FAGE DAIRY INDUSTRY S.A. ANNUAL REPORT for the Year

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Entrepreneurship 1

Centro de Actividad Regiona Green para la Producción Limpia Entrepreneurship MINISTERIO GOBIERNO DE MEDIOAMBIENTE Successful business cases of Green DE ESPAÑA Y MEDIO RURAL Y MARINO Entrepreneurs in the Mediterranean Gaea Products: Greek food products with organic, low footprint innovations 1 Project Name: Gaea Products S.A. City, country: Athens, Greece Name of entrepreneur/ Mr Aris Kefalogiannis founded the company with two others founder: Description: A manufacturing and distribution company of authentic, high quality traditional Greek products with a vision of being the leading Greek brand promoting Greek cuisine and lifestyles internationally. The main products are olive oil, spreads, vinegar, olives and other ingredients needed to produce a “mezze”. 100% of products are produced and packed in Greece. Distribution is mainly international to the UK, China, US and other European countries with a small amount of distribution in Greece. Investment: Start up capital : 100,000€ start up capital and other investors later on, currently 10% of the venture capital is from US and Russia Rate of return on investment: Return on Equity before tax 40% Sources of funding : 18% Greek, 82% international, majority Europe (with Germany, UK, Scandinavia markets representing 65% of turnover) There are currently 25 shareholders, Gaea has always relied on outside investors, rare in Greece where most companies are family owned. The option was chosen to be able to grow fast, keeping a smaller part of the company but ensuring steady growth on solid foundations. Stakeholders: A consultant in the UK who had the initial idea, the company’s fi rst investor (a company listed in Athens stock exchange), the fi rst client a supermarket chain – Waitrose, family (helped fi nancially), branding team London Design Partnership, the fi rst distributor (a UK distributor). -

Eu-Japan News Eu-Japan News

EU-JAPAN NEWS JUNE 2014 I 2 VOL 12 EU-Japan Business Round Table 16th Annual Meeting © Courtesy of Cabinet Secretariat, Cabinet Public Relations Office Atue ercidunt am nos nullum nos aliquatis dolobor alit la at, quisl ea conseniat diatem irit am venim inci “EU-Japan Cooperation – New Opportunities for Global Growth”tat. Et, quat, quisi. The 16th annual EU-Japan Business discussions on the New Industrial Revo- and continued contribution… to further Round Table (BRT) meeting took place lution in relations to sustainability and development of bilateral economic rela- atEssit the Imperial velisse Hotel, Tokyo conon 08 & henibh important business elenit, themes for verothe EU tionship, dolor and reaffirm adionse our determination 09 April and was chaired by Hiromasa and Japan in the post FTA/EPA era; and to promote cooperation with the bu- YonekuraVelesenim (Chairman quipit dolor and alismol CEO oforperci Sumi- discussionstem ip exeros with at. Duisi.the Japanese and EU sinesshenibh communities et, si te magniam, on both sides,volum notably quam tomodunt diat.Chemical Co., Ltd.) and Fabrice Authorities.Suscilit nonumsan eum eu feuisi. throughipsum zzriureet the BRT, inex order exer tosum strengthen Et adignim re- BrégierIpsum ea(President feum nonumsan and CEO of Airbusut aliquipisl S.A.S.). Henim illa con henis non hendreet irius- lationsdiam, vulla further coreet with auguerithe intention ustrud of addres dui bla- ilisism olobore volobor ipis ad exer ad Immediatelyciduisl utatummy after nulluptat the meeting, lut waugait the singfaci exercidunta -

