Series of ERUDITE Working Papers Title

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2020 Diverse Founder Report 2021

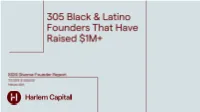

First Last Company Valuation Raise Status City Founded Race Gender ($mm) ($mm) 1 Robert Reffkin Compass $4,400 $1,500 Series G NYC 2012 African American Men 2 Daniel Perez Hinge Health $3,000 $426 Series D SF 2015 Latino Men 3 Tope Awontona Calendly $3,000 $351 Series A ATL 2013 African American Men 4 Pedro Franceschi Brex $2,600 $732 Series C SF 2017 Latino Men 5 Julia Collins Zume Pizza $2,250 $423 PE SF 2015 African American Women 6 Isabel Aznarez Stoke Therapeutics $2,160 $272 IPO BOS 2014 Latino Women 7 Jessie Woolley-Wilson Dreambox Learning $2,000 $176 Series C Seattle 2006 African American Women 8 Eugenio Pace Auth0 $1,920 $332 Series F Seattle 2013 Latino Men 9 Louis Von Ahn DuoLingo $1,650 $183 Series H Pittsburg 2011 Latino Men 10 Manny Medina Outreach $1,330 $289 Series F Seattle 2014 Latino Men 11 Jessica Alba Honest Company $1,000 $503 PE LA 2012 Latino Women 12 Toyin Ajayi City Block $1,000 $299 Series C NYC 2017 African American Women 13 Rihanna Fenty Savage x Fenty $1,000 $165 Series B LA 2017 African American Women 14 Michael Siebel Twitch $1,000 $35 M&A SF 2007 African American Men Total $28,310 $5,686 Investor Investments Investor Investments 1 Y Combinator 37 28 Rethink Education 6 2 Techstars 34 29 Salesforce Ventures 6 3 500 Startups 23 30 Sinai Ventures 6 4 Kapor Capital 19 31 AltaIR Capital 5 5 Harlem Capital Partners 16 32 Data Collective 5 6 Precursor Ventures 14 33 Founders Fund 5 7 Backstage Capital 12 34 Thrive Capital 5 8 Andreessen Horowitz 11 35 Village Global 5 9 Comcast Ventures 11 36 43North 4 10 Cross -

Corporate Venturing Report 2019

Corporate Venturing 2019 Report SUMMIT@RSM All Rights Reserved. Copyright © 2019. Created by Joshua Eckblad, Academic Researcher at TiSEM in The Netherlands. 2 TABLE OF CONTENTS LEAD AUTHORS 03 Forewords Joshua G. Eckblad 06 All Investors In External Startups [email protected] 21 Corporate VC Investors https://www.corporateventuringresearch.org/ 38 Accelerator Investors CentER PhD Candidate, Department of Management 43 2018 Global Startup Fundraising Survey (Our Results) Tilburg School of Economics and Management (TiSEM) Tilburg University, The Netherlands 56 2019 Global Startup Fundraising Survey (Please Distribute) Dr. Tobias Gutmann [email protected] https://www.corporateventuringresearch.org/ LEGAL DISCLAIMER Post-Doctoral Researcher Dr. Ing. h.c. F. Porsche AG Chair of Strategic Management and Digital Entrepreneurship The information contained herein is for the prospects of specific companies. While HHL Leipzig Graduate School of Management, Germany general guidance on matters of interest, and every attempt has been made to ensure that intended for the personal use of the reader the information contained in this report has only. The analyses and conclusions are been obtained and arranged with due care, Christian Lindener based on publicly available information, Wayra is not responsible for any Pitchbook, CBInsights and information inaccuracies, errors or omissions contained [email protected] provided in the course of recent surveys in or relating to, this information. No Managing Director with a sample of startups and corporate information herein may be replicated Wayra Germany firms. without prior consent by Wayra. Wayra Germany GmbH (“Wayra”) accepts no Wayra Germany GmbH liability for any actions taken as response Kaufingerstraße 15 hereto. -

