FAGE DAIRY INDUSTRY S.A. ANNUAL REPORT for the Year

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

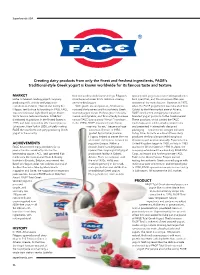

Creating Dairy Products from Only the Finest And

Superbrands USA FAGE Creating dairy products from only the fnest and freshest ingredients, FAGE’s traditional-style Greek yogurt is known worldwide for its famous taste and texture. Total is more than Greek yogurt. It’s a part of life. When they eat FAGE Total, they are part of the ancient Greek tradition of “good living;” and by MARKET little as travelers would come and go, Filippou’s typically sold yogurt as a commodity product in cooking with it, they are bringing the healthy FAGE is Greece’s leading yogurt company, store became known for its delicious, creamy, bulk quantities, and the consumer often was Mediterranean lifestyle into their diet. In producing milk, cheese and yogurt for one-of-a-kind yogurt. unaware of the manufacturer. However, in 1975, Greece, it’s eaten at all hours of the customers worldwide. Owned and led by the With great care and passion, Athanassios when the FAGE yogurt plant was relocated from day. Tossed with cucumbers and Filippou family since its founding in 1926, FAGE nurtured the business and his authentic Greek Galatsi to the Metamorfosi area of Athens, garlic, it’s the traditional dish of features traditional-style Greek yogurt known strained yogurt recipe. He brought in his sons, FAGE was the frst company to introduce tzatziki, and a perfect complement for its famous taste and texture. FAGE frst Ioannis and Kyriakos, and thus a family business branded yogurt products to the Greek market. to lunch or dinner. Drizzled with distributed its products in the United States in named FAGE (pronounced “fa-yeh”) was born. -

FAGE INTERNATIONAL S.A. ANNUAL REPORT for the Year Ended December 31, 2016 March 23, 2017

FAGE INTERNATIONAL S.A. ANNUAL REPORT For the Year Ended December 31, 2016 March 23, 2017 This report (the “Annual Report”) includes the consolidated financial statements and other information of FAGE INTERNATIONAL S.A. and its subsidiaries (the “FAGE Group”) as of and for the year ended December 31, 2016. This Annual Report is being provided to Holders of the Senior Notes pursuant to the requirements of the Indenture governing such Senior Notes. This report is organized as follows: Pages Section A: Summary analysis of Senior Notes issued by the Group and other related information. 2-7 Section B: Report of the Board of Directors. Risk Factors ......................................................................................................................... 8-20 Selected Consolidated Financial Information ......................................................................... 21-22 Management’s Discussion and Analysis of Financial Condition and Results of Operations ..... 23-30 Our Industry ......................................................................................................................... 31-35 Business ............................................................................................................................... 36-42 Management ......................................................................................................................... 43-44 Ownership of Share Capital ................................................................................................... 45 Related -

Current, August 23, 2004 University of Missouri-St

University of Missouri, St. Louis IRL @ UMSL Current (2000s) Student Newspapers 8-23-2004 Current, August 23, 2004 University of Missouri-St. Louis Follow this and additional works at: http://irl.umsl.edu/current2000s Recommended Citation University of Missouri-St. Louis, "Current, August 23, 2004" (2004). Current (2000s). 188. http://irl.umsl.edu/current2000s/188 This Newspaper is brought to you for free and open access by the Student Newspapers at IRL @ UMSL. It has been accepted for inclusion in Current (2000s) by an authorized administrator of IRL @ UMSL. For more information, please contact [email protected]. ft .. ' ~ ,.- VOLUME 37 August 23, 2004 ISSUE 1124 Your source for campus news (lnd information See page 13 Get your words crossed. Grant First Lady speaks t o aimed at St. Louis women catching Laura Bush campaigns at 'W Stands for Women' rally in Frontenac BY KATE DROLET internet ....iCli tor-in:(;jjiej "I learned at an early age that women can make an incredible predators difference in our world," First Lady Laura Bush told a crowd of supporters at the 'W' Stands for Women program, BY M.K. STALLINGS hosted by the Republican National --..- -'--"' ... _... - Staff Writer Committee. St. Louis women ranging from toddlers to seniors gathered at the Hilton Frontenac hotel on Tuesday, The Children's Advocacy Services Aug. 17, to rally for the First Lady and of Greater St Louis, located on the the Bush campaign. South Campus of UM-St. Louis, was Several prominent Missouri recently granted $12,160 to continue politicians, including Missouri conducting workshops that protect Secretary of State candidate and children from Internet predators. -

