2003 Hotel Market Overview China

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Chefsdemissionmanual YOG N

Chefs de Mission Manual Nanjing 2014 Summer Youth Olympic Games July 2014 Welcome Message from NYOGOC President Dear Chefs de Mission, The 2nd Summer Youth Olympic Games will open in Nanjing, China, on 16 August 2014. On behalf of the Nanjing Youth Olympic Games Organising Committee (NYOGOC), I would like to extend my sincere greetings to all the National Olympic Committees (NOCs) and offer you this Chefs de Mission Manual for Nanjing 2014 Summer Youth Olympic Games. With the invaluable guidance of both the International Olympic Committee (IOC) and the International Federations (IFs), and the great support of the NOCs, we have sought to put forward such concepts as youth and vigour, participation and sharing, cultural diversity and integration, wisdom and creativity, green energy and low-carbon emissions and safety and integrity, involving young people by giving them leading roles, and highlighting the importance of culture and education. Our aim is to stage a spectacular, high-quality event, which will encourage young people from around the world to “Share the Games, Share their Dreams”. As organiser of this global event, NYOGOC made the most of events such as the Chefs de Mission Seminar to listen to suggestions from NOCs and integrate them into the Chefs de Mission Manual, which compiles essential Games-related information, and policies and procedures in order to assist NOCs and to ensure their stay in Nanjing is both a pleasant and memorable one. Welcome to Nanjing! We hope our provision of top-quality facilities and an eco-friendly environment will guarantee the best services to young athletes and NOCs alike. -

Industrial Reform and Air Transport Development in China

INDUSTRIAL REFORM AND AIR TRANSPORT DEVELOPMENT IN CHINA Anming Zhang Department of Economics University of Victoria Victoria, BC Canada and Visiting Professor, 1996-98 Department of Economics and Finance City University of Hong Kong Hong Kong Occasional Paper #17 November 1997 Table of Contents Abstract ..................................................................... i Acknowledgements ............................................................ i I. INTRODUCTION .........................................................1 II. INDUSTRIAL REFORM ....................................................3 III. REFORMS IN THE AIRLINE INDUSTRY .....................................5 IV. AIR TRANSPORT DEVELOPMENT AND COMPETITION .......................7 A. Air Traffic Growth and Route Development ................................7 B. Market Structure and Route Concentration ................................10 C. Airline Operation and Competition ......................................13 V. CONCLUDING REMARKS ................................................16 References ..................................................................17 List of Tables Table 1: Model Split in Non-Urban Transport in China ................................2 Table 2: Traffic Volume in China's Airline Industry ...................................8 Table 3: Number of City-pair Routes in China's Airline Industry .........................8 Table 4: Overview of Chinese Airline Performance, 1980-94 ............................9 Table 5: Traffic Performed by China's Airlines -

AVIC AG600 "Kunlong"

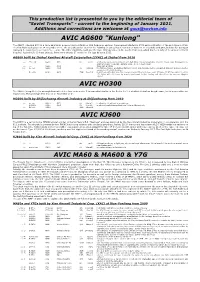

This production list is presented to you by the editorial team of "Soviet Transports" - current to the beginning of January 2021. Additions and corrections are welcome at [email protected] AVIC AG600 "Kunlong" The AG600 (Jiaolong 600) is a large amphibian powered by four Zhuzhou WJ6 turboprop engines. Development started in 2009 and construction of the prototype in 2014. The first flight took place on 24 December 2017. The aircraft can be used for fire-fighting (it can collect 12 tonnes of water in 20 seconds) and SAR, but also for transport (carrying 50 passengers over up to 5,000 km). The latter capability could give the type strategic value in the South China Sea, which has been subject to various territorial disputes. According to Chinese sources, there were already 17 orders for the type by early 2015. AG600 built by Zhuhai Yanzhou Aircraft Corporation (ZYAC) at Zhuhai from 2016 --- 'B-002A' AG600 AVIC ph. nov20 a full-scale mock-up; in white c/s with dark blue trim and grey belly, titles in Chinese only; displayed in the Jingmen Aviator Town (N30.984289 E112.087750), seen nov20 --- --- AG600 AVIC static test airframe 001 no reg AG600 AVIC r/o 23jul16 the first prototype; production started in 2014, mid-fuselage section completed 29dec14 and nose section completed 17mar15; in primer B-002A AG600 AVIC ZUH 30oct16 in white c/s with dark blue trim and grey belly, titles in Chinese only; f/f 24dec17; f/f from water 20oct18; 172 flights with 308 hours by may20; performed its first landing and take-off on the sea near Qingdao 26jul20 AVIC HO300 The HO300 (Seagull 300) is an amphibian with either four or six seats. -