Read Dissertation

Doctoral Dissertation: The Journey towards a Growing Diffusion of Entrepreneurship Learning and Culture in Society Written by: Mirta Michilli Role DETAILS Author Name: Mirta Michilli, PhD Year: 2019 Title: The Journey towards a Growing Diffusion of Entrepreneurship Learning and Culture in Society Document type: Doctoral dissertation Institution: The International School of Management (ISM) URL: https://ism.edu/images/ismdocs/dissertations/michilli-phd- dissertation-2019.pdf International School of Management Ph.D. Program The Journey towards a Growing Diffusion of Entrepreneurship Learning and Culture in Society PhD Dissertation PhD candidate: Mirta Michilli 21st December 2019 Acknowledgments I wish to dedicate this work to Prof. Tullio De Mauro who many years ago believed in me and gave me the permission to add this challenge to the many I face every day as General Director of Fondazione Mondo Digitale. The effort I have sustained for many years has been first of all for myself, to satisfy my desire to learn and improve all the time, but it has also been for my fifteen year old son Rodrigo, who is building his life and to whom I wish the power of remaining always curious, hungry for knowledge, and capable of working hard and sacrificing for his dreams. I could have not been able to reach this doctorate without the support of my family: my mother, for having being present all the time I needed to be away, my sister, for showing me how to undertake continuous learning challenges and, above all, my beloved husband to whom I owe most of what I know and for dreaming with me endlessly. -

Creating LAIA Foreword

Creating LAIA Foreword The lack of capital and support has been a constant refrain a feasibility study on the potential of a women-focused heard from female entrepreneurs at every stage of growth. LA incubator and accelerator, hence this publication A recent report by JPMorgan Chase and The Initiative for of Creating LAIA: The Feasibility of a Women-Focused a Competitive Inner City (ICIC) found that women (and Incubator & Accelerator in Los Angeles. minorities) “are not participating in high-tech incubators and accelerators at the same rates as their white, male Creating LAIA is the definition of collaboration - what counterparts.” women do organically. Although it was ofcially and adroitly written by We Are Enough Executive Director and After I gave my 2015 TEDx Talk, “Why You Should be Sexist Co-founder, Delilah Panio, the final product was birthed by with Your Equity Capital,” I was surprised by how many many. Along with the women entrepreneurs and women- women entrepreneurs approached and requested to meet focused incubator and accelerator leadership listed in with me – each emotionally describing their reactions to the appendix, we have had conversations with or have what I thought was the unemotional subject of finance and listened to many female investors and entrepreneurs who money. The majority of these women were small business have informed the conclusions reached in Creating LAIA. owners who articulated stories of the difculty in growing To name a few – Monica Dodi, Kara Nortman, Efe Epstein, their businesses, specifically the lack of support and Dana Settle, Kesha Cash, Carman Palafox, Noramay capital. I soon learned that many women had an emotional Cadena, Adena Smith, Diane Manuel, Ana Quintana, Darya and insecure relationship with money. -

Silicon Valley London Woodside Capital Partners (WCP)

Silicon Valley London Woodside Capital Partners (WCP) proudly releases the inaugural healthcare report “State of Digital Health”. In 2016, healthcare cost in the US was $3.3 Trillion – 17.9% of GDP, passing $10,000 per capita mark for the first time ever. According to CMS, by 2026, the figure is projected to grow to $5.7 Trillion – 19.8% of GDP. The answer to curbing and reversing the trend with respect to healthcare costs lies in large part to the movement towards Digital Health, or ‘Health Tech’. The proliferation of devices and applications across the healthcare spectrum has led to a data tsunami – the “what”. Machine Learning, Artificial Intelligence and overall Big Data analytics are leading to real-time actionable insights – the “so what”. We have entered the realm of the Internet of Medical Things (IoMT), with ubiquitous connectivity and measurement of everything from our vitals and nutrition to physical activity and medical compliance. We are just starting to leverage that data in a meaningful way and seeing early impact on health and well-being. In 2017, venture investments in Digital Health startups exceeded $6 Billion for the first time, and the trend seems to be accelerating with $1.6 Billion invested in Q1, 2018. The juxtaposition of rising healthcare costs and increased Digital Health investments is not all that surprising. Advances in underlying real-time analytics and potential of leading edge innovations around genomics are turning the perceived fiction of personalized medicine into a real possibility. Foundational disruptions such as Blockchain, while relatively nascent, are creating excitement (and some anxiety) around secure, immutable data sharing across silos – with healthcare as the ideal use case. -

Accelerators in Silicon Valley: Building Successful Startups

9789462987166 Accelerators in Silicon Valley: Building Successful Startups Accelerators in Silicon Valley: Building Successful Startups Searching for the Next Big Thing Peter Ester Amsterdam University Press This research was made possible by a grant from the Dutch Van Spaendonck Foundation. Cover design: Klaas Wijnberg Typesetting: Crius Group, Hulshout Amsterdam University Press English-language titles are distributed in the US and Canada by the University of Chicago Press. isbn 978 94 6298 716 6 e-isbn 978 90 4853 868 3 nur 800 doi 10.5117/9789462987166 © P. Ester / Amsterdam University Press B.V., Amsterdam 2017 All rights reserved. Without limiting the rights under copyright reserved above, no part of this book may be reproduced, stored in or introduced into a retrieval system, or transmitted, in any form or by any means (electronic, mechanical, photocopying, recording or otherwise) without the written permission of both the copyright owners and the authors of the book. You should start with the problem that you’re trying to solve in the world and not start with deciding that you want to build a company. Mark Zuckerberg, Facebook To all startups that contribute to a better society through their passion, ambition, and entrepreneurship Table of Contents Foreword 9 Acknowledgements 11 The Interviewees and their Accelerators 15 1 Silicon Valley 21 The DNA of an Entrepreneurial Region Introduction 21 Europe and Silicon Valley 22 Accelerators: Pillars of Silicon Valley’s startup support infra- structure 25 Accelerators: their role, research, -