FAGE INTERNATIONAL S.A. ANNUAL REPORT for the Year Ended December 31, 2020 March 24, 2021

FAGE INTERNATIONAL S.A. ANNUAL REPORT For the Year Ended December 31, 2020 March 24, 2021 This report (the “Annual Report”) includes the consolidated financial statements and other information of FAGE INTERNATIONAL S.A. and its subsidiaries (the “FAGE Group”) as of and for the year ended December 31, 2020. This Annual Report is being provided to holders of the Senior Notes pursuant to the requirements of the Indenture governing such Senior Notes. This report is organized as follows: Pages Section A: Summary analysis of Senior Notes issued by the Group and other related information. 2-7 Section B: Report of the Board of Directors. Risk Factors ....................................................................................................................................... 8-20 Selected Consolidated Financial Information ................................................................................. 21-22 Management’s Discussion and Analysis of Financial Condition and Results of Operations ...... 23-29 Our Industry ....................................................................................................................................... 30-34 Business .............................................................................................................................................. 35-41 Management ....................................................................................................................................... 42-44 Ownership of Share Capital .............................................................................................................. -

FAGE CASE STUDY in BRIEF Company-Wide Migration to .FAGE

CL dot brand case studies Oct 2020.qxp_Layout 1 14/09/2020 08:00 Page 1 .FAGE A recipe for success .FAGE CASE STUDY IN BRIEF Company-wide migration to .FAGE • Initiatives International dairy company, FAGE, boasts nearly 100 years of innovation1 in Localisation, simplified navigation manufacturing dairy products, including the iconic trend of Greek yoghurt, which began in the 1990s within the US. Now, it is making its mark in digital • Main model of use marketing, with the launch of its .FAGE TLD. Full migration, including internal domains FAGE, pronounced ‘fah-yeh’ (from the Greek ‘to eat’) has grown from its origins as a small dairy shop, opened in Athens, Greece in 1926, to an international dairy 2 • Key benefits company serving customers across 34 countries in Europe, the Americas, Asia, and Consumer trust, local language sites, Africa. Following its successful application for the dot brand gTLD .FAGE, in 2016 the domain name consolidation company migrated its entire internet presence over to .FAGE, including its websites and email. The company has domain name registrations under other TLDs, but they now redirect to the .FAGE domain; for example, FAGE.GR. Its main corporate website is now located at HOME.FAGE, and it uses MAIL.FAGE for corporate email. This is a significant move for such a large global organisation, and one which shows the value they place in their dot brand. HOME.FAGE FAGE is creating Notably, FAGE.COM is owned by a different company with the same name. This suggests that a motivation for FAGE in applying for their dot brand may have been keyword domains to the opportunity to move away from any complications relating to coexistence and direct consumers to conflicts over TLD registrations (especially as they don’t own FAGE.CO.UK), in favour of its own secure branded space. -

1-4.Qxd (Page 1)

$21.50 d's Dairy Class III Prices orl In W du $20.50 Since 2005 e st h r t y $19.50 February in Red g W n i e $18.50 e v Since 1876 k r e l y S $17.50 $16.50 $15.50 $14.50 $13.50 CHEESE REPORTER $12.50 $11.50 Vol. 132, No. 35 • Friday, February 29, 2008 • Madison, Wisconsin $10.50 2005 2006 2007 2008 Alto Dairy Co-op Members USDA Proposes Class I Price Hike In Approve Sale Of Assets To Saputo Cheese USA Fond du Lac, WI—Alto Dairy Three Southeastern Federal Orders Cooperative announced Wednesday Citing Emergency Marketing Southeast orders: 25 percent of Appalachian order, approximately that its members have approved the Conditions, USDA Skips deliveries to pool plants during the $17.5 million for the Southeast sale of the co-op’s assets to Saputo order and approximately $38 million Recommended Decision months of January, February, July, Cheese USA Inc. for total consider- August, September, October and for the Florida order. ation of $160 million. Washington—The US Department November, and 35 percent for the In estimating the impact on min- The sale, which was unanimously of Agriculture (USDA) today pub- other five months. imum producer prices, blend prices approved by Alto’s board of directors lished a tentative final decision that •Reduce touch-base standards to will increase by about 26 cents per in January, was voted on and increases Class I prices in the one day each month for the hundredweight for the Appalachian approved by 98 percent of the co- Appalachian, Southeast and Florida Appalachian and Southeast orders. -

