Cj E&M (130960)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

30, 1981 Evefy Thuridajr 26 Pages—25 Cents 11 Wwfcu.N.1

O O\ o oc- c< : <Q 2 m o - M a Q THE WESTFIELD LEADER o J The Leading and Most Widely Circulated Weekly Newspaper In Union County Publ[ih«d NINETY-FIRST YEAR, NO. 39 S^-ood Cbn PnUft PM WESTFIELD. NEW JERSEY,.THURSDAY, APRIL 30, 1981 Evefy Thuridajr 26 Pages—25 Cents 11 WWfcU.N.1. Y Official Balks at Town Another Sidewalk Battle Looms The battle of the Earl Lambert. project is needed to provide by the opponents is the Fairmont Ave., one of more sidewalks leading to Similar dissention oc- safe access for the walk to possibility of converting the than a dozen speakers at the Competition in Camp Market Washington School has been curred about a year ago Washington School and school system to a middle - public hearing on the or- revived—this year on the when council eventually opponents claiming their school concept which would dinance. "We don't need the Summer sports camps compete with the cost," he Jeremiah said he feared southeast side of St. Marks agreed to put sidewalks on own surveys do not warrant eliminate the two upper "Safety starts at home," Recreation Commission as a would emanate to make the said. the entrance of the Ave. between South South Chestnut St., and the the walks and subsequent grades in elementary replied Fred Gould of 716 St. competitor," William camps self-supporting and The Recreation Com- recreation' commission, or Chestnut and Sherman Sts. neighborhood was split on disruption to their schools and reduce Marks Ave. "Cost is not a Jeremiah toM Mayor Allen not dependent on tax mission proposes among its the "public factor," into a Originally scheduled for the issue. -

New Paradigm in Cinema Industry CJ 4DX : What Is 4DX?

4DX’s Challenge for Global Hallyu Creation Presenter: Byung-Hwan Choi CEO / CJ 4DPLEX Hallyu, at the Extension Stage 1980s 1990s 2000~ Cultural Hong Kong Japan Korea Trend In Asia Hong Kong Noir Movies Manga, Games, J-Pops Soap Operas, K-Pops, Games, Movies… Initial Before Hallyu stage Leaping Stage Extension Stage Revenue $Bil What is “Hallyu”? Highest Profit 1.2 Hallyu, the Korean Wave, is a Record neologism referring to the increase in the worldwide popularity of 1.0 <Dae Jang Geum> South Korean culture. First Hallyu 0.8 Culture 0.6 Export Culture Import Psy, 0.4 H.O.T Heyday of K-Pop debut in China 0.2 1980 1984 1988 1992 1996 2000 2004 2008 2012 Source: SERI Report (June 19, 2013) 1 CJ, Korea’s Leading Culture Creator CJ’s Hallyu Philosophy as Global Lifestyle company : 3 2 CJ Group, Business Portfolio Global CJ Foodville Global Bio Production Global CJ O Shopping Global CGV 184 stores in 10 countries Brazil, China, Indonesia, China, Indian, Japan, USA, China, Vietnam, Global bibigo Malaysia, USA Philippines, Thailand, Malaysia, Indonesia USA, China, UK, Japan, Turkey, Vietnam Singapore, Indonesia 3 CJ Group, Business Portfolio Sales by Year ($ Bil) 2013 9.2 2012 8.9 2011 8.2 2010 6.9 Weight of overseas sales as % of total sales 4 CJ Group, Business Portfolio Sales by Year ($ Bil) 2017 (exp) 5.0 2012 1.8 2011 1.5 2010 1.2 5 CJ Group, Business Portfolio CJ O Shopping Sales by Year ($ Bil) 2013 2.7 2012 2.5 2011 2.3 2010 1.8 CJ Korea Express CJ O SHOPPING GLOBAL BUSINESS 6 CJ Group, Business Portfolio PR Value from CJ’s Hallyu festivals - MAMA (Mnet Asia Music Awards) 2013 = 2.6 Bil - KCON 2014 = 36 Mil CJ E&M Sales by Year ($ Bil) 2013 1.6 2012 1.3 2011 1.2 CJ CGV & HelloVision Sales by Year ($ Bil) 2013 1.9 2012 1.5 2011 1.2 7 At the Center of Global Movie Industry Global Trends in Movie Industry Global Cinema Industry In Korea, cinema box office and attendance is continuously increasing since 2010. -