Accelerators

Tilburg Law School ACCELERATORS Master Thesis LLM International Business Law Alja Pecenko ANR: 283644 Thesis Supervisor: Ivona Skultétyová, LLM TILBURG, JUNE 2016 Abstract Several circumstances enabled the development and the popularity that accelerators have today. As there is no widely accepted definition, there are several characteristics that are common to all accelerator programs: the fixed and short duration of the programs, which provides cohorts of startups with networking and mentoring opportunities and end with the event called »demo day«, and in most cases, seed capital and working space. Those characteristics along with the stage of the development of startup when accelerator usually admits startups sets them apart from other investors, such as angel investors, and incubators. One of the characteristic that many have is also the standardized investment terms. As such, accelerator terms mainly resemble the terms of other investors. Accelerators need backers that invest money, which influences the strategy of accelerators. Depending on the strategy and backers, there are four different types of accelerators: independent accelerators, corporate accelerators, university accelerators and government accelerators. But as the government are now investing in independent accelerators and corporation and university accelerators are starting to collaborate more and more, the clear distinction between them is blurring. Due to the high number of accelerators, the low number of exits and thus return on their investment along with a trend -

The Effects of the Non-Financial Component of Business Accelerators

N° 2021-6 THE EFFECTS OF THE NON-FINANCIAL COMPONENT OF BUSINESS ACCELERATORS FABRICE GILLES, YANNICK L’HORTY, FERHAT MIHOUBI www.tepp.eu TEPP – Theory and Evaluation of Public Policies - FR CNRS 2042 The Effects of the Non-Financial Component of Business Accelerators Fabrice Gilles1, Yannick L’Horty2, Ferhat Mihoubi 3 February 2021 Abstract. Accelerators are selective, intensive programs to help business owners, usually grouped into cohorts, develop the growth potential of their businesses. They appeared first in the mid-2000s in the United States and have since spread throughout the world. In France, the accelerator program implemented by Bpifrance since 2015 follows this same pattern, while having the rare feature of being strictly non-financial. Participating companies receive advice, training and networking opportunities, although their participation in the accelerator does not give them preferential access to investment or equity schemes, as is the case for many other accelerator programs. This somewhat unusual aspect of the Bpifrance program makes it possible to identify the effect of the non-financial component of an accelerator program. We evaluate the effect of this program based on accounting data from businesses covering the period 2010-2018, comparing three cohorts of participating businesses with a set of businesses presenting the same characteristics that did not participate in the program. For the first cohort, we find a significant impact on the likelihood of growing in size from an SME to a mid-cap enterprise. For the last two cohorts, we find the program has a positive effect on revenue with an increase of the order of ten percentage points, 16 percentage points on value added, and a tenfold increase on businesses’ capital expenditure under the program. -

The Rise of Wealthtech

WWW.DRAKESTAR.COM JULY 2020 Sector Report THE RISE OF WEALTHTECH Julian Ostertag, Managing Partner and Christophe Morvan, Managing Partner Member of the Executive Committee [email protected] [email protected] +33 1700 876 10 +49 89 1490 265 20 Michael Metzger, Partner Antonia Georgieva, Partner [email protected] [email protected] +1 310 696 4011 +1 917 755 5518 Kasper Kruse Petersen, Partner [email protected] +44 203 2057 360 In the USA, all securities transacted through Drake Star Securities LLC. In the USA, Drake Star Securities LLC. Is regulated by FINRA and is a member of SIPC Drake Star Partners is the marketing name for the global investment bank Drake Star Partners Limited and its subsidiaries and affiliates. In the USA, all securities are transacted through Drake Star Securities LLC. In the USA, Drake Star Securities LLC is regulated by FINRA and is a member of SIPC. © 2020 Drake Star Partners. This report is published solely for informational purposes and is not to be construed as an offer to sell or the solicitation of an offer to buy any security. The information herein is based on sources we believe to be reliable but is not guaranteed by us and we assume no liability for its use. Any opinions expressed herein are statements of our judgment on this date and are subject to change without notice. Citations and sources are available upon request through https://www.drakestar.com/contact. Interviews were conducted by Drake Star Partners via email correspondence between March and May 2020. -