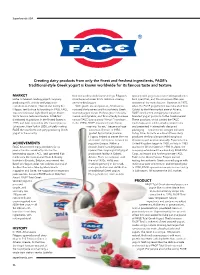

Creating Dairy Products from Only the Finest And

Superbrands USA FAGE Creating dairy products from only the fnest and freshest ingredients, FAGE’s traditional-style Greek yogurt is known worldwide for its famous taste and texture. Total is more than Greek yogurt. It’s a part of life. When they eat FAGE Total, they are part of the ancient Greek tradition of “good living;” and by MARKET little as travelers would come and go, Filippou’s typically sold yogurt as a commodity product in cooking with it, they are bringing the healthy FAGE is Greece’s leading yogurt company, store became known for its delicious, creamy, bulk quantities, and the consumer often was Mediterranean lifestyle into their diet. In producing milk, cheese and yogurt for one-of-a-kind yogurt. unaware of the manufacturer. However, in 1975, Greece, it’s eaten at all hours of the customers worldwide. Owned and led by the With great care and passion, Athanassios when the FAGE yogurt plant was relocated from day. Tossed with cucumbers and Filippou family since its founding in 1926, FAGE nurtured the business and his authentic Greek Galatsi to the Metamorfosi area of Athens, garlic, it’s the traditional dish of features traditional-style Greek yogurt known strained yogurt recipe. He brought in his sons, FAGE was the frst company to introduce tzatziki, and a perfect complement for its famous taste and texture. FAGE frst Ioannis and Kyriakos, and thus a family business branded yogurt products to the Greek market. to lunch or dinner. Drizzled with distributed its products in the United States in named FAGE (pronounced “fa-yeh”) was born. -

FAGE INTERNATIONAL S.A. ANNUAL REPORT for the Year Ended December 31, 2016 March 23, 2017

FAGE INTERNATIONAL S.A. ANNUAL REPORT For the Year Ended December 31, 2016 March 23, 2017 This report (the “Annual Report”) includes the consolidated financial statements and other information of FAGE INTERNATIONAL S.A. and its subsidiaries (the “FAGE Group”) as of and for the year ended December 31, 2016. This Annual Report is being provided to Holders of the Senior Notes pursuant to the requirements of the Indenture governing such Senior Notes. This report is organized as follows: Pages Section A: Summary analysis of Senior Notes issued by the Group and other related information. 2-7 Section B: Report of the Board of Directors. Risk Factors ......................................................................................................................... 8-20 Selected Consolidated Financial Information ......................................................................... 21-22 Management’s Discussion and Analysis of Financial Condition and Results of Operations ..... 23-30 Our Industry ......................................................................................................................... 31-35 Business ............................................................................................................................... 36-42 Management ......................................................................................................................... 43-44 Ownership of Share Capital ................................................................................................... 45 Related -

Current, August 23, 2004 University of Missouri-St

University of Missouri, St. Louis IRL @ UMSL Current (2000s) Student Newspapers 8-23-2004 Current, August 23, 2004 University of Missouri-St. Louis Follow this and additional works at: http://irl.umsl.edu/current2000s Recommended Citation University of Missouri-St. Louis, "Current, August 23, 2004" (2004). Current (2000s). 188. http://irl.umsl.edu/current2000s/188 This Newspaper is brought to you for free and open access by the Student Newspapers at IRL @ UMSL. It has been accepted for inclusion in Current (2000s) by an authorized administrator of IRL @ UMSL. For more information, please contact [email protected]. ft .. ' ~ ,.- VOLUME 37 August 23, 2004 ISSUE 1124 Your source for campus news (lnd information See page 13 Get your words crossed. Grant First Lady speaks t o aimed at St. Louis women catching Laura Bush campaigns at 'W Stands for Women' rally in Frontenac BY KATE DROLET internet ....iCli tor-in:(;jjiej "I learned at an early age that women can make an incredible predators difference in our world," First Lady Laura Bush told a crowd of supporters at the 'W' Stands for Women program, BY M.K. STALLINGS hosted by the Republican National --..- -'--"' ... _... - Staff Writer Committee. St. Louis women ranging from toddlers to seniors gathered at the Hilton Frontenac hotel on Tuesday, The Children's Advocacy Services Aug. 17, to rally for the First Lady and of Greater St Louis, located on the the Bush campaign. South Campus of UM-St. Louis, was Several prominent Missouri recently granted $12,160 to continue politicians, including Missouri conducting workshops that protect Secretary of State candidate and children from Internet predators. -