The K-Pop Wave: an Economic Analysis

The K-pop Wave: An Economic Analysis Patrick A. Messerlin1 Wonkyu Shin2 (new revision October 6, 2013) ABSTRACT This paper first shows the key role of the Korean entertainment firms in the K-pop wave: they have found the right niche in which to operate— the ‘dance-intensive’ segment—and worked out a very innovative mix of old and new technologies for developing the Korean comparative advantages in this segment. Secondly, the paper focuses on the most significant features of the Korean market which have contributed to the K-pop success in the world: the relative smallness of this market, its high level of competition, its lower prices than in any other large developed country, and its innovative ways to cope with intellectual property rights issues. Thirdly, the paper discusses the many ways the K-pop wave could ensure its sustainability, in particular by developing and channeling the huge pool of skills and resources of the current K- pop stars to new entertainment and art activities. Last but not least, the paper addresses the key issue of the ‘Koreanness’ of the K-pop wave: does K-pop send some deep messages from and about Korea to the world? It argues that it does. Keywords: Entertainment; Comparative advantages; Services; Trade in services; Internet; Digital music; Technologies; Intellectual Property Rights; Culture; Koreanness. JEL classification: L82, O33, O34, Z1 Acknowledgements: We thank Dukgeun Ahn, Jinwoo Choi, Keun Lee, Walter G. Park and the participants to the seminars at the Graduate School of International Studies of Seoul National University, Hanyang University and STEPI (Science and Technology Policy Institute). -

Cj Logistics Sustainability Report 2018-2019

CJ LOGISTICS SUSTAINABILITY REPORT 2018-2019 REPORT SUSTAINABILITY LOGISTICS CJ This report is printed on FSC™(Forest Stewardship Council) Certified paper with soy ink. CJ LOGISTICS SUSTAINABILITY REPORT 2018-2019 FORWARDING & INTERNATIONAL EXPRESS STEVEDORING & TRANSPORTATION CONTRACT LOGISTICS PROJECT LOGISTICS PARCEL www.cjlogistics.com ABOUT THIS REPORT CONTENTS 04 CEO Message SUSTAINABILITY AROUND THE GLOBE 54 USA Summary BUSINESS OVERVIEW 56 China CJ Logistics publishes a sustainable management report each year to 08 CJ Management Philosophy 58 India transparently disclose its economic, social, and environmental activities 09 About Us 60 Vietnam and achievements. We plan to publish a sustainable management report every year as a communication tool for stakeholders to reflect 11 Our Business 62 Others and maintain steady growth. 18 Global Network SUSTAINABILITY MANAGEMENT Reporting Period and Scope SUSTAINABILITY ISSUES 66 Corporate Governance This is a report on the key sustainable management performance 22 Business Performance 68 Risk Management during the period between January 1, 2018 to June 30, 2019. It includes 28 Safety and Health 70 Customer Satisfaction quantitative performance data from the most recent three years or 34 Environmental Management 72 Information Security more to identify trends. Some important information include details 74 Compliance from up to the second half of 2019 to facilitate your understanding. The SUSTAINABILITY FUNDAMENTALS 76 Human Rights report covers all work sites of CJ Logistics in Korea. Some information 77 Stakeholder Engagement from overseas work sites are also included. 40 Employees 78 Materiality Assessment 45 Partners 80 UN SDGs Report Preparation Standards 48 Community This report has been prepared in accordance with the Core Option of the Global Reporting Initiative (GRI) Standards, which is a standard for international reporting of sustainable management. -

