Annual Report 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

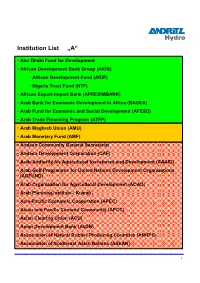

Institution List „A“

Institution List „A“ • Abu Dhabi Fund for Development • African Development Bank Group (AfDB) • African Development Fund (AfDF) • Nigeria Trust Fund (NTF) • African Export-Import Bank (AFREXIMBANK) • Arab Bank for Economic Development in Africa (BADEA) • Arab Fund for Economic and Social Development (AFESD) • Arab Trade Financing Program (ATFP) • Arab Maghreb Union (AMU) • Arab Monetary Fund (AMF) • Andean Community General Secretariat • Andean Development Corporation (CAF) • Arab Authority for Agricultural Investment and Development (AAAID) • Arab Gulf Programme for United Nations Development Organizations (AGFUND) • Arab Organization for Agricultural Development (AOAD) • Arab Planning Institute - Kuwait • Asia-Pacific Economic Cooperation (APEC) • Asian and Pacific Coconut Community (APCC) • Asian Clearing Union (ACU) • Asian Development Bank (AsDB) • Association of Natural Rubber Producing Countries (ANRPC) • Association of Southeast Asian Nations (ASEAN) 1 Institution List „B-C“ • Bank of Central African States (BEAC) • Central Bank of West African States (BCEAO) • Common Market for Eastern and Southern Africa (COMESA) • Baltic Council of Ministers • Bank for International Settlements (BIS) • Black Sea Trade and Development Bank (BSTDB) • Caribbean Centre for Monetary Studies (CCMS) • Caribbean Community (CARICOM) • Caribbean Development Bank (CDB) • Caribbean Regional Technical Assistance Centre (CARTAC) • Center for Latin American Monetary Studies (CEMLA) • Center for Marketing Information and Advisory Services for Fishery Products -

Tariq Bajwa: State Bank of Pakistan's 70Th Anniversary

Governor : Mr. Tariq Bajwa Title : SBP’s 70th Anniversary: Welcome Note by Governor SBP Date : July 01, 2018 Event : State Bank of Pakistan’s 70-year Celebration Event Venue : SBP Head Office Karachi. State Bank of Pakistan’s 70th Anniversary Welcome Note by Governor SBP Governor Sindh Mr. Zubair, Honorable Finance Minister, Dr Shamshad Akhtar, Respectable Former Governors, State Bank of Pakistan, Dr. Ishrat Husain, Mr. Yasin Anwar, Mr. Ashraf Wathra Distinguished guests, Ladies and Gentlemen, Assalam-o-aliakum and a very good morning! It is my pleasant duty and distinct privilege to welcome you all to the 70th anniversary of the establishment of State Bank of Pakistan. On the auspicious occasion of the opening of the SBP on July 1st, 1948, the Quaid said: “The opening of State Bank of Pakistan symbolizes the sovereignty of our state in the financial sphere. I need to hardly dilate on the important role the State Bank will have to play in regulating the economic life of our country. The monetary policy of the bank will have a direct bearing on our trade and commerce, both inside Pakistan as well as with the outside world and it is only to be desired that our policy should encourage maximum production and free flow of trade.” Page 1 of 4 The SBP as an institution has tried to live up to the expectations of the Quaid. From a modest beginning in borrowed premises, ladies and gentlemen, SBP rose to have earned the reputation of being a professional, progressive and forward-looking institution. The journey has been challenging, arduous, but rewarding. -