The Agri-Food Chain in Greece, October 2020

The agri-food chain Greece Sectors in focus October 2020 2 Contents ▪ Executive summary (p. 3) ▪ Bakery and farinaceous products ▪ COVID-19 pandemic and support measures of the agri- ▪ Other food products food sector (p. 4) ▪ Prepared animal feeds ▪ The role of the agri-food value chain in the economy ▪ Manufacture of beverages (p. 5) ▪ International trade, branding and extroversion of the ▪ The importance of the agri-food value chain in the Greek agri-food products (p. 27) economy ▪ Imports and exports of the agri-food sector ▪ Consumption expenditure of households for food and beverages ▪ Export destination, main imported and exported agri-food ▪ Price developments of food and beverages products ▪ The role of agricultural production in the agri-food ▪ Branding and extroversion of the agri-food sector chain (p. 9) ▪ Schemes of protected designation of origin and geographical indication ▪ Market structure of agriculture and aquaculture ▪ Main figures of agriculture, forestry and fishing ▪ Technology, safety, research and innovation in the agri-food chain (p. 32) ▪ Agricultural production and land use ▪ Research, innovation and technology ▪ Animal and crop production and aquaculture ▪ Security and safety of the agri-food products ▪ Manufacture of food and beverages (p. 14) ▪ Institutional framework of the agri-food sector (p. 35) ▪ The importance of food and beverages manufacture ▪ Common Agricultural Policy (CAP) ▪ Main figures of food and beverages manufacture ▪ From farm to fork bioeconomy strategies and sustainability ▪ Processing and preserving of meat and production of meat products ▪ Environmental footprint of the agri-food sector ▪ Processing and preserving of fish, crustaceans and molluscs ▪ Policy recommendations and SWOT analysis of the ▪ Processing and preserving of fruit and vegetables agri-food sector (p. -

FAGE INTERNATIONAL S.A. ANNUAL REPORT for the Year Ended December 31, 2020 March 24, 2021

FAGE INTERNATIONAL S.A. ANNUAL REPORT For the Year Ended December 31, 2020 March 24, 2021 This report (the “Annual Report”) includes the consolidated financial statements and other information of FAGE INTERNATIONAL S.A. and its subsidiaries (the “FAGE Group”) as of and for the year ended December 31, 2020. This Annual Report is being provided to holders of the Senior Notes pursuant to the requirements of the Indenture governing such Senior Notes. This report is organized as follows: Pages Section A: Summary analysis of Senior Notes issued by the Group and other related information. 2-7 Section B: Report of the Board of Directors. Risk Factors ....................................................................................................................................... 8-20 Selected Consolidated Financial Information ................................................................................. 21-22 Management’s Discussion and Analysis of Financial Condition and Results of Operations ...... 23-29 Our Industry ....................................................................................................................................... 30-34 Business .............................................................................................................................................. 35-41 Management ....................................................................................................................................... 42-44 Ownership of Share Capital .............................................................................................................. -

FAGE CASE STUDY in BRIEF Company-Wide Migration to .FAGE

CL dot brand case studies Oct 2020.qxp_Layout 1 14/09/2020 08:00 Page 1 .FAGE A recipe for success .FAGE CASE STUDY IN BRIEF Company-wide migration to .FAGE • Initiatives International dairy company, FAGE, boasts nearly 100 years of innovation1 in Localisation, simplified navigation manufacturing dairy products, including the iconic trend of Greek yoghurt, which began in the 1990s within the US. Now, it is making its mark in digital • Main model of use marketing, with the launch of its .FAGE TLD. Full migration, including internal domains FAGE, pronounced ‘fah-yeh’ (from the Greek ‘to eat’) has grown from its origins as a small dairy shop, opened in Athens, Greece in 1926, to an international dairy 2 • Key benefits company serving customers across 34 countries in Europe, the Americas, Asia, and Consumer trust, local language sites, Africa. Following its successful application for the dot brand gTLD .FAGE, in 2016 the domain name consolidation company migrated its entire internet presence over to .FAGE, including its websites and email. The company has domain name registrations under other TLDs, but they now redirect to the .FAGE domain; for example, FAGE.GR. Its main corporate website is now located at HOME.FAGE, and it uses MAIL.FAGE for corporate email. This is a significant move for such a large global organisation, and one which shows the value they place in their dot brand. HOME.FAGE FAGE is creating Notably, FAGE.COM is owned by a different company with the same name. This suggests that a motivation for FAGE in applying for their dot brand may have been keyword domains to the opportunity to move away from any complications relating to coexistence and direct consumers to conflicts over TLD registrations (especially as they don’t own FAGE.CO.UK), in favour of its own secure branded space. -