FAGE DAIRY INDUSTRY S.A. ANNUAL REPORT for the Year

FAGE DAIRY INDUSTRY S.A. ANNUAL REPORT For the Year Ended December 31, 2010 As Required by Greek law 3556/2007 Pursuant to the Adoption of the Transparency Directive 2004/109/EC March 28, 2011 This report (the “Annual Report”) includes the information that is required to be published by FAGE DAIRY INDUSTRY S.A. as of and for the year ended December 31, 2010, as required by Greek law 3556/2007 pursuant to the adoption of the Transparency Directive 2004/109/EC. This Annual Report is organised as follows: Pages Section A: Summary analysis of Senior Notes issued by the Company and other related information....... 2-6 Section B: Declarations of the members of the Board of Directors in accordance with art 4 (2) of Law 3556/2007.......................................................................................................................... 7 Section C: Report of the Board of Directors .................................................................................................. 8 Risk Factors........................................................................................................................... 9-17 Selected Consolidated Financial Information ..................................................................... 18-20 Management’s Discussion and Analysis of Financial Condition and Results of Operations.............................................................................................................................. 21-22 Results of Operations for the Group ................................................................................... -

Fage International S.A

FAGE INTERNATIONAL S.A. QUARTERLY REPORT For the Nine and Three Months Ended September 30, 2018 November 13, 2018 This report (the “Quarterly Report”) sets forth certain information regarding the financial condition and results of operations of FAGE International S.A. and its subsidiaries (the “FAGE Group”) for the nine and three months ended September 30, 2018. The Quarterly Report includes a review, in English, of the FAGE Group’s unaudited financial information and analysis for the third quarter as well as certain other information. The following unaudited financial statements in the opinion of the management reflect all necessary adjustments (which include only normal recurring adjustments) necessary for a fair presentation of the FAGE Group’s financial position, results of operations and cash flows for the periods presented. For a description of accounting policies see Notes to the Consolidated Financial Statements in the FAGE Group’s 2017 Annual Report. 1 Summary Analysis of Senior Notes Issued by FAGE INTERNATIONAL S.A. and FAGE USA DAIRY INDUSTRY, INC. On August 3, 2016, FAGE International S.A. (“FAGE International”) and FAGE USA Dairy Industry, Inc. (“FAGE USA” and together with FAGE International, the “Issuers”) issued $420,000,000 principal amount of their 5.625% Senior Notes due 2026 (the “Senior Notes”) under an indenture, dated as of August 3, 2016 (the “Indenture”), by and among the Issuers, FAGE Dairy Industry S.A. (“FAGE Greece”), as guarantor, The Bank of New York Mellon, acting through its London Branch, as trustee, The Bank of New York Mellon, as paying and transfer agent, and The Bank of New York Mellon (Luxembourg) S.A., as registrar. -

FAGE INTERNATIONAL S.A. ANNUAL REPORT for The

FAGE INTERNATIONAL S.A. ANNUAL REPORT For the Year Ended December 31, 2014 March 30, 2015 This report (the “Annual Report”) includes the consolidated financial statements and other information of FAGE INTERNATIONAL S.A. and its subsidiaries (the “FAGE Group”) as of and for the year ended December 31, 2014. This Annual Report is being provided to Holders of the Senior Notes pursuant to the requirements of the Indenture governing such Senior Notes. This report is organized as follows: Pages Section A: Summary analysis of Senior Notes issued by the Group and other related information. 2-7 Section B: Report of the Board of Directors. Risk Factors................................................................................................ ................................ 8-19 Selected Consolidated Financial Information ................................................................................................20-21 Management’s Discussion and Analysis of Financial Condition and Results of Operations................................22-29 Our Industry ................................................................................................................................ 30-33 Business................................................................................................................................................................34-41 Management ................................................................................................................................ 42-44 Ownership of Share Capital ................................................................................................................................45 -

The Elliniko Airport: Contested Politics and the Production of Urban Space in Athens, 1938-2014" (2014)