Development of Payment and Settlement System

CHAPTER 7 Development of Payment and Settlement System Khin Thida Maw This chapter should be cited as: Khin Thida Maw, 2012. “Development of Payment and Settlement System.” In Economic Reforms in Myanmar: Pathways and Prospects, edited by Hank Lim and Yasuhiro Yamada, BRC Research Report No.10, Bangkok Research Center, IDE- JETRO, Bangkok, Thailand. Chapter 7 Development of Payment and Settlement System Khin Thida Maw ______________________________________________________________________ Abstract The new government of Myanmar has proved its intention to have good relations with the international community. Being a member of ASEAN, Myanmar has to prepare the requisite measures to assist in the establishment of the ASEAN Economic Community in 2015. However, the legacy of the socialist era and the tight control on the banking system spurred people on to cash rather than the banking system for daily payment. The level of Myanmar’s banking sector development is further behind the standards of other regional banks. This paper utilizes a descriptive approach as it aims to provide the reader with an understanding of the current payment and settlement system of Myanmar’s financial sector and to recommend some policy issues for consideration. Section 1 introduces general background to the subject matter. Section 2 explains the existing domestic and international payment and settlement systems in use by Myanmar. Section 3 provides description of how the information has been collected and analyzed. Section 4 describes recent banking sector developments and points for further consideration relating to payment and settlement system. And Section 5 concludes with the suggestions and recommendation. ______________________________________________________________________ 1. Introduction Practically speaking, Myanmar’s economy was cash-based due to the prolonged decline of the banking system after nationalization beginning in the early 1960s. -

Ÿþn O T I F I C a T I O N S F R O M 0 3 M a Y T O 1 4 M a Y 2 0

TO BE PBLISHED IN THE NEXT ISSUE OF THE GAZETTE OF PAKISTAN PART I No.1/57/2012-E-2 GOVERNMENT OF PAKISTAN CABINET SECRETARIAT ESTABLISHMENT DIVISON *********** Islamabad, the 14th May, 2019 NOTIFICATION Mr. Ehsan-ul-Haq, a BS-19 officer of the Secretariat Group, presently posted as Deputy Secretary, Climate Change Division, is transferred and posted as Deputy Secretary, Maritime Affairs Division, with immediate effect and until further orders. 0-1/5"hq . (Mariam Kayani) Deputy Secretary to the Government of Pakistan The Manager, Printing Corporation of Pakistan Press, KARACHI •Copy to:- 1. The Secretary .to the Pre§ident, President's Secretariat (Public), Islamabad. 2. The Secretary to the Prime Minister, Prime Minister's Office, Islamabad. 3. The Secretary, Cabinet Division, Islamabad. 4. The Secretary, Establishment Division, Islamabad. 5. The Secretary, Maritime Affairs, Division, Islamabad. 6. The Secretary, Climate Change Division, Islamabad. 7. The A.G.P.R Islamabad. 8. The Additional Secretaries, Joint Secretaries, D.G (M.S Wing), Deputy Secretaries, Director (PD) and Sections concerned, Establishment Division, Islamabad. 9. The officer concerned with the request to furnish a copy of the charge relinquishment / assumption report to Director (PD) and Section Officer (E-2), Establishment Division, Islamabad. 10. The Estate Office, Islamabad. 11.Notification file / personal file of Officer(s). (Tah een Akbar) Section Officer (E-2) Tele # 051-9103653 Fax 14 051-9202784 TO BE PUBLISHED IN THE NEXT ISSUE OF THE GAZETTE OF PAKISTAN PART I No.1-16-2014-E-2 GOVERNMENT OF PAKISTAN CABINET SECRETARIAT ESTABLISHMENT DIVISION AAAAAA Islamabad, the 14th May, 2019 NOTIFICATION Mr. -

Introduction Establishment

ACU 1974 INTRODUCTION OBJECTIVES Secretary General settlement periods by a decision taken by unanimous vote of all of the Directors. Asian Clearing Union (ACU) is the simplest form of • To provide a facility to settle payments, on a multilateral The Board is authorized to appoint a Secretary General payment arrangements whereby the participants settle basis, for current international transactions among for a term of three years. The Secretary General may Interest payments for intra-regional transactions among the the territories of participants; be reappointed and shall cease to hold office when the Interest shall be paid by net debtors and transferred to participating central banks on a multilateral basis. The Board so decides. • To promote the use of participants’ currencies net creditors on daily outstandings between settlement main objectives of a clearing union are to facilitate in current transactions between their respective Agent dates. The rate of interest applicable for a settlement payments among member countries for eligible territories and thereby effect economies in the use period will be the closing rate on the first working day transactions, thereby economizing on the use of foreign The Board of Directors may make arrangements with of the participants’ exchange reserves; of the last week of the previous calendar month offered exchange reserves and transfer costs, as well as a central bank or monetary authority of a participant by the Bank for International Settlements (BIS) for one promoting trade among the participating countries. The • To promote monetary cooperation among the to provide the necessary services and facilities for the month US dollar and Euro deposits. -