Results Announcement for the Year Ended December 31, 2020

(GDR under the symbol "HTSC") RESULTS ANNOUNCEMENT FOR THE YEAR ENDED DECEMBER 31, 2020 The Board of Huatai Securities Co., Ltd. (the "Company") hereby announces the audited results of the Company and its subsidiaries for the year ended December 31, 2020. This announcement contains the full text of the annual results announcement of the Company for 2020. PUBLICATION OF THE ANNUAL RESULTS ANNOUNCEMENT AND THE ANNUAL REPORT This results announcement of the Company will be available on the website of London Stock Exchange (www.londonstockexchange.com), the website of National Storage Mechanism (data.fca.org.uk/#/nsm/nationalstoragemechanism), and the website of the Company (www.htsc.com.cn), respectively. The annual report of the Company for 2020 will be available on the website of London Stock Exchange (www.londonstockexchange.com), the website of the National Storage Mechanism (data.fca.org.uk/#/nsm/nationalstoragemechanism) and the website of the Company in due course on or before April 30, 2021. DEFINITIONS Unless the context otherwise requires, capitalized terms used in this announcement shall have the same meanings as those defined in the section headed “Definitions” in the annual report of the Company for 2020 as set out in this announcement. By order of the Board Zhang Hui Joint Company Secretary Jiangsu, the PRC, March 23, 2021 CONTENTS Important Notice ........................................................... 3 Definitions ............................................................... 6 CEO’s Letter .............................................................. 11 Company Profile ........................................................... 15 Summary of the Company’s Business ........................................... 27 Management Discussion and Analysis and Report of the Board ....................... 40 Major Events.............................................................. 112 Changes in Ordinary Shares and Shareholders .................................... 149 Directors, Supervisors, Senior Management and Staff.............................. -

Nanjing 2011 Cultivating Morality International Conference

CONFERENCE INFORMATION Finding your way to the conference hotel If you plan to take a taxi from Nanjing International Airport, show this card to the driver: Please take me directly to the Nanjing International Conference Centre Hotel. 请您将我带到南京国际会议大酒店 Address: 2 Sifangcheng, Zhongshan Ling, Nanjing, China 地址:南京市玄武区陵园路中山陵四方城2号 Phone: (+86)-25-84430888 Depending on traffic conditions, I understand the journey will take about 50 minutes and will cost around 150 Yuan. 据我所知从机场到南京国际会议大酒店大概要50分钟, 打车费用是150元左右 If you plan to take a taxi from Nanjing Train Station, show this card to the driver: Please take me directly to the Nanjing International Conference Centre Hotel. 请您将我带到南京国际会议大酒店 Address: 2 Sifangcheng, Zhongshan Ling, Nanjing, China 地址:南京市玄武区陵园路中山陵四方城2号 Phone: (+86)-25-84430888 Depending on traffic conditions, I understand the journey will take about 10-15 minutes and will cost about 20 Yuan. 据我所知从火车站到南京国际会议大酒店大概要10-15 分钟, 打车费用是20元左右 Emergency Contact Numbers Upon your arrival in Nanjing, you may call for assistance at the following numbers: WANG Qiang:13951842310; LIU Sunyuan:13951783669; JIN Shenghong: 13512508998 Hotel reception: (+86)-25-84430888-8 Nanjing Local Organising Committee Office Address: Research Institute of Moral Education, Nanjing Normal University, Ninghai Road No.122, Nanjing, Jiangsu, P. R. China Email: [email protected] Phone: (+86)-25-83598304 (Chinese and English) Fax: (+86)-25- 83721092 Mobile Phones The use of mobile phones is not permitted during the academic or cultural programmes as it is extremely disturbing to the presenters and participants. Please ensure that your mobile phone is switched off during all the sessions of the academic and cultural programmes. Filming and Photography Please note that some sessions or parts of the conference may be photographed or filmed. -