University of Wisconsin Milwaukee UWM Digital Commons Theses and Dissertations 5-1-2014 The lE liniko Airport: Contested Politics and the Production of Urban Space in Athens, 1938-2014 George Papakis University of Wisconsin-Milwaukee Follow this and additional works at: https://dc.uwm.edu/etd Part of the Geography Commons, History Commons, and the Urban Studies and Planning Commons Recommended Citation Papakis, George, "The Elliniko Airport: Contested Politics and the Production of Urban Space in Athens, 1938-2014" (2014). Theses and Dissertations. 478. https://dc.uwm.edu/etd/478 This Dissertation is brought to you for free and open access by UWM Digital Commons. It has been accepted for inclusion in Theses and Dissertations by an authorized administrator of UWM Digital Commons. For more information, please contact [email protected]. THE ELLINIKO AIRPORT: CONTESTED POLITICS AND THE PRODUCTION OF URBAN SPACE IN ATHENS, 1938-2014 by George Papakis A Dissertation Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy in Urban Studies at The University of Wisconsin- Milwaukee May 2014 ABSTRACT THE ELLINIKO AIRPORT: CONTESTED POLITICS AND THE PRODUCTION OF URBAN SPACE IN ATHENS, 1938-2014 by George Papakis The University of Wisconsin-Milwaukee, 2014 Under the Supervision of Professor Joseph A. Rodriguez This study traces the historical forces that conditioned the dearth of public spaces in Athens, Greece, and through the case study of the city’s first civil airport, examines the current redevelopment plans of Athens’ largest remaining open space as part of a wider process of urban transformation. After serving the city for sixty years, the airport closed its doors in 2001, and since then the site has remained vacant. -

THE MARKET FAGE Is Greece's Leading Yogurt Company, Pro

GREEN FOCUS FAGE’s presence in Johnstown, New York, has proven to be a win-win for the company and its chosen locale. For a gauge of the company’s success, yogurt sales have gone from 2,000 imported tons in 2004 to presently being able to produce up to 85,000 tons. And as with any yogurt factory process, such activity creates whey, but in this case it is not wasted. Whey from the burgeoning FAGE plant in Johnstown is pipelined to the town’s wastewater treatment facility to produce methane gas that runs that facility’s generators. When operations began in 2008, the town’s plant was producing 30 percent of its own power. With the increased activity resulting THE MARKET relocated from Galatsi to the Metamorfosi area FAGE is Greece’s leading yogurt company, pro- of Athens, FAGE was the first company to intro- from FAGE’s success, the town’s plant is now producing close to 80 to 100 ducing milk, cheese, and yogurt for customers duce branded yogurt products to the Greek mar- percent of its electricity, saving Johnstown $600,000 annually in electric worldwide. Owned and strategically led by the ket. These products, which carried the FAGE bills. Moreover, because of the cost savings, Johnstown has been able to Filippou family since its founding in 1926, FAGE trademark, were sold in smaller, sealed tubs and reduce its sewer rates for town residents. features traditional-style Greek yogurt known presented in attractively designed packaging — for its famous taste and texture. FAGE first similar to the designs still used today. -

Strategy for the Development of Greek Enterprises

School of Social Sciences Master in Business Administration Postgraduate Dissertation The international operations of Greek dairy industry - The case study of FAGE Antonopoulos Athanasios Supervisor: Tsinopoulos Christos Patras, Greece, September 2018 Theses / Dissertations remain the intellectual property of students (“authors/creators”), but in the context of open access policy they grant to the HOU a non-exclusive license to use the right of reproduction, customization, public lending, presentation to an audience and digital dissemination thereof internationally, in electronic form and by any means for teaching and research purposes, for no fee and throughout the duration of intellectual property rights. Free access to the full text for studying and reading does not in any way mean that the author/creator neither shall allocate his/her intellectual property rights, nor shall he/she allow the reproduction, republication, copy, storage, sale, commercial use, transmission, distribution, publication, execution, downloading, uploading, translating, modifying in any way, of any part or summary of the dissertation, without the explicit prior written consent of the author/creator. Creators retain all their moral and property rights. The international operations of Greek dairy industry - The case study of FAGE Antonopoulos Athanasios Supervising Committee Supervisor: Co-Supervisor: Tsinopoulos Christos Theotokas Ioannis HOU HOU Patras, Greece, September 2018 Athanasios Antonopoulos, The international operations of Greek dairy industry – The case study of FAGE Acknowledgements I would like to thank my supervisor Tsinopoulos Christos for his guidance in the completion of my dissertation. Postgraduate Dissertation iv Athanasios Antonopoulos, The international operations of Greek dairy industry – The case study of FAGE Abstract This thesis has examined the case of FAGE and how it works in international markets.