3 Who Is Who and What Is What

3 e who is who and what is what Ever Success - General Knowledge 4 Saad Book Bank, Lahore Ever Success Revised and Updated GENERAL KNOWLEDGE Who is who? What is what? CSS, PCS, PMS, FPSC, ISSB Police, Banks, Wapda, Entry Tests and for all Competitive Exames and Interviews World Pakistan Science English Computer Geography Islamic Studies Subjectives + Objectives etc. Abbreviations Current Affair Sports + Games Ever Success - General Knowledge 5 Saad Book Bank, Lahore © ALL RIGHTS RESERVED No part of this book may be reproduced In any form, by photostate, electronic or mechanical, or any other means without the written permission of author and publisher. Composed By Muhammad Tahsin Ever Success - General Knowledge 6 Saad Book Bank, Lahore Dedicated To ME Ever Success - General Knowledge 7 Saad Book Bank, Lahore Ever Success - General Knowledge 8 Saad Book Bank, Lahore P R E F A C E I offer my services for designing this strategy of success. The material is evidence of my claim, which I had collected from various resources. I have written this book with an aim in my mind. I am sure this book will prove to be an invaluable asset for learners. I have tried my best to include all those topics which are important for all competitive exams and interviews. No book can be claimed as prefect except Holy Quran. So if you found any shortcoming or mistake, you should inform me, according to your suggestions, improvements will be made in next edition. The author would like to thank all readers and who gave me their valuable suggestions for the completion of this book. -

List of Category -I Members Registered in Membership Drive-Ii

LIST OF CATEGORY -I MEMBERS REGISTERED IN MEMBERSHIP DRIVE-II MEMBERSHIP CGN QUOTA CATEGORY NAME DOB BPS CNIC DESIGNATION PARENT OFFICE DATE MR. DAUD AHMAD OIL AND GAS DEVELOPMENT COMPANY 36772 AUTONOMOUS I 25-May-15 BUTT 01-Apr-56 20 3520279770503 MANAGER LIMITD MR. MUHAMMAD 38295 AUTONOMOUS I 26-Feb-16 SAGHIR 01-Apr-56 20 6110156993503 MANAGER SOP OIL AND GAS DEVELOPMENT CO LTD MR. MALIK 30647 AUTONOMOUS I 22-Jan-16 MUHAMMAD RAEES 01-Apr-57 20 3740518930267 DEPUTY CHIEF MANAGER DESTO DY CHEIF ENGINEER CO- PAKISTAN ATOMIC ENERGY 7543 AUTONOMOUS I 17-Apr-15 MR. SHAUKAT ALI 01-Apr-57 20 6110119081647 ORDINATOR COMMISSION 37349 AUTONOMOUS I 29-Jan-16 MR. ZAFAR IQBAL 01-Apr-58 20 3520222355873 ADD DIREC GENERAL WAPDA MR. MUHAMMA JAVED PAKISTAN BORDCASTING CORPORATION 88713 AUTONOMOUS I 14-Apr-17 KHAN JADOON 01-Apr-59 20 611011917875 CONTRALLER NCAC ISLAMABAD MR. SAIF UR REHMAN 3032 AUTONOMOUS I 07-Jul-15 KHAN 01-Apr-59 20 6110170172167 DIRECTOR GENRAL OVERS PAKISTAN FOUNDATION MR. MUHAMMAD 83637 AUTONOMOUS I 13-May-16 MASOOD UL HASAN 01-Apr-59 20 6110163877113 CHIEF SCIENTIST PROFESSOR PAKISTAN ATOMIC ENERGY COMMISION 60681 AUTONOMOUS I 08-Jun-15 MR. LIAQAT ALI DOLLA 01-Apr-59 20 3520225951143 ADDITIONAL REGISTRAR SECURITY EXCHENGE COMMISSION MR. MUHAMMAD CHIEF ENGINEER / PAKISTAN ATOMIC ENERGY 41706 AUTONOMOUS I 01-Feb-16 LATIF 01-Apr-59 21 6110120193443 DERECTOR TRAINING COMMISSION MR. MUHAMMAD 43584 AUTONOMOUS I 16-Jun-15 JAVED 01-Apr-59 20 3820112585605 DEPUTY CHIEF ENGINEER PAEC WASO MR. SAGHIR UL 36453 AUTONOMOUS I 23-May-15 HASSAN KHAN 01-Apr-59 21 3520227479165 SENOR GENERAL MANAGER M/O PETROLEUM ISLAMABAD MR. -

