROF. ANNA OSELLO POLITECNICO DI TORINO SCUDO – SCUOLA DI DOTTORATO PH.D. DISSERTATION SMART DATA MANAGEMENT WITH BIM FOR ARCHITECTURAL HERITAGE Data management April 2016 POLITECNICO DI TORINO SCUDO - Scuola di Dottorato Dottorato in Innovazione Tecnologica per l’Ambiente Costruito XXVIII cycle Ph.D. Dissertation Smart data management with BIM for Architectural Heritage Ph.D. Student Ing. Matteo DEL GIUDICE Supervisor Prof. Anna OSELLO April 2016 Table of Contents 1. Acknowledgements ..................................................................................................3 2. List of abbreviations .................................................................................................4 3. List of figures ...........................................................................................................6 4. Abstract...................................................................................................................8 -

BIM): the Untapped Potential for Preservation Documentation and Management Laura Lee Worrell Clemson University

Clemson University TigerPrints All Theses Theses 5-2015 Building Information Modeling (BIM): The Untapped Potential for Preservation Documentation and Management Laura Lee Worrell Clemson University Follow this and additional works at: https://tigerprints.clemson.edu/all_theses Part of the Historic Preservation and Conservation Commons Recommended Citation Worrell, Laura Lee, "Building Information Modeling (BIM): The nU tapped Potential for Preservation Documentation and Management" (2015). All Theses. 2146. https://tigerprints.clemson.edu/all_theses/2146 This Thesis is brought to you for free and open access by the Theses at TigerPrints. It has been accepted for inclusion in All Theses by an authorized administrator of TigerPrints. For more information, please contact [email protected]. BUILDING INFORMATION MODELING (BIM): THE UNTAPPED POTENTIAL FOR PRESERVATION DOCUMENTATION AND MANAGEMENT A Thesis Presented to the Graduate School of Clemson University In Partial Fulfillment of the Requirements for the Degree Master of Science Historic Preservation by Laura Lee Worrell May 2015 Accepted by: Amalia Leifeste, Committee Chair Carter L. Hudgins Craig M. Bennett, Jr. i ABSTRACT The preservation field has few software programs specifically created to store historic and management documentation. Some programs and techniques are utilized in combination to aid in the management and documentation process of historic resources that include, laser scanning, AutoDesk AutoCAD programs, Rhino 3D, photogrammetry, geographic information system, and even Microsoft Excel. This thesis examines the applicability of the Architectural, Engineering, and Construction (AEC) industry’s Building Information Modeling (BIM) to create a three dimensional user interface for tracking and storing historic and management documentation. The case study performed for this thesis employs the Nathaniel Russell House owned by the Historic Charleston Foundation (HCF) located in Charleston, South Carolina.