Journal of Current Chinese Affairs

China Data Supplement March 2007 J People’s Republic of China J Hong Kong SAR J Macau SAR J Taiwan ISSN 0943-7533 China aktuell Data Supplement – PRC, Hong Kong SAR, Macau SAR, Taiwan 1 Contents The Main National Leadership of the PRC 2 LIU Jen-Kai The Main Provincial Leadership of the PRC 30 LIU Jen-Kai Data on Changes in PRC Main Leadership 37 LIU Jen-Kai PRC Agreements with Foreign Countries 45 LIU Jen-Kai PRC Laws and Regulations 48 LIU Jen-Kai Hong Kong SAR 51 Political, Social and Economic Data LIU Jen-Kai Macau SAR 58 Political, Social and Economic Data LIU Jen-Kai Taiwan 62 Political, Social and Economic Data LIU Jen-Kai ISSN 0943-7533 All information given here is derived from generally accessible sources. Publisher/Distributor: GIGA Institute of Asian Studies Rothenbaumchaussee 32 20148 Hamburg Germany Phone: +49 (0 40) 42 88 74-0 Fax: +49 (040) 4107945 2 March 2007 The Main National Leadership of the PRC LIU Jen-Kai Abbreviations and Explanatory Notes CCP CC Chinese Communist Party Central Committee CCa Central Committee, alternate member CCm Central Committee, member CCSm Central Committee Secretariat, member PBa Politburo, alternate member PBm Politburo, member BoD Board of Directors Cdr. Commander CEO Chief Executive Officer Chp. Chairperson COO Chief Operating Officer CPPCC Chinese People’s Political Consultative Conference CYL Communist Youth League Dep.Cdr. Deputy Commander Dep. P.C. Deputy Political Commissar Dir. Director exec. executive f female Gen.Man. General Manager Hon.Chp. Honorary Chairperson Hon.V.-Chp. Honorary Vice-Chairperson MPC Municipal People’s Congress NPC National People’s Congress PCC Political Consultative Conference PLA People’s Liberation Army Pol.Com. -

III. Status Quo of Capitalized Operation of China's Exhibition

Annual Report on China's Exhibition Economy (2019) Annual Report on China's Exhibition Economy (2019) Organizer: China Council for the Promotion of International Trade (CCPIT) Publisher Department of Trade and Investment Promotion of China Council for the Promotion of International Trade Academy of China Council for the Promotion of International Trade Chief Editorial Board Director: Zhang Shenfeng Vice Chairman of China Council for the Promotion of International Trade Deputy Director: Feng Yaoxiang Director, Department of Trade and Investment Promotion, CCPIT Ruan Wei Deputy Director, Department of Trade and Investment Promotion, CCPIT Zhou Tong Deputy Inspector, Department of Trade and Investment Promotion, CCPIT Lu Ming Vice Chairman of Academy of China Council for the Promotion of International Trade Executive Editorial Board Director: Zhang Shujing Chief, Exhibition and Conference Division, Department of Trade and Investment Promotion, CCPIT Liu Yingkui Director of Department of International Investment Research, Academy of China Council for the Promotion of International Trade Coordinator:Wang Jianjun, Dun Zhigang Business Support: Department of Trade and Investment Promotion, CCPIT: Zhou Jianxiu, Zhu Yingmin, Zhang Bo, Cao Yongping, Duan Jianrong, Fang Ke, Yuan Fang, Wang Jianjun, Liu Yujia Academy of China Council for the Promotion of International Trade: Liu Yingkui, Wan Xiaoguang, Dun Zhigang, Li Yuan, Wu Wenjun Information Department of China International Exhibition Center Group Corporation: Yuan Hang, Zhang Xi, Zhang Qian -