SBP Celebrates Seven Decades of Professional Excellence Page No.01 Col No.01

SBP celebrates seven decades of professional excellence Page No.01 Col No.01 RECORDER REPORT KARACHI: State Bank of Pakistan (SBP) celebrated its 70th anniversary on Sunday July 1, 2018 with a number of programs taking place simultaneously at the SBP in Karachi. These activities were aimed at sharing the history of SBP and bridging the information gap on various functions and achievements of SBP and its subsidiaries. The programs were attended by a cross section of society, particularly school children. The Bank (SBP) organized an insightful panel discussion on this historical occasion covering a wide variety of topics, including macroeconomic management, SBP’s conduct of monetary policy and its role in promotion of credit extension to priority areas and use of digital innovations and technology in providing banking services. In this discussion, current as well as previous SBP governors including Tariq Bajwa, caretaker Finance Minister w Dr. Shamshad Akhtar who also served as SBP governor, Dr. Ishrat Husain, Yaseen Anwar and Ashraf Mahmood Wathra, also participated. The participants shared their thoughts and candid views on their experiences and future vision for the Bank and congratulated executives and staff for achieving several milestones in its journey throughout past seven decades. SBP Governor Tariq Bajwa in his concluding remarks stated that the SBP had always strived to living up to expectations of Quaid-e-Azam (founder of Pakistan) pertaining to professionalism and forward-looking approach in discharging its mandate. A special documentary focusing on the history of the SBP was also screened during the seminar that portrayed challenges confronted by the Bank right after its inception, and its subsequent journey towards professional excellence. -

PM Meets Haroon Akhtar, Discusses Overall Economy, Tax Revenue

11th February, 2020 Mehtab Haider PM meets Haroon Akhtar, discusses overall economy, tax revenue ISLAMABAD: In an interesting development, Prime Minister Imran Khan on Monday listened to the views of former Special Assistant to PM on Revenue of the last PML-N government, Haroon Akhtar Khan, on the overall economy and tax revenues during a meeting of the economic team held at the PM Secretariat. Haroon Akhtar Khan was among the special invitees of the meeting held with the economic team under the chairmanship of Prime Minister Imran Khan. Haroon Akhtar Khan might be offered the position of Adviser to Prime Minister on Revenue anytime soon with the possibility to appoint the new chairman FBR of his choice, said sources. There are different names under consideration for the slot of chairman FBR including Tariq Pasha, Mujtaba Memon, Jehanzeb Khan, Nausheen Javed and Javed Ghani. With the latest development, Tariq Pasha is considered among the top contenders of this top position within the ranks of FBR. Pasha is going to reach the age of superannuation very soon, so if the government decides his name, he might be given a contract for three years period. Jehanzeb Khan, who is currently serving as Deputy Chairman Planning Commission, is in the race and he will also be retiring in coming August 2020. It is also a fact that Adviser to PM on Finance Dr Abdul Hafeez Shaikh wants to see Mujtaba Memon as the new chairman FBR but with the possibility of induction of new adviser to PM on revenue, his powers on the revenue front will be taken away from him. -