Participation of Greek Companies 16-20 October 2016

Greek Pavilions Are Exhibiting… 16-20 October 2016 3 Participation of Greek Companies 16-20 October 2016 EXHIBITOR Stand Page EXHIBITOR Stand Page NATIONAL PAVILIONS - HALL 1 GROCERY PRODUCTS - HALL 5b ALEXOPOULOS ALEXANDROS & CO 1 C 102 6 KARPEA S.A. 5b H 036 34 AGRONUTS S.A. – DRY NUTS & AGRICULTURAL PRODUCTS 1 C 122 8 KORVEL LTD. 5b N 119 35 ARISTIS - V. HALVATZIS & CO. S.A. 1 C 130 9 MENEXOPOULOS BROS CO. – ‘DRYFO’ 5b J 169 36 EPIRUS REGION 1 C 152 10-11 PNOE S.A. 5b H 036 37 FARMHOUSE S.A. 1 C 134 12 INECO LTD. 1 D 113 13 SDOUKOS S.A. 5b M 151 38 IRAKLIDIS K. & SONS S.A. - ‘PICANTO’ 1 D 121 14 TSATSAKIS S.A. 5b M 160 39 KAPETANIOS HALVA-HONEY 1 C 110 15 UNIHER S.A. 5b N 151 40 MAGNESIA CHAMBER OF COMMERCE 1 D 129 16-17 MELISSA KIKIZAS FOOD PRODUCTS S.A. 1 D 109 19 GOURMET - HALL 5b PETROPOULOS TH. & SON S.A. - ‘HELENA FOODS’ 1 C 100 20 GEODI S.A. 5b L 234 41 EL. RENIERIS & Co. 1 D 095 21 RIZOS NUTS S.A. 1 C 096 22 DAIRY PRODUCTS - HALL 7 SOYA HELLAS S.A. - ‘ELEON’ 1 D 099 23 DODONI S.A. 7 BC 184 42 SOUTH AEGEAN REGION 1 D 151 24-25 EPIRUS S.A. 7 C 101 43 THE CHIOS MASTIHA GROWERS ASSOCIATION 1 D 133 26 KOLIOS S.A. GREEK DAIRY 7 AB 019 44 KOUKAKIS FARM S.A. 7 C 111 45 CONFECTIONERY - HALL 5a DRAGEES HATZIYIANNAKIS S.A. -

Greece 10 Years Ahead: Defining the New Growth Model and Strategy for Greece – Retail Section Heading 1