Showboxatcannes 2011

SHOWBOX AT CANNES 2011 CONTACT IN CANNES LERINS R3-S2 T +33 (0)4 92 99 33 26 EXECUTIVE ATTENDEES Judy AHN Head of Int’l Business • Sales & Acquisitions M +33 (0)6 76 22 89 41 E [email protected] SooJin JUNG General Manager • Sales M +33 (0)6 88 02 04 61 E [email protected] Sonya KIM Manager • Sales & Festival M +33 (0)6 08 50 72 51 E [email protected] June LEE Manager • Acquisitions M +33 (0)6 72 64 91 26 E [email protected] Eugene KIM Int’l Marketing M +33 (0)6 74 61 63 95 E [email protected] HIGHLIGHTS THE YELLOW SEA Genre Action, Thriller Running Time 140 min (International Version) Release Date Dec 23, 2010 Directed by NA Hong-jin (THE CHASER) Starring HA Jung-woo (THE CHASER / TAKE OFF) KIM Yun-seok ( T H E C H A S E R / W O O C H I ) Co-presented by Showbox / Mediaplex Fox International Productions On the Chinese side of Chinese-Russian-North Korean border, there is a region where North Korea, China and Russia meet is known as Yanbian Korean Autonomous Prefecture. The film tells a story of a man from here, who embarks on an assassination mission to South Korea in order to pay off his mounting debt. He is only given some money in advance and takes on the job without knowing much about his target. However, he is endangered by a FESTIVAL / MARKET SCREENINGS series of conspiracy and betrayal, and eventually realizes that he is TO BE ANNOUNCED tricked into a vicious trap. -

A Study on the Foodservice Industry in Korea

CORE Metadata, citation and similar papers at core.ac.uk Provided by KDI School Archives A STUDY ON THE FOODSERVICE INDUSTRY IN KOREA: BY Sojung Heo THESIS Submitted to KDI School of Public Policy and Management In partial fulfillment of the requirements For the degree of MASTER OF BUSINESS ADMINISTRATION 2003 A STUDY ON THE FOODSERVICE INDUSTRY IN KOREA: BY Sojung Heo THESIS Submitted to KDI School of Public Policy and Management In partial fulfillment of the requirements For the degree of MASTER OF BUSINESS ADMINISTRATION 2003 Professor Seung-Joo Lee Copyright by Sojung Heo 2003 ABSTRACT A STUDY ON THE FOODSERVICE INDUSTRY IN KOREA: BY Sojung Heo In spite of the short history of family restaurant in Korea, the industry has achieved robust growth for last 15 years. It has been changing the landscape of the whole foodservice industry by forming new eating-out culture as well as by expanding the market volume of foodservice industry. Initially, the substantial growth has been driven by social, cultural and economical changes such as busier lifestyle, westernization of eating pattern and increase of income level in a booming economy. Then after the Korean financial crisis, the industry as a whole has chased undifferentiated growth strategy to survive under severe competition. However, profitability has been deteriorated because the growth stemmed from multi-store strategy. While most of the family restaurant companies have been focusing on volume without profits leading to financial difficulties, some successful players have captured the market by leveraging their core competence and have evolved from the second movers to market leaders. -

Download and Upload Speeds for Any Individual Device That Is Connected to the Network

UC Irvine UC Irvine Electronic Theses and Dissertations Title Acceleration and Information: Managing South Korean Online Gaming Culture Permalink https://escholarship.org/uc/item/2204k0wv Author Rea, Stephen Campbell Publication Date 2015 Peer reviewed|Thesis/dissertation eScholarship.org Powered by the California Digital Library University of California UNIVERSITY OF CALIFORNIA, IRVINE Acceleration and Information: Managing South Korean Online Gaming Culture DISSERTATION submitted in partial satisfaction of the requirements for the degree of DOCTOR OF PHILOSOPHY in Anthropology by Stephen C. Rea Dissertation Committee: Associate Professor Keith M. Murphy, Chair Professor Tom Boellstorff Professor Bill Maurer 2015 © 2015 Stephen C. Rea TABLE OF CONTENTS Page ACKNOWLEDGEMENTS iii CURRICULUM VITAE v ABSTRACT OF THE DISSERTATION vi CHAPTER 1: Playing at the Speed of Life: Korean Online Gaming Culture and the 1 Aesthetic Representations of an Advanced Information Society CHAPTER 2: “Slow to Industrialize, but Let’s Lead in Informatization”: The Korea 31 Information Infrastructure, the IMF, and Online Games CHAPTER 3: Situating Korean Online Gaming Culture Offline 71 CHAPTER 4: Managing the Gap: The Temporal, Spatial, and Social Entailments of 112 Playing Online Games CHAPTER 5: Crafting Stars: e-Sports and the Professionalization of Korean Online 144 Gaming Culture CHAPTER 6: “From Heroes to Monsters”: “Addiction” and Managing Online Gaming 184 Culture CONCLUSION 235 BIBLIOGRAPHY 242 ii ACKNOWLEDGEMENTS This dissertation would not have been -