Financial Sector: Performance Overview

FEDERAL FOOTPRINT n STATE OWNED ENTITIES (SOEs) Public Disclosure Authorized PERFORMANCE REVIEW FY2014-15 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized FEDERAL FOOTPRINT: STATE OWNED ENTITIES PERFORMANCE OVERVIEW FY 2014-15 TABLE OF CONTENTS List of Abbreviations .............................................................................................................. ii List of Tables .......................................................................................................................... iii DASHBOARD ........................................................................................................................ iv EXECUTIVE SUMMARY .................................................................................................... 1 INTRODUCTION .................................................................................................................. 4 Assumptions and Limitations:....................................................................................................... ..6 SECTION I: STATE OWNED ENTITIES MAPPING ...................................................... 8 A. Categorical Classification ....................................................................................................... 9 B. Administrative Classification ............................................................................................... 14 C. Sectoral Classification .......................................................................................................... -

ADB Review: News from the ADB Pakistan Resident Mission

Pakistan Resident Mission January 2020 New ADB President Masatsugu Asakawa Assumes Office "I am honored to assume the role of ADB in Fukuoka, Japan. Furthermore, in the President and to begin working in close immediate aftermath of the Global Financial cooperation with our 68 members. ADB has Crisis, he took part in the rst G20 Leaders’ been a trusted partner of the region for more Summit Meeting in his capacity as Executive than half a century, supporting strong growth that Assistant to the then Prime Minister Taro Aso. has improved the lives of people across Asia and Mr. Asakawa has had frequent engagement with the Pacic. I will strive to ensure ADB remains the Organisation for Economic Co-operation the preferred choice of its clients and partners," and Development, including as Chair of the Mr. Asakawa said. Committee on Fiscal Affairs from 2011 to 2016. Mr. Asakawa succeeds Mr. Takehiko Mr. Asakawa’s extensive international Nakao, who stepped down on 16 January 2020. experience includes service as Chief Advisor to In a career spanning close to four decades, ADB President Mr. Kimimasa Tarumizu between Mr. Asakawa has held a range of senior positions 1989 and 1992, during which he spearheaded at the Ministry of Finance of Japan, including Vice the creation of a new ofce in ADB focused on Minister of Finance for International Affairs, and strategic planning. gained diverse professional experience in Mr. Asakawa served as a Visiting Professor development policy, foreign exchange markets, at the University of Tokyo from 2012 to 2015 Masatsugu Asakawa assumes ofce as the and international tax policy. -

Toward a More Universal Currency: the Impact of the Clearing Mechanism on Developing Economies

State University of New York College at Buffalo - Buffalo State College Digital Commons at Buffalo State Applied Economics Theses Economics and Finance 5-2019 Toward a More Universal Currency: The mpI act of the Clearing Mechanism on Developing Economies Evan Ross Kaderbeck State University of New York College at Buffalo - Buffalo State College, [email protected] Advisor Dr. Ted Schmidt First Reader Dr. Ted Schmidt Second Reader Dr. Frederick Floss Third Reader Dr. Joelle LeClaire Department Chair Dr. Frederick Floss To learn more about the Economics and Finance Department and its educational programs, research, and resources, go to https://economics.buffalostate.edu/. Recommended Citation Kaderbeck, Evan Ross, "Toward a More Universal Currency: The mpI act of the Clearing Mechanism on Developing Economies" (2019). Applied Economics Theses. 40. https://digitalcommons.buffalostate.edu/economics_theses/40 Follow this and additional works at: https://digitalcommons.buffalostate.edu/economics_theses Part of the Finance Commons, and the International Economics Commons Toward a More Universal Currency: The Impact of the Clearing Mechanism on Developing Economies by Evan Kaderbeck An Abstract of a Thesis in Applied Economics Submitted in Partial Fulfillment Of the Requirements For the Degree of Master of Arts May 2019 Buffalo State College State University of New York Department of Economics and Finance ii ABSTRACT OF THESIS Toward a More Universal Currency: The Impact of the Clearing Mechanism on Developing Economies As part of a broader plan to reform the system of international finance, experts have indicated the need to modify the system of international money. They point to problems such as the difficulties faced by developing countries in obtaining hard currency needed for imports, or the flows of hot money which make the financing of long-term development projects difficult.