Thëse Docteur De L'université De Grenoble

THÈSE Pour obtenir le grade de DOCTEUR DE L’UNIVERSITÉ DE GRENOBLE Spécialité : Science de Geston Arrêté ministériel : 7 août 2006 Présentée par Wang Yong Thèse dirigée par Jacques TRAHAND et codirigée par Yuyinchuan YU préparée au sein du Laboratoire CNRS CERAG dans l'École Doctorale Science Gestion L'identification et l'étude d'évaluation sur le risque de stratégie des compagnies aériennes chinoises Thèse soutenue publiquement le 15 Octobre 2012 devant le jury composé de : Mr Charles MARTINET Professeur à l’IAE de Lyon, Rapporteur Mr Yuyinchuan Professeur à l’Institut de Recherche de Shanghai, Rapporteur Mr Alain SPALANZANI Professeur à l’Université Pierre Mendès France, Président M Jacques TRAHAND Professeur à l’Université Pierre Mendès France, Directeur de thèse Université Joseph Fourier / Université Pierre Mendès France / Université Stendhal / Université de Savoie / Grenoble INP ABSTRACT Nowadays, enterprises are facing more changes ˈ uncertainties but airlines companies are facing the greatest challenges. There is no systemic and comprehensive researches on the strategy risk in airline industry. Thus this article mainly studies strategy management from the risk perspective. There are three main parts. Firstly, this article proposed one strategy risk factors identification system for Chinese airlines companies based on the strategy position, strategy choice and strategy implementation. Work-risk analysis and expert interview were used to extract 16 strategy risks, and then the transformation conditions from strategy risk factors to strategy risks were analyzed. In the second part, ANP was used to get the weights for 16 strategy risks, and then the airline industry strategy risk levels were evaluated in three layers, strict control layer, control layer and watching layer. -

UNITED STATES BANKRUPTCY COURT Southern District of New York *SUBJECT to GENERAL and SPECIFIC NOTES to THESE SCHEDULES* SUMMARY

UNITED STATES BANKRUPTCY COURT Southern District of New York Refco Capital Markets, LTD Case Number: 05-60018 *SUBJECT TO GENERAL AND SPECIFIC NOTES TO THESE SCHEDULES* SUMMARY OF AMENDED SCHEDULES An asterisk (*) found in schedules herein indicates a change from the Debtor's original Schedules of Assets and Liabilities filed December 30, 2005. Any such change will also be indicated in the "Amended" column of the summary schedules with an "X". Indicate as to each schedule whether that schedule is attached and state the number of pages in each. Report the totals from Schedules A, B, C, D, E, F, I, and J in the boxes provided. Add the amounts from Schedules A and B to determine the total amount of the debtor's assets. Add the amounts from Schedules D, E, and F to determine the total amount of the debtor's liabilities. AMOUNTS SCHEDULED NAME OF SCHEDULE ATTACHED NO. OF SHEETS ASSETS LIABILITIES OTHER YES / NO A - REAL PROPERTY NO 0 $0 B - PERSONAL PROPERTY YES 30 $6,002,376,477 C - PROPERTY CLAIMED AS EXEMPT NO 0 D - CREDITORS HOLDING SECURED CLAIMS YES 2 $79,537,542 E - CREDITORS HOLDING UNSECURED YES 2 $0 PRIORITY CLAIMS F - CREDITORS HOLDING UNSECURED NON- YES 356 $5,366,962,476 PRIORITY CLAIMS G - EXECUTORY CONTRACTS AND UNEXPIRED YES 2 LEASES H - CODEBTORS YES 1 I - CURRENT INCOME OF INDIVIDUAL NO 0 N/A DEBTOR(S) J - CURRENT EXPENDITURES OF INDIVIDUAL NO 0 N/A DEBTOR(S) Total number of sheets of all Schedules 393 Total Assets > $6,002,376,477 $5,446,500,018 Total Liabilities > UNITED STATES BANKRUPTCY COURT Southern District of New York Refco Capital Markets, LTD Case Number: 05-60018 GENERAL NOTES PERTAINING TO SCHEDULES AND STATEMENTS FOR ALL DEBTORS On October 17, 2005 (the “Petition Date”), Refco Inc. -