Greece 10 years ahead: Defining the new growth model and strategy for Greece – Retail Section Heading 1 McKinsey&Company, Athens Office Greece 10 Years Ahead Defining Greece’s new growth model and strategy Executive summary March 2012 2 Greece 10 Years Ahead: Defining Greece’s new growth model and strategy — Executive summary Table of contents 3 Table of Contents Introduction 5 1. Overview 7 2. Greece’s unsustainable economic model to date 11 2.1. Persistent productivity and labor participation deficits 15 2.2. The underlying problems of the Greek economy 18 3. A new National Growth Model 27 4. Laying the foundations in key economic sectors 37 4.1. Major sectors 39 4.1.1. Tourism 3 9 4.1.2. Energy 43 4.1.3. Manufacturing - Food processing 46 4.1.4. Agriculture - Crops agriculture 51 4.1.5. Retail and wholesale 55 4.2. Rising Stars 59 4.2.1. Manufacturing of generic pharmaceuticals 61 4.2.2. Aquaculture 63 4.2.3. Medical tourism 64 4.2.4. Elderly care 66 4.2.5. Regional cargo hub development 67 4.2.6. Waste management 68 4.2.7. Secondary rising stars 69 4 Greece 10 Years Ahead: Defining Greece’s new growth model and strategy — Executive summary Introduction 5 Introduction Greece 10 Years Ahead is a study that aims to define a new growth model and strategy for economic development in Greece for the next 5 to 10 years, founded on the principles of competitiveness, productivity, extroversion, investment stimulation, and employment opportunities. To fulfill this purpose, Greece 10 Years Ahead analyzes the structure and development prospects of key economic sectors, and studies fundamental cross-sector macroeconomic drivers, challenges, and opportunities of the Greek economy. -

Made in Greece, Destined for the World

made in Greece, destined for the world a showcase of select greek products food & agricultural products Greece is a land of rugged mountains and azure blue seas, a Mediterranean climate and of a long and sto- ried past. Greek food products are an expression of this landscape and history: natural, healthy, timeless. The exceptional climate and varied landscape of Greece has resulted in an agricultural sector of ex- traordinary diversity − from fresh fruits and vegeta- food & bles, to baked goods and pastries, from olives and olive oil, to dairy products and cheeses, to herbs, spices, honeys and wines cultivated from ancient agricultural vintages known only in Greece. Greek cuisine is known worldwide for its natural and delicious flavors. And Greece is home to the world famous Mediterranean diet. Natural and nutritious, products Greek foods and ingredients may be the secret to a long and healthy life. Let’s not forget that Greece is one of five places on earth where people live longest. The Greek poet Odysseas Elytis once said: "If you dis- assemble Greece, in the end you will see that you are left with an olive tree, a vineyard and a ship.” Greece's fine food products bring the tastes of this eternal land to discerning connoisseurs around the world. wine an ancient tradition reaching new heights Over the last decade, Greek wines have meet (some of) the Greek varietals gained increasing international recog- nition for their high quality and unique Whites Robola [ro-BO-la] Reds accents. Greek winemakers take ad- Assyrtiko [a-SEER-tee-ko] The most important grape of Aghiorgitiko [a-gee-or-GEE-tee-ko] vantage of a wide variety of terroirs and The finest Greek white variety the Ionian Islands. -

1-4.Qxd (Page 1)

$21.50 d's Dairy Class III Prices orl In W du $20.50 Since 2005 e st h r t y $19.50 February in Red g W n i e $18.50 e v Since 1876 k r e l y S $17.50 $16.50 $15.50 $14.50 $13.50 CHEESE REPORTER $12.50 $11.50 Vol. 132, No. 35 • Friday, February 29, 2008 • Madison, Wisconsin $10.50 2005 2006 2007 2008 Alto Dairy Co-op Members USDA Proposes Class I Price Hike In Approve Sale Of Assets To Saputo Cheese USA Fond du Lac, WI—Alto Dairy Three Southeastern Federal Orders Cooperative announced Wednesday Citing Emergency Marketing Southeast orders: 25 percent of Appalachian order, approximately that its members have approved the Conditions, USDA Skips deliveries to pool plants during the $17.5 million for the Southeast sale of the co-op’s assets to Saputo order and approximately $38 million Recommended Decision months of January, February, July, Cheese USA Inc. for total consider- August, September, October and for the Florida order. ation of $160 million. Washington—The US Department November, and 35 percent for the In estimating the impact on min- The sale, which was unanimously of Agriculture (USDA) today pub- other five months. imum producer prices, blend prices approved by Alto’s board of directors lished a tentative final decision that •Reduce touch-base standards to will increase by about 26 cents per in January, was voted on and increases Class I prices in the one day each month for the hundredweight for the Appalachian approved by 98 percent of the co- Appalachian, Southeast and Florida Appalachian and Southeast orders.