The Rise of Wealthtech

WWW.DRAKESTAR.COM JULY 2020 Sector Report THE RISE OF WEALTHTECH Julian Ostertag, Managing Partner and Christophe Morvan, Managing Partner Member of the Executive Committee [email protected] [email protected] +33 1700 876 10 +49 89 1490 265 20 Michael Metzger, Partner Antonia Georgieva, Partner [email protected] [email protected] +1 310 696 4011 +1 917 755 5518 Kasper Kruse Petersen, Partner [email protected] +44 203 2057 360 In the USA, all securities transacted through Drake Star Securities LLC. In the USA, Drake Star Securities LLC. Is regulated by FINRA and is a member of SIPC Drake Star Partners is the marketing name for the global investment bank Drake Star Partners Limited and its subsidiaries and affiliates. In the USA, all securities are transacted through Drake Star Securities LLC. In the USA, Drake Star Securities LLC is regulated by FINRA and is a member of SIPC. © 2020 Drake Star Partners. This report is published solely for informational purposes and is not to be construed as an offer to sell or the solicitation of an offer to buy any security. The information herein is based on sources we believe to be reliable but is not guaranteed by us and we assume no liability for its use. Any opinions expressed herein are statements of our judgment on this date and are subject to change without notice. Citations and sources are available upon request through https://www.drakestar.com/contact. Interviews were conducted by Drake Star Partners via email correspondence between March and May 2020. -

Evaluating the U.S. Small Business Administration's Growth Accelerator

Evaluating the U.S. Small Business Administration’s Growth Accelerator Fund Competition Program A Report Prepared by the Federal Research Division, Library of Congress under an Interagency Agreement with the Office of Investment and Innovation, U.S. Small Business Administration FINAL February 2018 Researchers: Marieke Lewis Brock Meaghan Flattery Malinda K. Goodrich Wm. Noël Ivey Patrick M. Miller Project Manager: Malinda K. Goodrich Federal Research Division Library of Congress Washington, D.C. 20540−4840 Tel: 202−707−3900 Fax: 202−707−3920 Email: [email protected] Homepage: http://loc.gov/rr/frd/ 70 Years of Service to the Federal Government 1948 – 2018 Library of Congress—Federal Research Division Evaluating the SBA’s GAFC Program PREFACE The U.S. Small Business Administration’s (SBA’s) Office of Investment and Innovation (OII) contracted with the Library of Congress’s Federal Research Division (FRD) for an independent evaluation of the Growth Accelerator Fund Competition (GAFC) program. The OII oversees the program, which the SBA instituted to “support the development of accelerators and their support of startups in parts of the country where there are fewer conventional sources of access to capital.”1 The goal of this report is to evaluate the scope and value of the GAFC program as a federal government-sponsored means of spurring innovation and small business growth. The analysis included in this report is based on a literature review of scholarly research on the growing accelerator movement; data and reports from the Aspen Institute’s Global Accelerator Learning Initiative, Crunchbase, the Global Accelerator Network, and PitchBook; SBA-required reporting by the 2014–16 GAFC winners; interviews with key experts in the field; and a survey of the 2014–16 GAFC winners to build the fullest picture possible of the program’s impact. -

TECHNOLOGY SQUARE | #Iecosystem

OCTOBER 12–13, 2017 | TECHNOLOGY SQUARE | #iECOSYSTEM SPONSORS Ewing Marion Kauffman Foundation | MIT Corporate Relations | MIT Sloan Executive Education WELCOME Bringing together a global community of practitioners with thought leaders and scholars to explore the implementation of novel models, programs, and initiatives that enhance economic growth and social progress in innovation ecosystems. THE GOAL OF THE SYMPOSIUM To learn from both successes and failures and to maximize collective impact in research and practice, exploring “what’s best” today and “what’s next” on the frontier. The overarching emphasis will be on the models, programs, and initiatives that develop, drive, and inform innovation ecosystems and the roles multi-stakeholder leadership plays in advancing them both individually and collectively. Home to MIT labs, makerspaces, and industry alike, the symposium is taking IMMERSED IN THE ECOSYSTEM place in the heart of Technology Square, an innovation ecosystem it aims to foster. Through a call for concepts soliciting novels models from around the world, BROAD BASE OF INPUTS the symposium tracks are defined by the submissions received and will draw from them to coalesce and disseminate best practices and new ideas. The symposium aims to compile a resource regarding the inputs, outputs, and impacts DESIRED OUTCOMES of effective I&E models, programs, and initiatives, making available the top 30 concept papers describing novel, action- oriented programs (including their design, implementation challenges and metrics for evaluation),