Understanding Korean Society Through Popular Music

Situations Vol. 5 (Winter 2011) © 2011 by Yonsei University Hannah N. Bergen (Yonsei University, Seoul) Understanding Korean Society through Popular Music Today one of the most unique aspects of inter-Asian cultural sharing is the hallyu wave. This social phenomenon began in Seoul, South Korea and today accounts for the all pervasive nature of Korean popular entertainment dominating the airwaves of nearly every Asian country. From Japan to Thailand, “K-pop” has conquered the Asian market, and is now turning its attention to the rest of the world. In order to illustrate this current social phenomenon, I have found many sources that all point to the same aspects in K-pop which have allowed one small country to make their entertainment business one of its most lucrative exports. The hallyu wave as a whole has become a blending of uniquely Korean culture with aspects of Western and other Asian cultures which has created a style unique to this particular moment of history. In the words of Sun Jung, author of the article “Korean Masculinities and Transcultural Consumption: Yonsama, Rain, Oldboy, K-Pop Idols,” “Transcultural hybridity is one of the most significant aspects of contemporary South Korean popular culture in the postmodern era and is the main driving force behind its overseas popularity” (Jung 166). This combination has allowed the music and film from Korea to be extremely accessible to a wide audience of various nationalities and languages. In order to clearly illustrate the international success of hallyu, I will focus on one specific aspect of current Korean popular culture: music. -

CHAPTER I INTRODUCTION I.I Background of the Study By

CHAPTER I INTRODUCTION I.I Background of the Study By language, people can express their feeling by using words in their own language. People can express their feeling by using language then write it into a beautiful and meaningful word to make a song by its lyric. Lyrics in every song could have implicit or explicit meaning based on the use of words. A language is consisting of all the sounds, words, and infinitely many possible sentences, when you know language you know the sounds, the words, and the rules for their combination (Fromkin, Rodman.et.al: 2003). Language is a system of conventional spoken or written symbols used by people nowadays to communicate with each other.According to American dictionary Language is a system of communication by speaking, writing, or making signs in a way that can be understood, or any of the different systems of communication used in particular regions. According to Cambridge Dictionary language is a system of communication consisting of sounds, words, and grammar, or the system of communication used by people in a particular country or type of work . People need language to communicate, to interact and to get information from other people (Khadijah, Arifah: 2016). 1 Estimates of the number of languages in the world vary between 6,000 and 7,000. However, it is expected to succeed in an arbitrary change that might occur a mixture of language and dialect. Natural language is conversation or language, but each language can be encoded into media that uses audio, visual, or tactile stimuli, for example, graphic writing, braille, or whistling. -

Kim Min Young Dating

Aug 02, · Park Min Young has shared her thoughts on her rumored romance with her “What’s Wrong with Secretary Kim” co-star Park Seo Joon. On August 1, . Feb 05, · Kim Ji-min’s Boyfriend. Kim Ji-min is single. She is not dating anyone currently. Kim had at least 1 relationship in the past. Kim Ji-min has not been previously engaged. She dated fellow comedian Yoo Sangmoo between and According to our records, she has no renuzap.podarokideal.ruality: South Korean. May 20, · kim ji won for park seo joon!!!!! their chemistry is super good and by the way i can see that many ppl in the comment section voted for pmy, well min young is . Hyun Young. Kim Jong-min and Hyun Young were in a relationship from until Hyun Young is a multi-talented celebrity, that has worked as a model, actress, MC, and even singer. Not much is known as to why they broke up, but was the year Kim was in the military, and Hyun Young was busy with her career. Sep 28, · “Heart Signal Season 1” car racer contestant Seo Joo Won will be tying the knot with model and television personality Kim Min Young. “Heart Signal” is a dating . Who is she dating right now? According to our records, Min-jung Kim is possibly single. Relationships. Min-jung Kim has been in a relationship with Dong-geon Lee ( - ).. About. Min-jung Kim is a 37 year old South Korean Actress born on 30th July, in Seoul, South Korea. Her zodiac sign is Leo. -