China's Airline Deregulation Since 1997 and the Driving Forces Behind

CORE Metadata, citation and similar papers at core.ac.uk Provided by University of Southern Queensland ePrints China’s airline deregulation since 1997 and the driving forces behind the 2002 airline consolidations Yahua Zhanga,*, David K. Rounda aCentre for Regulation and Market Analysis, School of Commerce, University of South Australia, Adelaide, SA 5000, Australia *Corresponding author. E-mail address: [email protected] Phone: +61 8 830 20601 Fax: +61 8 830 27001 Abstract: This paper seeks to document and describe events in the last decade in China’s airline markets, and to clarify some misunderstandings in regard to the 2002 airline consolidations that brought sweeping changes to China’s aviation markets. Some possible reasons for the 2002 consolidations are inferred through analysing the numbers and facts of the late 1990s and early 2000s. We conclude that the consolidations may be a natural response to the changes that accompanied airline deregulation in China. Keywords: Deregulation, airline mergers, China 1. Introduction China’s airline markets have attracted the attention of many major international carriers, but have largely failed to attract the attention of academics. Literature on China’s airline markets remains relatively sparse, owing to the country’s opacity in aviation policies and the limitations of data availability. The dramatic changes that took place in China’s airline industry in the past 20 years, from a period of strict regulation and control to being relatively uncontrolled and loosely supervised, resulted in chaotic and unexpected outcomes. Those within the industry had two opposing attitudes towards these changes: some applauded them and called for further reforms, while others resisted and demanded a return to regulation. -

Chefs De Mission Manual Nanjing 2014 Summer Youth Olympic Games

Chefs de Mission Manual Nanjing 2014 Summer Youth Olympic Games July 2014 Welcome Message from NYOGOC President Dear Chefs de Mission, The 2nd Summer Youth Olympic Games will open in Nanjing, China, on 16 August 2014. On behalf of the Nanjing Youth Olympic Games Organising Committee (NYOGOC), I would like to extend my sincere greetings to all the National Olympic Committees (NOCs) and offer you this Chefs de Mission Manual for Nanjing 2014 Summer Youth Olympic Games. With the invaluable guidance of both the International Olympic Committee (IOC) and the International Federations (IFs), and the great support of the NOCs, we have sought to put forward such concepts as youth and vigour, participation and sharing, cultural diversity and integration, wisdom and creativity, green energy and low-carbon emissions and safety and integrity, involving young people by giving them leading roles, and highlighting the importance of culture and education. Our aim is to stage a spectacular, high-quality event, which will encourage young people from around the world to “Share the Games, Share their Dreams”. As organiser of this global event, NYOGOC made the most of events such as the Chefs de Mission Seminar to listen to suggestions from NOCs and integrate them into the Chefs de Mission Manual, which compiles essential Games-related information, and policies and procedures in order to assist NOCs and to ensure their stay in Nanjing is both a pleasant and memorable one. Welcome to Nanjing! We hope our provision of top-quality facilities and an eco-friendly environment will guarantee the best services to young athletes and NOCs alike. -

Notice of the Egm

Hong Kong Exchanges and Clearing Limited, The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. (A joint stock company incorporated in the People’s Republic of China with limited liability under the Chinese corporate name and carrying on business in Hong Kong as HTSC) (Stock Code: 6886) NOTICE OF THE EGM NOTICE IS HEREBY GIVEN that the EGM of the Company will be held at Conference room, Renaissance Nanjing Olympic Centre Hotel, 139 Aoti Street, Jianye District, Nanjing, Jiangsu Province, the PRC on Monday, February 8, 2021 at 2:00 p.m., to consider the following issues: ORDINARY RESOLUTION 1. To consider and approve the resolution on the election of Mr. Ke Xiang as a non-executive Director of the fifth session of the Board SPECIAL RESOLUTIONS 2. To consider and approve the resolution on the general mandate to issue onshore and offshore debt financing instruments of the Company 3. To consider and approve the resolution on amendments to the Rules of Procedure for General Meeting of Huatai Securities Co., Ltd. 4. To consider and approve the resolution on the Restricted Share Incentive Scheme of A Shares (Draft) and its Summary 5. To consider and approve the resolution on the Administrative Measures for the Restricted Share Incentive Scheme of A Shares 6.