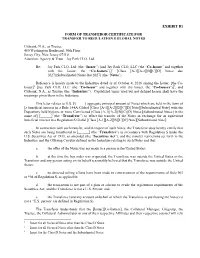

Exhibit B1 Form of Transferor Certificate for Transfer

EXHIBIT B1 FORM OF TRANSFEROR CERTIFICATE FOR TRANSFER TO REGULATION S GLOBAL NOTES Citibank, N.A., as Trustee 480 Washington Boulevard, 30th Floor Jersey City, New Jersey 07310 Attention: Agency & Trust—Jay Park CLO, Ltd. Re: Jay Park CLO, Ltd. (the “Issuer”) [and Jay Park CLO, LLC (the “Co-Issuer” and together with the Issuer, the “Co-Issuers”)]1 [Class [A-1][A-2][B][C][D] Notes due 2027][Subordinated Notes due 2027] (the “Notes”) Reference is hereby made to the Indenture dated as of October 4, 2016 among the Issuer, [the Co- Issuer]2 [Jay Park CLO, LLC (the “Co-Issuer” and together with the Issuer, the “Co-Issuers”)]3, and Citibank, N.A., as Trustee (the “Indenture”). Capitalized terms used but not defined herein shall have the meanings given them in the Indenture. This letter relates to U.S. $[_____] aggregate principal amount of Notes which are held in the form of [a beneficial interest in a Rule 144A Global [Class [A-1][A-2][B][C][D] Note][Subordinated Note] with the Depository held by][one or more Certificated [Class [A-1][A-2][B][C][D] Notes][Subordinated Notes] in the name of] [______] (the “Transferor”) to effect the transfer of the Notes in exchange for an equivalent beneficial interest in a Regulation S Global [Class [A-1][A-2][B][C][D] Note][Subordinated Note]. In connection with such transfer, and in respect of such Notes, the Transferor does hereby certify that such Notes are being transferred to [______] (the “Transferee”) in accordance with Regulation S under the U.S. -

C NTENT 2018 L

17-30 SEPTEMBER C NTENT 2018 www.contentasia.tv l www.contentasiasummit.com Sony kicks off new HBO counts down to 7 Oct horror debut AGT season Series goes live with int’l film fest stamp of approval David Foster, Anggun & Jay Park return Folklore: Tatami (Japan) David Foster, Anggun and Jay Park Three international film festivals – includ- Ratanaruang (Samui Song). Sony Pictures Television Networks Asia ing the Toronto International Film Festival Folklore: A Mother’s Love is about a kicked off the third season of Asia’s Got (TIFF) – have given their stamp of ap- single mother and her young son who Talent at the weekend with a Facebook proval to HBO Asia’s original Asian horror discover dirty and underfed children liv- Live judges session at the Pinewood Is- series, Folklore, which premieres on the ing in a mansion’s attic. Returning them kandar Malaysia Studios. All three judges regional service on Sunday, 7 October to their families stirs the wrath of their from last year – David Foster, Anggun and at 10pm. adopted mother, Wewe Gombel. Jay Park – are back, along with hosts Alan The six episodes of the anthology, each Folklore: Pob is about a journalist who Wong and Justin Bratton. helmed by a different director, debuted meets with Thai ghost Pob, who con- The show airs on AXN across Asia in in pairs at three festivals. In addition fesses to a murder. Finally finding an early 2019. to TIFF, which wrapped this weekend, outlet for complaint, Pob explains how The announcement of this year’s judges episodes will screen at Spain’s SITGES the murder happened.